A few weeks ago there was the debacle of the government introducing one afternoon a bill that would have imposed GST on investment management fees, ministers defending that bill the next morning, but then by lunchtime the policy was gone.

The proposed law change seemed on the face of it perfectly sensible in principle. I even read the Regulatory Impact Statement that was published with the bill, and most of the reasoning and argumentation made sense there too.

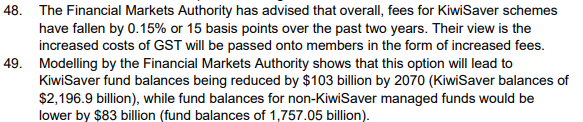

But it contained this little section

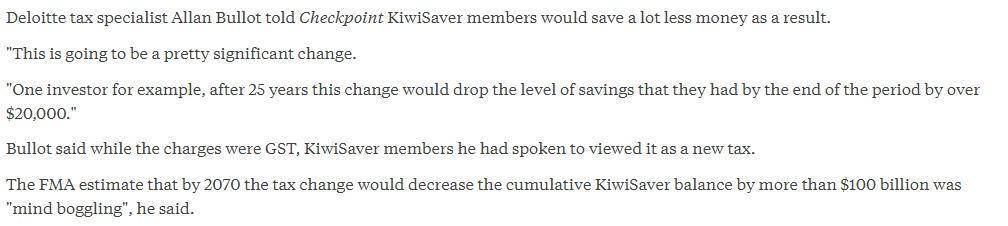

Perhaps unsurprisingly, those big numbers got a fair amount of media and political attention. As an example, here was an RNZ story

I was a bit curious about this “modelling”, which was not published at the time the bill was introduced. It wasn’t described in the RIS, the numbers weren’t put in any sort of context, they were just baldly stated. Quite probably ministers don’t read RISs, but perhaps you might think that the political advisers in their offices would (looking for fishhooks and headlines if nothing else). And you might have hoped that officials (Treasury/IRD) might have done a bit more than drop big numbers into the RIS – numbers that might reasonably be seen as creating problems for a sensible rational tax reform – rather than just stick the numbers out there waiting for the first curious journalist or Opposition MP to find them.

My suspicion was that something very simple, and potentially quite misleading, had been done. After all, one wouldn’t normally look to the FMA to undertake any serious modelling (it is a regulatory implementation agency). So I lodged a request for the modelling, and got a reply back this afternoon.

It is a helpful reply. They have set out their assumptions clearly, and even offered that I could talk to the responsible senior manager if I wanted to discuss matters further.

And it was pretty much as I had expected. They had assumed (probably reasonably enough [UPDATE; but see below]) that all of any GST burden would be passed on to customers/investors, and thus that overall returns would be a bit lower. But then they simply assumed that all the additional tax went to the government, which sat on it, and neither the government nor the savers made any subsequent changes in behaviour……..over the subsequent 50 years. And thus, mechanically, future managed fund balances would be lower than otherwise (about 4.5 per cent lower)

It might be a reasonable approximate assumption for a first year effect. Just possibly it might even be valid for the KiwiSaver component, since KiwiSaver contributions are largely salary-linked. But it makes no sense over a 50 year horizon, across all managed funds (let alone all private savings) and especially as the only macro-like number to appear in the entire document.

Over a 50 year view surely it would be reasonable to assume that one modest tax change makes no difference to the fiscal outlook, and thus that what is raised with this tax won’t be raised by some other tax. Household income won’t really be changed, and since most of the evidence tends to be that household savings rates in aggregate aren’t very sensitive to rates of return (partly because there are conflicting effects – low rates of return on their own might discourage saving, but on the other hand people with a target level of accumulated savings in mind for retirement will need to save a bit more when returns are lower than they had previously assumed) neither will the overall rate of household saving. There is more sensitivity (to return) on the particular instrument people choose to put their savings in, so that if returns on investment management products are a little lower than otherwise, people might prefer, at the margin, to hold a bit more of some other assets. But what of it? Supporting investment management firms’ businesses is no part of a sensible government’s set of goals.

Surely the best assessment would have been that over anything like a 50 year view, a small tax change like this, affecting returns on one form of savings product, simply would not be expected to make any material difference to accumulated household wealth in 2070, with perhaps some slight change in the composition of household asset portfolios: a little less Kiwisaver, not much change in other investment management products, and a little more in other instruments.

The FMA were at pains to point out that they “had limited time to feedback to IRD as part of IRD’s policy consultation”, although it isn’t clear whether IRD/Treasury requested these numbers or the FMA took it upon themselves to do it. And thus in a way I don’t much blame the FMA. They tend to be enthusiasts for and champions of KiwiSaver, and simply do not have a whole-economy remit or set of expertise.

What disconcerts me is that neither IRD nor Treasury (the latter especially) seem to have been bothered by FMA’s numbers, and neither seems to have made any effort to provide any context or interpretation. There wasn’t any obvious reason why those FMA numbers had to be in the RIS, but if they had put them in with a rider “On the (unlikely) assumption that governments simply accumulate the additional tax revenue for 50 years and neither they nor households make any other changes in behaviour, then FMA ‘modelling’ suggests……”, it might have done materially less damage, through highlighting the sheer implausibility of the assumptions over a 50 year horizon.

Of course, you might also have hoped that ministers and their political staff would have noticed that something seemed odd.

What was proposed still seems as though it would have been a sensible tax change. Perhaps it will even happen one day. Perhaps it would have been derailed anyway, even if those FMA numbers – unqualified – had never made it into the document. But neither ministers nor officials really seem to have helped themselves.

UPDATE

A reader got in touch and suggested I might have been too generous in accepting the FMA view that all the GST would have been passed on to customers. With that reader’s permission, here are his comments

“Having owned a fund manager as part of a wider business, the GST exemption was a pain. We could not recover GST on certain inputs and so therefore had to charge more – about 7.5% more because of this. Plus we had an extra employee in the finance area that we could have got rid of. It is not obvious to me that the fees would have gone up for this reason at all, except that the industry would probably have used it as an excuse to raise fees as it means that at some future point they could cut them and get a pat on the back from the FMA.”

I agree – we deserve better. Had to admire David Seymour as he came out in defense of the intention to treat all products in a similar manner for GST purposes. In other words, he “got it” better (it seems) than the Minister(s) unable to rationally defend it.

But yeah, that headline number was what sunk the ship – and yeah, TSY in particular should have seen the media use of those headline numbers coming like a train wreck out-of-the-blue at their Ministers.

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

Unfortunately, New Zealanders picked the worst performing and most corrupt Jacinda Ardern Labour government ever.

LikeLike