The Listener magazine this week reported the results of a caption contest they’d run for a photo of Reserve Bank Governor Adrian Orr.

I’d suggested what seemed to me a rather more apt caption.

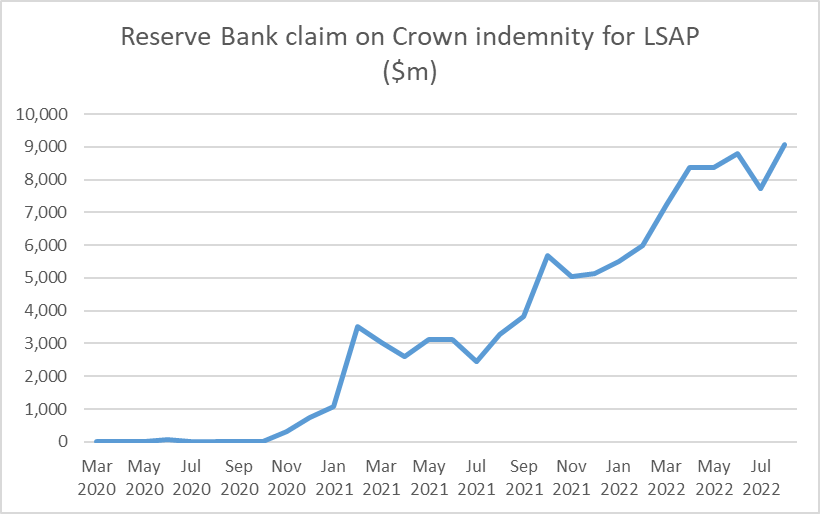

One good thing about the Reserve Bank is that they do report their balance sheet in some detail every month, and yesterday they released the numbers for the end of August. August was not a good month for the government bond market: yields rose further and the market value of anyone’s bond holdings fell. And thus the Reserve Bank’s claim on the government, under the indemnity the Minister of Finance provided them in respect of the LSAP programme, mounted.

This is the line item from the balance sheet

A new record high at just over $9bn.

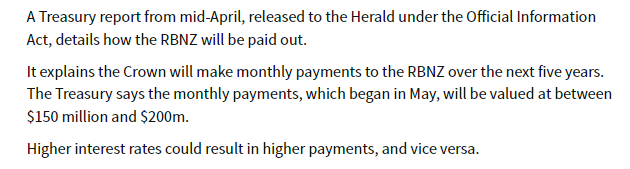

And that doesn’t seem to be quite the full extent of the losses the Governor and the MPC have caused. A while ago the Herald reported on an OIAed document from The Treasury.

I wasn’t sure quite what to make of that, but we know that from July the Bank has begun selling its bonds back to The Treasury. Over July and August they had sold back $830m of the longest-dated bonds (ie the ones on which the losses will have been largest) and presumably collected on the indemnity when the Bank realised the losses on those bonds at point of sale.

Presumably all the numbers will eventually turn up in the Crown accounts, but for now it seems safe to assume that Orr and his colleagues (facilitated by the Minister of Finance) have cost taxpayers around $9.5 billion dollars – getting on for 2.5% of New Zealand’s annual GDP (or about 7 per cent of this year’s government spending).

These are really huge losses, and to now the Governor’s defence seems to amount to little more than “trust us, we knew what we were doing”, accompanied by vague claims that he is confident that the economic benefits were “multiples” of the costs. But there is no contemporary documentation in support of the former claim (eg a proper risk analysis rigorously examined and reviewed before they launched into this huge punt with our money), and nothing at all yet in support of the latter claim.

Central banks should be (modest) profit centres for the Crown. Between their positions as monopoly issuers of zero-interest notes and coins and as residual liquidity supplier to the financial system there is never a good excuse for a central bank to lose money, and certainly not on the scale we’ve seen here (and in other countries) in the last couple of years – punting massively on an implicit view that bond yields would never go up much or for long (as they hadn’t much in the previous decade when other central banks were engaging in QE).

There are plenty of things governments waste money on, and plenty of big programmes that (rightly) command widespread support (through Covid you could think of the wage subsidy scheme). But this was just little more than a coin toss – low expected value, but with at least as high a chance of big losses as of any substantial gains. And seemingly with no accountability whatever. Orr has not apologised for the losses, nor have the other MPC members. No one has lost their job – but then this is the New Zealand public sector where hardly anyone ever does – and not a word has been heard from those charged with holding the Bank to account (the Board or the Minister of Finance).

Back when I was young the Bank ran up big (indemnified) foreign exchange losses in the 1984 devaluation episode. Searching through old papers I can’t find the precise number the Crown had to pay out, but between what I could find and my memory it may well have been of a similar order (share of GDP) as the LSAP losses. But the responsibility then rested directly with the Minister of Finance – the Bank was not operationally independent, and defending the fixed exchange rate under pressure was government policy. It was a rash policy – the Bank advised the government not to do it – and the large losses added to the obloquy heaped on Muldoon for his stewardship in his last couple of years on office. But the public got to vote Muldoon out, while there still appears to be a serious possibility that Orr – having cost New Zealanders perhaps $1800 each – will be reappointed (with just six months of his term to go if he is not going to be reappointed it will need to be announced soon to enable a proper search process for a replacement to occur). The LSAP losses may not even be the Governor’s worst failing, but no one directly responsible for that scale of taxpayer losses – on risks he simply did not have to take – should even be considered for reappointment, at least if accountability is to mean anything ever.

Of course, there have been bigger losses in New Zealand government history. I’ve just been reading John Boshier’s Power Surge on the Think Big debacle of the 1980s. As a share of GDP, total economic losses to the taxpayer from that series of projects were far greater than the LSAP losses, but I’m not sure that losing less in one punt than the worst series of discretionary public sector projects ever in New Zealand history should be any consolation or mitigation. And, for what it is worth, Boshier’s book suggests there was typically more advance risk analysis undertaken for the Think Big projects than we have yet seen evidence of for the LSAP.

I’m sure gambling appeals to some people, and I wouldn’t want to stop those minded punting on the bond market, the fx market, Bitcoin, equities or whatever. But if that is the sort of thing that takes Orr’s fancy – and it probably isn’t judging by his past financial disclosures – he could at least do it with his own money, not ours. And having rashly done it with our money, and lost heavily, have the decency to apologise.