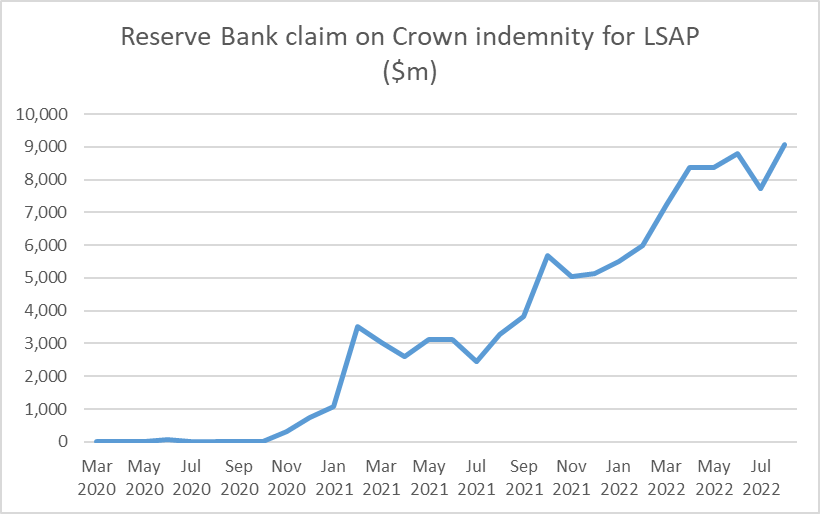

One good thing about the Reserve Bank is that they do report their balance sheet in some detail every month, and yesterday they released the numbers for the end of August. August was not a good month for the government bond market: yields rose further and the market value of anyone’s bond holdings fell. And thus the Reserve Bank’s claim on the government, under the indemnity the Minister of Finance provided them in respect of the LSAP programme, mounted.

This is the line item from the balance sheet

A new record high at just over $9bn.

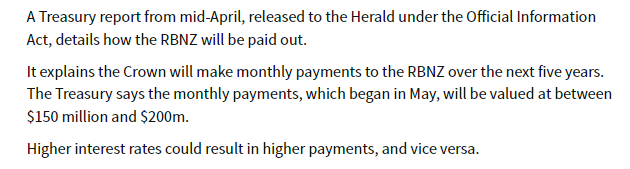

And that doesn’t seem to be quite the full extent of the losses the Governor and the MPC have caused. A while ago the Heraldreported on an OIAed document from The Treasury.

I wasn’t sure quite what to make of that, but we know that from July the Bank has begun selling its bonds back to The Treasury. Over July and August they had sold back $830m of the longest-dated bonds (ie the ones on which the losses will have been largest) and presumably collected on the indemnity when the Bank realised the losses on those bonds at point of sale.

Presumably all the numbers will eventually turn up in the Crown accounts, but for now it seems safe to assume that Orr and his colleagues (facilitated by the Minister of Finance) have cost taxpayers around $9.5 billion dollars – getting on for 2.5% of New Zealand’s annual GDP (or about 7 per cent of this year’s government spending).

These are really huge losses, and to now the Governor’s defence seems to amount to little more than “trust us, we knew what we were doing”, accompanied by vague claims that he is confident that the economic benefits were “multiples” of the costs. But there is no contemporary documentation in support of the former claim (eg a proper risk analysis rigorously examined and reviewed before they launched into this huge punt with our money), and nothing at all yet in support of the latter claim.

Central banks should be (modest) profit centres for the Crown. Between their positions as monopoly issuers of zero-interest notes and coins and as residual liquidity supplier to the financial system there is never a good excuse for a central bank to lose money, and certainly not on the scale we’ve seen here (and in other countries) in the last couple of years – punting massively on an implicit view that bond yields would never go up much or for long (as they hadn’t much in the previous decade when other central banks were engaging in QE).

There are plenty of things governments waste money on, and plenty of big programmes that (rightly) command widespread support (through Covid you could think of the wage subsidy scheme). But this was just little more than a coin toss – low expected value, but with at least as high a chance of big losses as of any substantial gains. And seemingly with no accountability whatever. Orr has not apologised for the losses, nor have the other MPC members. No one has lost their job – but then this is the New Zealand public sector where hardly anyone ever does – and not a word has been heard from those charged with holding the Bank to account (the Board or the Minister of Finance).

Back when I was young the Bank ran up big (indemnified) foreign exchange losses in the 1984 devaluation episode. Searching through old papers I can’t find the precise number the Crown had to pay out, but between what I could find and my memory it may well have been of a similar order (share of GDP) as the LSAP losses. But the responsibility then rested directly with the Minister of Finance – the Bank was not operationally independent, and defending the fixed exchange rate under pressure was government policy. It was a rash policy – the Bank advised the government not to do it – and the large losses added to the obloquy heaped on Muldoon for his stewardship in his last couple of years on office. But the public got to vote Muldoon out, while there still appears to be a serious possibility that Orr – having cost New Zealanders perhaps $1800 each – will be reappointed (with just six months of his term to go if he is not going to be reappointed it will need to be announced soon to enable a proper search process for a replacement to occur). The LSAP losses may not even be the Governor’s worst failing, but no one directly responsible for that scale of taxpayer losses – on risks he simply did not have to take – should even be considered for reappointment, at least if accountability is to mean anything ever.

Of course, there have been bigger losses in New Zealand government history. I’ve just been reading John Boshier’s Power Surge on the Think Big debacle of the 1980s. As a share of GDP, total economic losses to the taxpayer from that series of projects were far greater than the LSAP losses, but I’m not sure that losing less in one punt than the worst series of discretionary public sector projects ever in New Zealand history should be any consolation or mitigation. And, for what it is worth, Boshier’s book suggests there was typically more advance risk analysis undertaken for the Think Big projects than we have yet seen evidence of for the LSAP.

I’m sure gambling appeals to some people, and I wouldn’t want to stop those minded punting on the bond market, the fx market, Bitcoin, equities or whatever. But if that is the sort of thing that takes Orr’s fancy – and it probably isn’t judging by his past financial disclosures – he could at least do it with his own money, not ours. And having rashly done it with our money, and lost heavily, have the decency to apologise.

Ever since I’ve been writing about house prices – more or less the life of this blog – one of the things that has struck (and sobered) me is that I do not know of (and no one has ever been able to point me to) an example of a country or even a region that having once messed up its housing and urban land regulation, generating absurdly high house price to income ratios has undone things and returned to sustainably low price to income ratios (perhaps fluctuating around three times). There are, of course, many places in the United States where price to income ratios never went crazy. But never having dug a deep hole is a different matter than getting out of one once dug. One reads occasionally – even briefly on this blog – of how easy it is to build in Tokyo (and a culture of frequent demolition and rebuild), but no one ever suggests that Tokyo price to income ratios are low (just much lower than they were a few decades ago at the peak of the 1980s boom).

A month or two back I saw reference somewhere to Arbitrary Lines: How Zoning Broke the American City and How to Fix It, a new book by an American “professional city planner” Nolan Gray. Last week it turned up in the mail, and being neither very long nor very technical I’ve now read it.

Gray offers a pretty useful introduction to how zoning came to be in the United States (complete, as usual, with various Supreme Court cases), and if much of that isn’t very directly relevant to New Zealand I found it interesting nonetheless. And, of course, some of the best-known restrictions in many areas of the United States – single family dwelling zoning, to the complete exclusion of any other uses for the land (whether two single-storey townhouses, or a corner dairy, or a hairdresser’s), isn’t (and hasn’t really been) a widespread thing in urban New Zealand.

And there is some useful material on some of the potential wider costs to restrictive land use, although on my reading of the relevant papers Grey often jumps too readily to assert causal relationships. But then his background is planning (and is currently studying for a PhD in urban planning) and in some respects the book is best seen as an evangelistic tract (they have their place). No doubt it would appeal quite strongly to that small but vocal group of New Zealand reformers who dream of demolishing whole suburbs, long for light rail systems, and really dislike the idea of backyards (and increasing physical footprints of cities). They often dislike cars too. And often don’t seem too keen on – quite derisive of – people not like them.

And thus as the book went on I was finding it more than a little annoying in places. Gray makes many good points about the inadequacies (and worse) of US zoning systems. But it was pretty clear that he had one particular urban form in mind, and whole agenda of other issues he (and his publisher – explicitly focused on “solving environmental problems”) cared about. And, perhaps reflecting that, there was very little in the book about house prices themselves or the likelihood that his solutions would materially lower them. But there was quite a lot on emissions and energy use (which could simply be priced, as they now largely are in New Zealand), and a dislike of turning farmland (or any other undeveloped land) into suburbs (where, again, any externalities can and should be priced). He seems to have been living in Washington DC when he wrote the book, and enjoying that: we enjoyed our time living in a DC apartment too.

It was also getting frustrating that despite writing about a country that has quite diverse systems, for a long time there was almost no mention of the vast swathes of the United States with (a) population growth, and (b) low and fairly stable house prices.

Until, three-quarters of the way through the book, I came to the chapter headed “The Great Unzoned City”, about Houston. I wouldn’t be bothering with this post if Gray had simply been making the point that real house prices are pretty low, and fluctuate around a fairly stable trend, in Houston. There are, after all, many cities in the annual Demographia tables that are cheaper still. There isn’t that much zoning in Houston, and people have written previously about Municipal Urban Districts (MUDs) which enable land – outside established urban local government boundaries – to be readily developed by private developers, including dealing directly with (internalising) the associated infrastructure costs of development. It was nice to see his, perhaps grudging, recognition that (a) everyone drives in Houston, and b) people are moving to places such as it with cheaper housing. It works. And there has been considerable intensification in Houston over the years.

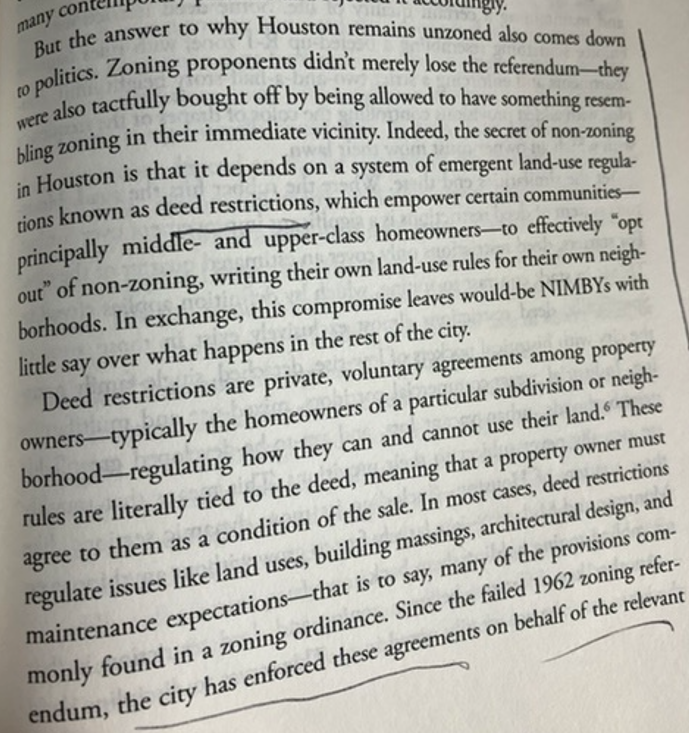

But the real thing I learned about – and the point of the post – was about the Houston system of Deed Restrictions.

Again, as long as I’ve been writing about housing and possible reform options for New Zealand, I have been intrigued (starting here I think) by the idea of allowing small groups of landowners in existing urban areas (perhaps at the scale of a city block or a small neighbourhood) to set collectively their own land-use rules for their own group of properties. They are an established market mechanisms in new developments in New Zealand, in the form of private covenants, and one could mount an argument that zoning was really an attempt to do much the same thing (collectively manage shared interests, where there are real externalities).

In a report some years ago, the Productivity Commission took a very dim view of private covenants, even suggesting that the government should legislate to restrict their use. But they’ve always seemed to me to be a way through the endless battles (eg the Christchurch City Council stories this morning) around land use, at least among those willing to operate in good faith (and it is never clear how many are). Why not, for example, remove all government restrictions on land use for housing (height, setback, site coverage, “character”, parking or whatever) in existing urban areas AND on undeveloped land, while allowing neighbourhoods/blocks (groups of existing property owners) to adopt by super-majority (and be able to amend by the same super-majority) previous restrictions as applicable to their land, and their land only?

Over the years, I’ve seen a few other people make similar suggestions (eg there was a UK think tank piece a year or two back) but it had about it perhaps an obscure textbook-y feel. It wasn’t clear that anyone had tried it ever, and I myself am inclined to invoke revealed preference arguments at times (if something doesn’t exist anywhere, it is worth at least thinking about whether there is a good – well-grounded, not just political – reason for that).

But it seems that in Houston they have done something very like what I’ve suggested, and it has been in place long enough to see how it works. It is a big, growing, city with pretty-affordable house prices (I’ve been looking recently at small modern units in Christchurch recently – NZ’s least unaffordable city of any size – and it is simply depressing (although also a reminder of what we could do) to check in from time to time and see what one gets for the same money, in a higher wage country, in Houston).

There have been attempts over the years to put in place more extensive zoning systems in Houston. They have failed, at several referenda. But here is Grey:

It is easy to develop on the margins of Houston, it is fairly easy to develop in much of the existing city, but those individual groups of landowners who want to have collective rules for their own properties can do so, and the local authority will enforce those rules on those properties. Deed restrictions are not set in stone for ever, but appear to be often time-limited and requiring a further (super-majority) vote of the then owners (a different group than 25 years earlier typically) at expiry to renew them.

It seems like a model that has a lot to offer here, and which should be looked at more closely by (a) officials, and (b) political parties exploring the best durable way ahead for New Zealand.

Those not operating in good faith – or at least much more interested in other agendas than a) widely affordable housing, and b) property rights (individual and collective) – would no doubt hate it. And, for the moment, they have the momentum – National and Labour last year rushed through legislation that stripped away many existing restrictions, and as a technical matter the government can if it likes force individual city councils to do as it insists. But governments can lose elections too, and if we are serious about much lower sustainable real house prices – and it isn’t clear how many central or local government figures are – we need durable models. The Houston model has proved to work, both in managing the politics and in delivering a city with widely affordable housing, and a wide range of available housing types. And if greenfields development is once again made easy – as distinct from say Wellington where the regional council is currently trying to make it even harder – urban and suburban land prices would fall a lot, and stay down.

One of the arguments some mount for over-riding local community preferences is that “people have to live somewhere”, suggesting that it is unacceptable (even “selfish”) for existing landowners (acting collectively) to protect their own interests and preferences for their own land. But that argument rests only on then unspoken earlier clause “because we will make it increasingly difficult to increase the physical footprint on cities”. Allow easy development, of all types (internalising relevant costs), and there is just no reason to ride roughshod over the collective interests of existing groups of landowners, providing they can restrict things only for their own group of properties.

Some might push back and argue that there is nothing to stop groups of landowners forming private covenants now on existing properties, and I gather that is legally so. But coordination issues and transactions costs are likely to be very high, and people seek to use political channels instead. How much better if we provided a tailor-made readily enforceable collective action model, and then got politicians right out of the business of deciding what sort of houses can be built where.

And, to be clear, as someone living at the end of a hillside cul-de-sac I would have no interest in a Deed Restriction for our property. My interest is ending the evil that is Wellington price to income ratios of 8x or more, and enabling ready affordability for the next generation.

The Herald’s Jenée Tibshraeny had a follow-up piece this morning on the Reserve Bank Board, with some interesting new information and (what appears to be) some ministerial spin and simply avoiding straight answers.

First we learn that Byron Pepper, appointed to the Board in late June, has now stepped down from his position as a director of an insurance company (Ando) that – by the vagaries of the details of the insurance legislation – is not an institution regulated by the Reserve Bank but is nonetheless substantially owned by another insurance company which is regulated, and which provides insurance on behalf of that regulated company. Again, it wasn’t illegal for Pepper to have held those two roles simultaneously, but it was quite improper, and it reflects poorly on him, on The Treasury (which made the appointment recommendations), on the Bank (Governor and key Board members), and on the Minister of Finance that it was ever allowed to happen. Reading again through the OIA papers I got back from Robertson the other day, it appears that Rodger FInlay was on the interview panel……so perhaps we should be less surprised. It is as if they have no sense of ethics, or of conflicts of interest in any sense other than the narrowly legal.

We don’t know whether Pepper jumped (volunteered himself to step down from Ando having thought again and realised it was a very bad look for an honourable person) or was belatedly pushed (by the Minister of Finance, Orr/Quigley, or The Treasury). My money would probably be on the Minister and the Beehive but if the conflict should never have been allowed to have arisen, at least it has been sorted out.

The sheer spin comes regarding Finlay.

Here is the timeline we know:

back in May 2021, Finlay put himself forward for appointment to the Reserve Bank Board (that is when positions for the Transition Board and the real thing were advertised). He was chair of NZ Post then, it owned a majority of Kiwibank then. From the documents Robertson released, we know he then signed a conflict of interest declaration stating “I can confirm that at the time of any Reserve Bank appointment I would not have any relevant conflicts of interest”.

In October 2021 Cabinet agreed to appoint him to the full Reserve Bank Board from 1 July 2022, and noted that the Minister had appointed him to the “Transition Board” (formally, as a consultant to the Reserve Bank during the establishment period prior to 1 July 2022).

No political parties raised any objections when they were consulted, as the new law required for Board appointments.

During the period of the Transition Board, Finlay was participating regularly in meetings of the then Reserve Bank Board.

On 8 June 2022, Cabinet’s Appointments and Honours Committee considered a paper recommending Finlay’s reappointment from 1 July 2022 as chair of NZ Post

On 10 June I wrote a post describing as “highly inappropriate” Finlay being both a board member of the prudential regulatory authority and the chair of the majority owner of Kiwibank, 5th largest bank in the country.

On 13 June, Cabinet approved the reappointment of Finlay as chair of NZ Post from 1 July 2022.

On 13 June, according to her piece, this morning, Tibshraeny asked Robertson’s office whether Finlay’s NZ Post terms would end on 30 June 2022 (which the existing term did). Her earlier reporting suggested she had been told – either by Robertson’s office or NZ Post – that FInlay’s term was ending on 30 June. (Those messages, highly misleading as it turns out, somewhat allayed her concerns at the time, and mine.)

On 21 June, Tibshraeny’s first article on the issue appeared.

On the same day there is a substantive email (reproduced in my previous post) from a ministerial adviser noting media concerns,and noting what were (at very least) process weaknesses, while also noting (it seems) that it had been hoped that the Kiwibank ownership restructuring would have been sorted out and that any conflict would have gone away.

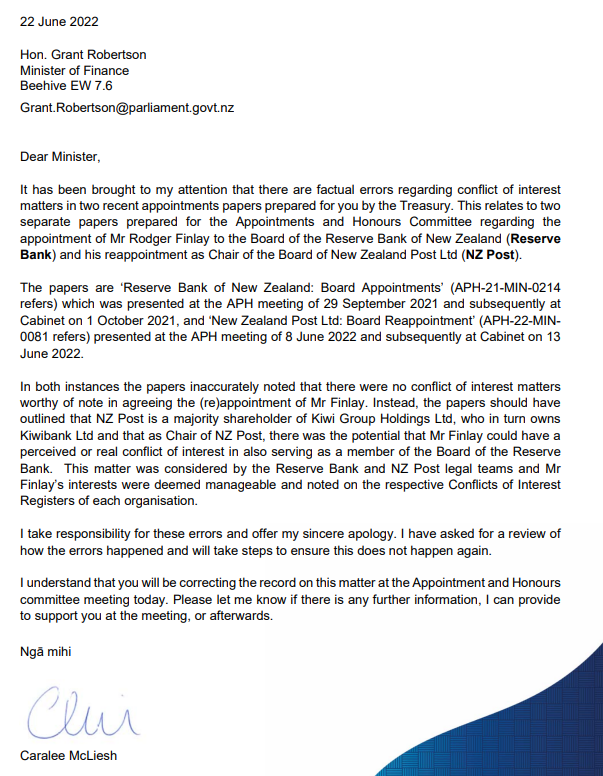

On 22 June, there is a letter (again reproduced in my previous post) from the Secretary to the Treasury to the Minister of Finance apologising that nothing about the actual/potential conflict of interest had been drawn to the attention of ministers either when Finlay was appointed to the Bank role (last year) or when reappointed to the NZ Post role (a week earlier). There is no hint in that letter that the Finlay NZ Post appointment was not proceeding, McLiesh simply noting that she understood the Minister would provide the relevant information at APH that same day.

By 1 July, Finlay was no longer showing as Board chair on the NZ Post website.

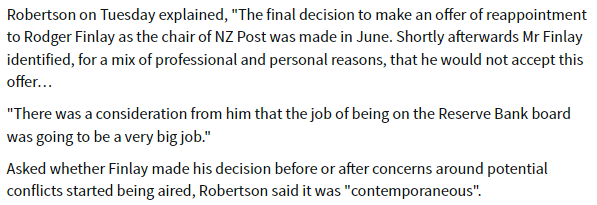

In Tibshraeny’s article she reports these comments from Grant Robertson

No thinking person should take this as a serious response.

We don’t know quite how many days RB Board members are expected to spend (my guess perhaps 25-30 a year) but it is hard to believe he had suddenly discovered it was going to be an unusually large commitment, especially as he had already spent 9 months actively engaged in the establishment phase and had served on various other public and private boards (and he was just an ordinary Board member, not holding the more time-consuming role of chair). And had he had any doubts any serious figure would have resolved them in his own mind before allowing his name to go forward for reappointment to the NZ Post chair role. As late as 22 June, he had been appointed by Cabinet (presumably his NZ Post Board and management colleagues had been told), and people from the Secretary to the Treasury down were still working on the basis the Post reappointment was going ahead. But by 1 July it wasn’t a thing.

I suppose it is always possible that (say) a serious family health emergency arose in those few days that meant he had to consider all his business and professional commitments……but (a) it appears that the NZ Post role (the one involving a serious conflict) appears to have been the only one given up, and (b) it would be quite straightforward to let something like that be known (and we’d all sympathise). But the article goes on “Finlay hasn’t responded to the Herald’s requests for comment”. That’s telling.

Most likely the Beehive jettisoned him at the last minute, realising that with media coverage and serious concerns being expressed by various senior figures, it was just a dreadful look heading into the new RB Board regime – when the new the rest of the Board they’d soon be announcing were in any case likely to be attacked as underqualified – and not worth going ahead with the Post reappointment. I’ve lodged fresh OIAs with the Ministers of Finance and State-owned Enterprises to see if we can learn more.

(One might wonder, if the Beehive story is correct, why they jettisoned him from the NZ Post role rather than the Reserve Bank one. Perhaps they reckoned it would be easier to find just another professional director for NZ Post – although none yet seems to have been appointed – plus his current term was actually expiring on 30 June. They probably hoped to get away without people realising they’d reappointed him just a few days previously. But don’t overlook also that if Finlay seems like a no-better-than-adequate appointee for the Board of the central bank and regulatory authority, the OIA papers make it clear how much difficulty Robertson and The Treasury had had in finding anyone half-qualified to serve, and Finlay is described on several occasions as the best on offer.)

A few other points caught my eye reading through again the OIA I received.

Treasury used two quite separate interview panels for appointing RB Board members. For the second wave, it was mostly Treasury and Reserve Bank people doing the interviews (including Finlay himself). But for the first round (where Finlay was chosen), they used a fairly high-powered panel, chaired by government favourite Brian Roche.

Among the interview panel was the Secretary to the Treasury. I was astonished to find that (so Treasury reported) she was on the panel because the Governor had asked for her to “reflect the seniority of the positions” (shame about that looking at what we ended up with), and “to provide gender representation”. Poor her, picked for purely tokenistic reasons.

But what really caught my eye was the presence of the head of the Australian Prudential Regulatory Authority, Wayne Byres, on the interview panel. Frankly, that seemed a little odd, for several reasons. First, one of the main relationships the Reserve Bank has to manage is that with APRA, and there will often – particularly at times of stress – be conflicting national interests. Second, APRA doesn’t operate with a part-time non-executive board (the sorts of role this interview process was selecting). But more generally, APRA is a pretty well-regarded organisation, and one might have hoped that having him on the panel would ensure at least one “adult in the room”, who really knew his stuff on the prudential side of what the Bank Board would be responsible for. And yet there is no sign that Wayne Byres, chair of a well-regarded prudential regulatory agency, had any qualms about appointing to the board of the prudential regulator, the chair of the majority owner of the 5th largest bank in the country. If he knew, did he really not care (there is no hint in any report to the Minister of any concerns being raised), and if he didn’t, how can it be that Treasury (providing the Secretariat to the process) or the Bank did not tell him? I suppose the head of APRA doesn’t need to know much about NZ-only banks, but it seems like a failure all round (including on his part, as the most prudential governance attuned person in the room) not to have found out, not to have raised concerns.

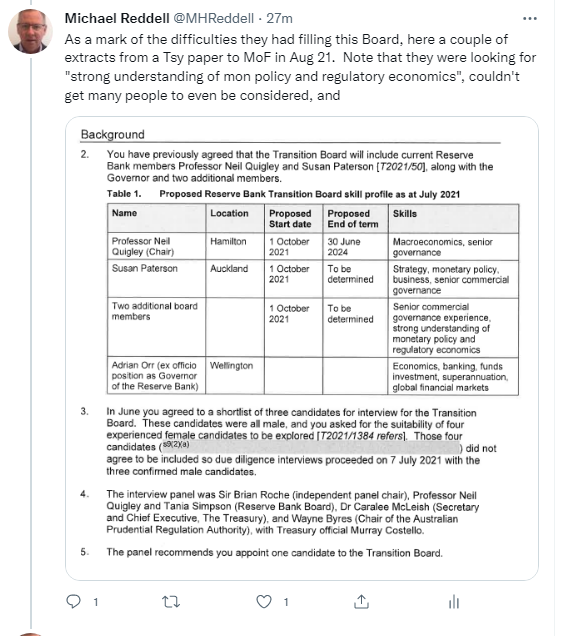

And finally, the saddest thing about reading through the OIA papers was the gradual diminution in ambition as (presumably) it became clear that (a) it was getting really hard to find any capable people even willing to put their names forward, and (b) that the government/Minister just didn’t really care about the substance at all.

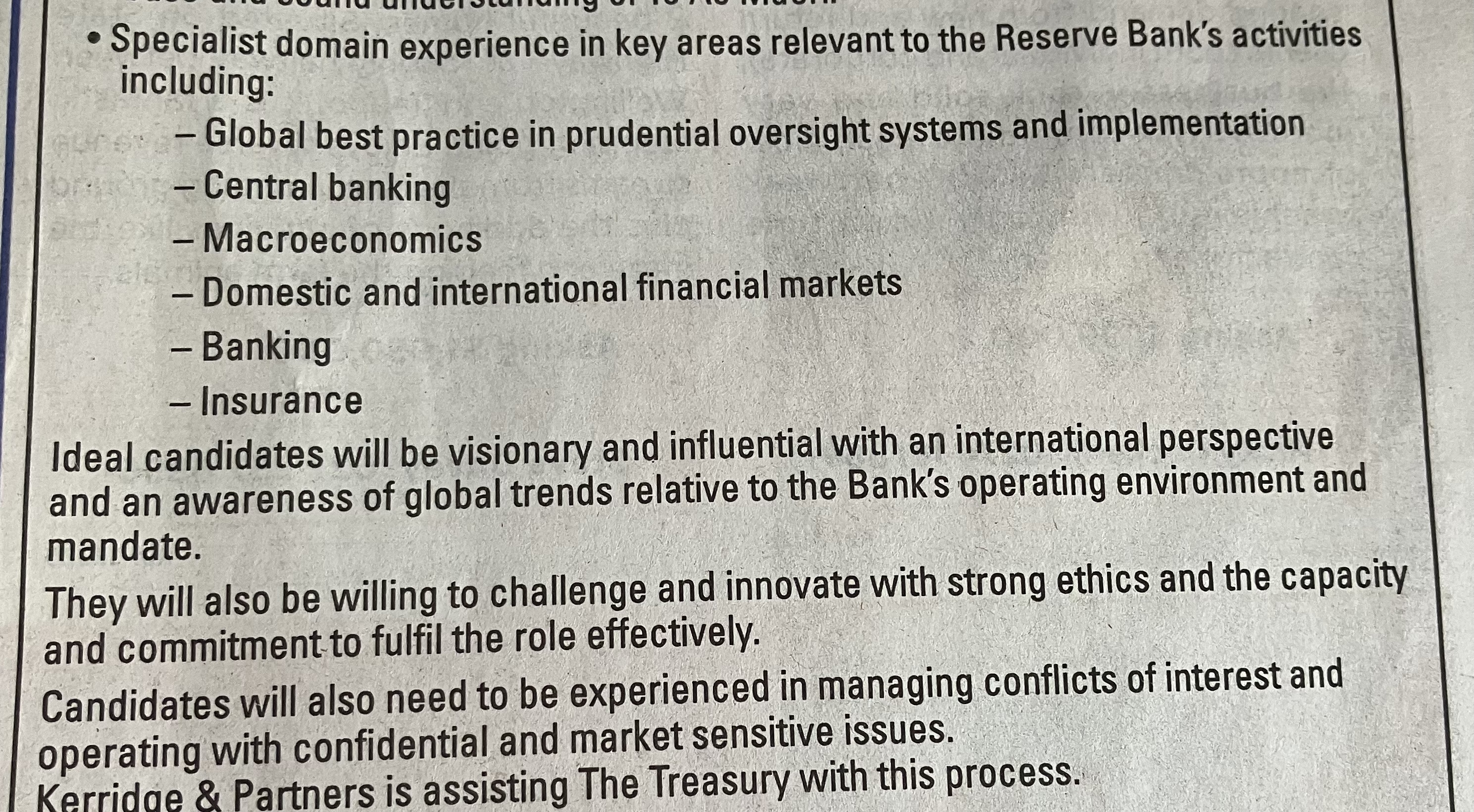

In what comes of not tidying one’s desk very often, I noticed a weathered copy of the newspaper advert from April/May 2021 for directors (transitional and permanent) sitting by my computer. Among the things they were looking for were these

Good stuff you might say.

But by February, from a report to the Minister they were reduced to this

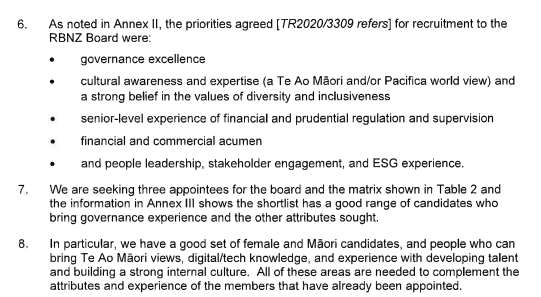

and by April, as they were closing in on the final list of those who were actually appointed, we get this summary

Perhaps a bit overqualified for a high-decile school board of trustees, and touching all sorts of political bases, but with no sign that any of them meet those ambitious “domain experience” goals once so prominent in their advertising. Oh, and no sign of any who are “visionary and influential with an international perspective and an awareness of global trends relative to the Bank’s operating environment and mandate”. The least underqualified would be the chair, but he was appointed only for a transitional two-year term. Here I might briefly disagree with Tibshraeny, who describes Finlay and Pepper as the two Board members with “the most experience when it comes to financial policy”: in fact, although both have worked in financial institutions, neither has any apparent background in prudential or related policymaking, financial stability etc, at all

As for “strong ethics” and “experienced in managing conflicts of interest” we ended up with two directors appointed who had clear and evident ongoing conflicts of interest, one of whom was involved in selecting the other. Are these really fit and proper people to be regulating and holding to account financial institutions (and those who run them), let alone the Governor? (And as a reminder, the Board is responsible for appointing and holding to account the Governor and the Monetary Policy Committee: they appear woefully underpowered when it comes to either aspect of their role.)

Then again, neither the Governor, the chair of the Board, the Minister of Finance, the Secretary to the Treasury, nor the Treasury staff charged with doing the donkey-work and actually managing these processes, seems to have seen any problem. Those asked don’t seem interested in straight answers or accountability either. And that should be even more concerning, as a reflection of what public life and governance in New Zealand seems to be becoming like.

Further to my post this morning, I’ve read a few more of the papers a bit more carefully.

It is still clear that when Rodger Finlay was appointed last October to the “transitional board” of the Reserve Bank and (from 1 July 2022) to the full Reserve Bank Board that no one (Treasury, Reserve Bank, Minister of Finance) seems to have been bothered by the stark conflict of interest between his twin roles as NZ Post chair (majority owner of 5th biggest bank in New Zealand) and the proposed role on the Board of the prudential regulatory authority. Any conflict was sufficiently unimportant (in the eyes of officials) that discussions were not documented, and ministers were not even advised of the issue in the relevant Cabinet and Cabinet committee papers.

To be fair, at that point it appears that Finlay’s term as NZ Post chair expired in the first half of 2022. But there seems to have been no discussion as to whether he would be reappointed, presumably because no one was bothered about the conflict. That reflects poorly on all involved – Treasury and Reserve Bank officials (junior and very senior), the chair of the Reserve Bank Board, Grant Robertson, and of course Finlay himself. A fit and proper person for the Reserve Bank Board role – the standard regulators apply to private sector appointees – would have immediately recognised the conflict (real and apparent) himself and made it clear that he could do one or other role but not both. Oh, and as I noted this morning, none of the other parties in Parliament raised any objections, or asked any questions, when Robertson consulted them about the RB Board appointment (as his new legislation required him to do).

I wrote my first post on the Finlay issue on 10 June 2022. It was the first piece drawing attention to the issue.

But it turns out that on 8 June 2022, Finlay’s reappointment as chair of the NZ Post board had been considered at the Cabinet’s Appointments and Honours Committee. His reappointment was confirmed at the full Cabinet on Monday 13 June 2022. In other words, just three weeks before the new Reserve Bank Board took office (and legal responsibility for bank supervision and prudential regulatory policy). And again, (other) ministers were not advised of the conflict (not even to note that a potential one had been recognised and arrangements were in place to manage it).

By this time, I’d had numerous emails from former senior central bankers astonished that the government was putting the chair of Kiwibank’s majority owner on the Reserve Bank Board. But apparently no ministers were at all bothered, as the reappointment to the NZ Post Board from 1 July 2022 was confirmed.

We know all this because a week or later there is a letter of apology from the Secretary to the Treasury to the Minister of Finance.

We know the reappointment was done on 13 June from this extract from a Cabinet paper from the acting Minister of State-Owned Enterprises

Poor Cabinet members. (Perhaps some should read my blog).

It does get worse. A journalist at the Herald had got interested in the story, and her story on Finlay ran on 21 June. For that story, she had asked around and had been told that Finlay’s term as chair of NZ Post was ending on 30 June 2022. As her story noted (and as I and other accepted) if so that made the situation less bad than it had first appeared, since although Finlay would have been on the transition board (and attending real RB Board meetings) while also chair of NZ Post he would not in fact be in both substantive roles at the same time.

That looks a lot like an active attempt by someone to mislead, since Finlay’s reappointment as NZ Post chair had been signed off by Cabinet on the 13th.

In the end it may be that what happened was more slipshod than a total abandonment of standards. That is suggested by this email dated 21 June (the day the Herald story appeared).

It seems likely, after last week’s announcement, that the redacted passages refer to the restructuring of the ownership of Kiwibank. After that restructuring is completed, and the Crown becomes the Kiwibank owner directly, there would be no conflict of interest between positions on the NZ Post and Reserve Bank Board. But that restructuring was only finally announced in mid August.

Slip-ups happen, but we should not skate over this one too quickly: Finlay’s reappointment to the Post position had occurred just a few days previously when presumably all involved at Treasury (and in the relevant ministers’ offices) knew that the ownership restructuring was not anywhere near announced, let alone done. That they failed to discuss the issue among themselves, that key figures failed to alert ministers and ministers to alert Cabinet, seems just consistent with the slack approach that had been taken on Finlay’s conflicts right back to October 2021. We don’t know whether the Governor knew of the Kiwibank ownership reshuffle plans, but either way there was still an onus on any Governor at all serious about avoiding actual or perceived conflicts, in the shiny new governance model, to have stamped his feet and insisted that Finlay’s situation be resolved. And, of course, there was Finlay himself – who, as far as we know, neither expressed nor felt any concerns.

The evidence suggests that sometime between 22 June and the end of the month Roger Finlay’s reappointment as chair of NZ Post was reversed. Perhaps ministers came to their senses and insisted on a rethink. Just possibly Finlay chose to stand down (the former seems more likely, since it is likely that the Herald story was the first time other ministers (including the PM) and their political advisers became conscious of the conflict issue, while Finlay had known of it for many months). In any case, by 1 July 2022, Finlay was no longer showing on the NZ Post website as board chair.

It all ends less badly than it might have, but it really should not be an acceptable standard of conduct from the Secretary to the Treasury, the Governor of the Reserve Bank, the Minister of Finance, or (now making regulatory policy including on fit and proper people in regulated institutions) Rodger Finlay. The twin appointments were never illegal (but should have been) but simply not being illegal does not make behaviours or appointments not improper. It is hard to think of any serious central bank anywhere where the possible twin government appointments (chairing the owner of a bank and serving on the regulatory authoritiy board) would be treated in such a slack and cavalier way.

This short post is mainly for those readers who don’t follow me on Twitter.

You may recall that a couple of months ago I highlighted as being highly inappropriate the appointment to the new board of the Reserve Bank (and the establishment “transitional board”) of Rodger Finlay, who was also chair of the state-owned enterprise New Zealand Post, which in turn was the majority owner of Kiwibank, the 5th largest bank in New Zealand.

The appointment was not illegal – itself a serious weakness in the new Act – but was clearly highly inappropriate in that the new Board was picking up responsibility for prudential supervision, most notably of banks.

When a couple of journalists got interested in the story, we were given to understand that Finlay’s term as chair of NZ Post would expire on 30 June 2022, and as the new Board only took legal responsibility for the Reserve Bank from 1 July 2022, that seemed to allay at least some concerns (about the situation looking ahead), even though it was clear that Finlay had been fully and extensively engaged with the activities of the Bank and the old Board during his “transition board” term, while serving as chair of Kiwibank’s majority owner,

Later that month, the rest of the appointees of the new Board were finally announced. It was a seriously underwhelming group of people, few of whom came anywhere near the sort of standard one should expect on the board charged with such considerable powers, including around the appointment and review of the Monetary Policy Committee. I lodged various Official Information Act requests for background material on the Board appointments, and this morning got back a (long) response from the Minister of Finance.

There might be a fuller post at a later date, but skimming through the documents, this succession of tweets (typos and all) captured the initial concerning aspects I spotted.

The key concern, at least to my mind, is that the papers make it clear that it was always intended that Finlay would continue serving as NZ Post chair (owner of Kiwibank) even once the new RB Board, on which he was serving making regulatory policy, took formal office, and that those who asked about this appear to have been actively misled.

It is concerning that this conflict was never drawn to the attention of Cabinet members considering the appointment, but that process failure itself appears to be primarily a reflection of the deeper problem that neither The Treasury nor the Reserve Bank appear to have considered the conflict to have mattered, either substantively or in appearance terms. There is text in the OIA release suggesting that Treasury and RB staff had discussed the matter at an early stage, but it doesn’t appear to have been treated very seriously in that there was no file note or record of those discussions kept, and no evidence of any discussion of the issues or risks with the Minister. The papers suggest they were having a great deal of difficulty getting able people to even consider appointment, and perhaps that meant standards slipped. They shouldn’t have.

Finally, one of the things that has interested me about the new RB legislation was the addition of the requirement that other parties in Parliament be “consulted” before Board appointments (including of the Governor) are made. In the release, there is a record of letters of consultation being sent to the other parties in Parliament. Sadly, there is no sign that any party raised any concerns about the Finlay appointment even though his chairmanship of NZ Post was explicitly mentioned in each of the consultation letters. I’ve been sceptical that the consultation requirement would mean anything much in practice, but it is sobering that no other party even appears to have raised the conflict of interest issue re Finlay, even when the letter was right in front of them. (For the record, National and ACT did send brief responses back to the Minister raising concerns about the later block of appointees announced in June.)

The Governor of the Reserve Bank must have been feeling under a bit of pressure recently about the LSAP programme. Losses have mounted and some more questions have started to be asked – by more than just annoying former staff – about value for money.

And thus on Thursday morning “Monetary Policy Tools and the RBNZ Balance Sheet” dropped into inboxes. It was an 10 page note setting out to defend the Bank and the MPC over the bond-buying LSAP programme and the inaptly-named Funding for Lending programme, the crisis facility under which the Bank is still – amid an overheated economy and very high core inflation – lending new money to banks.

Of course, the Monetary Policy Statement had been out the previous day. Had the Governor been serious about scrutiny and engagement, he’d have released his note a day or two before the MPS (or even simultaneous to the MPS). Then journalists could have read the paper and asked questions about it in the openly-viewed press conference. The Bank’s choice not to do so revealed their preferences. Oh, and then the note was released less than an hour before the Finance and Expenditure Committee’s hearing on the MPS, and since FEC no doubt had other things to consider it is unlikely any of the members had read the note before the hearing. That too must have been a conscious choice by the Bank (one that didn’t go down well with the Opposition members).

I noted earlier that the paper was 10 pages long, but there wasn’t a lot of substance. We still have nothing but the Bank’s assertions for their claims that the LSAP programme was worthwhile, and while we are told that they hope to provide some more analysis in a review document at the end of the year, attempting to kick for touch for another four months frankly really isn’t good enough. And, of course, we’ve heard nothing at all from the three non-executive MPC members who share responsibility for the programme. As it is, the 10 page note does not even provide a serious attempt at a rigorous framework for evaluating costs, benefits, and risks – there is more handwaving, and attempts to blur any analysis, than serious reasoning.

There are two separable strands. I am going to focus on the LSAP rather than the Funding for Lending programme (FLP), but it is worth making a few points on the latter:

the Bank claims that the FLP was necessary because banks were not yet operationally capable of managing a negative OCR, but the FLP was only finally launched in December 2020, and the Bank has separately told us that by that time banks’ system were in fact capable of coping with a negative OCR. Sure, the FLP had been foreshadowed over the previous few months and probably had some impact on retail rates then, but then the possibility of a negative OCR had also been foreshadowed,

the FLP was misnamed from the start (creating of lot of unnecessary controversy at the time about housing finance), with the name feeding an entirely fallacious mentality that shortages of settlement cash were somehow a constraint on bank lending. I am pleased to see that in this document the Bank (now that it suits) explicitly states “there is little evidence that higher settlement cash balances resulting from these programmes have directly impacted bank lending”. Paying the full OCR on all settlement cash balances – a Covid novelty that continues – will also have that effect.

it remains extraordinary that the Bank is still undertaking new lending under the FLP until the end of this year. It was a crisis programme, launched belatedly when crisis conditions had all but passed anyway, and there has been no clear justification for continuing new loans for at least the last year (recall the Bank wanted to raise the OCR last August). Arguments about predictable funding streams just fall flat, when the entire economic and financial climate was so uncertain, and when banks like everyone else recognise that circumstances have moved on from where they were two years ago. The Bank’s claim – that somehow banks would not future bank commitments seriously if they terminated early – deserve little more than to be scoffed at. And although the Bank will tend to play this down, we can tell that the FLP is relatively cheap funding – if it were not, banks would not still be tapping the facility. Similarly, arguing (as they do) that the OCR can offset the FLP is to concede the point: increases in the OCR should be leaning against real inflation pressures, not counteracting other lingering stimulatory crisis interventions.

But enough of the FLP, daft as it is still to be running it, the costs and risks are fairly small.

Not so the LSAP, where costs and risks are demonstrably high (now conceded by the Bank) while the alleged benefits are hard to pin down (not helped by the Bank making no serious public effort so far), and the water is being deliberately muddied by the Governor’s bluster and absence of careful delineation of the issues and arguments.

On financial costs, this from the Bank’s document is clear and straightforward (and I would hope might finally silence those who keep trying to claim they aren’t “real” costs, are all “within the Crown” or whatever). The Bank is clear that the financial losses themselves are real.

The best estimate of the net cost of LSAP is measured by the value of the Crown’s indemnity – unrealised losses based on current market valuation, reflecting a higher OCR – and losses realised by RBNZ upon the sale of the Bonds.

As to quantum, the claim under the indemnity fluctuates each day, and some of the Bank’s claim has now been paid by Treasury, but the Bank’s Assistant Governor was happy at FEC to use a ballpark $8bn figure. $8bn is roughly $1600 per man, woman, and child in New Zealand.

In the rest of this post, I am drawing on three sources of Bank comment: the 10 page document itself, the Bank’s appearance at FEC on Thursday (comments from Orr, Silk, and Conway, the chief economist), and the Governor’s full interview with the Herald (linked to in this article). Orr has made stronger claims orally than what is in the formal document, asserting twice that the wider economic gains of the LSAP programme were “some multiple” of the financial losses, following up to add that in his view it wasn’t even close. “Some multiple” must mean at least two, so at minimum the Governor is asserting (and recall there is no evidence advanced and not much argument) that the LSAP resulted in real economic gains of at least $16bn. At minimum, he is claiming a benefit of about 5 per cent of GDP at the time the LSAP was first launched. These are really huge claims, and you’d think he’d have at least some disciplined framework to demonstrate their plausibility (even just as ballpark estimates).

Instead, we are offering not much more than handwaving, and lines that at best veer close to outright dishonesty.

There seem to be three broad strands to whatever case Orr is trying to make:

there is the “least regrets” rhetoric,

there is talk (especially in the Herald interview) of the gains from bond market stabilisation back in March 2020, and

there is lots of talk (even the chief economist went down this line at FEC) about how much stronger than forecast the economy has been than was being forecast in 2020.

As Orr now tells it, “least regrets” meant the Bank would run monetary policy in such a way that it would prefer to see a grossly overheated high inflation situation (actual outcome) than a deep depression and entrenched deflation. Perhaps many people might share that preference if it was the only choice. But it wasn’t, and we’d be better off sacking and replacing all involved if they really want us to believe it was. Go back to 2020 and then when they were first talking about “least regrets” it was the much more reasonable framing (eg here) that, at the margin, and given that inflation had undershot the target for 10 years, they might be content with (core) inflation being a little above the target midpoint for a while rather than jump on things too early and risk keeping the unemployment rate higher than necessary for longer than necessary. Not everyone would necessarily have agreed with them on that, but it would have commanded pretty widespread assent (I wasn’t unhappy myself)….and in any case was entirely hypothetical at the time since, as I’ve documented in recent posts, actual inflation forecasts (Bank and private) were well below the target midpoint even as the Bank added no more stimulus beyond that (from OCR, LSAP, FLP or whatever) already embedded in the economic and inflation forecasts. So don’t be fooled by Orr rhetoric suggesting we should smile benignly on their handling of things because “the alternative was some Armageddon”. We pay him and his offsiders a lot of money to help ensure that those aren’t the choices.

Back when the LSAP programme was first announced – 23 March 2020 – there was a twin (related) motivation: generally to ease monetary conditions, and specifically to underpin the functioning of the government bond market. Global government bond markets were then in a mess, reflecting primarily US-sourced extreme illiquidity and flight to cash (at the time stock markets had been falling very sharply too). For those interested, here are a couple of links to what was going on at the time (here and here). Government bond rates were rising (even as policy rates had been cut): the disruption was real enough and it was getting very difficult to place paper. I’ve even gone on record here in the past stating that, even allowing for the moral hazard risks, I had no particular objection to some stabilising interventions, especially in the Covid context.

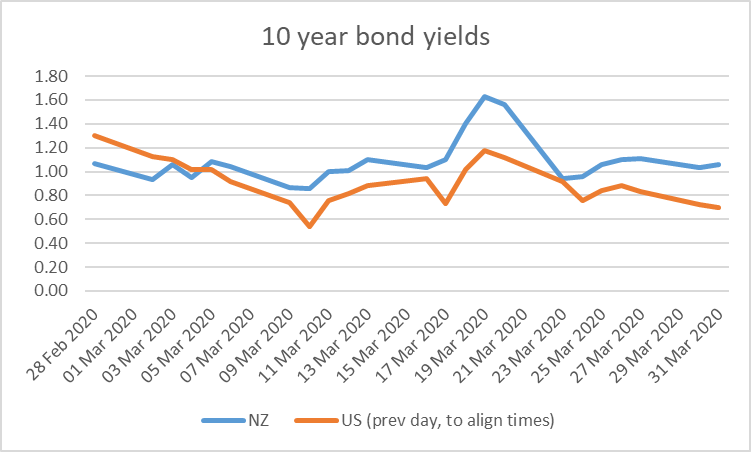

But here is a chart of US and NZ 10 year government bond rates for the month of March 2020 (with the US rates lagged a day to line with the NZ ones – changes in NZ bond rates in the morning are usually mostly a reflection of what has happened in the US overnight (the previous day for them).

You can see yields rising in that third week of the month even though both central banks had cut policy rates sharply that week (and the Fed had announced restarting of bond purchases). The NZ market is less liquid at the best of times than the US one. But yields in both countries peaked on 19 March (NZ).

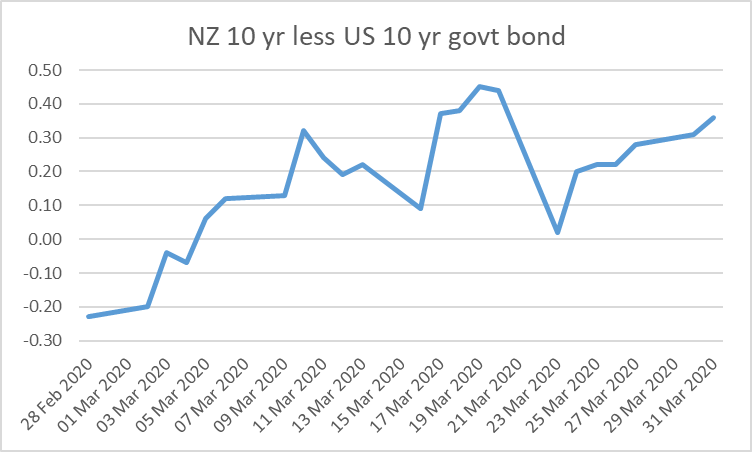

As did the gap between New Zealand and US rates. Days before the Reserve Bank did anything or even announced their own LSAP (although they had foreshadowed that one might be coming).

And if the Reserve Bank announced its LSAP on 23 March, on the same day (but remember the time difference) the Fed greatly expanded its own bond-buying programme. Almost immediately New Zealand long-term bond yields were back down to around 1 per cent.

Simple charts of yields – of the most liquid part of each market – don’t directly get to the illiquidity in other markets, but all indications are that the worst (globally) was already over by the time the Reserve Bank made its announcement, and given the US-sourced nature of the shock, it seems far more likely that the US actions were the more decisive policy contribution to stabilising markets. I don’t want to begrudge the Bank its small part in domestic market stabilisation (and they had some other interventions, including thru the fxs swaps market – but remember it is the LSAP they are defending), but even if we run through to 10 April, total bond purchases by the RBNZ to that point was only $3.6bn. Sure, a willingness to go on intervening offered a bit of cheap insurance to market participants, but if Orr wants to make much of what those earlier operations contributed (and it really can’t be much, given lockdowns, extreme economic and policy uncertainty etc) it relates to less than a 10th of the risk the Bank eventually exposed the taxpayer to through the LSAP.

(And if you want to note that over the month New Zealand bond yields did not fall as much as those in the US, recall that at the start of much US policy rates had much more room to fall than NZ ones did – and expectations of future short rates are the main medium-term influence on bond yields).

The third broad strand of Orr’s defence now appears to rest on how unexpectedly strong the economy (and inflation) proved to be.

From the 10 page report

His new chief economist tried the same line at FEC, with less nuance, and Orr himself when asked by Nicola Willis what evidence there was of the net benefits of the LSAP responded succinctly “the economy we live in today”.

It really is borderline dishonest. After all, all those dismal 2020 sets of forecasts – the Bank’s, the Treasury’s, and the myriad private sector ones – all included the effects of the policy stimulus (including the LSAP), and views on the path of the virus itself, so the resulting massive forecast error (for which I am not particularly blaming anyone) logically cannot be proof – or even evidence – of the effectiveness of a single strand of monetary policy (LSAP), or even of macro policy taken together. Since Orr and Conway are smart people, and know this point very well, it must be a deliberate choice to continue to muddy the waters as they do. They never even address the probability – high likelihood in my view – that most economists simply got wrong the extent of the adverse demand shock. At very least any serious analysis would have to unpick the various elements.

Instead, in none of their written material, or the comments of Orr and his offsiders, has there been any attempt (even conceptually) to think about the marginal effects of the LSAP programme itself. It was a discretionary (and last minute) addition to the toolkit. And even if we granted them a free pass for the first $3.6 billion or so of purchases (see above) all the rest was their choice. We know the financial costs (that $8bn or so of losses) but the alleged huge gains (Orr’s “multiples”) are unidentified – no effort has even been made. As just one small example, when the Herald’s journalist asked Orr whether, for example, they could have done less LSAP and instead cut the OCR to zero (which as even the Bank notes has no material market risk), Orr simply avoided answering the question.

I’ve run through previously the various reasons to be sceptical that the LSAP had much useful macro effect (those vaunted $16bn of gains Orr would need to show). In particular, even if the impact on longer-term bond rates was as large as Orr has claimed (again numbers that have never been documented), it isn’t at all obvious how that would have translated to large useful macro gains. It is commonly understood that the most important element in the interest rate bit of the New Zealand transmission mechanism is the short-end. Short rates (1-2 year bond rates) shape most retail lending rates, and are themselves largely influenced by expectations of the future OCR. Had the Bank been interested, say, in managing down a 3 year bond rate – as the RBA was – it could have done that directly, at very little financial risk. But instead they focused their bond buying at the longer end of the yield curve. Government borrowing costs may have been a bit less than otherwise as a result, but monetary policy isn’t supposed to be about getting cheap finance for the government but about macro stabilisation. Few private borrowers take borrowing at long-term fixed rates.

The Bank also claims that the exchange rate may have been lower than otherwise as a result of the LSAP. Perhaps, but (a) it depends on the counterfactual (they could have lowered that OCR further instead but chose not to) and (b) in most models the real economic effects of exchange rate moves take quite a long time to be felt, and even the Reserve Bank argues (contrary to quite a lot of literature) that the impact of the LSAP was decaying over time.

And it is worth pointing out that, as their document notes, they used the LSAP because of issues around operational readiness of banks for negative OCRs, but whose responsibility over the previous decade had it been to have ensured that banks were operationally ready? The taxpayer was exposed to the massive financial risk from the LSAP – without, it appears, any robust prior risk analysis – because of the Bank’s own failures. Just maybe there were some macro gains, but in a better world we’d have got those without the huge financial risk (and $8bn of losses). (A former colleague noted to me the other day that if we’d wanted to throw around an extra $8bn we’d almost certainly have gotten more macro bang for the buck by just giving $1600 to every man, woman and child and setting them free to spend – probably would have seemed a bit more equitable too.)

Oh, and did I add that if the last big macro policy tool deployed – the LSAP – was really as potent as the Governor seems to claim, then given how overheated the economy has been and the fresh ravages of high core inflation, it might have been much better (and lower risk) if the keys to the ill-prepared drawer marked LSAP had never been found and the instrument left untouched. We pay central bankers to do (materially) less badly than this, even (especially?) in difficult and uncertain times.

Bottom line: there has so far been no serious attempt by the Reserve Bank to frame an analysis that looks at the marginal impact of the LSAP programme, whether numerically or conceptually. Until there is, everything else they utter on the subject is really just defensive bluster. The public deserves better from senior officials of such a powerful institution. But as so often with the Bank, the question again arises as to why those paid to hold the Governor and MPC to account seem utterly uninterested in doing so.

A couple of weeks ago I did the first couple of posts in a series looking at the Reserve Bank’s stewardship of monetary policy since the start of 2020 (and the start of Covid). That proved to be too much for my intermittent (at best) post-Covid energy levels, and although I will come back and complete the series that won’t be this week either.

But I was glancing at the Reserve Bank’s page of selected OIA releases (always interesting to see what others have asked) when I found this release last Friday under the heading “Growth of RBNZ”. The Bank appears to have adopted a new strategy where the OIA request responses it chooses to release on the website are released there on the same day the requester themselves gets the information (a strategy often intended to reduce the payoff to the effort involved in actually devising and lodging an OIA request – it has been more normal over the years to put releases on the website at least a few days after providing the information to the requester.)

Actually on checking again, I find that there were three releases on Friday, quite possibly to the same person. First was “RBNZ Brand and Design” (which request appeared to be in response to a Bank advert a couple of months ago for a brand manager), second was “Growth of RBNZ”, and third was “RBNZ media inquiries”. There is the odd amusing snippet in the first, including

and

In the third release, the answers aren’t very interesting (which media interviews the Bank did), but there were several questions with potentially interesting answers which the Bank claimed were dealt with in (long) documents on Parliament’s website as part of the Bank’s Annual Review last year.

But what really caught my eye was the “Growth of RBNZ” request/answers, where the requester had asked for breakdowns of staff numbers over the last 10 years. They didn’t really need to go back that far – all the 200 FTE growth in staff numbers has occurred since Orr took office (up from 255 then to 454 on 30 June 2022) but it was interesting nonetheless. One gets a very clear sense of the bloat. Here for example

(I can recall a time, 35 years ago, when the numbers were probably larger but (a) total staff numbers were even larger than Orr levels), and (b) most counted the slimming down as something much more appropriate, and appropriately concerned with a restrained approach to public spending.)

The Bank’s functions haven’t changed but – like too many public agencies – the number of “communications” staff has increased hugely

An OIA I’d lodged a couple of years ago (and written about here) gives a bit more background on that function (although numbers have grown more since).

We know there has been senior management bloat – a whole new lawyer of second tier appointees (Assistant Governors) most of whom seem to have little subject expertise to offer)

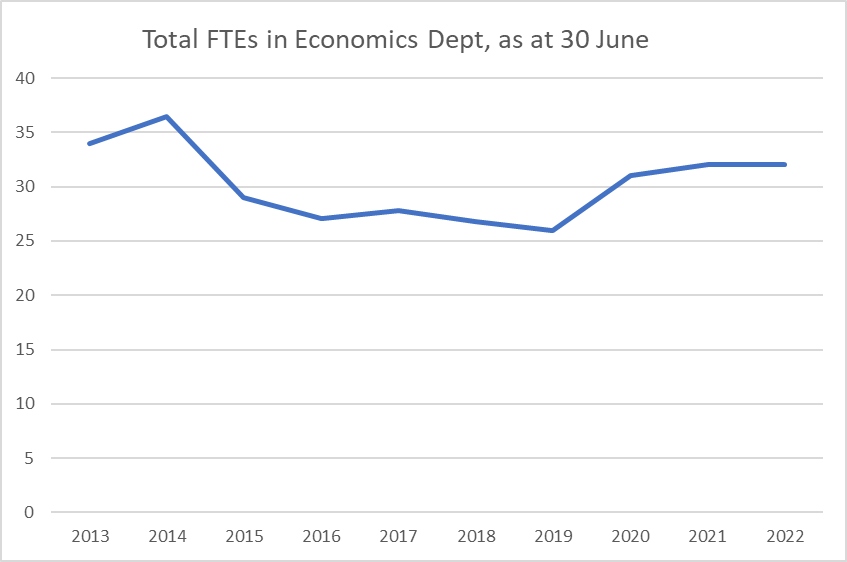

On the other hand, there are the Bank’s core economics functions. Until very recently, monetary policy was by statute the primary function of the Bank. That has changed (reasonably enough) but it is still a key core function. But here are staff numbers in the Economics Department

There are no self-evidently right or wrong answers as to how big a central bank Economics Department should be but there are few/no economies of scale, the Bank has been publishing very little serious research (or even revealing analysis) in recent years, and….inflation is through the roof. It doesn’t have the feel of an appropriate level of spending, especially when the Minister of Finance is throwing money at the Bank (all those hugely increased “support” functions above). But it is consistent with the stories one hears, at second hand but from inside the institution, suggesting that the Governor has little interest in monetary policy or the supporting macroeconomics. The Bank also released some salary data by function and it is striking that in 2021/22 the total salary spend on the Economics Department was almost 10 per cent lower than it had been in 2012/13.

The Financial Markets Department has usually been seen primarily as an element of the Bank’s monetary policy function (implementation etc), so it looks somewhat odd to see a huge increase in staff numbers there even as the economics function has been flat or falling. These were the operational people who, on the Governor’s instructions, lost the taxpayer billions and billions of dollars through the LSAP (so it isn’t even as if market functions were paying for themselves).

The other obvious area of growth – but harder to illustrate given the changing definitions/structures, so that numbers for the earlier period aren’t readily comparable to those now – is around the Bank’s financial stability functions. Some will welcome this growth, citing recommendations from the (fellow supervisors who did the) IMF’s FSAP a few years ago. Count me sceptical. For example, as at 30 June 2022 the Bank now has 38 people doing “Prudential Policy”, which feels large not just by historical Bank standards (there was a time 20 years ago when, perhaps going through the other extreme, all the prudential functions, not just policy, had about 10 people) but by comparisons with the policy functions for specific areas of policy in other ministries. It is, for example, more than the total staffing in the Economics Department. Oh, and they also have 22 staff doing “Financial Stability Assessment and Strategy” and yet the Bank publishes nothing particularly insightful and no research relevant to the prudential or financial stability functions. As best I can tell from this release, total staff numbers in the financial stability functions have more than doubled since 2018 when Orr took office.

Orr has long had something of a reputation as an empire-builder, and in his first four years at the Bank that seems to have been amply warranted again. This is scarce taxpayers’ money and yet Orr (facilitated by the Minister and the Board) flings it round with gay abandon……without even the consolation of better quality research, analysis, policy design, let alone policy outcomes. But it has been a windfall for HR people and former journalists.

I will resume my series of posts reviewing Covid monetary policy next week.

This post will be primarily of interest to former Reserve Bank staff, although may also interest those who are now, or were previously, charged with monitoring and holding to account the Reserve Bank. Most regular readers of the blog are likely to want to stop reading here.

I have set out below, without further comment, a significant chunk of the latest Annual Report of the Reserve Bank of New Zealand Staff Superannuation and Provident Fund. I am both a member and a long-serving trustee of the scheme. The report is now in the hands of members, but is also a public document (readily available on the Disclose register at the Companies Office). The material in the extracts below may also be of interest and relevance to former staff who were once members of the scheme but are so no longer, and whose financial interests may have been affected by (contested) rule changes made some considerable time ago.

In yesterday post, the first in this series, I tried to review and assess the Reserve Bank’s preparedness and its policy response to the Covid economic shock in the first 2-3 months (January to April 2020). They weren’t very well prepared, as it turned out, and this probably contributed to them rushing (and rushing The Treasury and the Minister) into some elements of the response that bore financial risks that were grossly proportionate to the likely economic or financial returns. But on the information they had at the time, and the way most other forecasters and commentators were thinking about the likely economic implications of Covid (and associated other policy responses), there wasn’t much doubt that a significant monetary policy response – easing monetary conditions – was well-warranted at the time. But there were mistakes – some perhaps not that consequential as it turned out (the pledge not to change the OCR, up or down, for a year come what may, but others (the LSAP, concentrated at the long end of the yield curve) much more so (in a variety of ways), and to a considerable extent foreseeably so on the information available at the time. And, as usual (but potentially mattering more in high stakes times) the Bank wasn’t very transparent.

A point I didn’t make explicitly yesterday, but should have, is that a stylised central bank (and among advanced countries there has never been one in recent decades) focused exclusively on inflation would have had no cause to have done anything different, given the data and the beliefs about (a) how the economy would behave, and (b) how the various possible monetary policy instruments would work.

Today I want to focus on the following year or so. Over that period, there weren’t a huge number of monetary policy initiatives (they really didn’t change the OCR at all, up or down, although did ensure that banks could cope with a negative OCR should the inflation outlook require such a rate in the future.

There were two significant policy announcements:

the extension of the LSAP (and the associated Crown indemnity) to a potential $100 billion of bond purchases, and

the establishment of the Funding for Lending scheme.

Inflation targeting has long been recognised as relying heavily on forecasts of inflation. Why? Because monetary policy actions don’t affect inflation anything like instantaneously. Prudent policy today will typically (but not always) be substantially informed by best view available on the outlook for inflation some way ahead. The lags matter.

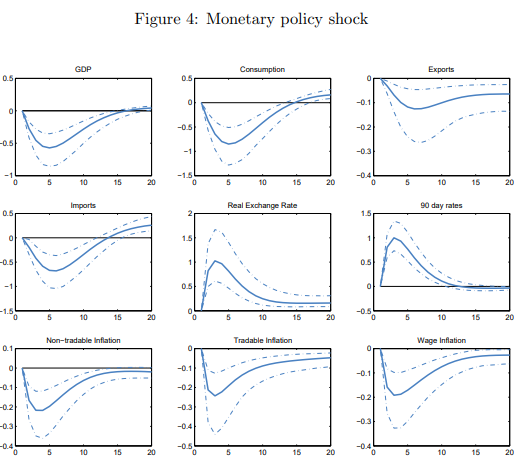

Quite how long those lags are is a matter for some debate. The old phrase was “long and variable”. I had a quick look at the Monetary Policy Handbook the Bank likes to boast of, and which is supposed to give readers a good sense of monetary policy as the Bank sees it. The word “lags” appears only once, and that referring to implementation lags in fiscal policy. I also checked the Discussion Paper in which the Bank’s calibrated economic model, NZSIM, is described, and was a bit surprised to find this chart

which seems to suggest very short lags (compare the 90 day and inflation charts), shorter than most practical discussion assumes. It is likely that the length of lags depends a bit on the shock, and a bit on the circumstances, but most pundits seem to think of the biggest impact of monetary policy on inflation as taking perhaps 12-18 months.

(Note that if the lags were as long as is sometimes rhetorically asserted – two years or more – the June quarter 2022 inflation outcomes (most recent we have) would have been substantially influenced by shocks to monetary policy in the June quarter of 2020, and since there were few/no dissenters then on the information available then, most questions of holding the RB now to account for recent inflation outcomes would be rendered largely moot. But few if any observers act, or consistently speak, as if the lags – for the largest effects – are that long.)

Implicitly or explicitly, all forecasts of inflation (and especially those that incorporate recent or prospective monetary policy changes) have a view on the length of lags, and when the Bank or officials ever discuss lags you also get the impression they have something like 12-18 months in mind.

So what did the Bank’s forecasts look like during this period? (Here, for the record, I an going to assume – I hope uncontroversially – that the published numbers were the Bank’s – or MPC’s – best view at the time.)

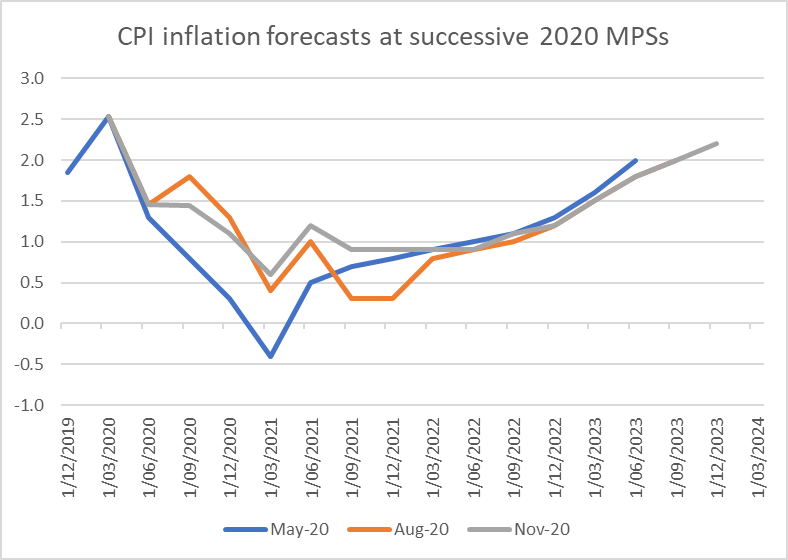

Here are the Bank’s inflation forecasts for the three successive MPSs, May, August and November 2020

Note that Reserve Bank published inflation forecasts almost always come back to 2 per cent eventually – it is the goal set for the Bank, and the default way the models are set up is for monetary policy to adjust endogenously to the extent required to get inflation back to target.

But note that these forecasts appear to have embodied views about the shocks monetary policy was leaning against that were severely disinflationary. Even with endogenous monetary policy, in all three of these sets of forecasts the inflation rates 12-18 months ahead were around 1 per cent, the very bottom of the target range and well below the 2 per cent successive governments required the Bank to focus on achieving. By the February 2021 MPS – not shown – the inflation outlook 12-18 months ahead was for outcomes around 1.4 per cent.

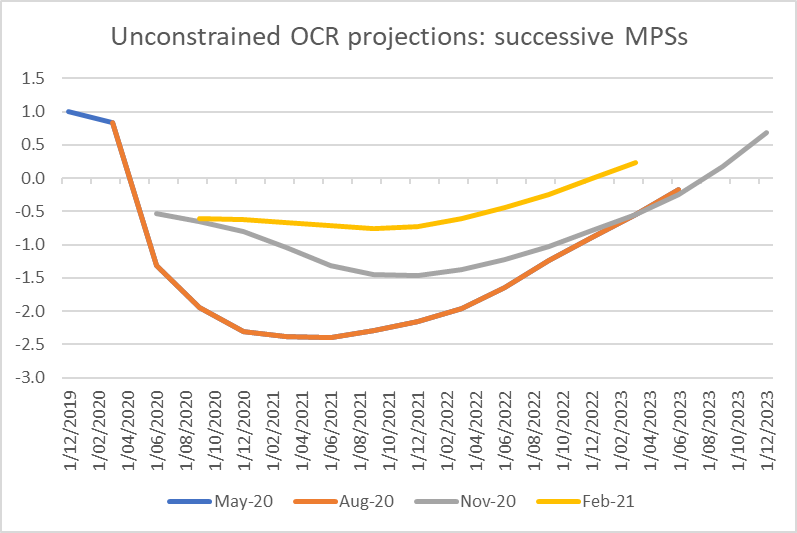

The Bank usually has OCR forecasts, but during this period (a) they had pledged not to change the OCR, (b) they believed the OCR could not yet be taken negative, and (c) they believed (or said they believed) that the LSAP was doing, and would do, a lot of the adjustment . So they published forecasts of what an “unconstrained OCR” would look like if a hypothetical OCR were to be doing its usual job.

Here were those projections (the paths in the May and August MPSs were identical)

So each of the published sets of projections through this period – but particularly those in 2020 – implied inflation well undershooting the target midpoint, even with substantial monetary stimulus (whether coming from the LSAP – which the Bank believed to be effective – or the OCR or – later – the Funding for Lending programme).

On their numbers it was pretty clear cut. The case for an aggressively stimulatory monetary policy was strong, whether considered against some pure inflation target or the Remit the MPC was charged with working towards.

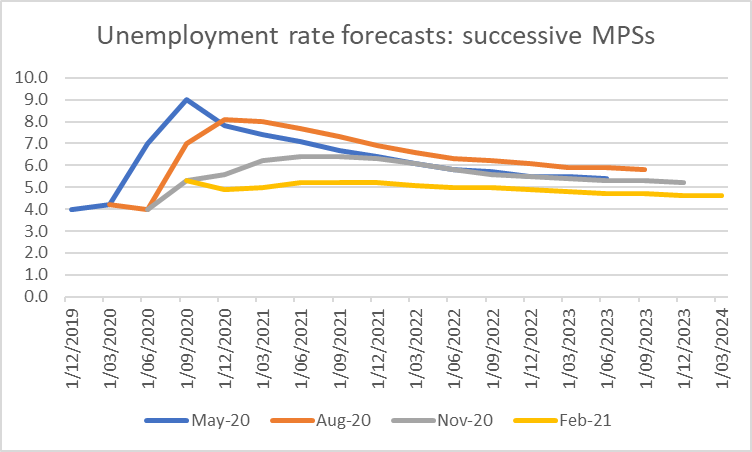

I haven’t mentioned the unemployment or output gap estimates. These were the unemployment rate forecasts, that take into account actual and endogenous future monetary policy

I don’t want to make much of them (in shocks like this most of the information is already in the inflation picture) but their best view through 2020 was the unemployment into 2022 would still be 6 per cent or thereabouts (well above any credible NAIRU estimate). By the Feb 2021 MPS there was a big revision downwards, but they reckoned then that this week’s unemployment number would be about 5 per cent (best guess a day out, something like 3 per cent).

The forecasts were, of course, wildly wrong. But (a) there is no reason to suppose they were anything other than the best view of the MPC/Governor at the time, and (b) on those forecasts, the purest of inflation targeters would have taken a similar view on how much monetary policy stimulus was required (arguably – it was an argument I made at the time – the projections argued for more).

It isn’t very satisfactory that an organisation we spend tens of millions of dollars a year on, and set up a flash new statutory committee to make the decisions, did that poorly. There is no getting away from the fact that they had the biggest team of macroeconomists in the country, and access to every bit of private or public data they would have requested.

But, they weren’t the only ones doing forecasts, putting their money and/or reputations on the line. Long-term bond yields, for example, were barely off their lows in early November 2020, when the Bank was finalising the last projections of 2020.

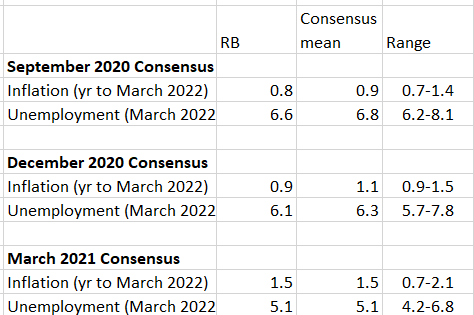

What were the published forecasts of other forecasters showing. Conveniently, NZIER each quarter publishes a collection in their Consensus Forecasts. Those numbers include projections from the five main retail banks, NZIER itself, the Reserve Bank and The Treasury. There are limitations to the comparisons – they report numbers for March years (as distinct from rolling horizons) – and each institution’s forecasts are finalised at different dates (and Treasury publishes numbers only twice a year). The data are slightly biased against the Reserve Bank, which typically finalises forecasts in the first or second week of the second month of the quarter, while the compilation is published in the middle of the final month of the quarter (so some will probably have updated their forecasts after the Reserve Bank publishes its MPSs).

But for what it is worth here are the comparisons for forecasts done in late 2020 and the first quarter of 2021.

In the September 202 comparison, the Reserve Bank’s numbers for both inflation and unemployment are very much middle of the pack (just a little less inflation and a little less unemployment than the mean response (NB: note to NZIER: medians are probably better)).

By the final quarter of 2020, the Reserve Bank had the lowest March 2022 inflation forecasts,,,,,,but not by much. 1.1 per cent – the mean response – was still a very long way below the target midpoint.

And in the March 2021 comparison – where those focusing on the Reserve Bank’s failures might have hoped to find them at odds with their peers, on the wrong side – the Bank’s inflation and unemployment forecasts sit right on the respective means (and the least-wrong forecaster – credit to them – still proved to be off on inflation by just less than 5 percentage points).

I think it is no small defence of the Reserve Bank, in making the monetary policy that was driving core inflation outcomes now, that it had very much the same sets of views as its local forecasting peers. There are other forecasters (eg Infometrics) but it isn’t obvious anyone doing and publishing forecasts was doing much better than the Bank when it mattered. If you disagree that it is “no small defence”, all I can really offer is “well, they’d be really culpable if the central tendency of private forecasters – each with fewer resources – had been materially less bad than them”.

Another comparison is with the NZIER’s Shadow Board exercise, which for each monetary policy review invites six economists (and a few others) to offer their views on what the Bank should (not “will”) be doing. Several of the bank chief economists are in the Shadow Board panel, as are Viv Hall (retired macro academic, and former longserving RB Board member), Prasanna Gai, macro professor at Auckland (and former overseas central banker/adviser), and Arthur Grimes (former chief economist of the RB and the National Bank).

Shadow Board members used to just be asked for an OCR view, with probability distribution, and given the chance to make comments (some take regularly, some occasionally, some hardly at all). So I look through each release starting with the June 2020 (non MPS) review. The question was posed about the degree to which respondents thought the RB should use (a) a negative OCR, and (b) further QE (ie an expansion of the announced QE programme) at each of (a) the upcoming meeting and (b) the coming 12 months.

In June 2020, of the six economist respondents two thought there was a strong chance that a negative OCR would eventually be required. Arthur Grimes thought there was a near-zero chance. Four of the six strongly favoured an eventual expansion of the QE programme. Prasanna Gai put that chance at 50 per cent. Arthur Grimes again assigned a near-zero probability. Sadly, neither Prasanna nor Arthur offered any comments in elaboration, so we don’t know whether they felt the LSAP would be ineffective, they had a more robust macroeconomic (inflation and/or unemployment) outlook, or what.

By the next review, enthusiasm for more stimulus had begun to fade somewhat (although Arthur – again with no comment – modestly increased his very low probability on more QE being appropriate.

By the September review the LSAP programme had been significantly expanded, but respondents views about the future hadn’t changed much. A couple thought a negative OCR quite likely to be required, but no one was keen on a further increase in the LSAP programme. Nothing much had changed in respondents’ views going into the November MPS (and none of the comments suggest a robustly different macro outlook).

By the February 2021 exercise, the question had changed. Respondents were now asked about the likely need for “tighter policy”, now and in the coming year. There was growing sense that a tighter policy stance would be required over the coming year, but only one respondent – Grimes – was confident that an immediate tightening was warranted.

Ah, you say “see, an academic who doesn’t even do monetary policy stuff these days bests the Reserve Bank”. Except for the awkward fact that this was the time Grimes chose to make comments and explain his stance. His explanation?

The RBNZ loosened monetary policy too much through 2020, causing soaring house prices (as well as other asset prices) which is very damaging for disadvantaged New Zealanders and for the next generation…..The tightening should continue until such time as house prices return to a much more affordable level provided the goods market does not enter deflation.

In other words, whatever the merits of Grimes’s stance may or may not be, he wasn’t at all focused on the outlook for the CPI. Instead he favoured using monetary policy to target house prices, with the explicit proviso that deflation might be a risk for general consumer prices. But – whatever merits or otherwise there may be to his argument – the target he was proposing was not the one the government had charged the Bank with pursuing.

(To look ahead, in the April survey Grimes again focuses on house price inflation but does talk about a need to “head off incipient goods market inflation pressures).

Again, maybe someone can point to some other commentators who did better, but from among the usual range of suspects there was little or nothing marking out the Bank’s overall view on inflation or monetary policy in the second half of 2020 or even early 2021. What there had been of course was a huge kerfuffle over house prices – where at times the Bank didn’t help itself (the chief economist once suggesting the higher prices were good and helpful), but where mostly I agree with Governor: house prices were not something the monetary policy arm of the Bank was supposed to focus on (construction costs are) and that it would be an inferior approach to monetary policy to make house prices a focus of monetary policy. It is not irrelevant that no other central bank does.