For 32 years the Board of the Reserve Bank hasn’t mattered very much. With no democratic mandate, no effective accountability, and no subject expertise either, they have a big say in who has become Governor (the Minister of Finance can only appoint someone they agree to recommend). But apart from that once in five years activity, they’ve mostly been asleep, turning up and collecting their (rather modest) fees but mostly doing little of what they are supposed to be doing – holding successive Governors to account. On paper, the model looked sensible enough, but once it became clear that accountability was a bit harder than it first looked, successive boards seemed to lose interest. With no resources and little expertise, and not much incentive either, they settled for a role that in practice – and it is documented in successive Annual Reports – amounted to little more than providing cover for successive Governors; when they did well, when they did poorly, and even when they went quite off reservation. It probably wasn’t greatly helped by the fact that when the Board finally got to have its own chair, the first two were former senior managers of the Reserve Bank. There were a few things they had legal responsibility for, but in the scheme of things it didn’t amount to much. And when they had little power, and even less inclination to use it, it didn’t very much matter who was appointed. Have we, for example, seen or heard any sign of hard critical accountability questions of the Bank re the recent monetary policy failure, or the $8bn of losses the Bank has run up? (That is a real question: I have an OIA in requesting the minutes of recent meetings.)

But on 1 July, a new era dawns. When the 1989 Act was passed, it gave almost all the powers of the Bank to the Governor personally. The 2018 amendment changed that, at least on paper, as regards monetary policy, but those responsibilities went to the MPC. The Board’s role didn’t change much, other than acting as postmen for the Governor to let the Minister know who he wanted appointed to the MPC. In what are now much the bigger areas of the Bank’s responsibility (banking regulation, insurance regulation, cash etc), the powers still rested with the Governor.

But not from 1 July. The Governor will still be a Board member, but it will be the Board that once again has the power and the responsibility for the discharge of the Bank’s powers and responsibilities (ex monetary policy). They can, and no doubt will, delegate many day to day things to the Governor, but they will have the power.

I’m not optimistic it will make much difference. Cultures change slowly, management is always much more motivated and better resourced than part-time government boards, and it is a poor signal that the previous chair is being carried over to the new regime. One might have hoped that the skills required for one role might be different from those for the new one. But apparently the Minister of Finance doesn’t see it that way.

Three weeks out from the start date the government has still not announced most of the members of the new board. But some months ago they announced the first three appointees, to serve as a “transitional board” smoothing the way to the new regime, before those three people take up formal board appointments on 1 July.

Here it is worth noting that the government has chosen to swing from one very unusual model to another one. It was very unusual (whether in New Zealand public life or overseas central banks and prudential regulatory agencies) to have so much power vested in a single individual. It is quite normal to have a Monetary Policy Committee (even if quite extraordinary to bar anyone with active expertise in the area from non-executive positions on the MPC). But it is very unusual to have banking, non-banking, insurance and payments system regulatory functions – policymaking and implementation – resting with a part-time non-executive board (especially when these same part-timers also have responsibility for MPC and Governor appointments). In such a model, avoiding potential conflicts of interest (actual and apparent) should always have been a critical consideration.

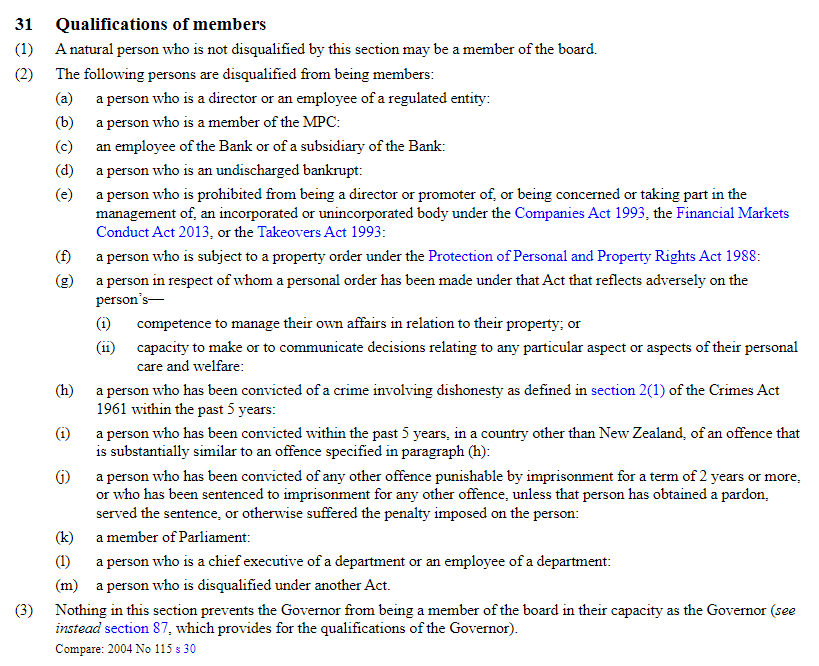

In the Act there is as a long list of types of people who are disqualified from being on the board.

I don’t have any quibble with the items that are on that list. My problem is with the ones that aren’t. One should probably add to (l) “or the chief executive or employee of any Crown agency”. But my biggest concern – and, as we shall see, the problem is already apparent – is with 31(2)(a). Again, just fine as far as it goes, but it does not go very far. Thus, a director or employee of an entity that owns a regulated entity is not disqualified (which just seems extraordinary), and nor is there anything to disqualify anyone who might earn a large chunk of their income (say as lawyer or consultant) from a regulated entity). No doubt the Board will have a conflicts of interest policy which would stop someone being directly involved in discussions on the institution they were part of, but such appointments simply should not be made at all. Policy affects sectors more generally, and these conflicts are not incidental. (Even with the old Board, which had no powers, there was an issue not that long ago with a Board member who was also a director of an insurance company, a sector for which the Bank is prudential regulator.)

Here is my specific concern.

I don’t know Mr Finlay, had never heard of him prior to this appointment, and know nothing about him beyond what is on the Bank’s own website.

But he has just been appointed to the board of New Zealand banking system regulator by the Minister of Finance when he is also chair of NZ Post, which is the majority owner of the 5th biggest bank in New Zealand (which also happens to be government-owned, and his appointment to the NZ Post Board is also a government appointment).

I checked the NZ Post website and there was no sign Finlay was just about to step down from that role (and even if he was, he should not be appointed to the RB role until quite clear of his banking-sector responsibilities).

It isn’t even as if Finlay seems to have any particular expertise in banking or financial system regulation – he just seems like another accountant and professional director, of a generic type that must be two a penny. If he did have great expertise it still wouldn’t justify such a conflicted appointment, but there is not even that to be said for him.

How can the Minister of Finance have thought such an appointment was okay?

But there are questions about others too.

The appointment of Board members is in the gift of the Minister, but it would be very unusual if the Governor (and the old/new chair) had not been consulted. Did they think it was just fine to have on the board of the banking regulator someone who is chair of a company that owns a large bank (all the more troubling when that bank is the weakest in the system, by capital, and most prone to bailout risk)? What advice did they provide to the Minister or Treasury on that point?

And one of the odd features of the new law is this provision

The fact that this provision was added, emphasises just how important these RB Board roles are seen as being (not just cosmetics like the old board). But where were the other political parties (National and ACT in particular) when Grant Robertson consulted them about Finlay’s appointment?

It is an outrageous appointment. It is hard to think of a comparable appointment in other advanced countries (but if anyone knows of one, let me know). It would not even be possible in most (generally run by executive boards). But even if some other advanced-country government somewhere has made such an appointment, it should not have been done here. It is bad form and – whatever the possible merits of Mr Finlay personally – it sets a dreadful precedent. If this government can do it for the chair of the owner of a state-owned bank, what is there to hold back some future government appointing someone in a similar position in a private bank. Mr Finlay himself, may be (probably is) a perfectly decent person, but if he really had what it took to be on the founding board of a banking regulator, he should have known not to have taken the RB appointment while holding the NZ Post one. Adrian Orr and Neil Quigley share responsibility, having (at best) stood silently by.

The real responsibility rests with Grant Robertson and the Cabinet. But they have apparently been given cover for this appointment by their political opponents, who apparently did not say no when Robertson came to consult, and even if (just possibly) they demurred then have said nothing since.

It is a sad example of the increasing corruption (institutional, rather than personal financial) of the New Zealand political system, notwithstanding those deluded annual Transparency International perceptions surveys.

This appointment should simply never have been made. It should be revoked, or Mr Finlay should do the decent thing and resign one or other of his NZ Post and Reserve Bank appointments.

UPDATE: According to this entry on The Treasury’s website, Finlay’s NZ Post appointment was for a term running from 21 August 2019 to 30 April 2022. As noted in the main post, he is still shown as chair on the NZ Post website, although I could not find an announcement of a renewal of his appointment by the relevant minister(s).

UPDATE: In addition to it being inappropriate to have someone on the board of the banking regulator who is chair of the majority owner of Kiwibank, it would also seem inappropriate to have someone on the central bank board – directly involved in the appointment of the Governor and MPC members – who is chair of the majority owner of the funds management business, Kiwi Wealth.

[…] Source_link […]

LikeLike

does Ngai Tahu say anything?

LikeLike

The Chartered Accountant appointment to the RBNZ is quite simply because the entire RBNZ team of economists failed to understand how the RBNZ QE operated from a Balance Sheet perspective. When QE first started every economist in the country including our Don Brash ex esteemed RBNZ governor thought the RBNZ was printing money. Any 2 bit Accountant would have known that the RBNZ QE was entirely debt driven just by reading the RBNZ Balance Sheet.

LikeLike

Sorry for the long C&P but it is important:

Geof Mortlock, a former central banker with fairly broad experience in the sector, wrote an open letter to RBNZ Chair Neil Quigley and Finance Minister Robertson about what’s been going on at the RBNZ.

A dozen or so others were cced, including a couple of journalists, and the thing crossed my inbox. With Geof’s permission, I’ve copied it here as I’ve not seen it picked up elsewhere.

Dear Mr Quigley, Mr Robertson,

I am writing to you, copied to others, to express deep concern at the increasingly political role that the Reserve Bank governor is performing and the risk this presents to the credibility, professionalism and independence of the Reserve Bank. The most recent example of this is the speech Mr Orr gave to the Central Banking Global Summer Meetings 2022, entitled “Why we embraced Te Ao Maori”, published on 13 June this year.

As the title of the speech suggests, almost its entire focus is on matters Maori, including a potted (and far from accurate) history of the colonial development of New Zealand and its impact on Maori. It places heavy emphasis on Maori culture and language, and the supposed righting of wrongs of the past. In this speech, Orr continues his favourite theme of portraying the Reserve Bank as the Tane Mahuta of the financial landscape. This metaphor has received more public focus from Orr in the last two years or so than have the core functions for which he has responsibility (as can be seen from the few serious speeches he has given on core Reserve Bank functions, in contrast to the frequent commentary he makes on his eccentric and misleading Tane Mahuta metaphor).

For many, the continued prominent references to Tane Mahuta have become a source of considerable embarrassment given that the metaphor is wildly misleading and is of no relevance to the role of the Reserve Bank. For most observers of central bank issues, the metaphor of the Reserve Bank being Tane Mahuta fails completely to explain its role in the economy; rather, it confuses and misrepresents the Reserve Bank’s responsibilities in the economy and financial system. It is merely a politicisation of the Reserve Bank by a governor who, for his own reasons (whatever they might be), wants to use the platform he has to promote his narrative on Maori culture, language and symbolism.

If one wants to draw on the Tane Mahuta metaphor, I would argue that the Reserve Bank, as the ‘great tree god’ is actually casting far too much shade on the New Zealand financial ‘garden’ and inhibiting its growth and development through poorly designed and costed regulatory interventions (micro and macroprudential), excessive capital ratios on banks (which will contribute to a recession in 2023 in all probability), poorly designed financial crisis management arrangements, and a lack of analytical depth in its supervision role. Its excessive and unjustified asset purchase program is costing the taxpayer billions of wasted dollars and has fueled the fires of inflation. In other words, the great Tane Mahuta of the financial landscape is too often creating more problems than it solves, to the detriment of our financial ‘garden’. Some serious pruning of the tree is needed to resolve this, starting at the very top of the canopy. We might then see more sunlight play upon the ‘financial garden’ below, to the betterment of us all.

There is nothing of substance in Orr’s speech on the core functions of the Reserve Bank, such as monetary policy, promotion of financial stability, supervision of banks and insurers, oversight of the payment system, and management of the currency and foreign exchange reserves. Indeed, these core functions are treated by Orr as merely incidental distractions in this speech; it is all about the narrative he wants to promote on Maori culture, language, the Maori economy, and co-governance (based on a biased and contestable interpretation of the Treaty of Waitangi).

I imagine that the audience at this conference of central bankers would have been perplexed and bemused at this speech. They would have questioned its relevance to the core issues of the conference, such as the current global inflation surge, the threat that rising interest rates pose for highly leveraged countries, corporates and households, the risk of financial instability arising from asset quality deterioration, and the longer term threats to financial stability posed by climate change and fintech. These are all issues on which Orr could have contributed from a New Zealand perspective. They are all key, pressing issues that central banks globally and wider financial audiences are increasingly concerned about. Instead, Mr Orr dances with the forest fairies and devotes his entire speech (as shallow, sadly, as it was in analytical quality) on issues of zero relevance to the key challenges being faced by central banks, financial systems and the real economy in New Zealand and globally.

I have no problem with ministers and other politicians in the relevant portfolios discussing, in a thoughtful and well-researched way, the issues of Maori economic and social welfare, Maori language, and the vexed (and important) issue of co-governance. In particular, the issue of co-governance warrants particular attention, as it has huge implications for all New Zealanders. It needs to be considered in the light of wider constitutional issues and governance structures for public policy. But these issues are not within the mandate of the Reserve Bank. They have nothing to do with the Reserve Bank’s functional responsibilities. Moreover, they are political issues of a contentious nature. They need to be handled with care and by those who have a mandate to address them – i.e. elected politicians and the like. The governor of the central bank has no mandate and no expertise to justify his public commentary on such matters or his attempt at transforming the Reserve Bank into a ‘Maori-fied’ institution.

No previous governor of the Reserve Bank has waded into political waters in the way that Orr has done. Indeed, globally, central bank governors are known for their scrupulous attempts to stay clear of political issues and of matters that lie outside the central bank mandate. They do so for good reason, because central banks need to remain independent, impartial, non-political and focused on their mandate if they are to be professional, effective and credible. Sadly, under Orr’s leadership (if that is what we generously call it), these vital principles have been severely compromised. This is to the detriment of the effectiveness and credibility of the Reserve Bank.

What is needed – now more than ever – is a Reserve Bank that is focused solely on its core functions. It needs to be far more transparent and accountable than it has been to date in relation to a number of key issues, including:

– why the Reserve Bank embarked on such a large and expensive asset purchase program, and the damage it has arguably done in exacerbating asset price inflation and overall inflationary pressures, and taxpayer costs;

– why it is not embarking on an unwinding of the asset purchase program in ways that reduce the excessive level of bank exchange settlement account balances, and which might therefore help to reduce inflationary pressures;

– why the Reserve Bank took so long to initiate the tightening of monetary policy when it was evident from the data and inflation expectations surveys that inflation was well under way in New Zealand;

– how the Reserve Bank will seek to balance price stability and employment in the short to medium term as we move to a disinflationary cycle of monetary policy, and what this says about the oddly framed monetary policy mandate for the Reserve Bank put in place by Mr Robertson;

– assessing the extent to which the dramatic (and unjustified) increase in bank capital ratios may exacerbate the risk of a hard landing for the NZ economy in 2023, and why they do not look at realigning bank capital ratios to those prevailing in other comparable countries;

– assessing the efficacy and costs/benefits of macroprudential policy, with a view to reducing the regulatory distortions that arise from some of these policy instruments (including competitive non-neutrality vis a vis banks versus non-banks, and distorted impacts on residential lending and house prices);

– strengthening the effectiveness of bank and insurance supervision by more closely aligning supervisory arrangements to the international standard (the Basel Core Principles) and international norms. The current supervisory capacity in the Reserve Bank falls well short of the standards of supervision in Australia and other comparable countries.

These are just a few of the many issues that require more attention, transparency and accountability than they are receiving. We have a governor who has failed to adequately address these matters, a Reserve Bank Board that has been compliant, overly passive and non-challenging, and a Minister of Finance who appears to be asleep at the wheel when it comes to scrutinising the performance of the Reserve Bank. We also have a Treasury that has been inadequately resourced to monitor and scrutinise the performance of the Reserve Bank or to undertake meaningful assessments of cost/benefit analyses drafted by the Reserve Bank and other government agencies.

It is high time that these fundamental deficiencies in the quality of the governance and management of the Reserve Bank were addressed. The Board needs to step up and perform the role expected of it in exercising close scrutiny of the Reserve Bank’s performance across all its functions. It needs directors with the intellectual substance, independence and courage to do the job. There needs to be a robust set of performance metrics for the Reserve Bank monitored closely by Treasury. There should be periodic independent performance audits of the Reserve Bank conducted by persons appointed by the Minister of Finance on the recommendation of Treasury. And the Minister of Finance needs to sharpen his attention to all of these matters so as to ensure that New Zealand has a first rate, professional and credible central bank, rather than the C grade one we currently have. I would also urge Opposition parties to increase their scrutiny of the Minister, Reserve Bank Board, and Reserve Bank management in all of these areas. We need to see a much sharper performance by the FEC on all of these matters.

I hope this email helps to draw attention to these important issues. The views expressed in this email are shared by many, many New Zealanders. They are shared by staff in the central bank, former central bank staff, foreign central bankers (with whom I interact on a regular basis), the financial sector, and financial analysts and commentators.

I urge you, Mr Quigley and Mr Robertson, to take note of the points raised in this email and to act on them.

Regards

Geof Mortlock

International Financial Sector Consultant

Former central banker (New Zealand) and financial sector regulator (Australia)

Consultant to the IMF and World Bank

These are Mortlock’s views; he notes that his views are shared by others.

I note that I have heard similar views around the Bank’s deterioration of research capabilities, and around its loss of focus, from rather a few former RBNZ people unable to put their names to it – and even unable to be quoted anonymously in some cases.

LikeLike

I’m just now writing a post on the Orr speech, and will be including some or all of Geof’s letter there.

LikeLike

[…] “It is an outrageous appointment,” he said in a recent blog post. […]

LikeLike

[…] “It is an outrageous appointment,” he said in a recent blog post. […]

LikeLike

[…] may recall that a couple of months ago I highlighted as being highly inappropriate the appointment to the new board of the Reserve Bank (and the establishment “transitional […]

LikeLike