For 32 years the Board of the Reserve Bank hasn’t mattered very much. With no democratic mandate, no effective accountability, and no subject expertise either, they have a big say in who has become Governor (the Minister of Finance can only appoint someone they agree to recommend). But apart from that once in five years activity, they’ve mostly been asleep, turning up and collecting their (rather modest) fees but mostly doing little of what they are supposed to be doing – holding successive Governors to account. On paper, the model looked sensible enough, but once it became clear that accountability was a bit harder than it first looked, successive boards seemed to lose interest. With no resources and little expertise, and not much incentive either, they settled for a role that in practice – and it is documented in successive Annual Reports – amounted to little more than providing cover for successive Governors; when they did well, when they did poorly, and even when they went quite off reservation. It probably wasn’t greatly helped by the fact that when the Board finally got to have its own chair, the first two were former senior managers of the Reserve Bank. There were a few things they had legal responsibility for, but in the scheme of things it didn’t amount to much. And when they had little power, and even less inclination to use it, it didn’t very much matter who was appointed. Have we, for example, seen or heard any sign of hard critical accountability questions of the Bank re the recent monetary policy failure, or the $8bn of losses the Bank has run up? (That is a real question: I have an OIA in requesting the minutes of recent meetings.)

But on 1 July, a new era dawns. When the 1989 Act was passed, it gave almost all the powers of the Bank to the Governor personally. The 2018 amendment changed that, at least on paper, as regards monetary policy, but those responsibilities went to the MPC. The Board’s role didn’t change much, other than acting as postmen for the Governor to let the Minister know who he wanted appointed to the MPC. In what are now much the bigger areas of the Bank’s responsibility (banking regulation, insurance regulation, cash etc), the powers still rested with the Governor.

But not from 1 July. The Governor will still be a Board member, but it will be the Board that once again has the power and the responsibility for the discharge of the Bank’s powers and responsibilities (ex monetary policy). They can, and no doubt will, delegate many day to day things to the Governor, but they will have the power.

I’m not optimistic it will make much difference. Cultures change slowly, management is always much more motivated and better resourced than part-time government boards, and it is a poor signal that the previous chair is being carried over to the new regime. One might have hoped that the skills required for one role might be different from those for the new one. But apparently the Minister of Finance doesn’t see it that way.

Three weeks out from the start date the government has still not announced most of the members of the new board. But some months ago they announced the first three appointees, to serve as a “transitional board” smoothing the way to the new regime, before those three people take up formal board appointments on 1 July.

Here it is worth noting that the government has chosen to swing from one very unusual model to another one. It was very unusual (whether in New Zealand public life or overseas central banks and prudential regulatory agencies) to have so much power vested in a single individual. It is quite normal to have a Monetary Policy Committee (even if quite extraordinary to bar anyone with active expertise in the area from non-executive positions on the MPC). But it is very unusual to have banking, non-banking, insurance and payments system regulatory functions – policymaking and implementation – resting with a part-time non-executive board (especially when these same part-timers also have responsibility for MPC and Governor appointments). In such a model, avoiding potential conflicts of interest (actual and apparent) should always have been a critical consideration.

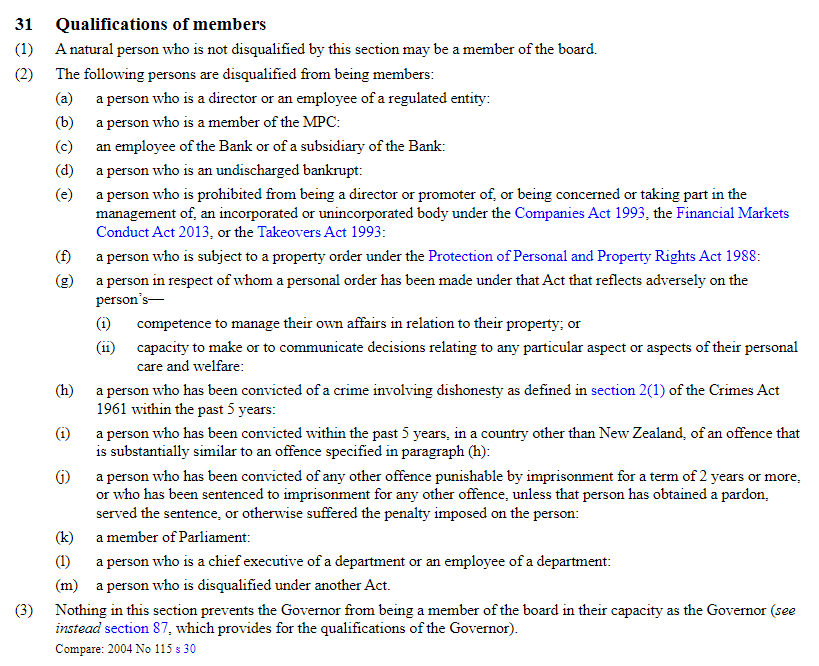

In the Act there is as a long list of types of people who are disqualified from being on the board.

I don’t have any quibble with the items that are on that list. My problem is with the ones that aren’t. One should probably add to (l) “or the chief executive or employee of any Crown agency”. But my biggest concern – and, as we shall see, the problem is already apparent – is with 31(2)(a). Again, just fine as far as it goes, but it does not go very far. Thus, a director or employee of an entity that owns a regulated entity is not disqualified (which just seems extraordinary), and nor is there anything to disqualify anyone who might earn a large chunk of their income (say as lawyer or consultant) from a regulated entity). No doubt the Board will have a conflicts of interest policy which would stop someone being directly involved in discussions on the institution they were part of, but such appointments simply should not be made at all. Policy affects sectors more generally, and these conflicts are not incidental. (Even with the old Board, which had no powers, there was an issue not that long ago with a Board member who was also a director of an insurance company, a sector for which the Bank is prudential regulator.)

Here is my specific concern.

I don’t know Mr Finlay, had never heard of him prior to this appointment, and know nothing about him beyond what is on the Bank’s own website.

But he has just been appointed to the board of New Zealand banking system regulator by the Minister of Finance when he is also chair of NZ Post, which is the majority owner of the 5th biggest bank in New Zealand (which also happens to be government-owned, and his appointment to the NZ Post Board is also a government appointment).

I checked the NZ Post website and there was no sign Finlay was just about to step down from that role (and even if he was, he should not be appointed to the RB role until quite clear of his banking-sector responsibilities).

It isn’t even as if Finlay seems to have any particular expertise in banking or financial system regulation – he just seems like another accountant and professional director, of a generic type that must be two a penny. If he did have great expertise it still wouldn’t justify such a conflicted appointment, but there is not even that to be said for him.

How can the Minister of Finance have thought such an appointment was okay?

But there are questions about others too.

The appointment of Board members is in the gift of the Minister, but it would be very unusual if the Governor (and the old/new chair) had not been consulted. Did they think it was just fine to have on the board of the banking regulator someone who is chair of a company that owns a large bank (all the more troubling when that bank is the weakest in the system, by capital, and most prone to bailout risk)? What advice did they provide to the Minister or Treasury on that point?

And one of the odd features of the new law is this provision

The fact that this provision was added, emphasises just how important these RB Board roles are seen as being (not just cosmetics like the old board). But where were the other political parties (National and ACT in particular) when Grant Robertson consulted them about Finlay’s appointment?

It is an outrageous appointment. It is hard to think of a comparable appointment in other advanced countries (but if anyone knows of one, let me know). It would not even be possible in most (generally run by executive boards). But even if some other advanced-country government somewhere has made such an appointment, it should not have been done here. It is bad form and – whatever the possible merits of Mr Finlay personally – it sets a dreadful precedent. If this government can do it for the chair of the owner of a state-owned bank, what is there to hold back some future government appointing someone in a similar position in a private bank. Mr Finlay himself, may be (probably is) a perfectly decent person, but if he really had what it took to be on the founding board of a banking regulator, he should have known not to have taken the RB appointment while holding the NZ Post one. Adrian Orr and Neil Quigley share responsibility, having (at best) stood silently by.

The real responsibility rests with Grant Robertson and the Cabinet. But they have apparently been given cover for this appointment by their political opponents, who apparently did not say no when Robertson came to consult, and even if (just possibly) they demurred then have said nothing since.

It is a sad example of the increasing corruption (institutional, rather than personal financial) of the New Zealand political system, notwithstanding those deluded annual Transparency International perceptions surveys.

This appointment should simply never have been made. It should be revoked, or Mr Finlay should do the decent thing and resign one or other of his NZ Post and Reserve Bank appointments.

UPDATE: According to this entry on The Treasury’s website, Finlay’s NZ Post appointment was for a term running from 21 August 2019 to 30 April 2022. As noted in the main post, he is still shown as chair on the NZ Post website, although I could not find an announcement of a renewal of his appointment by the relevant minister(s).

UPDATE: In addition to it being inappropriate to have someone on the board of the banking regulator who is chair of the majority owner of Kiwibank, it would also seem inappropriate to have someone on the central bank board – directly involved in the appointment of the Governor and MPC members – who is chair of the majority owner of the funds management business, Kiwi Wealth.