There will be more important issues facing the incoming government – even in what are, broadly speaking, economic areas.

There are house prices, for example, where two successive governments have done nothing material to solve the structural problems that have been evident for 15 years now (present for longer). It is a matter of (in)justice as much as anything.

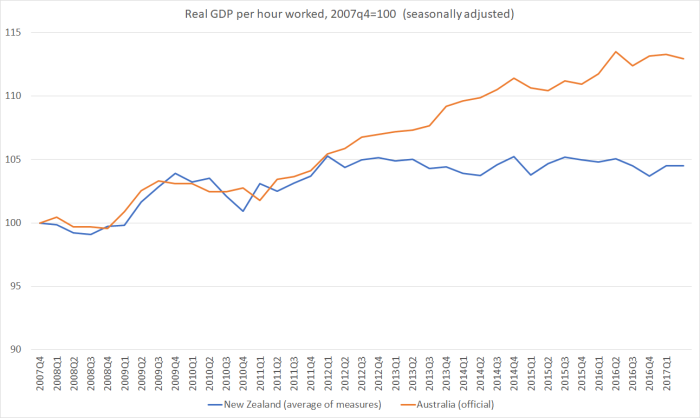

Or reversing the dismal productivity performance, epitomised by the last five years or no productivity growth at all.

Or reversing the dismal export performance which has seen exports as a share of GDP slipping – not usually a path to sustained prosperity – and which is forecast, by Treasury, to keep slipping (all else equal).

But if these things matter much more to our longer-term prosperity, it doesn’t make an overhaul of the Reserve Bank less important. And action on that front is now quite pressing. Apart from anything else, the Bank has an (unlawfully appointed) caretaker Governor, and whoever is appointed as the new Governor – under current legislation wielding huge amounts of power singlehandedly – will surely want to know quite what the shape of the job they are taking on is. If the three parties who will be part of the new government are to be believed, any change isn’t just going to be limited to some slightly different words in the new Governor’s Policy Targets Agreement.

I wrote a post last week on the possible implications for monetary policy of a new government. I’ll reproduce below the bits of that post that are relevant to the sort of Labour-led government we will actually have.

But the Reserve Bank isn’t just a monetary policy agency. If anything, the case for legislative reform is even stronger in respect of the other functions (notably the extensive financial regulatory functions the Governor exercises under various acts) than it is for monetary policy. These issues have less immediate political salience of course. But whereas for monetary policy there is, at least, a statutorily-required Policy Targets Agreement which can be used as a legal basis to hold the Governor to account, there is nothing remotely similar in respect of the prudential regulatory powers. The Governor – whoever he or she may be – exercises huge discretionary power, especially over banks, with little or no means for anyone to hold the Governor to account. You might like LVR limits (I don’t). But, whatever the merits of such controls, the Governor can impose or remove completely those controls on the basis of little more than a personal whim. There are process hoops he or she would have to jump through, but no substantive constraints. The same goes for debt to income limits. Or higher, or lower, capital requirements on banks.

It is simply far too much power to vest in any one person – especially an unelected person, who cannot easily be removed from office. A new Governor might be a truly exceptional person, blessed with wisdom and judgement far above the average. But we have to build our institutions around typical people – and typical public sector chief executives (including Governors), are typically average, a mix of strengths and weaknesses, insights and blindspots.

It isn’t the way in which other central banks and financial regulatory agencies are typically structured and governed. No other country that has reformed its institutions in the last 40 years has given a Governor anything like as much personal power as our system does – and even those who wrote our legislation would be flabbergasted at how much power our Governor actually wields since back then no one envisaged such an active discretionary regulatory role for the Bank.

Perhaps as importantly, it isn’t the way we govern almost anything else in New Zealand:

- public companies have boards,

- charities have boards,

- the judiciary has several layers of appeal, and in the higher courts benches of judges decide cases rather than individuals,

- the Cabinet itself is a decision-making committee, with the Prime Minister not much more – in extremis – than primus inter pares. Prime Ministers can typically be ousted quickly by a party caucus.

- Crown entities (from a school Board of Trustees to a major central government entity like the Financial Markets Authority) are governed by decisionmaking Boards.

Chief executives typically play an important role, but it is almost always an executive role, advising on and implementing a strategy set by others, and ensuring that the organisation itself functions effectively. In areas of policy in particular, single decisionmakers are very rare, and in areas of policy with as much discretion as those the Reserve Bank exercises unknown. And recall that governance structures don’t exist for the good times, or the occasions when everyone agrees; they are about resilience in tough times, resilience to inevitable human frailty.

It isn’t just a matter of policy discretion, moving away from the highly-unusual and risky single decisionmaker approach. There are oddities such as the Reserve Bank being responsible for its own legislation – something very unusual for a regulatory agency – and thus, often, for reviewing its own performance. We’ve seen that just this week: industry complaints that the Reserve Bank is reviewing its own performance as insurance industry prudential regulator. No doubt the regulatory agency has useful input to such reviews, but they just can’t bring the degree of detachment and independence to a review of their own performance that the public should expect.

And then there is transparency. The Reserve Bank has sought to claim over the years that it is highly transparent. In what matters, it is anything but. The Bank scores well in transparency over things it knows almost nothing about: they will happily tell us what they think will happen to the OCR in 2019, for example. But, unlike most government agencies or Parliament itself, they won’t, as a matter of course, publish submissions made on regulatory proposals. They provide particular secrecy to the submitters with the deepest pockets and the strongest interest in limiting regulation (banks themselves), and rely on a provision of the Act that was never intended to cover such submissions and which is well overdue for reform. They won’t publish the background papers to Monetary Policy Statements, even many months down the track (I did once succeed in getting 10 year old papers released). They won’t publish minutes of the advisory Governing Committee meetings. They won’t publish, even with a lag, even anonymised, the advice and recommendations the Governor receives when reviewing the OCR. Like many government agencies, they are persistently obstructive, pushing the very limits of the Official Information Act.

I could go on, but won’t today. Perhaps especially in a small country, an excellent central bank can be a significant part of the set of economic institutions that can help to shape and improve our economic performance. We need better from the Reserve Bank – not just specific decisions, but better supporting analysis, and a more robust and open institution (not one attempting to silence critics) than we’ve had in recent years. And so reform shouldn’t just be about the odd line of legislation here and there, but about (re)building a capable, open, and accountable institution that supports better quality decisionmaking. Finding the right person to be Governor, as one part of a new set of governance institutions, is a big part of that. And that is where the urgency needs to begin. Simply relying on names generated by a search and application process that began under the outgoing government, where applications closed even before the incoming Prime Minister became leader and gave much hope to her side, where applicants are all being interviewed and vetted by a Board of private company directors (and the like) appointed by the previous government – and apparently content with how things have been – is most unlikely to be a good basis for identifying the right person. And, again, it isn’t the way they do things in other countries.

I don’t want to be misread as suggesting that the Reserve Bank is more important than it really is. Better macroeconomic management – keeping the economy fully-employed, in a context of price stability – and appropriate financial system regulation, significant as they are, do not offer the answers to our long-term economic performance problems. Those answers rest with structural policy choices that the Bank has no special role in. But (a) good governance of very powerful institutions matters in its own right, and (b) in the short-medium term central bank choices, including around monetary policy, do make a real and material difference to economic performance. Ours has been poor over the last decade. In particular, we simply shouldn’t be in a position where the unemployment rate has been above any credible estimate of the long-run sustainable rate (or the NAIRU) for the whole of this decade so far. Most other countries with their currencies, and own monetary policies, aren’t in the same situation. This country can do so much better. A better-led central bank, operating under reformed laws and institutional arrangements, can be one part of that mix.

(And now that the National-led government is leaving office, I am hopeful that the OIA request I lodged again 10 days or so ago for the Rennie review report and associated papers might at last lead to some documents being released.)

Here are the bits of last week’s post on what a Labour-led government might mean for monetary policy, (for ease of reading I’ve not block-quoted the material).

—————————————————————————————————————————

And what if Labour leads the next government, requiring support of the Greens and New Zealand First for legislation? [We’ve already had confirmation, as I suggested then, that the Singaporean model is simply not going to happen.]

In that case, legislative reforms are more certain, but somewhat similar questions remain about what difference they might make.

Thus, the Labour Party campaigned on amending section 8 of the Act to include some sort of full employment objective. They haven’t provided specific suggested wording, and would no doubt want official advice on that. The Greens have endorsed that proposal and there is no obvious reason why New Zealand First would oppose it. But they might want to try to get some reference to the exchange rate or the tradables sector included, whether in the Act itself or in the Policy Targets Agreement.

Winston Peters’ private members bill [from a few years back] sought to amend the statutory goal of monetary policy (section 8 of the Act) this way (adding the bolded words)

The primary function of the Bank is to formulate and implement monetary policy directed to the economic objective of maintaining stability in the general level of prices while maintaining an exchange rate that is conducive to real export growth and job creation.”

[As I noted then, this wording goes too far and asks the Reserve Bank to do something that is impossible (real exchange rates are real phenomena, not monetary ones). I hope Labour and the Greens would not accept it, but we must presumably expect something of the flavour to find it way into the ACT or the PTA.]

I’ve also previously suggested that if Labour is serious about the full employment concern, it might make sense to amend section 15 of the Act (governing monetary policy statements) to require the Bank to periodically publish its estimates of a non-inflationary unemployment rate (a NAIRU), and explain deviations of the actual unemployment rate from that (moving) estimate. In principle, something similar could be done for the real exchange rate, but the (theoretical) grounds for doing so are rather weaker. Perhaps the political grounds are stronger, and such a change might encourage the Bank to devote more of its research efforts to real exchange rate and economic performance issues.

But – and I deliberately use the same words I used above – such legislative changes are not ones that would, on their own, make any practical difference to the conduct of monetary policy. Reflecting back on the 25 years of advice I gave to successive Governors on the appropriate OCR, I can’t think of a single occasion when the advice would have been likely to be different under this formulation than under the current wording.

The Labour Party and the Greens also campaigned on legislative reforms to the monetary policy governance model (including a decisionmaking committee with a mix of insiders and relatively expert outsiders, and the timely publication of the minutes of such a committee.) Although those proposals would represent a step in the right direction, they are rather weak. In particular, since Labour proposed that all the committee members would be appointed by the Governor, the change would largely just cement-in the undue dominance of the Governor. But I’d be surprised if they were wedded to those details, and it shouldn’t be too hard to reach a tri-party agreement on a decisionmaking structure for monetary policy – probably one that put more of the appointment powers in the hands of the Minister of Finance (as elsewhere) and allowed for non-expert members (as is quite common on Crown boards – or, indeed, in Cabinet).

So legislative change in that area – probably quite significant change – seems like something we could count on under a Labour-led government.

But whether it would make much difference to the actual conduct of policy over the next few years still largely depends on who is appointed as Governor. Not only will whoever is appointed as Governor going to be the sole decisionmaker until new legislation is passed and implemented – which could easily be 12 to 18 months away – but that individual will be an important part of the design of the new legislation and the sort of culture that is built (or rebuilt) at the Reserve Bank.

As I noted earlier, the appointment process for the Governor has been underway for months. Applications closed at a time – early July – when few people would have given the left much chance of forming a government. And the Board, all appointed by the current government and strong public backers of the conduct of policy in recent years, have the lead role in the appointment. Perhaps a new Labour-led government would reject a Bascand nomination. But even if they did so, they have no idea which name would be wheeled up next.

There are alternatives, if the parties to a left-led government actually wanted things done differently at the Bank. First, they could insist that the Bank’s Board reopen the selection process, working within the sorts of priorities such a new government would be legislating for. Or they could simply pass a very simple and short amending Act to give the appointment power to the Minister of Finance (which is how things work almost everywhere else). Of course, there is still the question of who would be the right candidate, but at least they would establish alignment of vision from the start – a reasonable aspiration, given that the Reserve Bank Governor has more influence on short-term macro outcomes than the Minister of Finance, and yet the Minister of Finance has to live with the electoral consequences.

Over time, governance changes are important as part of putting things at the Reserve Bank on a more conventional footing (relative to other central banks, and to the rest of the New Zealand public sector). I think some legislative respecification of the statutory goal for monetary policy – along the lines Labour has suggested – is probably appropriate: if nothing else, it reminds people why we do active monetary policy at all. But on their own, those changes won’t make any material difference to the conduct of monetary policy – or even to the way the Bank communicates – in the shorter-term (next couple of years) unless the right person is chosen as Governor. Perhaps so much shouldn’t hang on one unelected individual, but in our system at present it does.

Symbols matter, but so does substance. It will be interesting to see which turns out to matter more to a new government with New Zealand First support.

In closing, there is a long and interesting article in today’s Financial Times on some of the challenges – technical and political – facing central bankers. As the author notes, in many countries authorities are grappling with a mix that includes very low unemployment and little wage inflation. In appointing a Governor for the Reserve Bank of New Zealand, it would be highly desirable to find someone who recognises, and internalises, that the challenges here are rather different. Unlike the US, UK, or Japan (for example) New Zealand’s unemployment rate is still well above pre-recessionary levels – when demographic factors are probably lowering the NAIRU – and real wage inflation, while quite low in absolute terms, is running well ahead of (non-existent) productivity growth. There are some other countries – the UK and Finland notably – that also have non-existent productivity growth, but it is far from a universal story. Productivity growth carries on in the US and Australia and (according to a commentary I read last night) in Japan real output per hour worked is up 8.5 per cent in the last five years (comparable number for New Zealand, zero).

Some of these issues are relevant to monetary policy (eg unemployment gaps) and some are relevant to medium-term competitiveness (wages rising ahead of productivity growth). We should expect a Governor who can recognise the similarities between New Zealand’s experiences and those abroad, but also the significant differences, and who can talk authoritatively about what monetary policy can, and cannot, do to help. Perhaps even, as a bonus, one who might even be able to provide some research and advice to governments on the nature of the economic issues that only governments can act to fix.