One of the things that seems to worry establishment people in New Zealand is a belief that our economy is somehow very vulnerable to anything that disrupts the trade of New Zealand firms with China. It is a more-than-slightly puzzling concern, since only around 20 per cent of our exports go to China, and exports themselves aren’t an overly large share of GDP in New Zealand. For the firms involved – even if not the wider economy – there are clearly somewhat greater risks, since China has a demonstrated track record of being willing to use targeted trade sanctions for “punishment”. Those are the risks you take, as a private company, when you choose to play in that particular sandpit.

For the world economy, of course, any serious dislocation of China’s economy is a significant risk. With interest rates in most of the world not much above zero, any serious downturn in one of the world’s two largest economies could be quite problematic (as the US recession/financial crisis in 2008/09 was). But such downturns generally do even more damage to the economy at the centre of the problems than to everyone else. We all have a stake in a better-managed Chinese economy, even if the Chinese authorities are showing increasingly autarckic tendencies, and even if China isn’t anywhere near as internationally connected as the major Western economies are. But that interest isn’t a good reason to orient foreign policy around deference to China, or to refuse to have an open debate about Chinese government interference in the domestic affairs of other countries.

One case study that sometimes get mentioned when people talk about the vulnerabilities of trade with China is Finland. After a rather difficult time in World War Two – gallantly losing to the Soviet Union in 1939/40, and then ending up on Germany’s side – Finland spent the post-war decades in an awkward position. A new word was added to the international vocabulary: Finlandization

the process by which one powerful country makes a smaller neighboring country abide by the former’s foreign policy rules, while allowing it to keep its nominal independence and its own political system. The term literally means “to become like Finland” referring to the influence of the Soviet Union on Finland’s policies during the Cold War.

And largely, no doubt, just because of geography, much of Finland’s foreign trade was with the Soviet Union during those decades (it was a highly managed and regulated trade). Eyeballing a long-term chart, over the post-war decades to 1990 around 20 per cent of Finland’s exports were to the Soviet Union. And in the 1970s and 1980s, total exports as a share of GDP averaged just over 25 per cent in Finland. In other words, exports to the Soviet Union were averaging about 5 per cent of Finland’s GDP, pretty similar to New Zealand exports to China today. (A century ago, by contrast, New Zealand exports to the United Kingdom in the 1920s were 20-25 per cent of our GDP.)

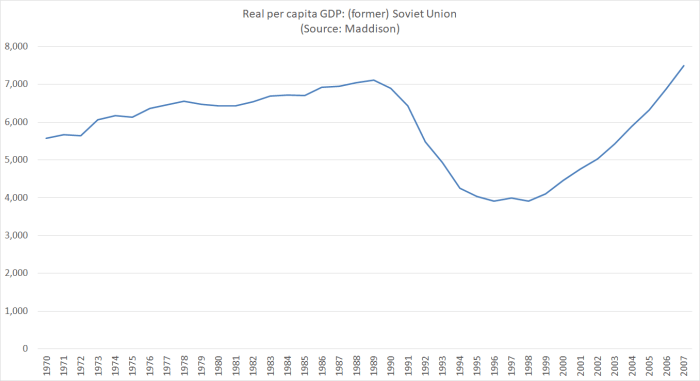

The Soviet Union ended messily, at least in economic terms. Here is a chart, using Maddison data, of real per capita GDP in the (once and former) Soviet Union.

In the slump, and associated disarray, imports plummeted, including those from Finland. In fact, in 1992 Finnish exports to Russia (the largest chunk of the former Soviet Union) were less than 1 per cent of Finnish GDP.

At the time, Finland itself was going through one of more wrenching recessions seen until then in post-war advanced economies. The unemployment rate rose from 3 per cent to over 17 per cent in just three years, and real per capita GDP fell by 11 per cent from 1990 to 1993.

The collapse of the Soviet Union wasn’t the only thing going on at the time. There were recessions in many western economies (including New Zealand and Australia) around 1991, but Finland’s experience was particularly savage (and also worse than the experiences around the same time of other Nordic countries).

One distinctive was house prices.

Real house prices rose by about two thirds (across the country) in just a couple of years, and then more than fully reversed the increase. The 50 per cent fall in real house prices involved a very sharp fall in nominal house prices, only matched in recent times in Ireland.

To some New Zealand readers it will all seem like just the sort of stuff they worry about. Isn’t our economy heavily dependent on trade with China, which could easily but cut off or otherwise implode, and aren’t house prices extraordinarily high? Isn’t the great Finnish recession exactly the sort of thing Graeme Wheeler and the Reserve Bank were warning of?

No doubt there are some similarities in what they were warning about. But if Finland offers lessons for us, they aren’t about who our firms trade with, nor even really about house prices and housing lending exposures. Instead, they are the (now) age-old lesson about the risks of severely overvalued exchange rates, with an overlay of a warning about the transitional risks of financial liberalisation (readers will recall that New Zealand and Australia also had a tough time in that transition in the late 1980s).

Finland had had quite high inflation even by the standards of many other European countries during the great inflation of the 1970s. Persistently high inflation, in a fixed exchange rate system, is typically accompanied by a succession of devaluations. We went through almost 20 years of something similar in New Zealand. But in Finland in the 1980s they decided to break the cycle, and set out to maintain a “hard markka” – the fixed exchange rate holding down imported inflation and, supposedly, imposing domestic disciplines that would lower domestically-sourced inflation. Much of the advanced world was disinflating at the same time, and so for a while the approach looked pretty successful. Core inflation was 12 per cent in 1980, and not much above 3 per cent by 1986.

But the Nordic economies, including Finland, were also liberalising their domestic financial systems in the 1980s. And a necessary corollary of a fixed exchange rate system is that, with an open capital accounts, your country’s interest rates are heavily influenced by those abroad. And German interest rates, which had been 7.5 per cent in 1980, just kept on falling – the Bundesbank’s discount rate was 2.5 per cent by 1988.

In process – fixed exchange rate, falling global interest rates – what followed was a massive speculative credit and investment boom in Finland. Lending and asset prices surged. Inflation picked up, and Finnish industry became increasingly uncompetitive internationally. That in turn created doubts about the stability of the exchange rate peg, prompting increases in domestic interest rates.

Here is what happened to the real exchange rate

And a measure of real short-term interest rates

Real interest rates didn’t peak until well into 1992, two years after the recession began. Why? Not because inflation was a particular problem – it was back down to not much above 3 per cent in 1992 and falling fast – but because of the extreme reluctance of the authorities to float the exchange rate. There had been grudging periodic adjustments under pressure, but it wasn’t until September 1992 that the markka was finally allowed to float.

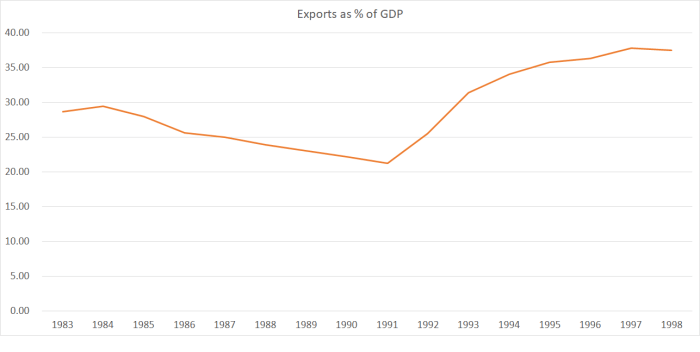

In the process – the boom over the late 80s and the subsequent bust, both heavily linked to the fixed exchange rate – the Finns managed to bring on themselves a very severe domestic financial crisis. And there had been huge shifts in the shares of various components of the economy. Here was the export share of GDP.

Investment as a share of GDP fell from around 30 per cent at the end of the boom, to around 19 per cent at the trough.

Floating exchange rates can be messy, but unless you economy is very closely aligned to – and integrated with – the currency of some other country, they are usually better than the alternative. That was certainly Finland’s experience over the crisis of the early 1990s.

And what of the financial crisis? Surely with house prices falling by that much, residential mortage losses must have been a big part of the story? In fact, the overwhelming bulk of the problem loans were to businesses and although many residential borrowers did get into trouble – rapid increases in unemployment and rising real interest rates in combination can be a toxic brew – in the end only 1 per cent of household loans were written off. That isn’t particularly surprising, is a point made in numerous studies, and is consistent with a survey of financial crises done a few years ago by the Norwegian central bank. As they put it

We look at a wide range of national and international crises to identify banks’ exposures to losses during banking crises. We find that banks generally sustain greater losses on corporate loans than on household loans. Even after sharp falls in house prices, losses on household loans were often moderate. The most prominent exception is the losses incurred in US banks during the 2008 financial crisis . In most of the crises we study, the main cause of bank losses appears to have been propertyrelated corporate lending, particularly commercial property loans.

And thus it was in Finland (and neighbouring Sweden for that matter). It is a point I’ve been making about New Zealand: when severe adverse shocks hit, provided your exchange rate is floating, not only does the exchange rate fall, but interest rates typically do too. Those are typically very powerful buffers, especially in the case of an adverse shock that isn’t global in nature.

And what of the role of the collapse in Finnish exports to the (now) former Soviet Union. I found various books and articles on my shelves about the Finnish experience – it was one of the handful of defining post-war crises. None of them regard that sudden drop as a particularly important part in the Finnish recessionary story. For anyone interested, there is an interesting recent paper by a couple of Finnish researchers. Their summary is as follows

It is shown that empirically, the strong credit expansion resulting from the simultaneous liberalization of the domestic financial markets and international capital movements has played the most important role in explaining the changes in real economic activity in Finland during the time period analyzed. In fact, over a longer time period (1980-2005) exports to Russia emerge as a countercyclical variable: slightly contractionary after the crazy years, and expansionary during the following depression [exports to Russia recovered somewhat after the first chaotic year or two].

Exporters were fairly soon able to find alternative markets for their products, helped – after 1992 – by the much lower real exchange rate.

And what of the overall Finnish economy itself? After freeing the exchange rate and allowing real interest rates to drop sharply, the economy itself rebounded quite rapidly. By 1997, real per capita GDP was already 4 per cent above somewhat flattering boom-exaggerated 1990 levels.

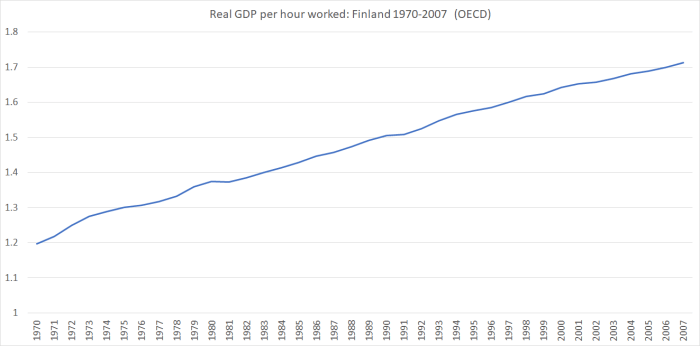

And consistent with a story I’ve run here in various posts over the years, through all that disruption and dislocation, here is the path of Finnish real labour productivity (real GDP per hour worked).

And consistent with a story I’ve run here in various posts over the years, through all that disruption and dislocation, here is the path of Finnish real labour productivity (real GDP per hour worked).

As was the case with the numerous US financial crises in the 19th and early 20th centuries, there isn’t much sign of any enduring damage to productivity (levels or growth) from the Finnish crisis. That’s reassuring, if not terribly surprising.

(Finland’s economic performance in the last decade has been pretty shockingly bad, including a productivity performance that – like the UK’s – is even worse than New Zealand’s over that period. But that is a story for another day.)

Saying that China accounts for 20% of NZ’s exports probably understates it’s effect. Although nominal true, China increasing demand for soft commodities in the last decade has been the major price determinates for our products.

If China implodes not only will it result in reduced exports to that country but also affect prices we can command for our exports to other countries..

However saying this, I wonder if we overstate China’s influence for commodities like dairy products. My understanding was that European Union subsidy policy change was the major cause of previous rise in prices.

Unfortunately, NZ is overly reliant on commodites. We really to need to move into manufacturing. Perhaps this is the reason for the poor productivity performance. There are only so many houses we can sell to each other and hairs to cut. We need scalable industries and exports of manufactured goods should be our focus. To many of our industries are duoplies or oligolopies and domestically focused. With this domestic focus, it makes no financial sense to invest in productive machines and processes as the outlay would not be compensated. The only world class industry we have is agriculture.

If Ikea was to only sell in Sweden, you would not have the low prices/ and increased productivity in their furniture industry.

There is a parochialism that limits NZ.

LikeLike

Re your first point, yes I agree to some extent (altho your point is probably more true for Australia, where China consumes a massive proportion of the global production of iron ore). It is the point i was making about the global economy’s vulnerability to a slump in any of the big 3 economies (US, euro-area, or China).

But precisely because dairy is priced globally, our dairy industry’s exposure to China is probably less than it appears on the surface. There is probably greater vulnerabilty in the export education sector, since capacity not sold to Chinese students probably won’t be sold that easily to people from elsewhere.

LikeLike

cracking; with snippets of history like that (which I’m still being enlightened by..), sometimes wonder’s how the recent financial crisis was a ‘shock’…

LikeLike

Crises in places like Ireland shouldn’t have been a surprise. It had all the classic ingredients – fixed exchange rate, interest rates too low for domestic circumstances, sharp appreication in the real exchange rate, rapid credit growth and huge property development, well-recogniser deterioration in lending standards…..and national hubris as well.

The US situation was much harder to pick.

LikeLike

Michael just to expand on Finland’s WW2 story.The Soviet Union invaded Finland in the winter of 1939. The Finn’s attributed this invasion to the Molotov-Ribbentrop agreement between the Soviet Union and Germany where these European super powers divided up Europe into areas which they could each invade.

No country came to the aide of Finland -in particular they were short of advanced weaponry -such as anti-tanks guns. As you say the Finn’s gallantry defended themselves -perfecting the molotov cocktail for instance. https://en.wikipedia.org/wiki/Molotov_cocktail

Finland lost territory (11% of its landmass) but not sovereignty when it sued for peace in 1940 with the Soviet Union. Finland relocated all its citizens, with the state gifting these citizens compensating land.

Hitler saw the Soviet’s relatively poor performance against Finland as a reason for Germany to renege on its agreement with the Soviet Union and thus to invade the Soviet Union. Hitler did a deal with Finland -giving the country heavy weaponry -thus Finland came on to the Axis side for this part of the war. But Finland did not purge its jewish community and there were Finnish jews fighting for Finland in nazi uniforms.

Towards the end of WW2, Finland’s president -Mannerheim wrote to Hitler withdrawing military cooperation on the grounds that unlike Germany (a superpower that it would survive in some form post-war) that it was uncertain if Finland (a small nation) would survive losing the war.

The Soviet Union gave Finland a very short time to get German troops out of Finland or else they would do it for Finland (ad probably never leave). Thus Finland had to fight Germany at the end of WW2. The German troops burnt down much of the buildings in Lapland when they retreated from Finland.

LikeLiked by 2 people

Very good blog post and discussion.

LikeLike