When Winston Peters talks about the exchange rate two things tend to be emphasised: the average level of the exchange rate (too high – relative to some benchmark presumably based something like on tradables sector performance or external indebtedness), and the volatility of the exchange rate (too volatile).

Not everyone would agree with him on the first point, but many would. Graeme Wheeler, former Governor, certainly did, often highlighting structural concerns about the real exchange rate. With slightly different emphases than Wheeler, I also agree, and have been highlighting for years how our real exchange rate has diverged markedly from the sort of path that differences in productivity growth between us and other advanced economies might have predicted. But the other common ground between Wheeler and I would be that these imbalances aren’t ones monetary policy can do anything much to fix.

By contrast, I think pretty much everyone would accept that monetary policy choices and regimes make a difference to the volatility of the exchange rate. New Zealand’s exchange rate – against the currency of by far its largest trading partner, the UK – changed only once in the first 30 years of the Reserve Bank’s history. There was some variability in the real exchange rate – adjusting for inflation differences – but not much.

Countries make choices about their exchange rate regimes – and thus about their monetary policy regimes. Some choose to fix their exchange rate, some to float, some to form common currency areas, and some to manage a non-fixed exchange rate (eg Singapore). Of course, choices about exchange rate regimes are influenced by real structural features: it might make a lot of sense to fix to a major trading partner if your two economies are very similar, but it probably wouldn’t if your two economies were regularly exposed to very different shocks, or if there was no dominant trading partner at all. Exchange rate regimes may change trade patterns a little, but they won’t change the underlying structural differences in two economies.

And there is a difference between short-to-medium term perspectives and longer-term ones. In the short-to-medium term, all else equal, floating exchange rate countries will tend to have more variable real exchange rates than other countries. In the longer-term, real structural forces will out. We had some pretty large adjustments in the last two decades of our fixed exchange rate era. Often it was good that we did. When the terms of trade fall (rise) sharply, a substantial drop (increase) in the exchange rate can be a useful part of how the economy adjusts to that change in fortunes.

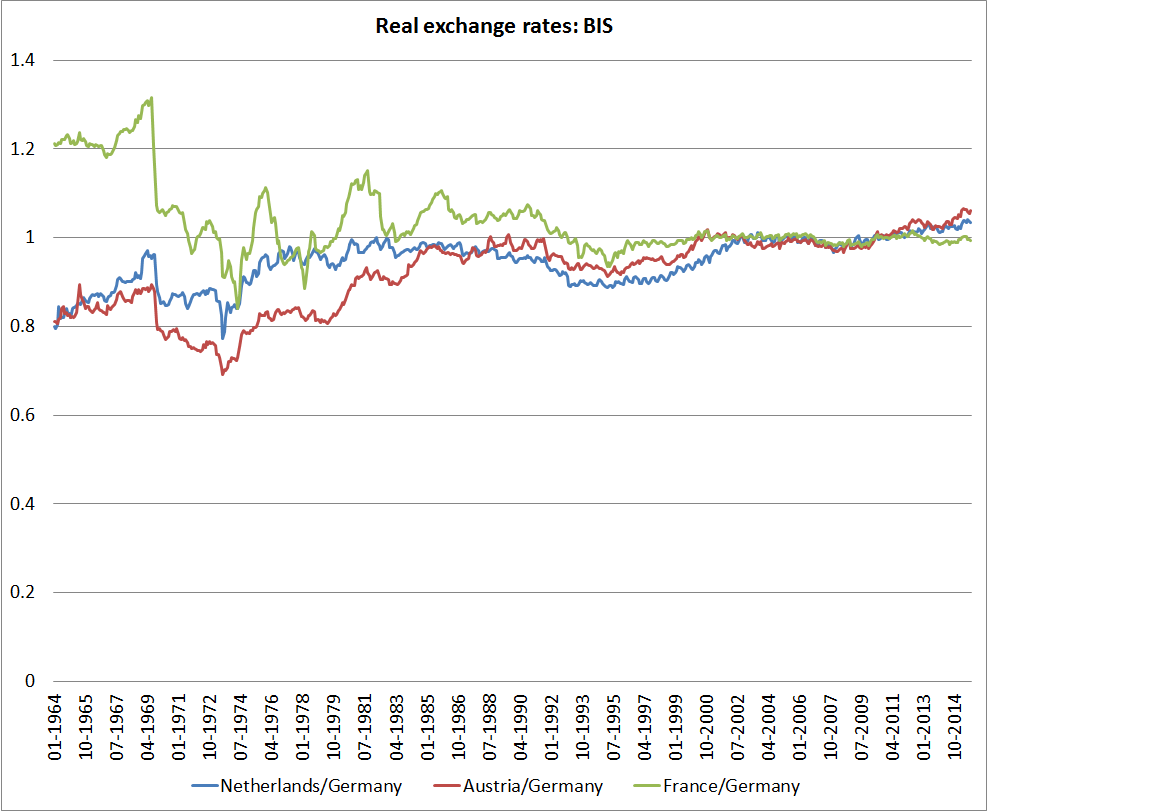

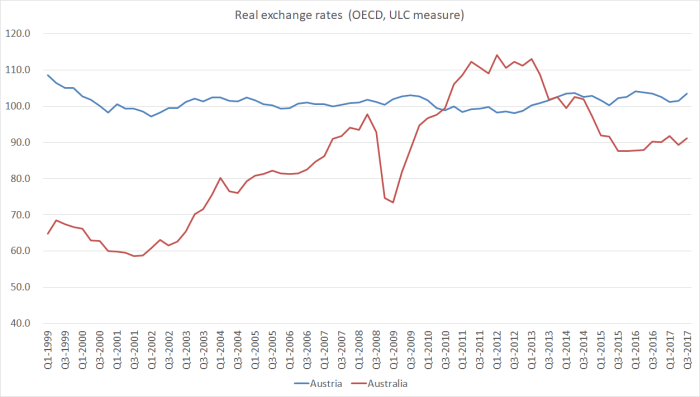

As a simple illustration of differences in real exchange rate volatility, I took the first two countries on an OECD table (Australia and Austria) and showed their real exchange rate since the start of 1999 when the euro began.

The point isn’t that Australia had Austria’s options – it didn’t (most of its trading partners weren’t simultaneously forming a common currency area) – or even that it would have wanted that option (in the face of very big terms of trade swings), just that there are huge differences.

And what about New Zealand? The Reserve Bank did a useful paper a few years ago looking at the volatility issue. In that paper, they looked back as far as the 1960s. That had the advantage of looking through specific choices about how the exchange rate is managed – over that period, we’ve had almost all the types of exchange rate regimes known to man, other than a common currency. The results suggested that the volatility of the New Zealand exchange rate had been relatively high – less so for short to medium term horizons, but more so if one focuses on longer-term exchange rate cycles.

But since Winston Peters has been talking about the potential for monetary policy regime changes to affect exchange rate volaility, here I wanted to look at a couple of shorter periods. The current monetary policy implementation system – the OCR – has only been in place since the start of 1999, and as late as 1996/97 we were still using exchange rate “comfort zones” to manage the very short-term variability in the TWI exchange rate.

And who to compare us to? The BIS has monthly broad real exchange rate indexes dating back to the start of 1994 for 60+ advanced and emerging countries. The OECD has a couple of quarterly real exchange rate series for its 35 member countries, with complete data for all countries since 1996. Of course, many of these countries are part of the euro, and I’ve shown results below for both all the individual countries and excluding the individual euro-area countries and including just the euro area as a whole.

There are more sophisticated ways of looking at volatility, but here I’ve just used two measures: the standard deviation of each country’s exchange rate index, and the range (high to low) expressed as percentage of the average value of the respective country’s real exchange rate index.

Here is how we’ve done relative to other countries on the BIS index. (I’ve shown both the full period of data since 1994 and also just the last 10 years – in case something is materially different about the most recent decade, but bearing in mind that 10 years is typically only about one exchange rate cycle).

| BIS real exchange rate | |||

| standard deviation | high-low range as % of average | ||

| Since Jan 1994 | |||

| NZ | 10.5 | 46.5 | |

| Australia | 12.3 | 54.5 | |

| Canada | 9.4 | 40.3 | |

| Japan | 17.9 | 54.3 | |

| Israel | 8.3 | 32.3 | |

| USA | 9.2 | 33.1 | |

| Median of all countries | 10.4 | 42.2 | |

| Median excluding individual euro countries | 11.9 | 52 | |

| Last 10 years | |||

| NZ | 7.1 | 36.8 | |

| Australia | 8.5 | 41.5 | |

| Canada | 8.1 | 34.3 | |

| Japan | 12 | 40.8 | |

| Israel | 4.8 | 23.9 | |

| USA | 7.1 | 23.7 | |

| Median of all countries | 5.5 | 23.2 | |

| Median excluding individual euro countries | 7 | 28.5 | |

Overall? Well, our experience looks a lot like that of the median country and a little less variable than Australia’s real exchange rate over this period. Since I first noticed the phenomenon almost a decade ago now, I’ve also been struck by the fact that exchange rate variability in New Zealand has been less than that in Japan and quite similar to that in the United States. Over just the last decade, the amplitude of the exchange rate cycle has been larger for New Zealand and Australia than for most of these countries, but that just reflects the fact that both exchange rates fell so far in the 2008/09 crisis/recession – surely a welcome, buffering, development. Officials certainly thought so at the time.

I didn’t show Singapore separately, but the variability of its exchange rate over this period was similar to that for the euro-area as a whole, but materially larger than that for most individual euro-area countries.

What about the OECD measure?

| OECD real exchange rate (ULC) | |||

| standard deviation | high-low range as % of average | ||

| Since Dec 1996 | |||

| NZ | 14.6 | 56.7 | |

| Australia | 16.3 | 66.4 | |

| Canada | 12.4 | 44.5 | |

| Japan | 18.8 | 75.1 | |

| Israel | 11.2 | 42.6 | |

| USA | 12.0 | 36.7 | |

| Median of all countries | 10.1 | 40.5 | |

| Median excluding individual euro countries | 12.1 | 48.0 | |

| Last 10 years | |||

| NZ | 8.4 | 33.8 | |

| Australia | 10.4 | 41.8 | |

| Canada | 7.3 | 23.9 | |

| Japan | 12.6 | 48.0 | |

| Israel | 6.9 | 26.7 | |

| USA | 8.6 | 26.7 | |

| Median of all countries | 6.8 | 23.5 | |

| Median excluding individual euro countries | 7.6 | 31.7 | |

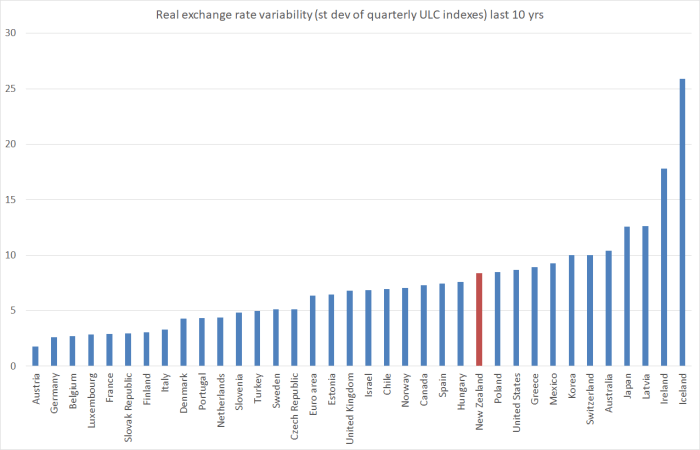

Still less variable than the exchange rates of Australia or Japan. And at least over the last decade, little to mark us out from the median of the floating exchange rate countries (ie the series excluding the individual euro-area countries).

This chart is just one index for just one period, but it helps illustrate a few points.

Notably:

- all the countries to the far left of the chart are in the euro (or pegged to it – Denmark),

- among the floating exchange rate countries, the variance of our real exchange rate hasn’t stood out over the last decade,

- even being in the euro is no protection from considerable real exchange rate variability if the fundamentals of your economy aren’t closely aligned to those of the large country(or countries) you are pegged too – see Ireland and Greece.

I wouldn’t want anyone to go away from this post with a sense that I’m indifferent to real exchange rate volatility. I’m not. The extent of the variability in many real exchange rates is something of a puzzle, even when dressed up in “the exchange rate is an asset price” language. On the other hand, not all real exchange rate variability is a bad thing – many of the biggest moves see the exchange rate acting as a helpful buffer. Exchange rate variability may also be more of an issue in a small country, where firms probably have to take their products international at an earlier stage than might be the case in a larger country.

But, equally, New Zealand’s realistic options are quite limited. We don’t have a single dominant trading partner, with whom our economic fundamentals are well-aligned. And with structural demand pressures so different from most of the advanced world (ie interest rates that average persistently higher), attempting to solve the problems by simply choosing a big currency to peg to would, most likely, have been a recipe for an Irish mess.

The biggest constraints on growth in the New Zealand tradables sector are the relative scarcity of good opportunities in such a remote location, compounded by the persistently high level of the real exchange rate. Considered against that backdrop, the volatility of the exchange rate – real or nominal – which isn’t that unusual by the standards of countries in our sort of position is likely to be (a) a second or third order issue, and (b) one where attempted fixes could easily leave us worse off than we are now.