There was interesting and stimulating piece by Matthew Klein the other day on the FT’s blog Alphaville headed “The euro was pointless”. I’ve been a euro sceptic from way back, and am still counting the months until it dissolves. A common currency should be an intrinsic part of common nationality, and if the latter isn’t going to happen neither, generally, should the former. The exception, where there might be some gains from a common currency, and no real costs, could be if countries’ economies were so similar that they faced the same shocks and the same stresses.

That said, I’m not persuaded that Europe’s current plight can be attributed largely to the creation of the euro. After all, the whole region is at or near the lower bound for nominal short-term interest rates. If each of the countries had their own currencies, perhaps some would be doing a little better than they are, but on average interest rates couldn’t be lower, and there is no reason to think that, on average, the real exchange rate would be lower. The zero bound looks as though it binds more tightly in countries/regions with little or no population growth than in others.

But what caught my eye was when Klein got into his stride with a discussion of “the most natural currency union never to exist: Australia and New Zealand”.

I presume he is unaware that for the first 89 years of its modern existence, New Zealand to all intents and purposes did enjoy a currency union with Australia. To the extent that one can even think of a NZ/Aus exchange rate until 1929 (or NZ/UK or Aus/UK ones) they were each 1. After 1914 it was no longer a matter of law, but the private sector still found it worthwhile to manage the exchange rates to retain parity. (Of course, prior to 1901, “Australia” was a geographical expression only – a continent made of up of several different self-governing colonies). There was no banking union or fiscal union (but a great deal of debt), although labour flowed pretty freely between the two countries in response to differences in economic performance. In those days, of course, both countries traded primarily with the United Kingdom, and trade between them was not overly important. Some of the shocks – see the Australian financial crisis of the 1890s – were nastily asymmetric.

(Here is a link to an earlier post on the longer-term developments in the NZD/AUD exchange rate.)

What about now? We largely share the same banks, but not the same banking system (having different currencies and different regulators). Australia is New Zealand’s largest trading partner, but it is by no means a dominant partner (and some of the trade is simply commodity exports – oil notably – where it really doesn’t matter if the product is shipped to Australia, or to, say, Singapore or Japan.) Foreign investment flows are substantial, although in terms of Australian foreign investment in New Zealand the largest single component is the banks.

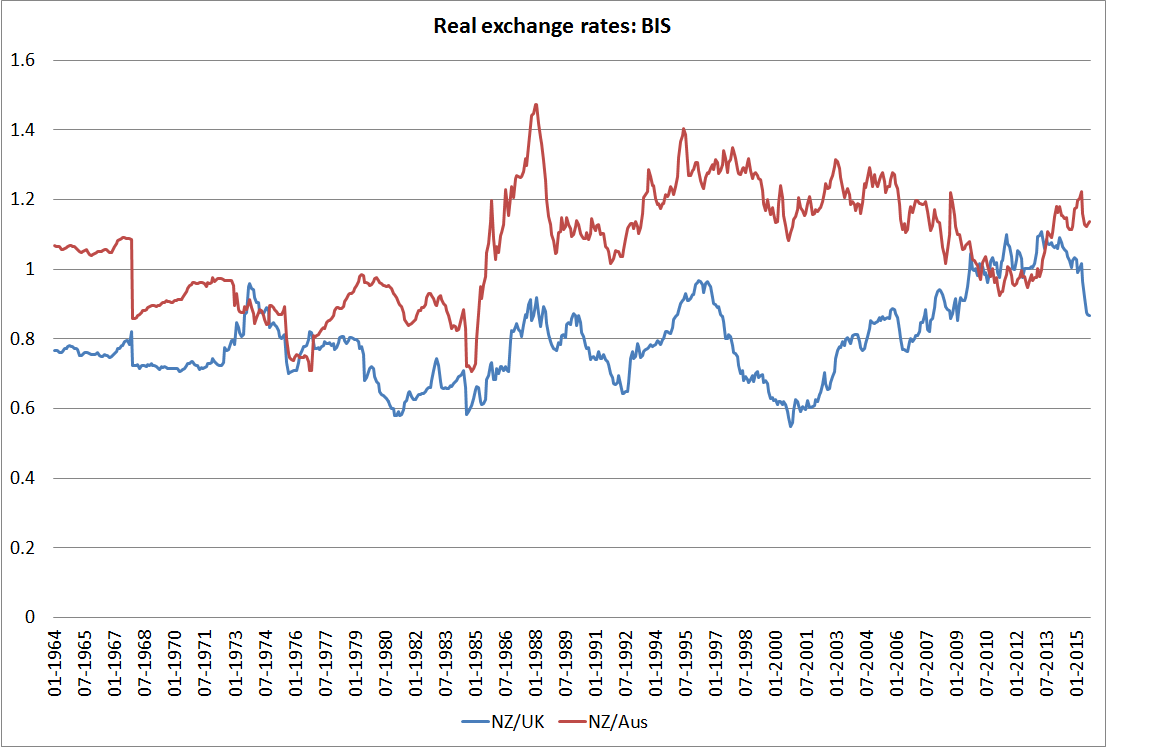

Klein argues that we do just fine with separate currencies, but I suspect he undersells the possible costs and benefits in the economic case for a common currency. If the NZD/AUD is typically one of the least variable of New Zealand’s exchange rates, it is much much more variable than the exchange rate between, say, the Netherlands or Germany. In just the last three years, the monthly average NZD/AUD exchange rate has fluctuated between 79c and 98c – a difference of around 25 per cent. Commodity exporters in the two countries have to live with that sort of variability (and more) in world markets for those products, but in the rest of tradables sectors most of the pricing variability comes through the nominal exchange rate. Economists haven’t been very successful in identifying the empirical magnitudes of the costs of exchange rate variability, and Klein usefully reminds us of the cases of Hungary and the Czech Republic which, even with floating exchange rate, have become highly integrated with Germany (gross exports to Germany in excess of 20 per cent of each country’s GDP, compared with well under 10 per cent of New Zealand’s GDP in exports to Australia).

Nonetheless, it doesn’t seem plausible that the degree of variability in the NZD/AUD exchange rate is not reducing the amount of trade between the two countries to some extent. Much of the integration of Hungary and the Czech Republic with Germany is, as he points about, about large scale FDI by the highly capital intensive (and highly internationalised) German car industry – a scale of manufacturing that neither New Zealand or Australia has. Fluctuations in the exchange rate can be managed within the balance sheets of the car companies themselves (and for them, FDI is often a way of managing the variability of exchange rates). But that is not an option for smaller producers. Typical Australia firms considering supplying New Zealand, and vice versa, have to manage themselves the still-substantial fluctuations in the exchange rate, in a way that small firms in the Netherlands don’t face in dealing with Germany, or those in the South Island don’t facing in dealing with the North Island. Physical distance is still a barrier that is not going away, but it is hard to believe that the exchange rate is not also an obstacle to growing that foreign trade. The overall effect on potential GDP might be small, but it must be bigger for New Zealand than for Australia, and….after our performance in the last few decades, every little would help.

But the other side of the picture is interest rates. As Klein notes, we have had similar inflation rates (actually Australia’s have been a bit higher, reflecting the higher inflation target) but real interest rates in New Zealand have been persistently higher than those in Australia. There have been brief exceptions, but consider the current (not unrepresentative) situation: Australia’s policy interest rate is 2 per cent, and its inflation target is 2.5 per cent, while our OCR is 2.75 per cent against an inflation target of 2 per cent. Putting an Australian interest rate on the New Zealand economy in the last 20 years would have been a recipe for rather more rapid credit growth, a bigger boom, higher inflation, and a more serious risk of a nasty economic and financial adjustment somewhere down the track.. That is, after all, pretty much what happened in Ireland and Spain, where a German (or Franco-German) interest rate was put on economies that typically needed rather higher interest rates.

It is why, unless we are signing up to a full political union with Australia, I’d be pretty reluctant to think that a common currency was a reasonable proposition, even though such an arrangement might boost real trade. Perhaps it would be different if we’d seen a couple of decades in which New Zealand’s real interest rates had persistently averaged very close to those in Australia.. And even then, there would still be that nagging “are you sure about what you are getting yourself into”.

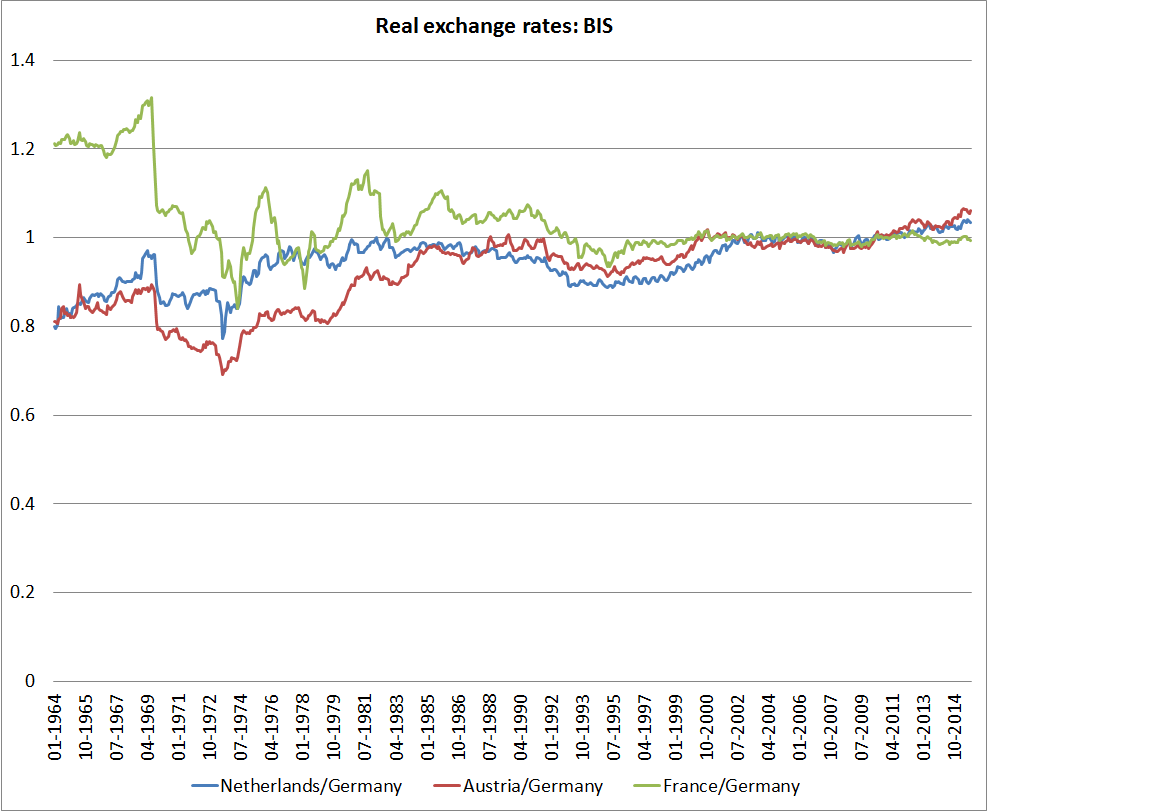

After all, one could easily look at France, Germany, Austria, and the Netherlands and think that a common currency and single policy interest rate worked fine there. Real exchange rates had been pretty stable for decades (in contrast to, say, NZ/Australia or NZ/UK real exchange rates).

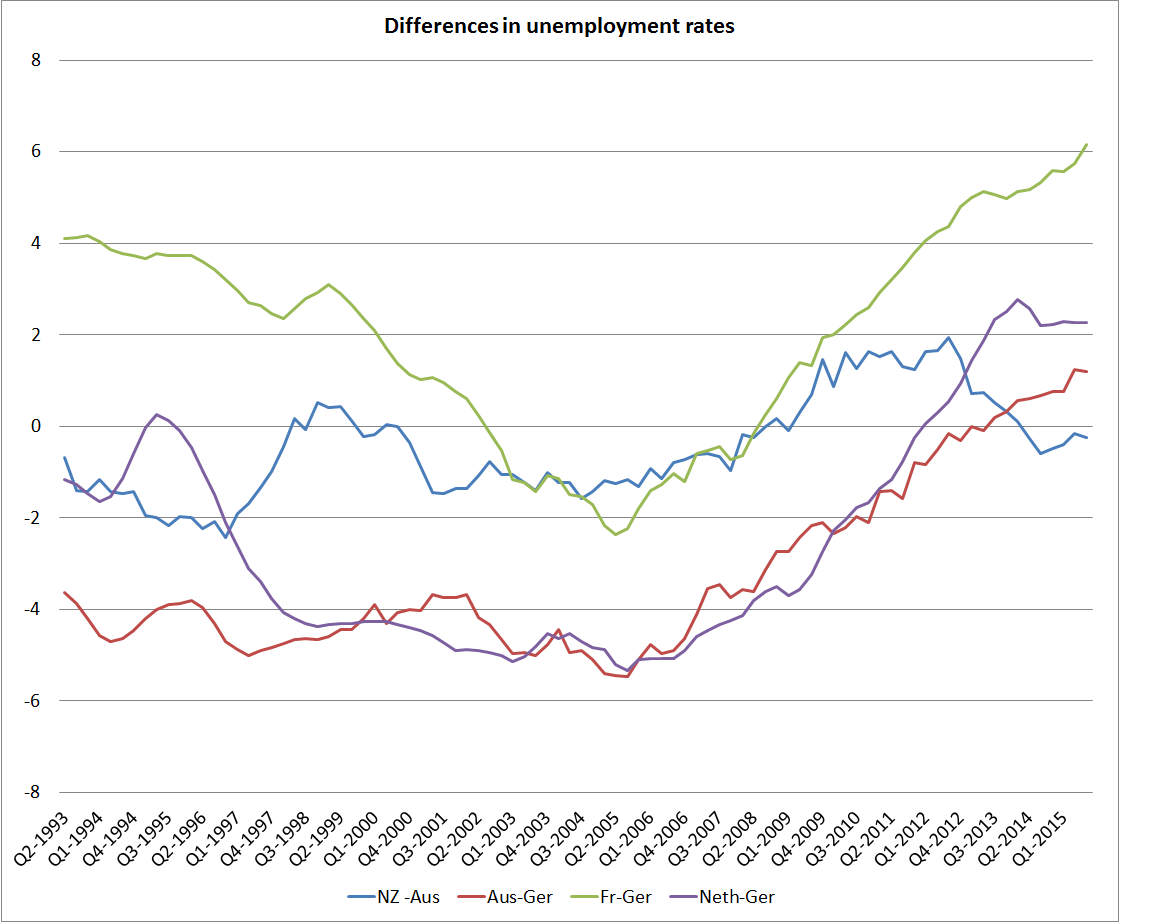

But notwithstanding that, or perhaps even because of it, the unemployment rates in New Zealand and Australia have tracked materially more closely over the last 20 years or so (data for all countries only exists since 1993) than the unemployment rates of France, Austria, or the Netherlands have tracked with that of Germany. If stabilisation is a concern – and it is usually does count for rather a lot in modern macro and modern politics – it isn’t obvious that the euro has necessarily been a great economic choice even for this core group of countries. In principle, microeconomic policy can deal with these difference, but somehow New Zealand’s and Australia’s arrangement look practically better – not optimal necessarily (few things are) but not too bad as things are.

Then again, if your countries are merging, and becoming a single state none of that may matter. But there has never seemed much public appetite for that in Europe, and perhaps even less now than there was six months ago.

Michael, I’d be interested in your thoughts on the costs and benefits of an economy that is very flexible, and reasonably capable of adjusting internally to external shocks (eg, Hong Kong), fixing or stabilising its currency in some way. (I am not suggesting NZ is such an economy, though I guess many might wish that it were.)

LikeLike

Looking at the cycles in Hong Kong unemployment (back to 81 on the HKMA website) they look, if anything, slightly bigger than those for NZ (even bearing in mind our huge “cycle” in the disinflation/structural change period. But then their peg- and the persistence with it – were political as much as anything. They get the worst of both worlds, pegged to an exchange rate of a country they aren’t closely integrated with.

I suspect NZ and Aus probably would be ok together if, but only if, the neutral real rates converge. Even our terms of trade cycles, back 100 years or more, have been pretty similar (biggest divergence was the last few years).

LikeLike

Michael, the FT blog seems to indicate the composition of capital flows might play a material part in successful economic integration and macroeconomic outcomes for small countries next to big ones e.g. FDI from Germany into Eastern Europe relative to cross border bank flows into the euro periphery. More broadly, looking at the aggregate data on NZ, I think about two thirds of external liabilities comprise ‘portfolio’ and ‘other’: is that in any way an issue in relation to NZs economic outcomes? Is there such a thing as a ‘right’ mix of inward capital flows? any thoughts appreciated

LikeLike

Interesting question. Most of out net capital inflow is either bank offshore debt funding or govt offshore debt funding. I argue that that reflects the combination of rapid population growth in the context of modest savings rates. We need to borrow to finance the houses, roads, shops etc that a fast-growing population needs (as it did in Spain). But at the same time those pressures on scarce resources drive up our real interest rates and real exchange rate, tending to make business investment here (esp in the tradables sector) relatively unattractive. I argue that we’d get better outcomes (les debt, more equity, and higher business investment per capita, higher exports, and higher per capita incomes) if we had rates of population growth more like those E European countries. In the EU case, the Spanish exacerbated their problems – excess demand didn’t flow into higher interest rates – since they got the German one – but into the mix of higher inflation (which actually reduced their real interest rates further) and the extraordinarily large current account deficits.

ALso fair to note that NZ’s external debt has been large for 25 years (and not getting larger relative to GDP), whereas Spain’s blew-out dramatically in the 00s.

LikeLike

Thanks Michael, appreciated – much to ponder but for now, the cricket match requires attention!

LikeLike

The other option to borrowings is to sell state assets to fund infrastructure. However in this current global low interest rate environment it is likely better to borrow rather than to sell state assets. The government can borrow at a much lower interest rates than current govt bond rates if Wheeler wasn’t so stubborn to hold interest rates up higher than it needs to be.

LikeLike

Our high interest rates cannot be due to scarce resources. Our interest rates are highly influenced by the RB and not by external investors as evidenced by how closely related the OCR is with the 90 day bank bill rate. You can’t have a country with huge mineral, metals, oil and grass fed wealth the size of Japan and only 4.2 million people(only 1 million working) and savings of $200 billion(cash and kiwisaver) and say New Zealanders are poor and poor savers.

LikeLike

Australia fully supports a common currency as long as it is the Australian dollar and managed by RB Australia.

LikeLike

But then we should only go into such an arrangement if we are confident enough the two economies are so similar, and that NZ will never have a severely adverse shock Aus does have, that it doesn’t make much difference who runs it. Being 85% or more of the combined Aus/NZ economy, whoever legally runs it Aus conditions will (and should) dominate.

LikeLike

Michael, thanks for the response above. To take my query a little further, do you have any thoughts on whether there is any trade-off between the internal instability that comes with a stable/fixed exchange rate and the possible benefits for the externally exposed tradables sector? Hong Kong may have had less internal stability, but what about its tradables sector, and overall, growth?

I recognise that the floating exchange rate probably buffers commodity exporters more than if buffets them, and that the empirical evidence on deleterious effects from exchange rate instability on the tradables sector are hard to find. But is the latter because it’s the multi-year swings in the exchange rate that do the damage (if there is any damage) and on those we have only a handful of data points?

LikeLike

Bruce

The problem with using HK is the one I alluded to before – it pegged to the USD but its trade wasn’t US oriented. Look at the BIS real exchange rate series, and HK has had materially more exch rate variability (cyclical amplitude) than NZ.

But yes, the general point you are making is fine – it is in essence my point that much of the non-commodity export sector looks as tho it should do better with a common currency, But be wary of how much difference: perhaps it would raise our exports/GDP to Aus by 1 or 2 pps (worth having, but if we get a nasty adverse shock and have five years of unemployment well above the NAIRU, the gains from those exports could dissipate rather quickly in a cost-benefit analysis (and while our neutral int rate is higher than that of Aus, adopting a common currency would increase the chances of a nasty Irish or Spanish (or Aus 1890s) recession at some point.

LikeLike