Really ever since the end of the immediate financial crisis in the first half of 2009 there has been a hankering – often more than that – among some central bankers, some former central bankers. and some agencies that associate with and support central bankers (ie the BIS – Bank for International Settlements) for things to “get back to normal”. What leaves these people particularly uncomfortable is the level of official interest rates, which in most of the major advanced economies (and quite a few smaller ones) have been very close to zero (sometimes modestly negative). And it is now almost nine years since the end of that first intense crisis phase. And, at least in nominal terms, there had been no precedent for such low official interest rates.

It was, perhaps, an understandable reaction in the immediate aftermath. I certainly shared it then. I was on secondment to The Treasury, and recall talking things over with a colleague who had previously been at the Reserve Bank. We agreed that the Reserve Bank (Alan Bollard personally) appeared to have done a thoroughly excellent job in cutting the OCR aggressively during the crisis/recession, but that it seemed likely – and appropriate – that many of those cuts should soon be reversed. We welcomed early indications that that was exactly the Bank’s intention. I also recall pointing out to colleagues that bond markets appeared to be pricing a reasonably prompt, and near-full, rebound in policy interest rates (not just in New Zealand but in range of advanced economies).

It all made sense at the time: very sharp cuts in policy rates had been appropriate in a sharp economic downturn accentuated by an extreme rise in uncertainty and liquidity preference, but once those fears eased (with time and various direct interventions) it didn’t seem obvious that anything very structural about economies had changed. If so, it wasn’t obvious that future average interest rates would be much different from those of the previous decade or two.

That was then. But now it is 2018. And the median policy interest rate among OECD central banks (that have their own monetary policy) is about the same now as it was in the trough in 2009. Some individual countries have lower rates now, and some higher (the US notably), some have tried to raise rates and had to reverse themselves (eg New Zealand twice, Sweden, and the ECB). No OECD central bank has simply left its policy rate unchanged since 2009.

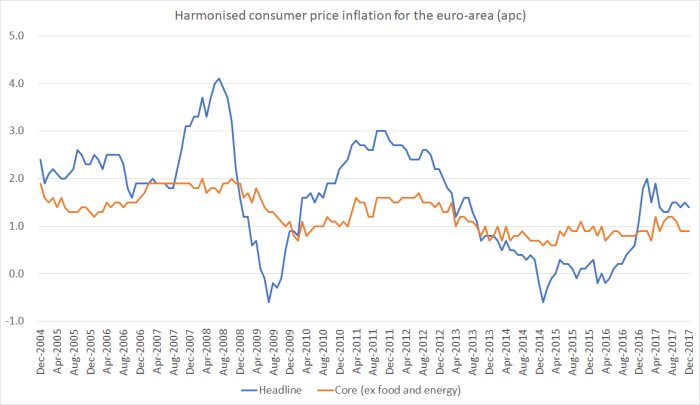

And throughout that period inflation (headline and core) has remained pretty quiescent. Here is an indicator of core inflation across OECD countries (well, monetary areas, so the euro-area is a single observation).

Not all central bankers like to own up to paying any attention to (indicative) measures of excess capacity, but over the decade unemployment rates have typically dropped back quite slowly (as in New Zealand) and output gaps are still estimated to be around zero, often negative. As a reminder, these outcomes have come about with interest rates very (historically) low. They aren’t themselves an argument for much higher policy rates.

And yet the anguishing continues. Some of it has become almost pro forma in nature. The former Governor of the Reserve Bank used to regularly talk about how “extraordinarily stimulatory” he thought interest rates were and openly hankered for “normalisation” here and abroad. His temporary successor (the “acting Governor”) throws in occasional references along similar lines. I suspect it makes them more reluctant to lower the OCR than they otherwise would be but – in fairness – they do eventually seem to be led by the data rather than by their mental model of how the world should work.

Others seem to want to translate the model into action. I noticed one example yesterday, in the form of a new column by former ECB board member (in effect he served as chief economist) and former Bundesbank Deputy Governor, Jurgen Stark. Former BIS chief economist (and former Bank of Canada Deputy Governor) Bill White has had a succession of speeches and articles along similar lines, and his latest was published in the Financial Times a few days ago.

Stark opens his argument with the recent sharp dip in US share prices which, he asserts

revealed just how addicted to expansionary monetary policy financial markets and economic actors have become.

Possibly, but since the S&P this morning is still a touch higher than it was on 31 December 2017 – a mere seven weeks ago – I’m not sure it is particularly compelling evidence.

He moves to a somewhat more macroeconomic argument

The fact is that ultra-loose monetary policy stopped being appropriate long ago. The global economy – especially the developed world – has been experiencing an increasingly strong recovery. According to the International Monetary Fund’s latest update of its World Economic Outlook, economic growth will continue in the next few quarters, especially in the United States and the eurozone.

I’m not sure we should be particularly encouraged that “economic growth will continue in the next few quarters”, but nor am I sure how it is relevant. First, projections of continued growth – even growth a bit faster than medium-term potential growth – are, in part, reflections of – and, at very least, consistent with – the low interest rates. And second, inflation – or some other nominal variable – is supposed what central banks focus on first and foremost.

The US Federal Reserve has been raising interest rates, but it isn’t enough for Stark.

But the Fed’s policy is still far from normal. Considering the advanced stage of the economic cycle, forecasts for nominal growth of more than 4%, and low unemployment – not to mention the risk of overheating – the Fed is behind the curve.

It isn’t clear that “the advanced stage of the economic cycle” means much more than that it has been a few years now since the US had a recession. Nominal GDP growth – currently around 4 per cent – shows no sign of racing away, and has averaged 3.8 per cent per annum since 2010. And core PCE inflation – the Fed’s target variable – is currently 1.5 per cent, while the Fed’s self-chosen target is 2 per cent. Yes, the unemployment rate is low, but as on the one hand some analysts suggest the headline number is underestimating residual labour market slack, and on the other the Fed is actually raising policy interest rates (and is expected to continue to do so), it is hard to find any backing for Stark’s claim that the Fed is “behind the curve”. And even if, for example, the latest round of ill-judged fiscal stimulus does end up providing the boost that lifts inflation nearer target, it is hard to believe (and there is no obvious evidence for) that inflation expectations are so weakly anchored that a lift in inflation to target (after all these years) will destabilise expectations in a dangerous and damaging way. This isn’t 1974.

But if the Fed is bad, on Stark’s reckoning, many other advanced economy central banks are “even worse”

The ECB, in particular, defends its low-interest-rate policy by citing perceived deflationary risks or below-target inflation. But the truth is that the risk of a “bad” deflation – that is, a self-reinforcing downward spiral in prices, wages, and economic performance – has never existed for the eurozone as a whole. It has been obvious since 2014 that the sharp reduction in inflation was linked to the decline in the prices of energy and raw materials. In short, the ECB should not have regarded low inflation as a permanent or even long-term condition that demanded an aggressive monetary-policy response.

The ECB’s policy is also out of line with economic reality: the eurozone, like most of the rest of the global economy, is experiencing a strong recovery.

I think there is quite a bit to argue about over the way the ECB interjected itself into the euro crisis, and one can mount arguments – as Stark did – about the appropriateness of the quasi-fiscal policies the ECB ended up adopting. But what about inflation – the macro variable the ECB says it targets, under its treaty mandate to pursue price stability?

The ECB targets something “below, but close to, 2%” (in practice something like 1.9 per cent). Headline inflation certainly fluctuates – there (as Stark notes) and other places fluctuations in oil prices make a big difference in the short-run. But the last time euro-area wide core inflation was at 1.9 per cent was the end of 2008. And there hasn’t been any obvious sign in the last 12 or 18 months that core inflation is picking up strongly again. Now Stark is German, and activity and demand in Germany have done better than in the rest of the euro-area. Inflation in Germany is also higher than in the euro-area as a whole but on neither headline nor core measures is it as high as 1.9 per cent – and monetary policy is supposed to be set for the region as a whole, not just for the single largest national economy.

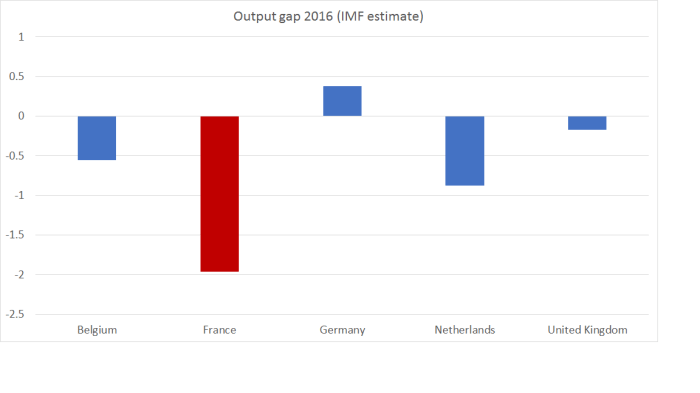

As for the “strong recovery”, things in the euro-area are certainly a great deal better than they were, but in its last published forecasts the IMF estimated that for the euro-area as a whole, there was still a negative output gap last year, and forecast one around zero this year. And that with interest rates at (historically) very low levels.

The sort of argument that Stark uses might make a bit of sense if he wanted to argue that interest rates at these levels are having no effect (on demand/activity). If they were having no effect, there might be no harm in having them higher again. But that isn’t his argument. Instead

One of those consequences is that the ECB’s policy interest rate has lost its steering and signaling functions. Another is that risks are no longer appropriately priced, leading to the misallocation of resources and zombification of banks and companies, which has delayed deleveraging. Yet another is that bond markets are completely distorted, and fiscal consolidation in highly indebted countries has been postponed.

This “misallocation of resources” line often pops up in commentaries like Stark’s (it is there is White’s FT article as well) although it is never clear quite what is meant. It really only seems to make much sense if one can confidently assume that their model – in which interest rates should be so much higher – is correct, and thus relative to that benchmark choices are made differently than they would be in the alternative universe. Perhaps it is right, but we have no very obvious means of knowing that it is – after all these years. If neutral rates are lower than they think, “misallocations” might just be “choices”.

And the claim seems to involve the suggestion that some real activity is now happening which wouldn’t happen if only interest rates were higher. Stark actually states it more or less directly: in his view current policies have ‘delayed deleveraging”, and the “fiscal consolidation in highly-indebted countries has been postponed”. But had a whole succession of governments actually been under more pressure to run lower deficits/larger surpluses, cutting their debt levels, where and how does he suppose the replacement demand might have come from? It isn’t as if any monetary area in the advanced world has had consistent excess demand this decade. There are, of course, standard responses about confidence effects, and private demand replacing public spending – at times even the New Zealand experience in the early 1990s is cited – but those offsetting adjustments typically take place in part through lower interest rates and a lower exchange rate (governments cut spending, central banks ease monetary policy, and additional private spending is crowded in ). Stark’s model rules out that process almost by construction. Much the same story is likely to hold for corporate or household deleveraging: the process by which it occurs usually involves (incipient) weaker overall short-term demand and activity. Oh, and if Stark was right and the ECB raised policy interest rates in the current climate and it seems reasonable to expect that the euro exchange rate would be higher. There is no guarantee about exchange rate effects, but (probabilistically) it is another channel that would weaken demand and activity further.

I’m not convinced there is a particularly good case at present for the ECB to still be buying large volumes of bonds. But the case for higher interest rates – across the whole euro-area, or even just for Germany – seems threadbare in the extreme.

Stark ends his article this way, generalising beyond just the ECB.

Today, monetary policy has become subordinate to fiscal policy, with central banks facing intensifying political pressure to keep interest rates artificially low. As the recent stock-market turmoil shows, this is drastically increasing the risk of financial instability. When more – and more severe – market corrections take place, possibly affecting the real economy, what tools will central banks have left to deploy?

The evidence for these claims seems thin at best. There has certainly been a huge increase in net government debt in some of the larger OECD countries in the last decade – France, Italy the US, the UK, Japan, although not Germany – but it isn’t obvious that monetary policy is playing out materially differently in those countries than in places like Switzerland, Sweden or Israel (where net debt has fallen as a share of GDP over the decade – and where official interest rates are very low) or in places like New Zealand or Canada that have seen only modest increases, from low bases, in the levels of net public debt.

And what of the claim that “interest rates are artificially low”? Well, that simply seems to impute far too much power to central banks. Central banks set very short-term interest rates, and over those short-term horizons no one else can do much about it. Central banks do not set long-term interest rates and typically have very little direct influence on extremely long-term interest rates. The longest German inflation-indexed government bond matures in 2046: the current yield on that bond is negative. Perhaps Stark would argue that the ECB bond-buying programme directly or indirectly influences those yields. But in most countries, central banks aren’t engaged in bond buying programmes at all, and very long-term nominal and real interest rates are extremely low. Swiss 10 year conventional bond yields, for example, are basically zero. US 30 year inflation-indexed bonds (and the US currently has by far the highest interest rates among the larger economies) are currently around 1 per cent. And even in little old New Zealand – typically with the highest real interest rates in the advanced world – our 22 year government indexed bond is yielding just slightly over 2 per cent (down from 5 per cent 20 years ago). It is a global phenomenon, and it can’t just be down to the (misguided or otherwise) choices of central banks. Rightly or wrongly, some mix of demographics, weak expected productivity or whatever, seem to be at work. Central banks might not fully understand what is going on – nor might anyone else – but it would brave, nay foolhardy, for the central banks of the world to stake out a stance that relied on a completely different view (“interest rates should be much higher”).

Which, of course, brings us to that very last line in Stark’s article. When things really go wrong, what tools will central banks have left to deploy?

That is, of course, a serious issue, and it is one that ever central bank, every finance ministry, every Minister of Finance should be worrying about. After all, they’ve had years of notice of the issue now. When the next serious recession happens – and one will happen again – it looks as if most central banks in advanced countries will have little or no room to cut interest rates, the typical counter-cyclical stabilising policy instrument. Even countries like New Zealand and Australia will have far less room than typical (the Reserve Bank could probably cut the OCR by 2.5 percentage points, but had to cut by 6.5 percentage points after the last recession). Markets know that constraint, which in turn risks exacerbating the severity of the downturn once it begins. Most major advanced countries also have very little fiscal leeway left (whether as a matter of technical/market limits or political limits).

I’m all for growth-enhancing structural reforms. They would benefit countries now, and in the future (both lifting demand and activity, and raising market assessments of neutral interest rates). There are few signs of those sorts of reforms in most countries (indeed, often – probably including New Zealand – the reverse). But what is the best path now, around macro policy, to provide greater leeway when the next serious recession comes?

On monetary policy, the standard prescription is pretty clear: higher inflation expectations are the only thing monetary policy can do to underpin higher medium-term nominal interest rates. In other words, the best things central banks could have been doing in recent years was to aggressively pursue higher demand and inflation (there being no sign that weak inflation was a result, all else equal, of strengthening productivity growth). Cut interest rates so as to later raise them by rather more (the opposite of the Reserve Bank strategy which turned out to be, in effect, “raise interest rates only to cut them more later”). Few or no central banks have had the courage to adopt this course (or to openly consider higher inflation targets), partly (I suspect) transfixed by the desire for “normalisation”. And what of fiscal policy? In some of the countries with large deficits and high debt, it might well make sense to look to secure fiscal consolidation (giving, among things, more room for countercylical stimulus in the next recession). For a country like the US, more or less back to a fully employed economy, that makes particular sense. But it is far from obvious that the same logic follows in France or Italy (still with negative output gaps): all else equal, fiscal consolidation will tend to worsen economic activity now, and yet euro-area monetary policy has all but reached its limits and can provide no offset. Increasing the chances of a new recession now to slightly reduce the chances/severity of one five years hence is, to say the least, a difficult call (economically or politically).

At present, I’m reading one of the numerous books on my shelves about the politics and monetary policies of the inter-war period. It is, I think, now widely accepted that monetary policy problems were at the heart of the seriousness of the Great Depression in many of the major economies (even New Zealand for that matter); in particular the way the Gold Standard had been run – and patched back together (“normalisation”) during the 1920s after the extreme disruption of World War One.

Some of the abler observers in the late 1920s realised that problems were building up – including that perhaps two-thirds of the world’s monetary gold being held in France and the United States, without the natural stabilising mechanisms being allowed to work freely – but there was never a sufficiently strong shared sense among policymakers that something needed to be done, and promptly. In the US, for example, there was constant unease about the stock market boom, and thus a reluctance to allow the Gold Standard mechanisms to work as they should (when gold floods in interest rates fall, demand increases etc). As I read through the book, I was reminded of the Governor of the Bank of England deliberately accentuating the risks to the UK peg to gold, to keep the pressure on British ministers to make large fiscal cuts (that were probably never substantively warranted). And, even when the UK finally, reluctantly, went off the gold peg in September 1931, instead of embracing the opportunity, for some time all the great and the good (even Keynes) were focused on generating conditions that would warrant a return to gold. Economic historians are now pretty clear that monetary expansionism – made possible as countries slowly, and mostly reluctantly, broke the link to gold – was a significant part of economic recovery in the 1930s.

Historical parallels are never exact but is hard not to see the constant hankering for “normalisation” – and vigorous calls for it in some circles – and even unease about asset prices, as akin to the well-intentioned policy mistakes of the late 20s and early 30s, leaving our world badly exposed when and if the next serious downturn occurs.

(And if – as White and Stark claim – financial stability is your real concern, use financial regulatory instruments and agencies to attempt to tackle those issues directly. Sometimes monetary policy “mistakes”/shocks can be closely linked to subsequent financial stability problems. Arguably that was the situation in Ireland and Spain in the 2000s – interest rates that suited German conditions but not Irish or Spanish ones – but I doubt anyone can point to a single example today of an advanced economy dramatically overheating as those two did.)

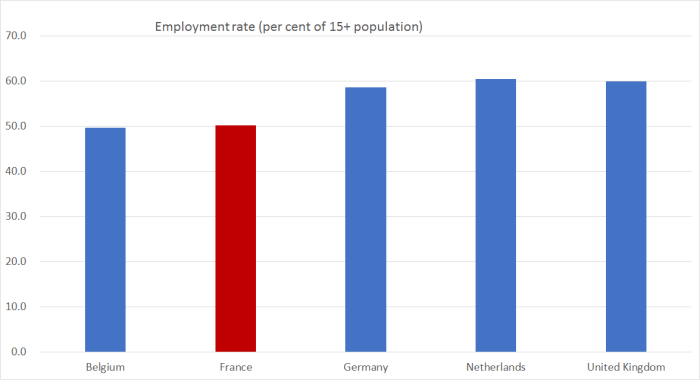

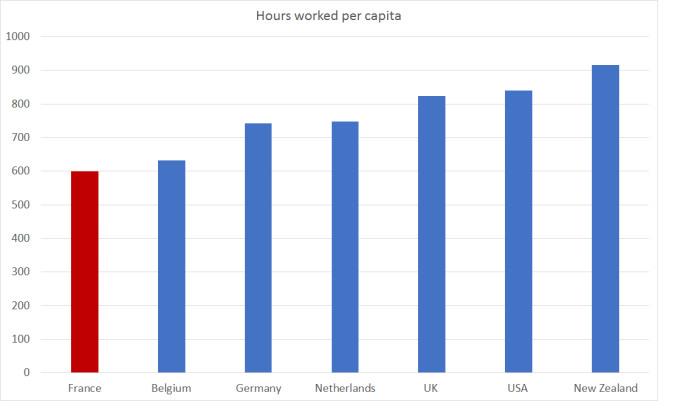

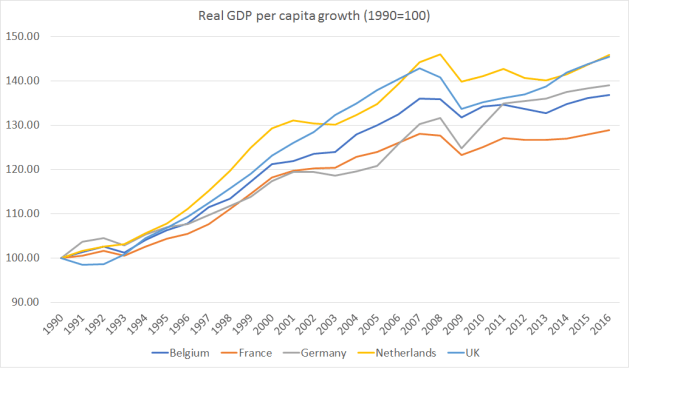

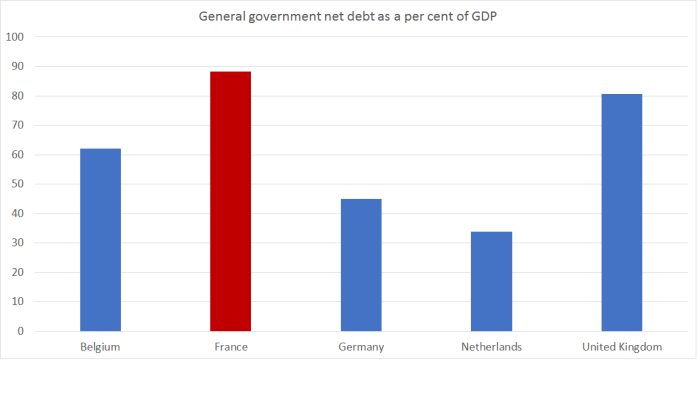

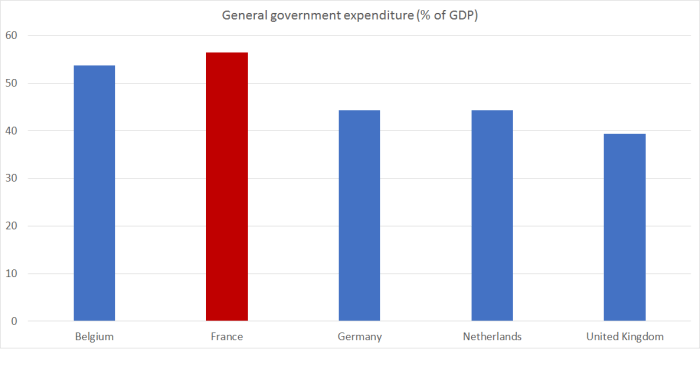

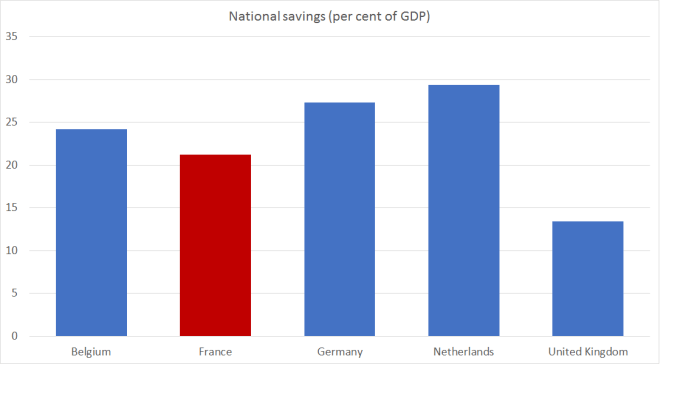

France is, again, the worst performer.

France is, again, the worst performer.

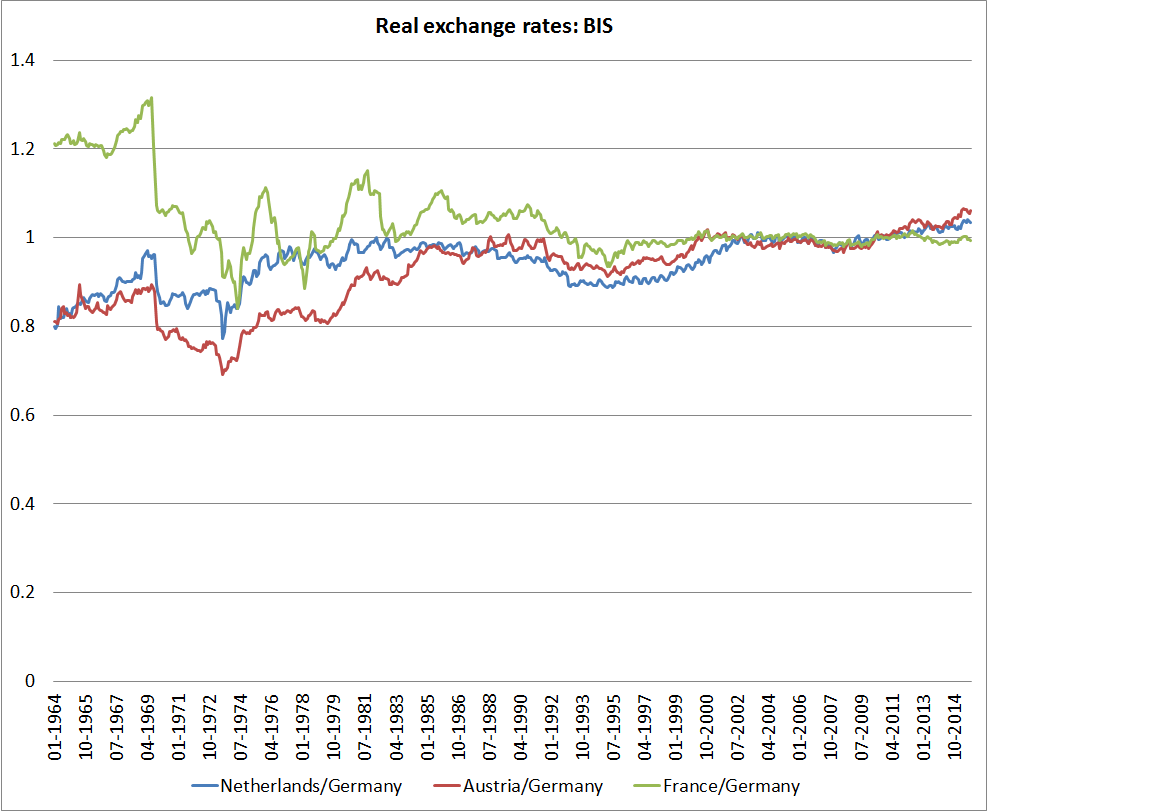

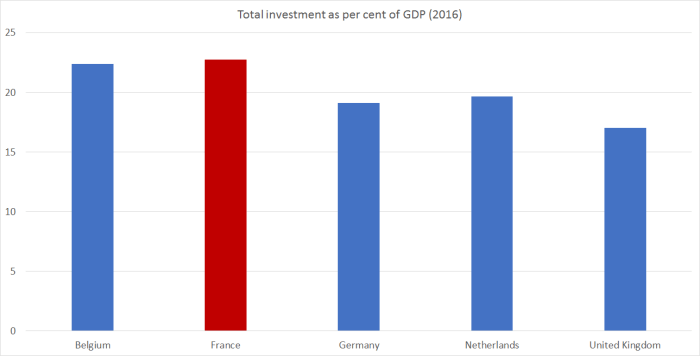

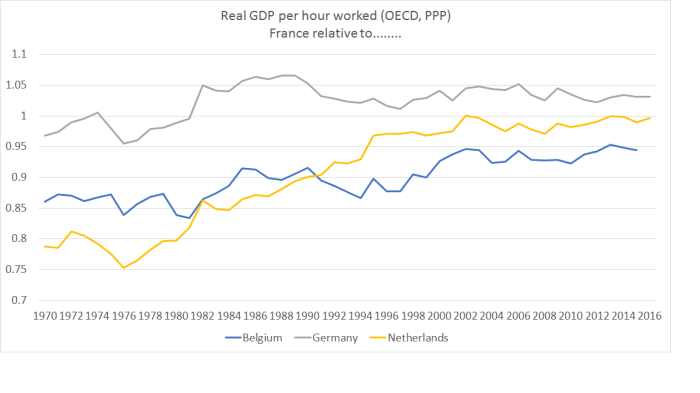

France caught up over the first few decades and has largely held its own since, at least relative to these comparators.

France caught up over the first few decades and has largely held its own since, at least relative to these comparators.