I’ve been reading recently a couple of books by former officials, the common theme of which is probably “avoiding the next collapse”.

Mohammed El-Erian spent much of his career at the IMF, and at one stage was even touted as an outside possibility to become Managing Director of the Fund (being Egyptian when people were trying to break the European lock on the job). These days he works for Allianz, the big German insurance and asset management company, and previously ran PIMCO, a major subsidiary of Allianz. I’ve always been a bit skeptical of El-Erian but picked up his book The Only Game in Town – which a reader had kindly passed on – with interest. His key idea is that there has been too much reliance on central banks in the last decade to stimulate activity, and that countries need a wider range of policy responses, better targeted at the underlying issues, to get us back on a more sustainable path.

Initially it sounded plausible, and there is some interesting material in the book, but I came away unconvinced that El-Erian really had much of significance to add to the current debate. A key part of his argument rests on the not-uncommon line that global monetary policy is incredibly stimulatory (the same line Graeme Wheeler runs here), which gives little weight to the idea that the neutral or natural rate of interest might have changed (fallen) quite substantially. The fact that advanced country inflation is so low, despite the low interest rates, suggests there isn’t very much stimulation going on. And there are external reasons to think that neutral interest rates have fallen – notably the falling rates of population growth (involving less need for new capital) and the declining rate of productivity growth (also likely to associated with a reduced demand for new capital). If so, central banks haven’t been the heroes of the last few years (as El-Erian’s tale has it), but rather bureaucrats sluggishly recognizing and reluctantly adjusting to the changing external conditions – often enough champing at the bit to take interest rates back up to levels that might have been appropriate a decade ago, but simply aren’t now.

And yet in the index to El-Erian’s book there are no references to neutral or natural interest rates (let alone Wicksell), and no references to demography or population growth rates. In the text there are many more references to PIMCO than to productivity.

Of course, markets have often also been slow to recognize what has been going on – and probably no one has a fully convincing answer – but most central banks deserve little of the praise El-Erian bestows on them.

Of course, his praise of central banks is partly a rhetorical device – a stick with which to beat governments, most of whom have done little in the way of structural reform in recent years. But he doesn’t actually have much specific to offer on boosting productivity growth. And I’m also more than a little sceptical because of El-Erian’s enthusiasm for multilateral solutions (“the world needs to return to the wisdom of strong multilateralism’) – perhaps a not unexpected enthusiasm from a former senior IMF official and quintessential internationalist. In a book published only a few months ago, El-Erian laments the seeming inability of the EU to deliver on their “ever closer political union”: perhaps he might lament it, but few citizens of European countries seem to. He can’t seem to face the alternative – that the process might actually be about to head in reverse. Perhaps even less relevantly, he calls for reforms of the IMF as key part of his list of desirable changes. Whatever the answers to the current problems ailing the world, I find it difficult to see that:

- giving the IMF more money

- giving China more say

- removing the European lock on the MD job, and

- strengthening the ability of the Fund “to name and shame countries”

is a material part of the answer. What legitimacy, one might reasonably wonder, might the IMF have? What interests does it pursue? And even if it had legitimacy, none of those measures are ever likely to materially change economic outcomes for the better.

But the main point of this post was to write about The End of Alchemy, by Mervyn King, the former Governor of the Bank of England. It is a book prompted by the financial crisis of 2008/09, but it isn’t directly about that crisis. It isn’t a memoir. King suggests that such books are “usually partial and self-serving” – no doubt, but surely readers can compare and contrast and reach their own judgements (for example, I found his former boss, Alistair Darling’s account of the crisis very useful) – and reckons that future historians can have his account “when the twenty-year rule permits their release”. Of course, British taxpayers can’t force former Governors to write a memoir, but when a longstanding Governor (including through the biggest crisis in modern times) of considerable intellect and capacity with the pen retires laden with state honours (Knight of the Garter and peer of the realm – Lord King of Lothbury) perhaps it wouldn’t have been unreasonable to have hoped for a bit more accounting for the crisis and his role in it. Ben Bernanke’s book won’t be the last word on the US crisis, but the debate is better for it having been written.

Following the end of his Bank of England term, King visited New Zealand a couple of years ago, and I had the opportunity to participate in a couple of roundtable discussions with him at the Reserve Bank. I wasn’t the only person who came away from those sessions struck by his reluctance to acknowledge any mistakes whatsoever. Even tactically, after such a costly banking crisis and disruptive few years, one might have expected some minor concessions, but there was nothing. Senior people tend to look better, more credible and authoritative, for being seen to recognise that all humans – even them – make mistakes, even if just small ones. It was, for example, no secret that in the years prior to the crisis King had had little or no interest in the financial stability functions on the Bank of England.

In many ways King’s book is much more ambitious than any memoir, and it is a stimulating contribution to a different debate: how should we best organize banking systems and financial regulation to produce the best long-term outcomes for the countries of the world. It is quite ambitious in its reach – both in the material he covers, and in audience he aims at. It is explicitly not a book aimed just at economists, but at “the reader with no formal training in economics but an interest in the issues”. I suspect the book will stretch such readers, but mostly in a good way – even if I disagree with him in a number of areas, I’d recommend it. There is a lot of context and background material that is often taken for granted (as well as fascinating bits of obscure history such as the monetary arrangements of French overseas territories in WWII), and King writes fluently and authoritatively. The downside, perhaps, is that there is so much background, that King devotes less space to fleshing out the case for his alternative perspective than might have been desirable.

There is a lot of stuff in the book that I like. King is very skeptical of central banks’ forecasting capabilities – which, of course, didn’t stop him presiding over the development of the current forecast-based system at the Bank of England – and has long been recognized as a sceptic of the euro. He is one of the few senior (establishment) people in Europe willing to openly discuss – and not deplore – the possibility of a break-up of the euro.

And some of his practical policy suggestions seem very much along the right lines. Higher capital ratios for banks, with an important role for a more constraining leverage ratio (a tool used by most bank regulators, but eschewed by our own Reserve Bank), are appropriate responses to the high (demonstrated) risk that governments will bail-out failing banks, and to the limited ability of apparently-sophisticated capital models to truly capture the changing nature of the risks around complex credit exposures. Higher required capital ratios, especially for large banks, come at little or no efficiency cost, especially in jurisdictions where the tax system treats debt and equity reasonably neutrally. And higher liquidity requirements are a prudent part of any system in which, come a crisis, a central bank will act as lender-of-last-resort in the face of intense liquidity pressures. Requiring banks to hold a larger proportion of liquid assets, so that they can’t just “force” central banks to lend on assets that are highly illiquid even in good times (which is what happened, including in New Zealand, in 2008/09), is a step in the right direction. Most central banks have moved this way since the 2008/09 crisis, and market pressures have (for now) worked in the same direction. King suggests that what has been done already is not enough.

But I’m still left uneasy about some key aspects of his argument.

For example, he puts a lot emphasis on the point that credit to GDP ratios are a lot higher than they were a few decades ago (although in places like New Zealand and Australia data suggest they may still be lower than they were in the 1920s). In this context he discusses the possible contributions of falling real interest rates and a liberalization of domestic and international financial systems. But in many countries, the largest single component of domestic credit is lending for housing. And in many countries – the UK and New Zealand among them – it is now widely recognized that planning restrictions have created artificial scarcity in urban land supply, bidding the prices of urban land and houses. Younger generations purchasing houses need to borrow more to buy such houses (in effect, borrowing from the older generations, including – indirectly – the sellers), That raises the level of gross credit in an economy, and perhaps even erodes the financial stability of the system, but it is best understood as an endogenous response to the binding planning restrictions (especially in combination with population growth pressures), not as something driven out of the banking system. And yet in a book of almost 370 pages there is no mention of this factor at all. Perhaps banks have aided and abetted the rigging of urban land markets by governments, but the fault surely largely rests with governments not banks.

His historical account of the evolution of central banks, and particualry of the Federal Reserve, is entirely conventional, in playing up the number and severity of the crises the pre-Fed United States experienced. But he doesn’t seriously engage with either the argument that the crises were themselves partly the outcome of the extensive regulatory restrictions the US had in place in those pre-Fed decades, nor with the experience of some other countries – notably Canada – which operated for decades with no central bank and no systemic crises. This isn’t the opportunity to review all the arguments and evidence on those issues, but on my reading King comes down far too readily on the side of the instability of the system – perhaps with some of the zeal of a convert.

In many ways, Britain itself is a good illustration of the point. Prior to 2008/09, the last really serious systemic financial crisis in the United Kingdom was that prompted by the outbreak of World War One (an episode King discusses, and which is more fully dealt with here). That crisis wasn’t really the result of any systemic weaknesses in the financial system – rather governments suddenly changed the rules of the game, having more pressing geopolitical concerns in mind. Even the crisis in the United Kingdom in 2008/09 was primarily the result of the troubled banks’ exposure to offshore markets – loan losses on UK domestic banking books never posed a systemic threat. The key offshore market, the US, was one that was highly distorted by other regulations.

King concludes his book thus

A long-term programme for the reform of money and banking and the institutions of the global economy will be driven only by an intellectual revolution. Much of that will have to be the task of the next generation. But we must not use that as an excuse to postpone reform. It is the young of today who will suffer from the next crisis – and without reform the costs of that crisis will be bigger than last time.

But I simply didn’t find persuasive the claim that the costs of the next crisis will inevitably be bigger than the last one. After all, in most countries the experience of the 2008/09 recession was much less severe than that of the Great Depression – the last really big common advanced country crisis. Perhaps this points to one of the other issues that King didn’t really address. If the extent to which GDP per capita and productivity measures are today so far below the pre-crisis trend level is all down to the financial crisis itself, and the associated failings of the financial system, then perhaps King’s case gets stronger. But he doesn’t make the case for that claim, and since the productivity slowdown was already underway well before the financial crisis, it isn’t necessarily an easy case to make successfully.

Since I got to the end of the book, the title itself has been troubling me. King is careful to define his “alchemy”

By alchemy I mean the belief that all paper money can be turned into an intrinsically valuable commodity, such as gold, on demand and that money kept in banks can be taken out whenever depositors ask for it. The truth is that money, in all forms, depends on trust in its issuer…..For centuries, alchemy has been the basis of our system of money and banking.

No one, surely, disputes the importance of trust in a market economy. But if there are distinctive characteristics of the issue as it affects money and banking, the issues around trust aren’t unique to money and banking. I trust that the food on sale at the supermarket hasn’t been poisoned. If ever widespread doubt arises about the validity of that assumption, there will be serious economic disruption. Perhaps we could prosper with a different banking system – most practical alternative suggestions seem to me unlikely to make very much difference – but the West has done quite astonishingly well with the one it has (notwithstanding the current mediocre decade).

And King simply does not seriously engage with the question of how government, bureaucracies, and “government failure” have given risen to some of the distinctive challenges around the banking system. If, for example, a tendency to bail-out failing banks is a feature of the political system, if regulators tend too easily to see things from the perspective of the regulated, and so on, how confident can we be in the robustness of alternative policy models, which depend on the active ongoing decisions of a new generation of policymakers and officials? I think King is partly right to describe the last crisis as not primarily the fault of particular individuals – many of whom were responding to the incentives they faced – but have the political and bureaucratic and market incentives really changed that much? Would, for example, Gordon Brown (keen on promoting the City of London as a global banking centre) have appointed Mervyn King as Governor in 2003 if Mervyn King had been known to be all over the issue of financial stability and actively making the case for much tighter controls on banks and the banking system? What is it that means those same incentives and constraints won’t be at work again as the memory of the last crisis fades?

King devotes some space to the debate as to whether monetary policy should be used to lean against asset price booms and the build-up of credit (or just focus on the inflation target, in the upswing, and after any bust). This was a major debate at the Bank of England – including at the Monetary Policy Committee level – as far back as the late 1990s. King seems to hanker for the “do something” camp – that perhaps “doing something” with monetary policy might have led people to reassess their future income prospects earlier, and limited the extent of the imbalances that built up. Of course, as he recognizes there were problems. In a world of national policymaking, a central bank that tried to lean against the boom would tend to see a higher exchange rate, and in some respects a more unbalanced economy.

I’ve always thought that the other problem was that – thankfully – central banks typically have a rather constrained form of independence. Had the Fed or the Bank of England – or the RBNZ for that matter – tightened monetary policy materially more aggressively during the boom, the pressures on policymakers to change the target – or the powers of the central bank – would have been great. In Britain, the inflation target is set each year by the Chancellor – I find it scarcely credible that Gordon Brown would have welcomed a years-long undershooting of the inflation target he himself had set, and not just as a result of “forecasting errors”, but as a matter of deliberate policy choice. Perhaps there is something in the old line about the job of the central bank being to remove the punchbowl just as the party is getting into full swing, but the actually the waiter can really only remove the punchbowl with the consent of the partygoers. In the last boom, there was simply no appetite anywhere for materially tougher policies – and no one knew the future, and many credit booms (even those of 00s) haven’t ended badly. King rightly stresses the importance of “radical uncertainty”, but central banks and financial regulators are no more gifted with insight or fine judgement than the rest of society. And they face institutional incentives, for good and ill, as the rest of us do.

King is clearly uneasy about the current low level of world interest rates. And in one sense, he is right to be so – we all want to better understand the underlying forces that have delivered such interest rates (not just policy rates, but the extraordinarily low bond yields). And it is also, clearly, correct that monetary policy is not an instrument that can generate the sort of faster long-term productivity growth that most countries would now welcome. But to suggest, even if only implicitly, that somehow things would have been materially better if only policy rates had not been held so low for so long seems more like wishful thinking than hard-headed analysis. If he has such analysis, it didn’t make it into the book.

It is an interesting and stimulating book, well worth reading. In a way it is shame that he overreaches. His mostly-sensible actual policy recommendations do not, to me, seem to represent anything like the sort of transformation his title implies. But nor, I suspect, is such a transformation needed.

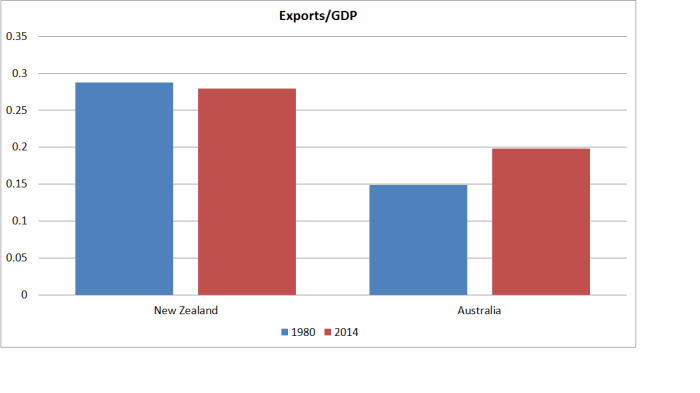

New Zealand’s export share of GDP hasn’t changed in 35 years.

New Zealand’s export share of GDP hasn’t changed in 35 years.