It is very difficult to get a good sense right now of how much excess capacity there is, here or other countries In New Zealand’s case, part of that is about the gross inadequacies of our official statistics. We are one of only two OECD countries without official monthly employment/unemployment data (the other is Switzerland) – and if this has been a long-running deficiency, it seems more striking than ever from a government that amended the central bank act to highlight the focus it wanted on avoiding as much as possible excess labour market capacity.

Of course, there is a variety of less formal, or less fit-for-purpose, partial indicators. We know how many people get the unemployment benefit but many people looking for work are not (rightly in my view) eligible for the unemployment benefit. There is a new SNZ indicator using IRD data and providing a monthly employment indicator which should be quite useful in normal times, but isn’t when the government is paying firms to keep people notionally on the payroll, even if doing little or no work. And although SNZ collects HLFS survey data steadily through the quarter, they seem uninterested in making even that partial monthly data available (larger margins of error as it would inevitably have). We’ll only finally get the June quarter HLFS data in August.

There are other hints of excess capacity. The wage subsidy scheme paid out in respect of some staggering share (around half) of New Zealand workers and the self-employed, but that is now very backward-looking since the bulk of the eligibility related to the severe regulatory restrictions on many/most business during the government’s so-called “Level 4” period, from late March to late April. Most of the employees covered would not have been made unemployed even if no wage subsidy had then been on offer.

The new wage subsidy scheme comes into effect this week. The rules were tweaked again last week, and although this scheme only covers eight weeks (rather than twelve in the original scheme), the expected cost (close to $3.5 billion) suggests a lot of excess capacity still exists, or is expected to exist. Not, of course, that we have any official data on that.

Of course, other countries have also had the mix of regulatory restrictions (“lockdowns”), self-chosen reductions in social and commercial activity, and the impact of the sharp disruption to world economic activity. Labour is generally not being particularly fully-employed at present. But in most advanced countries, even those with monthly labour force survey data, this excess capacity does not really show up in the official unemployment rate at present – after all, most other countries have deployed some form or other of fiscal support designed to keep workers attached to firms, even if for now they are doing little or nothing. In most countries, the monthly official unemployment rate has risen this year, but mostly not by much (and there are vagaries in the statistics such that in Italy the official unemployment rate has fallen).

Only three OECD countries are reporting really large increases in their official unemployment rates. These are percentage points changes this year to date.

Canada +8.1

Colombia (new to the OECD) +9.5

United States +9.8

The US numbers came out on Friday night. There is some controversy about the monthly change, but all the caveats (including those from the BLS themselves) suggest that the “true” or “underlying” number is even higher than the reported number.

I’m not putting much weight on Colombia (knowing almost nothing about it), but we have every reason to suppose that the dislocation of the economy in New Zealand over recent months in New Zealand was at least as large as those in the US and Canada (whether one looks at a regulatory restrictions index, mobility data, or stylised indicators like the degree of dependence on the labour-intensive foreign tourism sector). Forecasts of the drop in June quarter GDP are higher for New Zealand than for most other advanced countries.

The “true” increase in excess capacity to last month (the US and Canadian data are for May) in New Zealand is almost certain to have been at least as large as those in the US and Canada. One might think in terms of an unemployment rate equivalent of at least 13 per cent, which would be (by some margin) the worst New Zealand had experienced since the 1930s.

One can debate the merits of the wage subsidy scheme – and even more so the extended version, which seems focused on tying workers to firms that are least likely to recover any time soon, if ever – but without it we would have a much clearer sense of just how severe the labout market excess capacity actually is. (Even if, as I have favoured, one took a more generous approach to individuals facing serious income loss this year.) Perhaps even when all the wage subsidy schemes have passed the official unemployment rate will be “only” in the high single figure range – although if the schemes expire in September I’m still sceptical of that – but for now it is all but certain that the excess capacity in the labour market, that needs reabsorbing one way or the other, is well into double-digit percentages. And political debate about what needs to be done should operate with those sorts of numbers in mind.

On which note, I’ve been reflecting over the last few days on what it takes to see full employment restored. It isn’t like, for example, everyone simply coming back to work after the summer holidays. Everyone – individuals and firms – planned on summer holidays and planned on returning. By contrast, even in New Zealand with (for now) almost no Covid, that isn’t the parallel at all. The income lost over the last couple of months – probably well in excess of $20 billion, relative to normal expectations – isn’t coming back. The border is still largely closed. The virus still stalks the earth, with associated heightened uncertainty. The world economy is in a severe recession and (rightly or wrongly) almost all forecasters think it will take several years for activity levels to get back to normal. So if wealth has taken a hit already, and some significant sources of external demand are either restricted (by regulation) or impaired, where is the demand going to come from to quickly reabsorb workers who are either already displaced, or who are hanging in some temporary wage-subsidy limbo.

You see occasional talk of people “doing their bit” for New Zealand businesses by going out and spending more than usual, but it is a bit hard to envisage it happening on any significant or sustained scale. I tried some introspection. My household hasn’t been materially adversely economically affected by Covid shocks, and there doesn’t seem to be any material employment risk. And yet we aren’t spending any more than usual, possibly a bit less. Why would it be otherwise? We’ll have a break in the school holidays, but then we always do (and when we booked the other day it was a bit shorter than it might have been, Auckland Museum having had to cancel/postpone the exhibition we hoped to see). Many shops are still a pain to go in to. And I find myself still slightly shell-shocked after the last few months and a bit more cautious and abstemious than otherwise. And if I thought about “doing my bit” on any serious scale – there are always jobs around the house than could be done – then I’d contemplate the dramatic change in the fiscal position. I’m not suggesting some full-blown Ricardian effect here, but (whether I approved of the scheme or not) it seems rather less likely than it was a few months ago that my kids will get fees-free tertiary education, and even if a centre-right government were to be elected tax cuts seem less likely than they did. And even prospects for the kids to get part-time jobs don’t seem what they were (and there are probably people needing the jobs more anyway). Oh, and I’m conscious that another round of Covid restrictions, and economic dislocation, isn’t impossible or even unlikely.

Perhaps you are different. Perhaps you are energetically contemplating spending more aggressively. But I suspect most people won’t be, even those (notably in the public sector) fairly confident of keeping their jobs).

In a typical serious recession, changes in incentives (relative prices) do quite a lot of the work. Lower real interest rates ease pressure on the most-indebted but (more importantly) they draw spending forward. Often those changes in real interest rates have been rather large. Sometimes, tax rates (income or consumption) are cut. And, particularly in countries with a fair bit of foreign debt and not typically treated as international safe-havens (or home bases for pools of savings), the exchange rate falls a lot, drawing demand (from locals and foreigners) towards New Zealand. Oh, and of course sometimes the government itself does a lot more direct spending on goods and services.

(Oh, and of course there is always pro-productivity and pro-investment micro reforms but…….this is modern New Zealand.)

The key point is that if, at some like current real wages, we are to get back fairly quickly to full employment (which, in my view, should be a high policy priority, given the dreadful scarring effects sustained periods of unemployment can have on some individuals) it needs quite a lot of people to spend quite a bit more than they otherwise would, to replace the demand that has (for now at least) disappeared or been somewhat impaired).

Of those mechanisms:

- real interest rates have barely changed. The Reserve Bank can huff and puff all it likes about possible portfolio balance effects etc from its LSAP programme, but if they don’t change prices in ways that encourage more spending than was happening at the start of the year (and they haven’t) it is really little more than sound and fury (and, just possibly, having stopped things getting worse),

- the exchange rate is now about the same level it averaged last year,

- consumption tax rates haven’t changed, and although there have been some business tax changes (a) most of the effects will be intra-marginal (flowing to people who woin’t change their behaviour, and (b) uncertainty is very bad for business investment (ie even if the effects are in the right direction, they are likely to be very weak for now)

The government is, of course, spending a lot. Most of that isn’t direct spending on goods and services (consumption and investment) but income transfers in one guise or another. Even there however, the largest and most concentrated spend has already happened over the last three months (with some more in the next couple of months).

From the “fiscal hawk” side of the debate, one hears quite a bit of worry about fiscal excess and heavy future burdens. I come and go on how sympathetic I am to those complaints and warning, but mostly I end up not being that sympathetic (and I noticed over the weekend a centre-right UK think-tank, Policy Exchange, taking what appeared to be a similar stance, of for different reasons). And why? Because if we are concerned at all about getting people back into work faster than simply allowing nature to take its course – recessions will heal themselves eventually, but it could take quite a few years (perhaps tourism will be back to normal levels in 2025?) – someone (many actually) have to be willing to spend more now than they were otherwise planning to. I’d much prefer that monetary policy were doing its job – not just here, but in Australia and most other developed countries – because I think much lower interest rates and a much lower exchange rate would do a lot (as they did after 1933, 1967, 1991, 1998, and 2008/09), by changing relative prices/incentives, but it isn’t. And with a hole this deep – and borrowing costs this low (which don’t make fiscal policy a “free lunch”) and on-market borrowing this easy – it would imprudent for fiscal policy to be doing no more than just letting the automatic stabilisers work. And, in truth, at least on the domestic interest rate leg, letting monetary policy do its job also involves people taking on more debt now than they’d otherwise planned to (voluntarily chosen and all that, but debt nonetheless).

If we are starting from (effectively) perhaps double-digits effective rates of unemployment, it is far from clear that anything like enough macro policy stimulus is being done. If fiscal policy hasn’t reached its political limits – it is nowhere near the market limits, but neither should we test those – it must be much closer than it was and, on the other hand, monetary policy is doing almost nothing. That is really inexcusable, If Orr and the rest of the MPC want to take on themselves some sort of mantle of Hayek or Mellon (as caricatured) as do-nothing liquidationists, Robertson, Ardern Peters, Shaw (and, it seems, Muller and Goldsmith) shouldn’t be standing idly by, by default offering their imprimatur.

(The post was headed “Recovering”: unfortunately, I am doing so only slowly from some bug I’ve picked up, so posts this week may continue to be patchier than I’d like.)

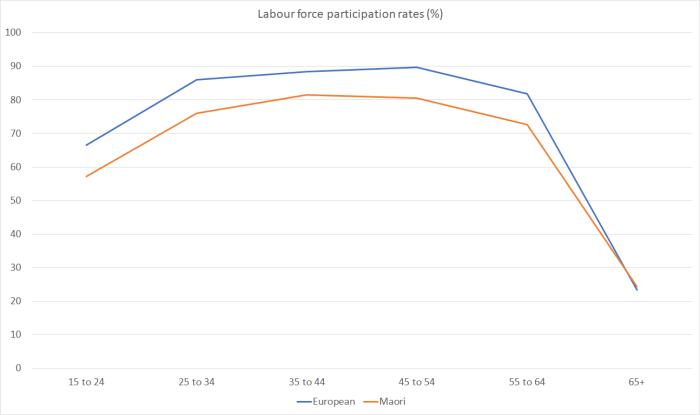

In the early 90s 5 per cent of old people were in the labour force (working or actively seeking), and now that figure is almost 25 per cent. By contrast, the labour force participation rate for 15-24 year olds is now only around 63 per cent (it was 74 per cent when the HLFS began). (Frankly, the drop in youth participation rates surprises me a bit given that (eg) university fees are much much higher than they used to be, and that one has to work only an hour a week to be counted as employed so, for example, after school jobs should be captured.)

In the early 90s 5 per cent of old people were in the labour force (working or actively seeking), and now that figure is almost 25 per cent. By contrast, the labour force participation rate for 15-24 year olds is now only around 63 per cent (it was 74 per cent when the HLFS began). (Frankly, the drop in youth participation rates surprises me a bit given that (eg) university fees are much much higher than they used to be, and that one has to work only an hour a week to be counted as employed so, for example, after school jobs should be captured.)

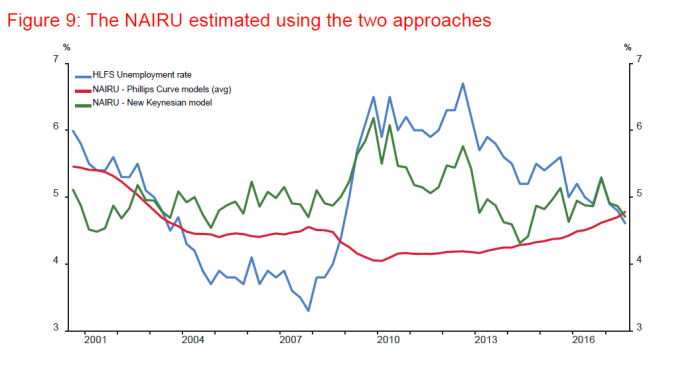

As we headed into the recession there was a lot of expectation of a strong rebound. Even up to around 2012, respondents expected growth to accelerate. For the last few years they haven’t expected any acceleration, and now the expect it to slow. To be specific, respondents expect 1.6 per cent total growth in the first half of this year, slowing to 1.2 per cent in the second half of this year. We don’t know quite why – perhaps they expect immigration numbers to slow – but it doesn’t speak of a sense that things are getting away on the Reserve Bank. Similarly, two years out respondents expected that the unemployment rate would still be 4.9 per cent.

As we headed into the recession there was a lot of expectation of a strong rebound. Even up to around 2012, respondents expected growth to accelerate. For the last few years they haven’t expected any acceleration, and now the expect it to slow. To be specific, respondents expect 1.6 per cent total growth in the first half of this year, slowing to 1.2 per cent in the second half of this year. We don’t know quite why – perhaps they expect immigration numbers to slow – but it doesn’t speak of a sense that things are getting away on the Reserve Bank. Similarly, two years out respondents expected that the unemployment rate would still be 4.9 per cent.

Perhaps there is some sign of a possible pick-up in the analytical unadjusted series (which doesn’t try to correct – inadequately – for productivity changes) but it is a moderately volatile series, and the most recent rate of increase is still below the peak in the last little apparent pick-up a year or two back.

Perhaps there is some sign of a possible pick-up in the analytical unadjusted series (which doesn’t try to correct – inadequately – for productivity changes) but it is a moderately volatile series, and the most recent rate of increase is still below the peak in the last little apparent pick-up a year or two back.