Former UK Labour MP (and academic administrator) Bryan Gould, and former Reserve Bank Governor (and political leader) Don Brash have been engaged in a fairly robust exchange of views in the op-ed pages of the Herald.

Gould began it a couple of weeks ago with a column, initially prompted by some combination of the initiatives from both the Minister of Finance, and the Labour Party, that may lead to governance reforms at the Reserve Bank, and Sonny Bill Williams’ Islam-inspired objections to interest, and hence to sponsorship by the BNZ. The politicians being not very radical at all, Gould pointed us to Williams.

Sonny Bill, however, has succeeded, if we are thoughtful enough to recognise it, in throwing a spotlight on the entire role of the banks in our economy and our society.

Gould’s specific concern?

It is the willingness, not to say keenness, of the banks to lend on mortgage that provides the virtually limitless purchasing power that is constantly bidding up the prices of homes in Auckland and, now, elsewhere.

It is the banks that are fuelling the housing unaffordability crisis, a crisis that is leaving families homeless and widening the gap between rich and poor.

Gould isn’t keen on operational autonomy for the Reserve Bank, whether on monetary policy or banking regulation, at all.

Why should the Government be able to hide behind the Governor of the Reserve Bank and duck responsibility for a policy of the greatest importance to so many Kiwis? Why should ministers not be held to account in Parliament and to the country for failing to deliver outcomes they were elected to deliver?

And actually, I have some sympathy with him on that. Banking regulation should be administered by the Reserve Bank, but approved by the Minister of Finance or Parliament itself.

But Gould’s argument isn’t some abstract one about the optimal assignment of powers within the Reserve Bank Act. His concern is that banks create credit, and in so doing create new deposits, as a profit-making business.

They lend you money that they themselves create out of nothing, through the stroke of a pen or, today, a computer entry.

The banks make their money, in other words, by charging interest on money that they themselves create. Not surprisingly, they are keen to lend as much as possible.

In fact, most businesses are keen to increase volume, at least for as long as they can make money on the marginal addition to their sales. Supermarkets are typically keen on selling you more groceries, health food shops on selling you more health food, fashion outlets on selling you more clothes etc. But Gould’s bugbear is banks (and, presumably, other lending institutions). To read Gould, you’d think that banks crammed money down the throats of unwilling borrowers. There doesn’t seem to be any role for demand in his story (let alone for the regulatory restrictions that artificially inflate urban land values). Banks, as currently structured, don’t appear to serve any socially useful purpose.

As you might expect, Don Brash – a former Governor, a former ANZ director, and currently chair of one of the small Chinese banks in New Zealand – disagreed. Writing of Gould he notes

He then goes on to blame this money creation for the housing affordability crisis which Auckland now finds itself in, and to attack the Government for washing its hands of this aspect of the housing crisis.

Mr Gould is not alone in peddling this nonsense, but that certainly doesn’t make it correct.

Don Brash isn’t disputing the rather obvious point that the banking system, in the course of lending, also create deposits. As he says

The banking system does create money.

But at this point he rather veers away from the substance of the issue (Gould’s claim that bank credit creation at the root cause of the housing affordability problems – dismissed by Brash as “peddling this nonsense”) to make a correct, and useful, but in this context perhaps subsidiary, point. What is more or less true of the system as a whole, just isn’t true for any individual bank.

If individual banks really could create money by “the stroke of a pen or a computer entry”, as Mr Gould contends, why do they bother paying interest on deposits, why do they borrow funds from parent banks overseas, why do they borrow funds in the international market, why do they need to hold some funds in government securities as a liquidity reserve, why do some banks occasionally run out of money when customers lose confidence in them?

….I now chair the small New Zealand subsidiary of the Industrial and Commercial Bank of China….. It would certainly make life very much easier if we could, “by the stroke of a pen or a computer entry”, simply create the money which we lend out to New Zealand borrowers. Unfortunately, we can’t.

Individual banks, and their managers and boards, have to worry (sometimes a lot) about the funding side of their balance sheets. If Don Brash’s bank increases lending to New Zealand borrowers, that process will indeed create new deposits for the New Zealand banking system as a whole. But there is no guarantee any of those deposits will come back to his bank. In the immediate term, if one bank increases lending more than other banks do, that will lead to a loss of liquidity from the lending bank. In boom times, it might be easy to fund such rapid lending growth. In times of crisis, funding can be almost everything. I was heavily involved in these issues in the midst of the 2008/09 financial crisis, and recall banks telling us then that no matter what initiatives the government or the Reserve Bank took, they’d be reluctant to increase lending if they couldn’t count on secure on-market funding. Their Boards just wouldn’t let them.

But in a way, Brash’s response didn’t actually deal with Gould’s point – that for the banking system as a whole, deposits don’t usually constrain lending. Rather the two typically grow as part of a simultaneous process (with some exceptions about changes in the current account deficit etc). If so, perhaps the credit creation process could be the root cause of the (housing) problem?

Gould returned to the fray in a column in yesterday’s Herald. But, oddly, he doesn’t attempt to defend his view that banks are the cause of the housing problem. Rather he tries to teach the former Governor to suck eggs, offering lay lessons in monetary economics, and suggesting that Brash doesn’t really know what he is talking about.

In fact, he first misrepresents what Brash said

…..I said the vast majority of new money in circulation is created by the banks “by the stroke of a pen”, and they then make their profits by charging interest on the money they create.

If this is “nonsense”, the “peddlers” include some very distinguished economists.

But, as you can see from the quotes above, Brash seems to be mostly using the “peddling nonsense” phrase to respond to the housing affordability argument. Moreover, he explicitly states (see above) that the banking system creates money (personally, I’d prefer he’d used “deposits” rather than “money”).

In fact, in the entire latest Gould column there is not a single mention of the housing issue. Instead, there are extensive quotes from a very good – but entirely conventional – Bank of England Bulletin article from a few years ago on how the credit and deposit creation process actually works, and how that process is quite different from the very stylised approach that often lingers in elementary economics textbooks. In fact, our Reserve Bank made many of the same points in an article in their Bulletin a few years earlier. A (then) Reserve Bank senior manager was making these points in a speech 15 years ago. But the Bank of England article is very good. Then again, recall that the Bank of England runs things pretty much exactly the same way our Reserve Bank does. There simply isn’t any stunning fresh insight in the BOE piece to up-end how best to think about monetary policy and banking regulation.

So when Gould quotes the BOE piece

They then go on to say, “Another common misconception is that the central bank determines the quantity of loans and deposits in the economy by controlling the quantity of central bank money – the so-called ‘money multiplier’ approach…[but that] is not an accurate description of how money is created in reality.”

They go on. “Banks first decide how much to lend depending on the profitable lending opportunities available to them – which will, crucially, depend on the interest rate set… It is these lending decisions that determine how many bank deposits are created by the banking system.

Anyone who knows anything about this stuff is simply drumming their fingers, and going “yes, yes, tell us something we didn’t know”. But do notice the mention of interest rates in that second paragraph. The way central banks choose to manage the monetary system these days relies on adjusting an official interest rate, not on attempting to directly manage quantities (of base money, lending, deposits or whatever). Demand for credit matters quite a lot, and the interest rate is a key rationing device. When overall demand is weak at any given interest rate – as has been the case for the last decade – interest rates tend to fall, and official interest rates are typically cut. Banks can’t just generate new demand out of thin air.

Gould concludes

But the capacity they [banks] have is hugely important. I concluded by asking whether it was wise to entrust such wide-ranging powers – so significant in their impact on the whole economy – to the banks, and then to arrange that the only person able to regulate that impact was himself a banker – the Governor of the Reserve Bank.

Reasonable people can differ on the extent to which banks should be regulated, and even on who should do the regulation (one should always cautious about the risk of capture, of bureaucrats/ministers by those they are supposed to be regulating).

But in his two articles put together, Gould has done nothing (at all) to substantiate his claim that banks are the prime (or even just a key) source of the housing affordability problems. Simply describing the way in which credit and deposits are created, across the banking system as a whole, contributes little.

I would grant one point. If banks could not create credit – in the process (simultaneously) allowing young generations to borrow from older ones – house price cycles would look rather different. Perhaps house prices would be a little lower. But the biggest change would probably be not in the level of house prices, but in who owned the houses. Even more young people would be unable to purchase their own home, and more of those homes would be owned by those not constrained by access to credit (be it the evil “investors”, cashed-up foreigners, or institutional vehicles such as pension funds). Systemic credit risks might be lower, but at what cost to individual families etc? The fundamental factors that create (artificial) scarcity – land use restrictions running hard into rapidly rising population-fuelled demand – wouldn’t have changed at all.

And for believers in the idea that the banking system is the source of the problem, it is often worth pointing them to the United States. It has the same sort of banking system we do – the banking system simulataneously creates loans and deposits – and yet vast swathes of the country, including big cities often with quite rapid population growth, have had no problems with unaffordable house prices (as a resource on this, try this excellent interview with leading US housing academic Joseph Gyourko, which almost deserves its own post). The private banking system isn’t the problem. Land use and housing supply restrictions are. The banking system certainly enables some people who would otherwise be squeezed out completely to purchase (in fact that is what it always did for first home buyers – whether the “bank” was a private one, or the State Advances Corporation). If house prices ever do fall back a long way, some borrowers might well regret having borrowed. But in all sorts of areas of life, hindsight is like that. For now, they’ve made the best decisions they could for themselves, with the information they have,

Monetary reform ideas have a long tradition – sometimes advocated by some pretty prominent economists (eg Laurence Kotlikoff, who came through New Zealand a few years ago). Usually, there is (a lot) less there than the advocates make out. Sometimes – as with Social Credit – the analysis is simply misconceived, or even straight-out nutty. I suspect Gould is in the former camp. We could, if we wanted to, have a quite different system of monetary management. I think we’d mostly be worse off if we did. And since our system is the same system adopted now across virtually the entire world, the burden of proof should surely be on the advocates of change to demonstrate that the outcomes of their alternative visions would be demonstrably superior. Gould hasn’t done that. And it is no use simply going ‘but the 2008/09 crisis was so awful, anything has to be better’ without a great deal more supporting analysis, of the causes and consequences of those crisis episodes, than is on offer here.

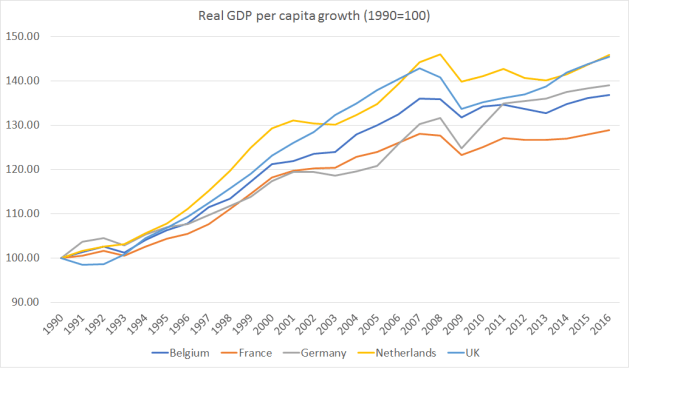

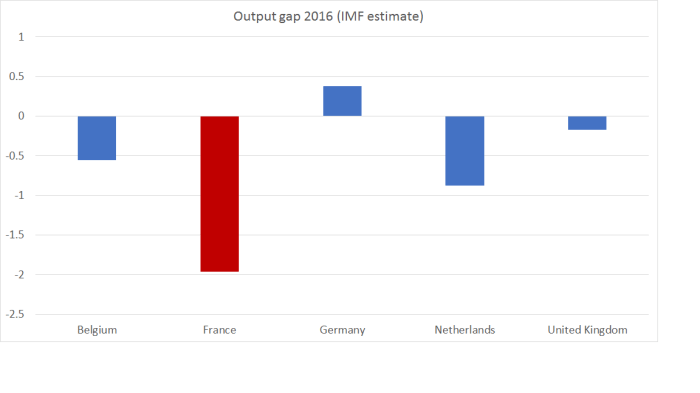

France is, again, the worst performer.

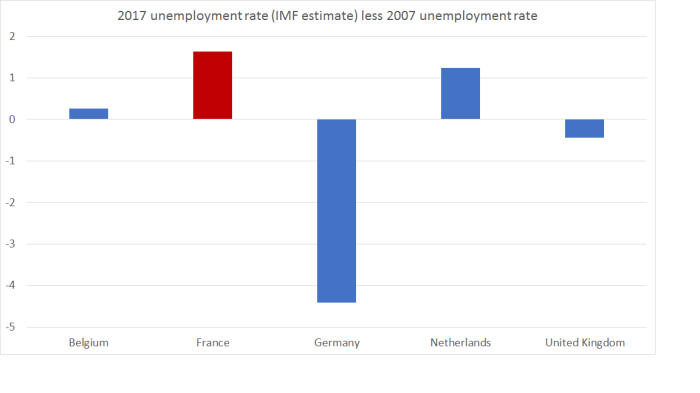

France is, again, the worst performer.

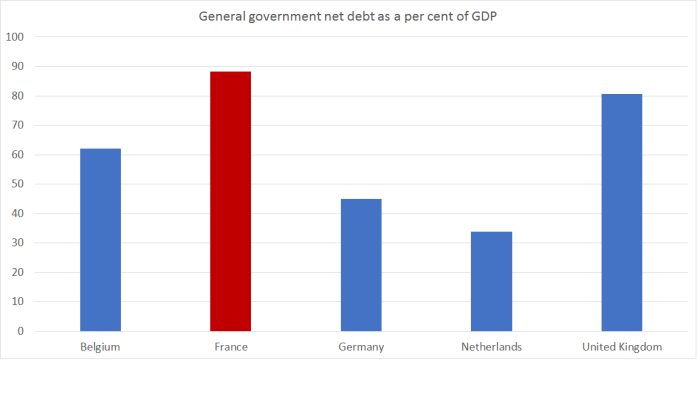

France caught up over the first few decades and has largely held its own since, at least relative to these comparators.

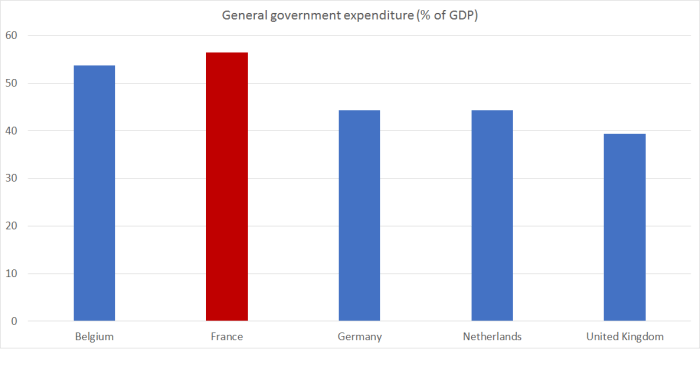

France caught up over the first few decades and has largely held its own since, at least relative to these comparators.