After a run of posts on immigration, or indeed on Reserve Bank issues, I often feel like something completely different. No doubt that is a relief to readers, but it also helps remind me that I intend to write about what takes my fancy and interests me, and not primarily pushing particular causes.

And it is not as if I want to weigh in to the Herald vs Winston Peters contretemps, in which (at least on my reading) the Herald was using numbers that were accurate but seriously misleading (whether with an agenda, or just because they weren’t famliar with the better data, or some combination of the two, I have no idea), while Winston Peters was also, as far as I can tell, factually accurate but really rather distasteful.

But France is coming towards the end of a fascinating election campaign, which (for political junkies) has meant lots of fascinating articles about French politics, French society, and so on. It has resolved to a race between two unconventional candidates, neither with strong parliamentary support, and so potential challenges in governing. And if, as seems likely, Macron wins, the challenge to the “globalist” establishment seems unlikely to go away any time soon.

No doubt there have been some articles around on the French economy, but I must have missed them. So I decided to download some data, mostly from the IMF World Economic Outlook database, and amuse myself by looking at a few comparisons between France on the one hand, and Belgium, Netherlands, and Germany on the other (with a sideways glance at the rather different UK economy from time to time). They seem like good comparators for France, as Australia often is for New Zealand. References to New Zealand will be few and far between, but just note that these are all countries with materially higher real GDP per capita than New Zealand has. And the productivity gaps – using real GDP per hour worked – are much larger again. For those four continental countries, the OECD estimates that average GDP per hour worked is now more than 60 per cent higher than that in New Zealand.

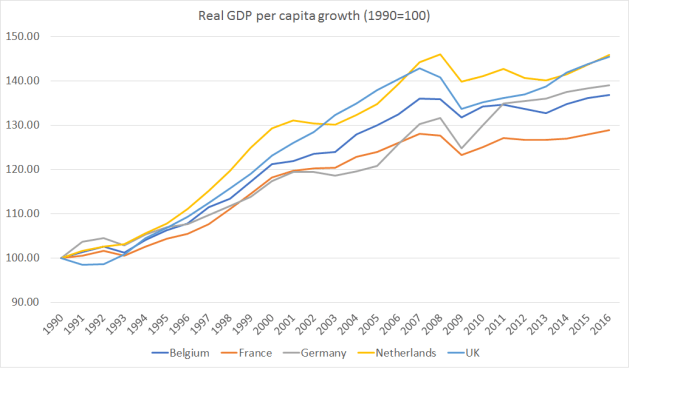

First up is a comparison of real per capita GDP growth, in national currency terms (although of course all four continental countries use the same currency now) since 1990.

Over that full period, France has been clearly the worst performer, but interestingly that has only been clear since about 2010. Until then, on this measure Germany and France had been tracking very closely together.

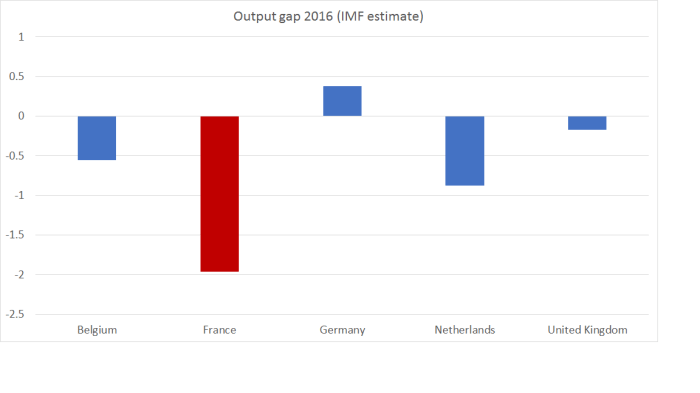

And some of the difference with Germany may still “just” be cyclical (things that economists put “just” in front of can still matter quite a bit in elections). Here are the IMF estimates of the respective output gaps.

There is materially more excess capacity in France than in the other four countries.

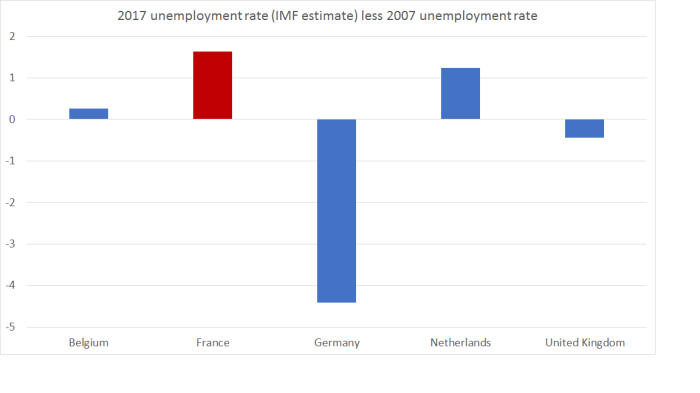

Consistent with this, the unemployment rate is materially higher in France than in the other countries. It is about 10 per cent in France, compared with a range of 4 to 6 per cent for Germany, Netherlands and the UK (with Belgium in the middle). France probably has a higher NAIRU. But here is the IMF estimate of this year’s unemployment rate, less the actual unemployment rate for 2007, the last year of the previous boom.

France is, again, the worst performer.

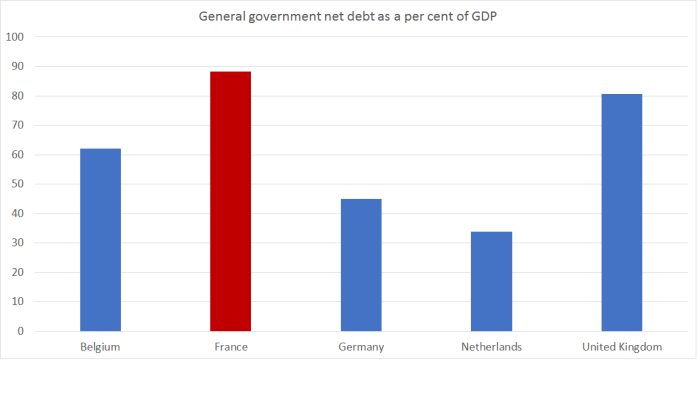

France is, again, the worst performer.

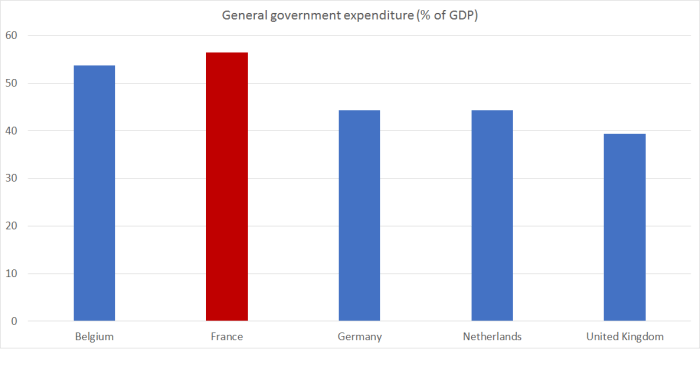

The government debt position is pretty poor too (although not that much worse than the UK’s).

I’m never quite sure why people think Germany should increase government spending and increase its government debt – especially in a country with little or no population growth. France’s numbers – among the very highest in any advanced country – don’t look like something to emulate, no matter good the resulting school lunches might be.

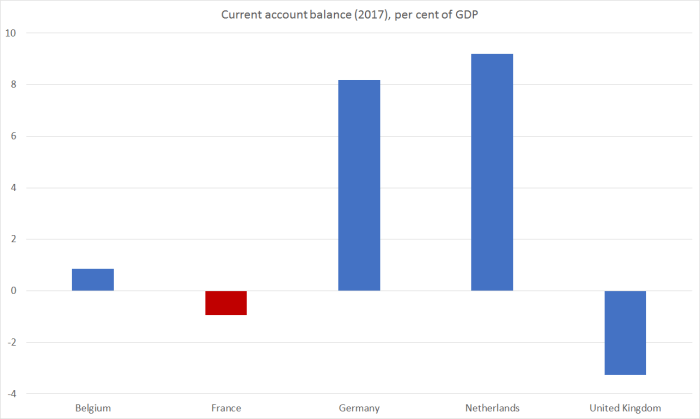

Current account numbers aren’t that easy to interpret without lots of context, but even for an advanced economy with modest population growth, surpluses the size of Germany’s (or the Netherlands) look, at very least, anomalous. There isn’t anything inherently virtuous about France’s near-balance position, but it typically wouldn’t be an indicator of serious trouble either.

With a bit more demand and a stronger cyclical position – hard to engineer with such high public debt, and no national monetary policy – the current account deficit would no doubt be a bit wider.

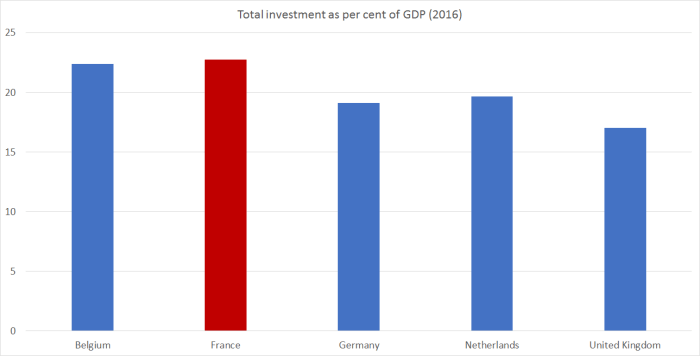

It isn’t all a bad news story. Here, for example, is total investment as a share of GDP.

The investment share of GDP in France last year was higher than that of any of these countries – far higher, for example, than in cyclically more-stretched Germany. At least some of those big, really successful, global French companies must have been seeing some good opportunities at home.

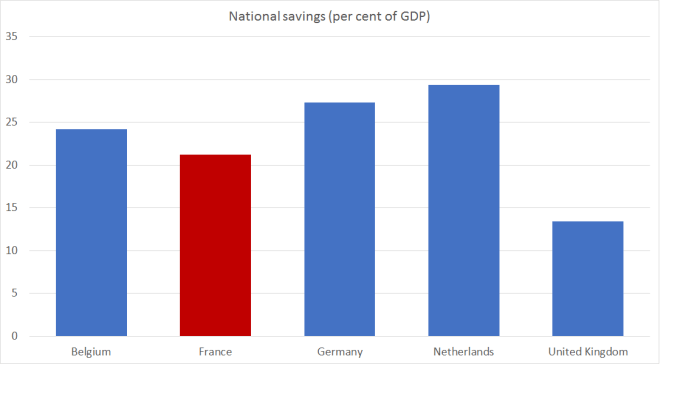

Despite all that government spending and generous welfare provision, nothing really stands out about the French national savings rate either.

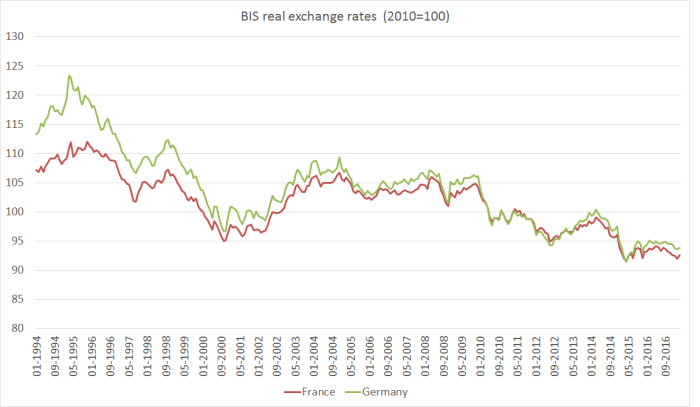

Even within common currency areas, real exchange rates can move – at times quite considerably. We saw that a lot in the run-up to the crisis, with real exchange rate appreciations in peripheral countries (such as Ireland) relative to core euro countries. Perhaps such movements help explain, or mitigate, France’s disappointing relative performance?

These are the BIS’s broad real exchange rate measures for France and Germany.

The two countries’ real exchange rates have moved all but identically ever since the creation of the euro. It isn’t clear why there hasn’t been more movement (especially in recent years) but it isn’t hard to suspect that if the franc and mark were again different currencies, we wouldn’t have seen anything like as strong a common trend.

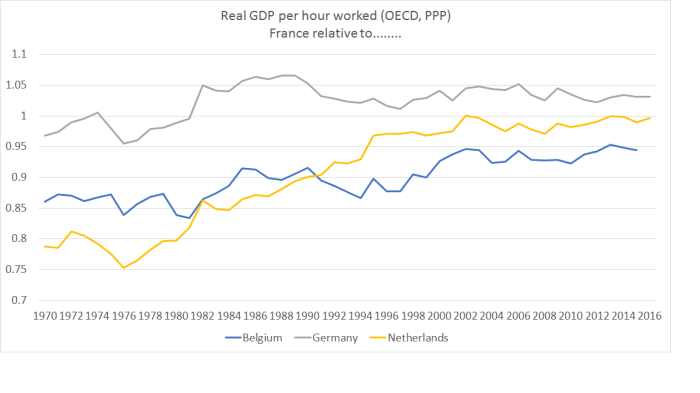

Over the longer-term, it is hardly as if France is some hopeless case. If we look at meausures of labour productivity, real GDP per hour worked (in PPP terms) in each of France, Belgium, Netherlands and Germany are among the highest anywhere, averaging something very similar to the US numbers (the UK is quite a bit lower). The OECD’s series for that data goes back to 1970. Here is how France has done relative to the other three continentals.

France caught up over the first few decades and has largely held its own since, at least relative to these comparators.

France caught up over the first few decades and has largely held its own since, at least relative to these comparators.

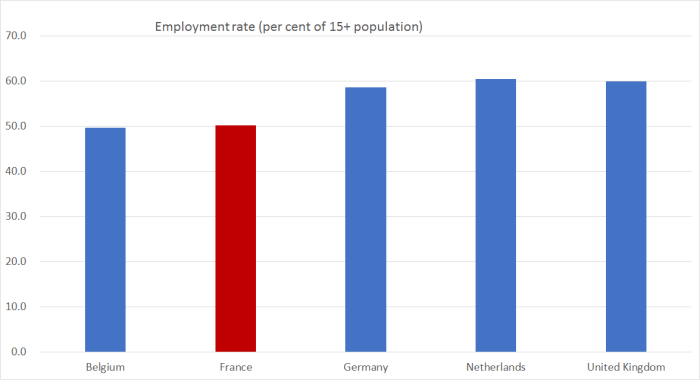

Of course, one of the striking things about France is how little labour input is used.

Since, as we saw above, the French unemployment rate is higher than usual, the picture is slightly exaggerated at present. but the difference between France (and Belgium) and the other three countries is stark. (In New Zealand, by the way, the employment rate in the same quarter was 66.9 per cent, while the US is similar to Germany, Netherlands and the UK.)

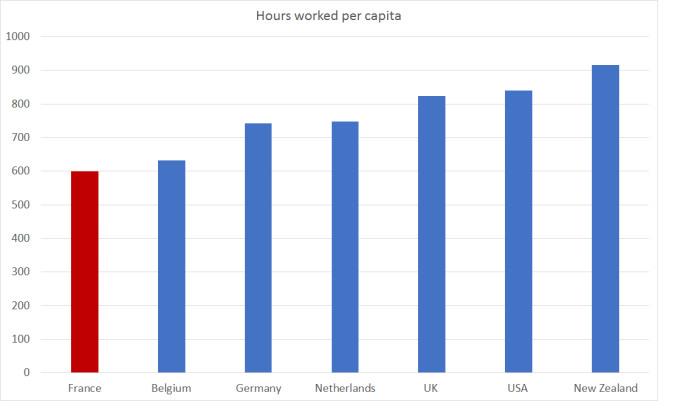

The differences are just as stark, if not more so, if we look at hours worked per capita. Here I use the Conference Board’s Total Economy database.

The average French person – man, woman, child, young middle-aged and old – worked around 600 hours last year. The average New Zealander worked more than 50 per cent more – and still managed clearly the lowest real GDP per capita of any country in this chart. So little output for so much input.

There are lots of stories about the possible connections between hours and productivity. If, for example, you impose tough regulations and make employing labour very expensive, firms will have to adapt such that the people who are employed are highly productive (they have to earn their keep). The less productive firms and people are simply priced out. But higher taxes – certainly than somewhere like New Zealand – and provisions of retirement income policies also play a part in discouraging French working hours, and not just from the unproductive. Plenty of very capable people have long holidays, shortish work weeks, and relatively early retirements. As a result, French GDP per capita is lower than those of the other continentals in this sample, even though productivity per hour worked is very similar.

I don’t have strong lessons to draw from this post – it was a discursive tour, as much out of curiosity as anything. But I’ve long been a sceptic of the euro and – disruptive as a break-up or withdrawal inevitably would be – it isn’t obvious that French voters could look on the single currency as any sort of unalloyed blessing for them, and their country, especially in the years since 2007.

There are good reasons to be glad not to be in France – Islamic terorism among them. But when one looks as these data – not just for France but for each of the continental countries here – from a New Zealand perspective, aware of all the regulation and high taxes etc in France, it is a reminder of how much location really does seem to matter. I’m in the middle of reading a wonderful new book by a leading academic expert on trade, convergence etc – which I expect I will write about here soon. As he notes, technological innovations made extensive trade in goods possible from the 19th century, and then trade in ideas (all that ICT), but if anything face-to-face contact now seems to matter more than ever, and firms and global economic activity seems increasingly concentrated in cities and regions like those of northern Europe (or east Asia, or North America), not in the isolated peripheries.