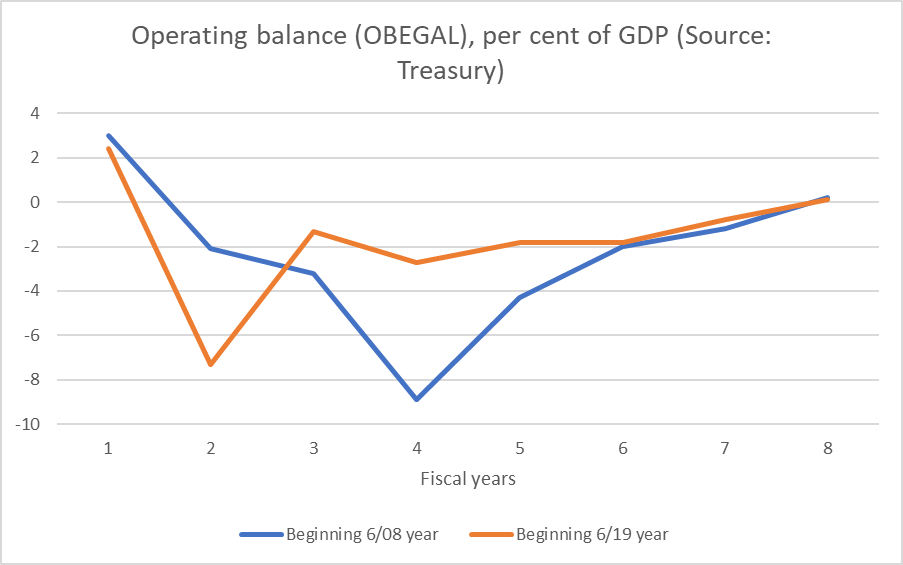

In the government’s Budget, the Treasury projects that on current policies the government will be running an operating deficit for six straight years (while in the 7th the surplus is so tiny that even if it were not for Eric Crampton’s point about tobacco excise revenue we might as well just call it a coin toss as to whether, if the economy played out as Treasury projects we’d see a surplus or a deficit that year).

People have from time to time pointed out that under the previous National government there was also a spell of six straight years of deficits. In fact, here is a chart. The blue lines shows actual fiscal balances from the last surplus (year to June 2008) to the first surplus again (year to June 2015), while the orange line shows actual and Treasury forecasts from the year to June 2019 (last surplus) to the first (tiny) projected surplus (year to June 2026)

In each period, there was one really really large deficit year. In the earlier period that was the year to June 2011, which captured much of the cost to the Crown resulting from the Canterbury earthquakes. In the more recent period, the peak deficit was the year to June 2020, the period encompassing the first and longest Covid lockdown (huge wage subsidy outlays and all).

If these forecasts come to pass we”ll have had an operating surplus (or balance) in five of the last seventeen years.

What about context? In both periods there was a very big exogenous event: earthquakes in the one period and Covid (lockdowns) in the other. Both were, almost necessarily, very expensive for the government. Few people have much problem with meeting many of the direct costs as fiscal obligations.

But….there was a really important difference between the two periods. In the first, the economy headed straight into a fairly deep recession (partly domestically-sourced – our inflation rate had got above the top of the target band – and partly the global downturn associated with the 2008 financial crisis. It was all aggravated by the fact that the 2008 Budget was very expansionary – and yes, that was extravagant and it was election year, but the Treasury advised them that such an approach would not push the budget into deficit over the forecast horizon. It wasn’t one of Treasury’s better calls.

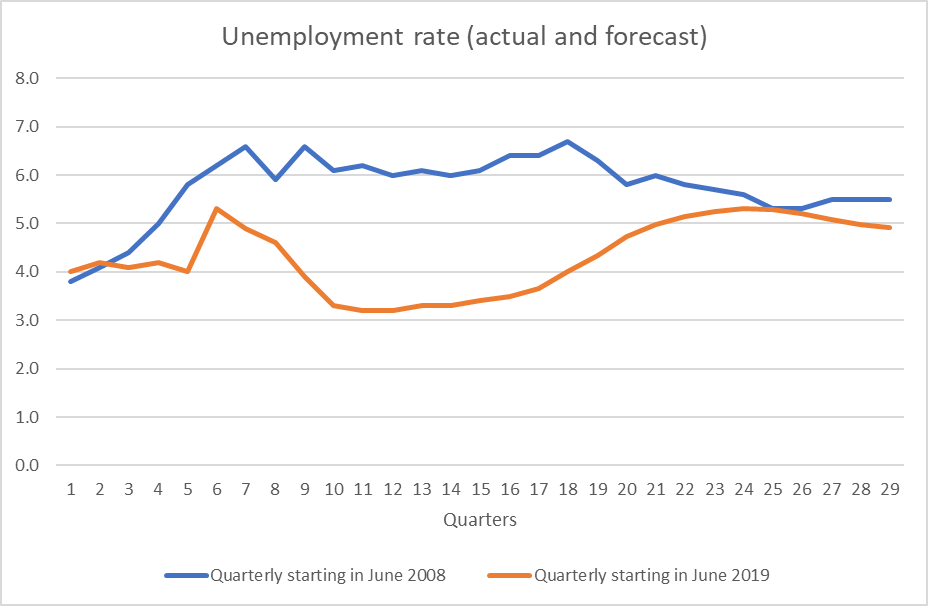

By contrast, at the end of 2019, the unemployment rate was low and, notwithstanding the brief but severe interruption to output around the lockdowns, has mostly remained very low since. When there isn’t excess capacity in the economy, tax revenue tends to come flooding in.

Here is a comparative chart of the unemployment rates in the two periods.

That difference in the unemployment rates makes quite a big difference to the fiscal outcomes, for any set of spending choices. You might criticise the previous government for doing nothing about a Reserve Bank that let unemployment linger well above the NAIRU for so long, as you might criticise the current government for doing nothing about a Reserve Bank that had the economy so overheated for so long. But the economic backdrops to those paths of fiscal deficits were simply very different: with an overheated economy and lots (and lots) of fiscal drag, the revenue was flooding into Treasury over recent years. There was simply no good macroeconomic reason for having operating fiscal deficits at all in an overheated economy, especially once the big direct Covid spending had come to an end (which it had a year ago). By contrast, the earlier government presided over a very sluggish recovery – and so weak, relative to target, was inflation that there was barely any fiscal drag. Even if the Budget was structurally balanced, cyclical factors would have left a small deficit (on Treasury and Reserve Bank numbers there was a negative output gap every year through to 2016).

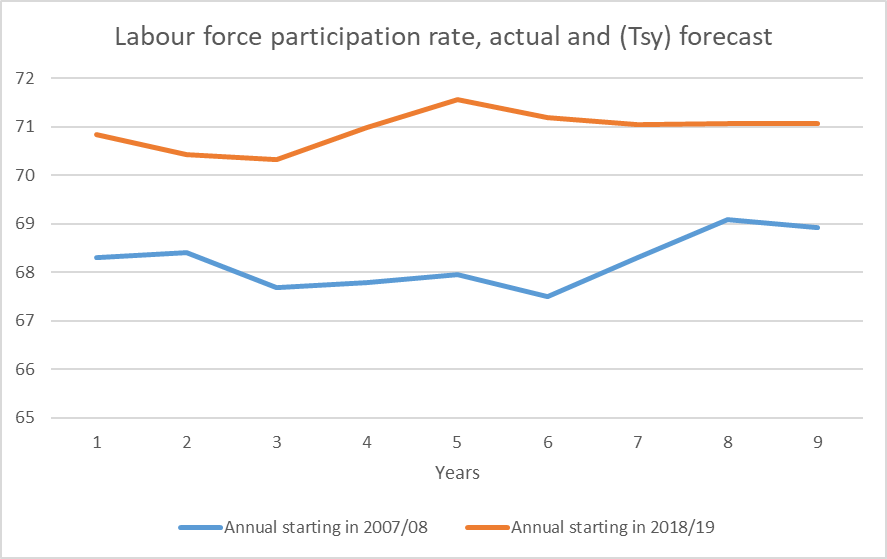

If the unemployment rates and output gaps give a sense of the cyclical slack (or overheating), labour force participation rates are also valuable context

A materially larger share of the population is now in the labour force now than in the period of that previous run of deficits (and given that unemployment rates have been lower this time, the difference in employment rates is even larger. Revenue has been abundant.

I’m not really convinced there was an overly strong case for the previous government having continued to run operating deficits in the last couple of years of their stretch of six. Had the Reserve Bank been doing its job better, perhaps they wouldn’t have (the economy would have been more fully employed and inflation would have been nearer the target).

But I’m quite convinced there has been no good economic case at all for operating deficits in 22/23. 23/24, or 24/25. Take 22/23 (the year just ending) as an example: on Treasury estimates there has been a positive output gap, and the unemployment will have averaged about 3.5 per cent (well below anyone’s estimate of NAIRU). And with 6-7% inflation, fiscal drag has been a big revenue raiser. And if there has been any residual direct Covid spending (a few vaccinations?), the amounts involved must have been vestigial indeed. So cyclically the revenue was flooding in, but they still ran a deficit: it was pure choice to undertake routine operational spending without the honesty to go to the electorate and raise the taxes to pay for that spending.

The cyclical position is less favourable over the next couple of years – the recesssion (as indicated by the 2 percentage point rise in the unemployment rate) required to get inflation back down again – but the government has chosen to adopt discretionary new giveaways with borrowed money.

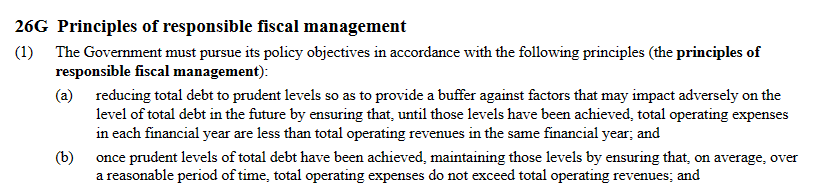

It isn’t just some idiosyncratic Reddell view that operating budgets should be balanced (none of this is about capital spending or arguments about infrastructure). It is there in the Public Finance Act

Now, if I was writing the Public Finance Act, I wouldn’t word things quite that way. But……the Public Finance Act is something both main parties have signed up to. It may make sense to borrow to fund useful longer-term investment, but it makes no sense to be borrowing to pay the groceries, especially in times when income has been more abundant than usual.

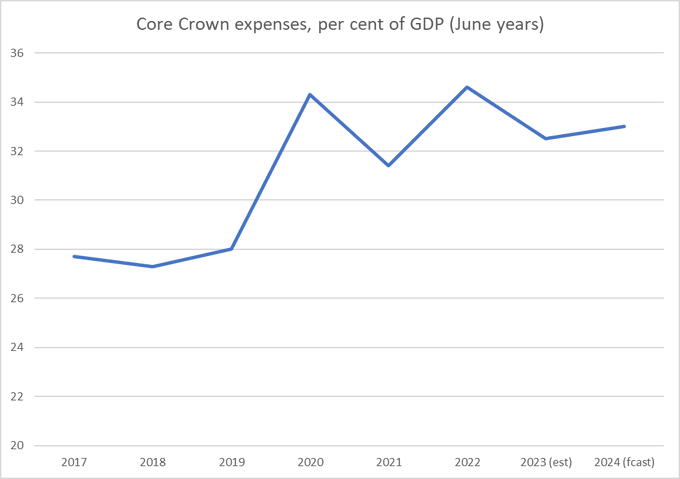

Just two more Budget charts. The first is one I showed on Twitter yesterday

Now, there is plenty of scope for political argument about the appropriate size of government spending, and left-wing parties will typically be keener on higher numbers than right-wing parties. My own interest here is more about fiscal balances, but it is worth being conscious of just how much larger a share of the economy is now represented by Crown operating spending than was the case even five or six years ago. Those were the days of the pre-election Labour/Greens budget responsibility rules

Next year’s spending at 33 per cent of GDP is not quite at the previous peaks (Covid and the earthquake years) but nor might one really have expected it to be. But there is an election to win I guess.

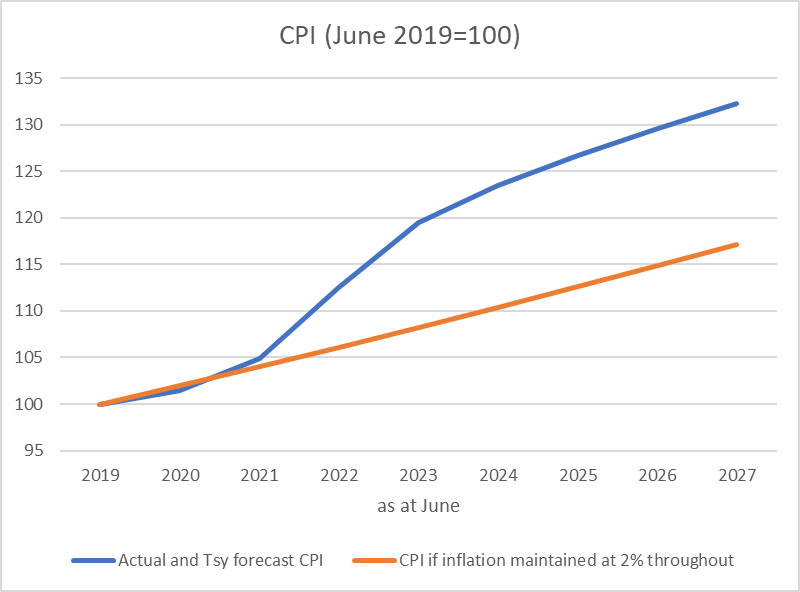

And finally, inflation. Treasury doesn’t run monetary policy but (a) the Secretary sits as a non-voting MPC member, and (b) Treasury are the Minister’s advisers on the Bank’s performance, so they aren’t just any forecaster. On the Treasury numbers, it isn’t until the year to June 2027 that CPI inflation gets back to the middle of the target range (the 2 per cent midpoint the MPC is supposed to focus on).

This chart uses Treasury’s annual numbers to illustrate what a difference the monetary policy mistake has made, and is making, to the price level

The blue line is the actual (annual) data and the Treasury forecasts. The orange line is what the price level would have looked like in a stylised scenario in which the MPC had delivered 2 per cent inflation each year over this period. The difference is substantial: the price level in the blue line is almost 13 per cent higher than in the orange line by the end of the period. The Minister of Finance appears to be quite happy for the current gap (about 10 per cent) to keep widening for the next five years. He shouldn’t be.

We do not run a price level targeting regime. That means bygones are treated as bygones and we don’t attempt to pull the actual inflation rate back down to the orange line having once made the policy mistake that pushed it so far above. It does not – or should not – mean indifference to the arbitrary redistributions that big unexpected changes in the price level impose, strongly favouring borrowers (especially those with nominal debt and long-term fixed interest rates) and heavily penalising financial savers (holders of real assets can be largely indifferent over time). Inflation – and especially unexpected inflation – is deeply damaging, and there were good reasons for reorienting monetary policy to deliver medium-term price stability. But now the powers that be appear unbothered by 7 years in succession of inflation above the target midpoint. It seems about on a par with being happy to set out to deliver six successive years of operating deficits. Poor fiscal policy, poor monetary policy, poor performance from both the Governor and MPC and the Minister of Finance (the latter not only having direct responsibility for fiscal policy, but overall responsibility for monetary policy and the people he appoints to conduct it). It will be interesting to compare the Reserve Bank (considerably more up to date) forecasts next week.

I’m going to be away for the next couple of weeks so there won’t be any new posts here until after King’s Birthday.

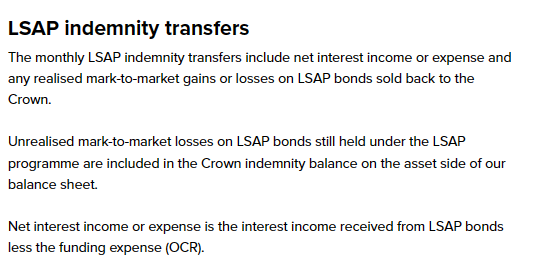

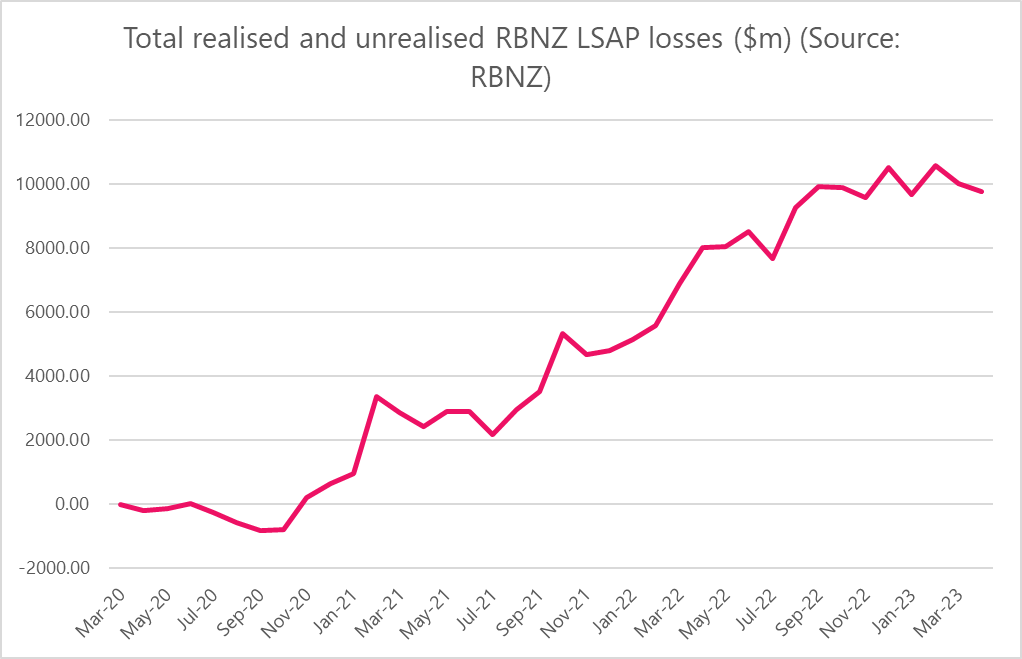

There have been various posts here over the last couple of years about the losses to the taxpayer resulting from the Reserve Bank’s Large Scale Asset Purchase (LSAP) programme. Some of these have been more about explaining than excoriating (the latest such explanatory post is here).

As I noted in that most recent post, in the early days of the LSAP the line item on the Reserve Bank balance sheet for the claim on the Crown indemnity was a rough but reasonable estimate of the total losses, based on market prices as at the successive balance dates. It became an increasingly inadequate indicator as the LSAP programme started to be unwound, with the longest-dated bonds being sold back to Treasury, losses being realised, and payments being made from the Treasury to the Reserve Bank under the indemnity.

But the amounts of those indemnity payments were not being routinely disclosed (eg the RB does not publish a monthly income statement) and analysts were reduced to picking up snippets of information from OIAed documents. It wasn’t exactly transparent.

Anyway, in an OIA request to the Treasury and in a conversation with someone from the Bank I suggested it would be helpful if the monthly indemnity payment amounts by Treasury were to be routinely disclosed. That way, whatever debates we might want to have about the merits or otherwise of the LSAP programme, at least we would all be working with the same numbers.

And thus it has come to be, and this morning a new spreadsheet on the Bank’s website went live with monthly updates on payments and receipts under the LSAP indemnity. The link to it is about half-way down this page.

Here are the two components

Here is the Bank’s own description of the numbers in the blue line

There were net transfers to Treasury for a while because the coupon rates the Reserve Bank was receiving were higher than the (OCR) funding cost.

And here is the chart showing total losses, realised and unrealised.

The total will keep fluctuating a bit from month to month as market rates change, but the variability will gradually diminish as (a) the size of the remaining LSAP portfolio continues to steadily shrink, and (b) the longest-dated bonds have been sold back first. But for at least the last eight months, something around $10bn in total losses has been the best (market price) guess.

There were two points to this post. The first was to use the new data to illustrate better than has been possible until now with hard numbers just what has happened with the LSAP gains and losses over time. And the second was to acknowledge the Bank and thank them for making the data available. The losses probably aren’t something the Bank is really comfortable with, but one shouldn’t be hiding from the hard numbers, and in publishing them regularly now the Bank apparently is not. And that is welcome.

$10 billion is, however, a lot of taxpayers’ money to have lost.

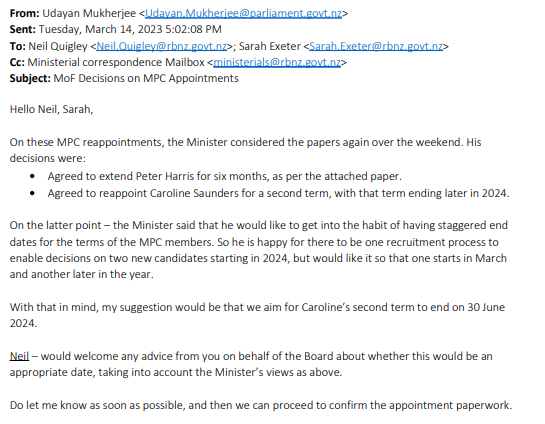

There have been a few posts here recently about Professor Caroline Saunders, whose initial term on the Reserve Bank MPC expired at the end of March and who was eventually, belatedly, and with no announcement at all, appointed by the Minister of Finance to a short second (and final) term on the MPC. The most recent of those posts was here.

When there was no announcement before the Saunders term expired, I had lodged OIA requests with both the Reserve Bank and the Minister of Finance for material relating to her reappointment (or otherwise). Responses to both emails have now come back.

If it is now clear that the bottom line reason why Saunders was not reappointed before her term was expired was administrative slackness (between the Minister’s office and Treasury mainly), the documents that were released don’t put any of those involved in a particularly good light.

My request to the Bank was fairly broadly phrased

I am writing to request all and any material (including any advice to the Minister) relating to the expiry of the MPC term of Caroline Saunders and any discussions or decisions to reappoint her (or not) or to extend her term

and since the Bank says it has not withheld any documents, it seems fair to assume that what I have is all there is.

This was the first document they released, from the minutes of the Reserve Bank’s 7 December 2022 Board meeting/

In other words, there was no paper analysing the record of the MPC or the personal contribution to the MPC made by Saunders, even though the decision to recommend reappointment was being made in the midst of the worst monetary policy failure in the decades since the Reserve Bank was given operational independence around monetary policy. There was also apparently no paper discussing the best balance of the MPC in the period ahead, or the appropriate length of time for a reappointment (not even, apparently, a discussion as to why the recommendation is for an extension of “up to three years” when the law would allow up to a four year second term. There is also no sign in those minutes of any substantive discussion or hard questions being posed by Board members (unsurprisingly perhaps given the lack of relevant background of all but the chair, who presumably had any conversations with the Governor in private, unminuted).

It was, it should be noted, no better when the other two external MPC members were reappointed (for terms from 1 April 2022), but the inadequacy of the process is all the more glaring by late 2022 when the extent of the monetary policy failure, for which MPC members are responsible, was much clearer than perhaps it was to the previous Board in late 2021.

The Board chair then seems to have moved fairly expeditiously, sending a letter of recommendation to the Minister dated 16 December 2022.

although it is not entirely clear whether this was sent directly (it is signed and dated) or only as an attachment to a memorandum to the minister from Quigley dated 9 January 2023. This is the entire substance of that memo

Note several things

(trivially) there is actually a mistake in the letter (Buckle’s second term expires in March 2025 not September 2025

there is no advice (not a word) to Minister about the contribution Saunders had made over her (by then) 3.75 years on the MPC, a period in which (a) the regime was new, and (b) monetary policy was sorely tested.

despite explicitly noting to the Minister that Saunders could be reappointed for four years, the Board chair offers the Minister no information as to why the Board thinks the extension should be only “up to” three years.

presumably after discussions with Treasury, the Minister is told that the process for reappointment should take about two months (this in a document submitted on 9 January). Elsewhere in the formal recommendations the Minister is asked for a decision by 23 January.

And then there are no other documents (and the Minister has also not indicated that he has withheld whole documents) for more than two months. The next document is dated 8 March, only three weeks before the Saunders term expires.

In any country with serious scrutiny of the MPC – and a belief that external MPC members made any difference whatever – serious questions would have been being asked by now, by market participants and by journalists. After all, on paper MPC members wield a great deal of power, and things hadn’t been going that well with monetary policy. But there weren’t.

In an internal Reserve Bank email (to the Governor) we learn that on 2 February “the MoF’s office asked for a clarification to be made to the letters/report which we provided (that CS be reappointed ‘up to 3 years’ subject to the preference of the MoF”.

And again nothing until 4 March when the timeline in this same email records that “MoF’s office call Neil Quigley to seek clarification on Caroline Saunders’ reappointment. On 6 March, the Reserve Bank learns “from MoF’s office that the recommendation will go in the weekend bag….and we should get an outcome early next week”.

And they did

which is strange again, because while the Minister is reported as favouring staggered terms for MPC members (and very sensibly so) he deliberately, and with no officials’ recommendation plumped for a term for Saunders which will mean that the terms of all three external members expire between 31 March 2024 and 31 March 2025. It would have been easy to have given Saunders a three year term or even a four year term and really stretched things out. But he did not, and there is no indication why in any of the papers.

Quigley reverts to the Minister accepting the general idea and a very short extension to 30 June 2024 is agreed. Quigley observes that “Caroline’s term ending at that time is entirely workable from my point of view. As you say, the search for a replacement can still be part of the same search that we undertake to fill the other vacancy from 1 April 2024”. Since it is already May, one might suppose that a new search process – since both Saunders and Harris cannot be reappointed again – will be getting underway fairly shortly.

At this point it is realised that they are too late to get the Saunders reappointment confirmed before her term expires (it needed to go through the Cabinet Appointment and Honours Committee and to be confirmed by the full Cabinet) but nobody seems very bothered by this. As the documents note, and as I initially missed, the (dubious) statutory provisions for MPC appointments allow an MPC to stay in place after their term ends unless advised otherwise by the Minister. But there is no sense of urgency, no sense (perhaps accurately) of any likely media or market interests (despite the on-paper power these positions wield), at least until I wrote a post on 3 April, which prompted the Reserve Bank comms staff to (a) prepare a draft statement if at that late point there were to be any media questions (which there weren’t) and (b) quickly update their website to make clear that members could remain in office after the expiry of their term,

There is no hint in any of the papers released as to why the Minister of Finance chose not to announce formally the reappointment of Saunders (or the extension of Harris, to get around election timing) and rather leave the fact to be discovered either by chance or by assiduous readers of the Gazette.

In the grand scheme of things, perhaps none of this matters a great deal, but the promise was, in reforming the Reserve Bank Act, that MPC members really would matter, and would make a difference. Over four years, there has not been the slightest evidence for it.

But it still seems to be a very bad look, given that the government chose to keep on with the curious appointment model in which the Minister can only appoint people his hand-picked (and not for relevant expertise) Board recommends, that there is no evidence the Board itself engaged in (or received) any serious analysis or review of Saunders’ contribution to the MPC through such a challenging period, and that there is no evidence that any serious substantive advice was being provided to the Minster on her contributions, strengths and weaknesses. It doesn’t reflect much better that there is no sign that the Minister cared, or sought such advice (despite how far outside the target range core inflation has been). The Minister’s office processes seem to have been slack, to say the least. No doubt he is a busy man, but he has a fully staffed office, and there is much justification for sitting doing nothing for two months on a recommendation for an appointment that really should be somewhat market sensitive.

As for Saunders, were she really making a stellar contribution to the MPC (a) the Board might have been expected to have highlighted that and recommended a full four year term extension, and (b) the Minister might have been expected to have enthusiastically agreed (she was after all his preference four years ago). Instead, nothing, and about the shortest credible extension it was possible to have given her.

Finally, there are some issues for any incoming government later this year. As I often point out, a new government that was unhappy with how the Reserve Bank and MPC have been operating cannot simply get rid of the Governor. They can however make appointments around him (including Board and MPC members). Any different government has been given quite a gift by Robertson, in that all the external MPC member positions will expire by 31 March 2025 and all have to be replaced. The Board chair’s own term expires on 30 June 2024 (he was given only a two year (presumably final, transitional) term on the new Board. Given the mediocre appointments to date, and lack of evidence of serious scrutiny and review, if an incoming government really cares about making things better at the Reserve Bank, they will need to take the issue in hand early and make it clear to the Board – themselves quite unqualifed to judge – just what sort of people the Minister will consider appointing (removing, for example, and one would hope, the current blackball on anyone actually engaged now or in future in any serious macroeconomic analysis and research). It is most unlikely that better outcomes (people, process, policy) if Orr and Quigley are simply left to do things as they’ve been done for the last four years.

The question of course is whether the Opposition parties really do care. It is easy to run lines now about “cost of living crises” and high inflation, but (core) inflation is a Reserve Bank outcome and the Minister of Finance is ultimately responsible for, and wields more than a few levers over, the Reserve Bank (people, processes, budgets, and policy goals).

In the meantime, what this little episode reveals again is the empty charade the new MPC is, and always was. We have a minister who was interested in the appearance of change rather than the substance of change, and who has shown no interest at all in holding policymakers to account for signal policy failures. And a Governor who could live with (perhaps even embrace the rhetoric of ) the appearance of change so long as his actual dominance of the process and institution was left substantively unchallenged. A double coincidence of wants, just not one well aligned with the wider public interest.

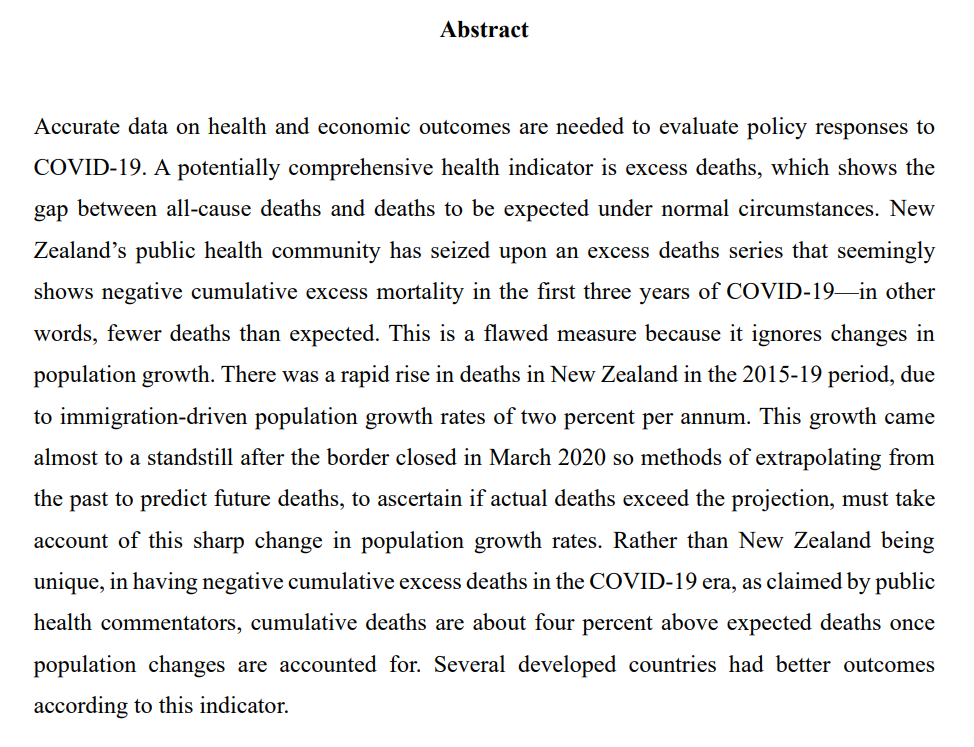

Back in 2020 and 2021, in and around the straight economics and economic policy posts, there were quite a few on aspects of the Covid experience in New Zealand, particularly in a cross-country comparative light.

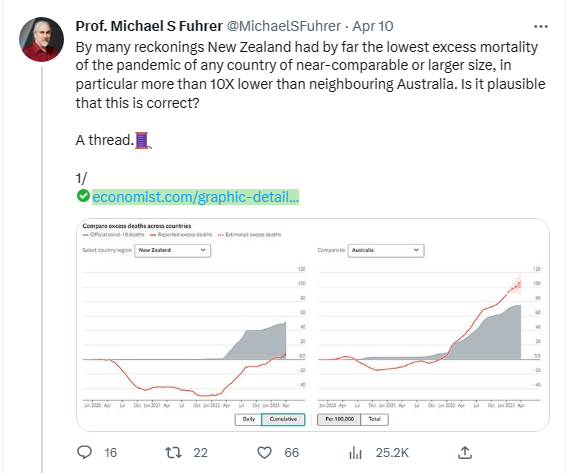

More recently, you see from time to time suggestions that New Zealand’s experience may have been so good that in fact excess mortality here since Covid began might actually have been negative (in which case, fewer people would have died than might have been expected had Covid never come along.

A couple of alternative perspectives on that caught my eye in the last couple of months, both from academics, one from a physicist and one from an economist.

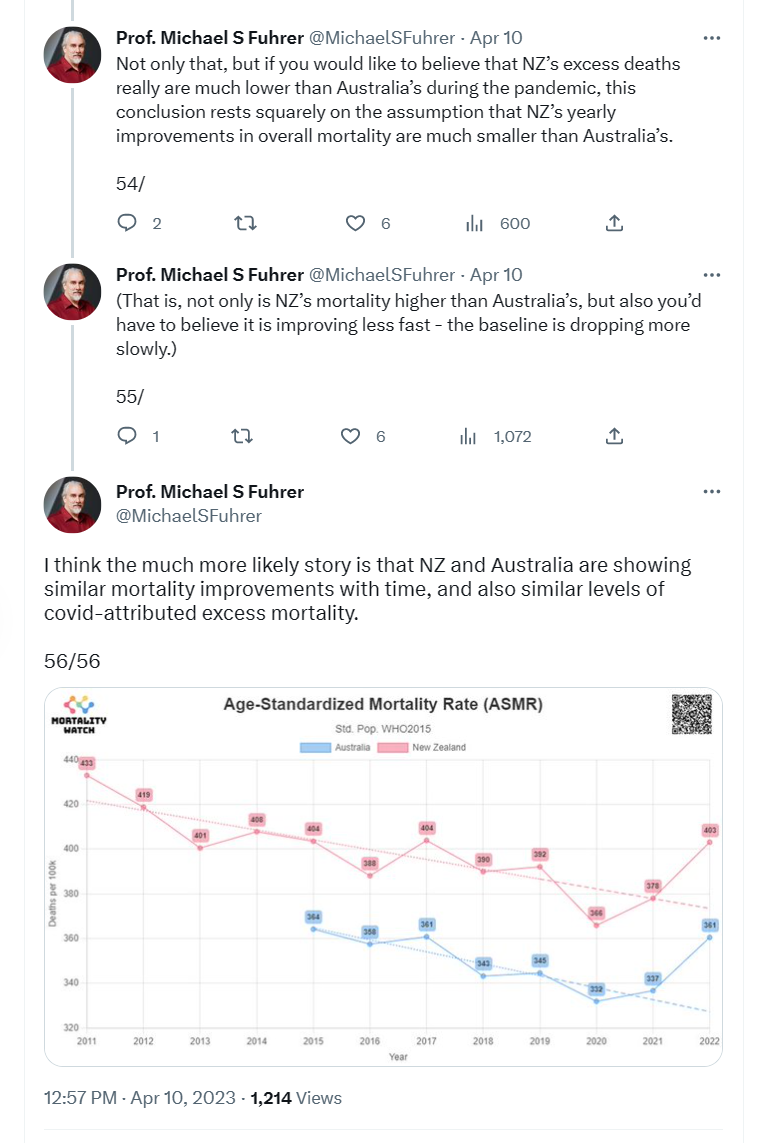

The first was a very very long Twitter thread from Professor Michael Fuhrer at Monash in Melbourne. His thread starts with this tweet

and after reviewing the evidence, and granting that

he concludes that

All of which sounded plausible, at least having read the entire thread.

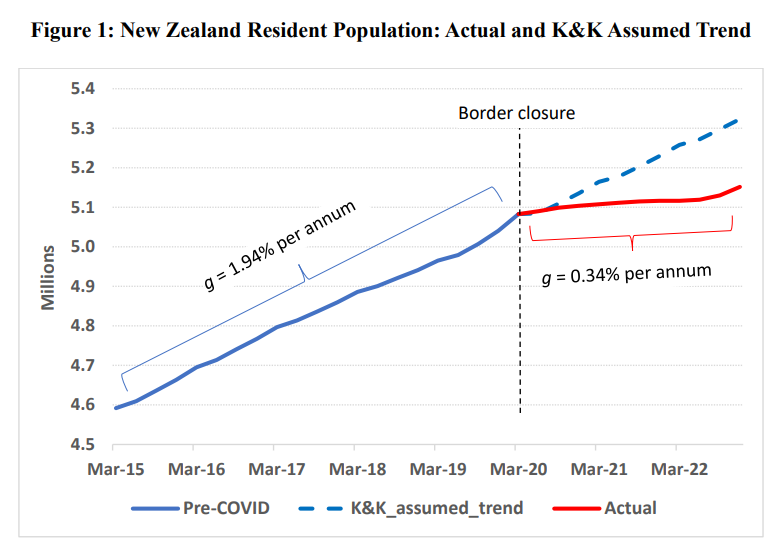

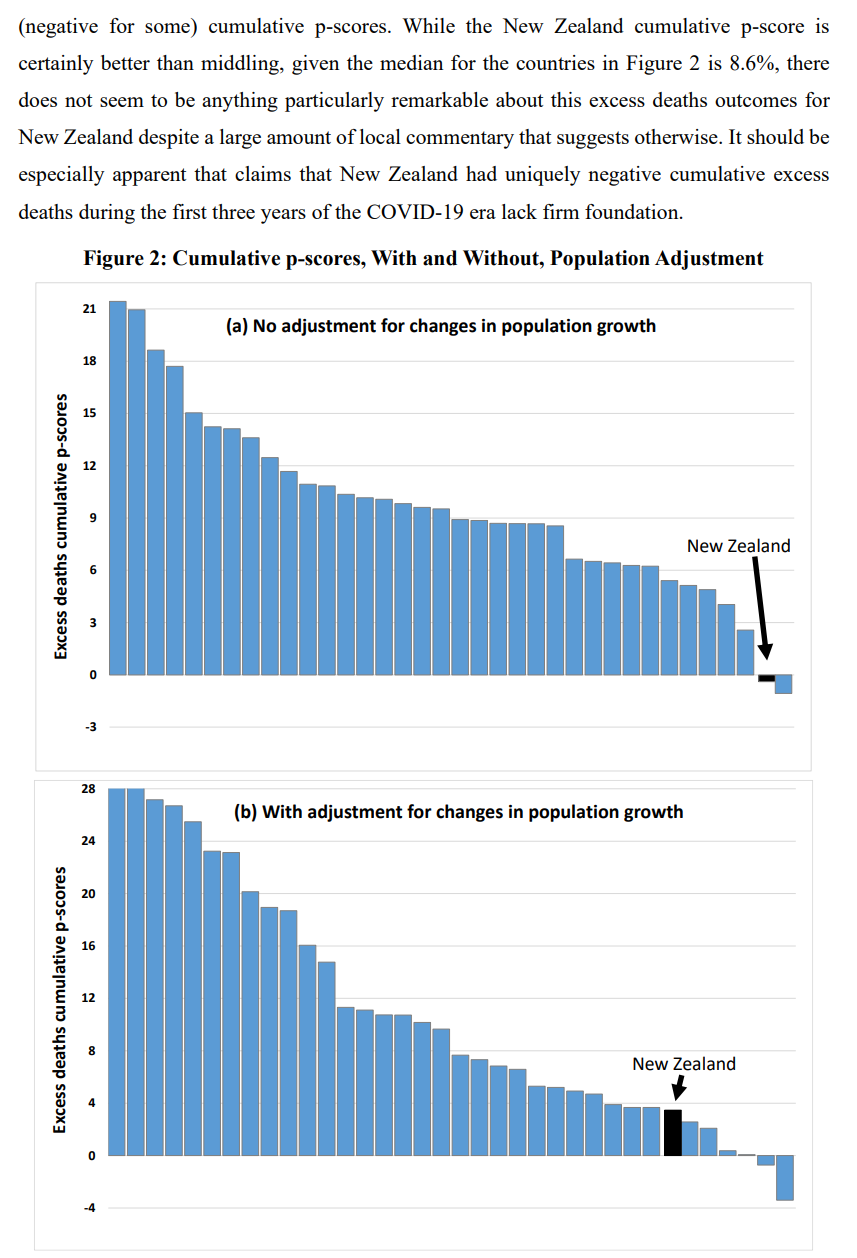

For New Zealand, one of the biggest things that changed over the first 2.5 years of the Covid era was a dramatic slowing in the population growth rate, not because of Covid or other deaths but because net migration went from a hugely positive annual rate to a moderately negative rate. Pre-Covid – and probably again now – migration is the biggest single influence on the year to year change in New Zealand’s population. He includes this chart

Here is Gibson’s abstract

It is a short paper, and easy enough to read, so I’m not going to elaborate further, and will simply cut and paste the final page.

It is a shame he hasn’t labelled all the other countries, but his text tells us that the countries to the right of New Zealand on that bottom chart are Luxembourg, Canada, the Netherlands, Iceland, Israel, and Australia. Note too that several countries just to the left of New Zealand have estimated excess mortality barely different from that estimated for New Zealand.

Across the entire grouping of countries New Zealand still rates fairly well (there are many other things we might reasonably hope to be in the best quartile for but are not; this one we are), but as he notes for the three years to the end of 2022 even in New Zealand there does appear to have been positive excess mortality in the Covid era.

I have no particular point to make, but found both Fuhrer’s thread and Gibson’s note interesting notes, providing some useful context to thinking about the New Zealand experience. Since one still sees claims (including reportedly from David Seymour just a couple of days ago) that there have been no excess deaths in New Zealand over the Covid period, is it too much to hope that some media outlet or other might give some coverage to what appears to be careful work by, in particular, Gibson, a highly-regarded New Zealand academic?

The incoming Australian Labor government last year established an independent review of the Reserve Bank of Australia’s monetary policy functions, structures and performance. The review panel (chaired by a former Bank of Canada Deputy Governor) reported a few weeks ago and their full report is here. Periodic reviews of this sort aren’t uncommon, and are often triggered by episodes of discontent around the performance of the respective central bank (in New Zealand, the 2001 review conducted by Lars Svensson was an example).

There is no clear-cut single preferred way to organise policy functions that society (as represented by government and parliament) wishes to delegate decision-making responsibility to. That is true whether one thinks globally, or just of the subset of advanced economies that countries like New Zealand and Australia usually use as benchmarks or experiences/structures that might offer insight.

If this proposition is true generally, it is no less true of monetary policy specifically. And that shouldn’t really be surprising, including because monetary policy is really quite a recent thing. In New Zealand and Australia the transition to a market-based financial system and a floating exchange rate is not quite yet 40 years old, and even among larger economies floating exchange rates more generally date back only 50 years or so. Modern monetary policy is a cyclical management function (leaning against cyclical macroeconomic fluctuations subject to a constraint of keeping the inflation rate in check), and yet our data sets are really quite limited (since 1984/85 New Zealand has had 4 or 5 business cycles, and the creation of the euro means there are really only perhaps 15 or so advanced-country monetary policy agencies). We simply do not know with any degree of confidence that one form of monetary policy governance etc structure will produce better results over time than another. Instead we (all, including the RBA review panel) argue from small select samples, from specific historical incidents (where multiple influences are always likely to have been at work), and from the mental models we carry round (some likely to have achieved a professional consensus, others not).

None of which is to suggest that such reviews should not take place. Of course they should, and with good people and a government that is interested in good future structures (as distinct, say, from just being seen to having had the review – there were dimensions of the latter around the review then then New Zealand government commissioned from Lars Svensson) useful insights, outcomes, and reforms can often emerge. There will always be aspects of current practice or legislation than benefit from someone standing back and concluding that it is really time for an update, even if in practice the old arrangements were working tolerably adequately.

But one should also be cautious about expecting too much from any particular review or any particular set of reforms.

The current RBA model is not one anyone would prescribe today if they were setting up a central bank from scratch. A fair bit of the legislation dates back to the founding in 1959, including this

It has been interpreted, stretching language and concepts to a considerable extent, as encompassing the way monetary policy has been run for the last few decades, but really it was written for an age of (among other things) fixed exchange rates. No one would write it that way now.

And the governance? The Reserve Bank of Australia Board makes the monetary policy decisions (back in the day in practice the Treasurer did) and is much as constituted decades ago. The Governor, Deputy Governor, and the Secretary to the Treasury are ex officio members and there are six non-executive directors appointed by the Treasurer. The non-executive members have typically been (often quite prominent) business figures, but over recent decades it has been normal for one of the six to be a professional economist. It is a very unusual model these days for the conduct of monetary policy, although note that the sort of people appointed as non-executive directors is a matter of political choice (successive Treasurers) and I can’t see anything in the legislation that would have prevented six technical experts being appointed.

If the relevant bits of the legislation haven’t changed a lot over the decades, practice has. Monetary policy decisions are clearly made independently by the RBA, in pursuit of a target that is in practice agreed in advance with the Treasurer, they are announced transparently, there are minutes of a sort published, as well as the quarterly Statements on Monetary Policy. Senior managers appears before parliamentary committees and have fairly extensive and serious speech programmes. The RBA is a modern inflation targeting advanced country central bank, but operating on quite old legislative foundations. As an organisation, over the decades it has had considerable strengths, including typically a strong bench of very capable senior managers, and people coming up behind them. Successful organisations in many fields tend to promote mainly from within: that has been the RBA approach (and is very much in contrast, say, to the RBNZ). Note here that promoting from within is not itself a basis for a successful organisation, simply one feature that already successful organisations, continually refreshing themselves, often display.

I was an admirer of the RBA for a long time, and 20+ years ago when the Svensson review was underway (when I was both part of the small secretariat and a senior manager at the RB) thought that New Zealand should look to adopt elements of the structure and culture of the Reserve Bank of Australia. They tended to produce more stable outcomes, produce better research, communicate more effectively, and have a stronger sense of legitimacy than our “Governor as sole decisionmaker” system had achieved (or than Svensson’s preference, of a small internal decision-making committee (of which the position I then held would have been a member) was likely to be able to achieve. The RBA on the other hand saw us as somewhat strange, not always entirely fairly. I recall a time when Glenn Stevens as Assistant Governor and he came over to observe our monetary policy and forecasting week leading up to an MPS (shortly after we had started publishing forward interest rate projections), and he emerged from the week genuinely surprised that our approach was far less mechanical, nay mechanistic, than he had been led to expect. Or a visit from David Gruen, then head of research at the RBA, suggesting that the fact that our interest rates averaged higher than those in Australia suggested we had monetary policy consistently too tight (in fact prior to 2009 New Zealand inflation typically averaged in the top part of the target range).

Over recent decades, Australia has enjoyed a reasonable degree of macroeconomic stability (the review report includes a table showing the standard deviation of real GDP growth less than for any other country shown), this in any economy exposed to very big swings in the terms of trade. As noted above, the samples are small but there is nothing obvious to suggest that overall the Australian approach to monetary policy has delivered worse than other advanced country central banks. But there have been troubling episodes, notably including the one in the years running to Covid when Australian core inflation ran consistently well below target (much more so than anything seen at the time in other countries, including New Zealand where core inflation by then was getting close to the target midpoint). There are also more recent episodes of concern – about specifics of the RBA Covid response and latterly about the sharp rise in core inflation – but through that period it is perhaps hard to differentiate the RBA’s failure (underperformance) from that of a wide range of other advanced country central banks (themselves with a wide range of governance models).

This was one of the things that troubled me about the review report. The first substantive chapter is focused specifically on these recent episodes. It is easy to highlight areas where things could have been done better in (almost any) specific episode – and some of the material cited is pretty disconcerting – but that is almost certainly true of every central bank, and there is no attempt I saw in the report to illustrate that anything would have been very much different with a different governance/committee structure. We might hope it would have been, but the panel offers little reason (and realistically they couldn’t offer more) that it would have been. New Zealand, after all, has introduced a committee, and the panel notes favourably (too favourably) the expertise of its members relative to RBA external board members, but many or most of the same mistakes or weaknesses the panel highlight in Australia over the last three years were also evident in New Zealand – as far as we can tell, as less material has been released here than there, us not having had a recent external review and the Reserve Bank’s own review was largely defensive and unenlightening in nature). Should there have been a proper cost-benefit analysis, and serious questioning from the Board, before the RBA bond-buying programme was launched? No doubt (and the review report is properly critical about the absence, and the likely weak case) but there is no evidence of anything even slightly better in New Zealand. Or, as far as I’m aware, in any or many other advanced countries. Perhaps the RBA case was less excusable, since they started bond buying a lot later, rather than in the heat of the crisis, but the practical difference ends up being slight.

The review panel proposes a new model with these important features

monetary policy decisions would in future be made by a Monetary Policy Board (with a separate RBA governance board, and the existing Payment Systems Board),

the MPB would have nine members, the Governor, the Deputy Governor, the Secretary to the Treasury, and six expert non-executives appointed for non-renewable terms of five years, extendable for up to one year)

non-executive members would be expected to devote about one day a week to the role (around eight monetary policy decisions a year)

there would be a press conference for each decision,

votes would be disclosed but not attributable (ie a decision might be made 7:2, but the two would not be identified by name)

non-executive members would be expected to do at least one public engagement or speech a year,

non-executive vacancies would be advertised, but recommendations to the Treasurer (who would make the final appointments) would be by the Governor, the Deputy Governor and a third person (presumably to be chosen – altho by whom, Treasurer or the officials? – from time to time).

If you were starting from scratch, one could think of worse systems. But this proposal seems to have a number of weaknesses and reason to suspect that unless a strong political consensus developed early around making things work really differently (rather than differently in appearance) it is far less good a system than could have been devised. Even then, I would not be overly optimistic. More generally, my impression is that the report tends to underweight the relative importance of the Governor and very senior management to how central banks operate.

Starting with the small stuff, as the report notes it is highly unusual for the Secretary to the Treasury to be a full voting member of a central bank monetary policy decision-making body. It was one thing in 1959 – at that time New Zealand also had the Secretary to the Treasury as a full member of the (largely toothless) central bank board – but it is 2023. Other countries – including the UK and New Zealand – have preferred the model of a non-voting Treasury observer, which seems bit suited to (a) the desire to ensure at the highest levels that information flows freely between monetary and fiscal agencies) and (b) the Secretary’s own primary responsibilities and loyalties. The report proposes amending the legislation to make clear that the Secretary is voting his/her own judgement, but if so that tends to defeat the purpose of their place on the Board (being there solely ex officio), and in times of tension – and one should build system for resilience in tough times, not for when everyone is getting on fine and everything is going swimmingly – will likely complicate the Secretary’s own position (including as adviser to the Treasurer in holding MPB members to account for performance).

In general I am in favour of a model in which external members outnumber executives, but 6:3 in a nine person board doesn’t feel right (even if it parallels current numbers). 4:3, with the third executive being the Assistant Governor responsible for economic policy, seems a better size overall, and also more realistic about the ability of the system to continue to generate a steady stream of able people to fill (only) five year non-executive terms. And a 7 person committee is more likely to limit the risk of free-riding by individual non-executives.

It is difficult to see how a “day a week” model is likely to work IF the goal really were one having a powerful role, including as expert counterweight to staff, if non-executives were devoting only one day a week to the role. I am not aware of any precedents for such a small contribution, which seems to sit closer to the current RBA Board model (might such board members devote 2 days a month to the role, one to the meeting, one to the papers?) than to other advanced country MPCs. At the Bank of England MPC, probably still the best model, non-executives are paid for 3 days a week work, and at a rate that (least by academic standards would be a reasonable fulltime income). On a day a week model, not only is the actual amount of time any member can devote to RBA matters limited, but the remuneration would that for any non-retired person it would have to be just one part of the member’s employment/income. Most plausibly, they would be current academics, who might otherwise not spend a vast amount of time keeping track of data or of the literature in the specific fields relevant to central banking. We might assume that people will not be disbarred (as is NZ) for doing ongoing research in relevant fields, but even in Australia the numbers of such people are not limitless. One day a week looks like a recipe for an ongoing dominance of management and staff. Consistent with this, while the report suggests that externals should have direct access to staff, if they do not have dedicated analytical support staff of their own their ability to make a difference and shape what is in front of the MPB is likely to be limited. This is, incidentally, one argument for a quite different system – as in Sweden or the US – in which outsiders become full insiders while they are MPC members.

The appointment process is also a concern. One of the weaknesses of the New Zealand MPC system is that the Governor exercises considerable effective control on who serves on the MPC. A really good Governor would have a strong interest in promoting genuine diversity of view and real ongoing intellectual and policy challenge. Real world bureaucrats, running their own bureau, perhaps less so. No doubt there will be arguments about “fit” etc, but the value of outsiders is often in the extent to which they are willing to bring fresh thinking and not be easily deterred by management flannel and weight of paper. With a strong “third person”, perhaps it would work out okay, especially if a Treasurer was clearly committed to viewpoint diversity, challenge etc, but many potential “third persons” might be inclined just to defer to the perceived expertise of the Governor and Secretary.

Accountability does not appear to be a key element in the RBA reform proposal. That seems unfortunate – perhaps especially coming hard on the heels of the massive financial losses central bankers have run up and the scale of their inflation forecasting and policy mistake. If as a society we delegate great discretionary power to unelected officials – and that is what we do in MPCs – accountability is a key counterbalance, including in maintaining the long-term legitimacy of the model. At very least, MPB members should be required to have their named votes recorded and disclosed. Ideally – but it is probably only an ideal – people should be able to be removed from office for non-performance. In fact, one of the other weaknesses of the proposed single term model for externals is the complete absence of accountability. Their views don’t have to be disclosed, their votes don’t have to be disclosed, and since they can’t be reappointed, there is really no accountability at all. Lack of accountability doesn’t exactly encourage members to devote intense energies to getting things right. Some no doubt will, but it will be all too easy to defer to management and treat membership of the MPB as a prestige appointment (like being on the RBA Board now), this time narrowed down to being for economists, rather than a role in which one will make a difference and expect to be held to account.

As I said earlier, there is no one ideal structure. In the end, one is trying to combine technical expertise, experience, judgement, ability to communicate, and something around accountability to produce good policy outcomes taken in ways consistent with our open and democratic societies and under structures that are resilient to bad times and to bad people All in a field where uncertainty is pervasive.

Many of these requirements might well be met with no outsiders at all. You won’t see it highlighted in the review report but the Bank of Canada is one in which, formally and legally, the Governor himself wields the monetary policy powers (akin in that feature to the RBNZ system pre-2019). But in practice the BoC has built a strong internal culture and an effective system where a Governing Council of senior internal managers makes monetary policy decisions by consensus. I don’t think it is ideal – there is no individual accountability except (presumably) to the Governor – but the BoC has built partially compensating mechanisms with extensive research programmes, self-review programmes, and extensive engagement with academic and other wider communities. Indeed, the Bank of Canada model – which I do not champion – highlights just how important the quality of staff and internal processes are. It isn’t necessarily a problem if decisionmakers typically defer to staff and management expertise – in fact it is what you would expect in a normal corporate board – so long as those decisionmakers can continually assure themselves that staff and management have robust and resilient processes in place, including those that encourage, generate and accommodate, genuine diversity of view and openness to alternative perspectives. In that sort of context, some expert external MPC members can be very helpful (especially if they are familiar with, engaging with, perhaps contributing to) emerging literature, but they aren’t the only type of member who could add value. The willingness to actually ask the idiot question, and never to be content with management bluster, is valuable in any governance context. Thus, in an RBA context, one might wonder whether it is really worth having a whole new Board (especially when the RBA is not a “full service central bank” (doing prudential supervision)), when one could have left the RBA Board responsible for monetary policy but with a requirement say that several members should have directly relevant professional expertise. One could argue that being a board member, responsible for all the RBA functions and governance, might make for a person better able to contribute effectively as a monetary policy decisionmaker (and note that there is plenty of role for outside expert advisers anyway, and the report does suggest a more active macro research programme for Australia generally). And of course, in all our systems Ministers of Finance – rarely very expert at all – make major contentious economic policy decisions in climates of extreme uncertainty, drawing on expert advisers but rarely handing decision-making power to such experts.

Overall, I can’t help feeling that if the Australian government goes ahead and legislates all these changes, none of them (not all taken together) will matter quite as much as who gets appointed as Governor, and the sort of internal culture and people, the Governor (and his/her successors) build. That is a critical choice – in Australia, in New Zealand, probably anywhere – and is likely to far outweigh any potential difference that a few day-a-week academics, cycled through the decisionmaking system on five year terms, might make. A great Governor (and we can’t build systems that assume one) will build and maintain a culture that delivers most of what the review panel (often rightly) seems to be looking for.

This post has gone on long enough. It is about someone else’s country so why my interest? Two reasons I think. First, it is a significant report on a central bank in the midst of troubled times, and there are few of those yet. And second because the choices Australia makes are always likely to be an important backdrop to any future reforms in New Zealand. We have had extensive reforms, clearly designed to look different rather than be different, and any new government needs to look to do over quite a few of the aspects of the New Zealand model.

I was going to engage specifically with the AFR article last Friday by Ian Macfarlane, former RBA Governor, criticising the review (and I thank the two readers who sent me copies). Time and space is limited, so I won’t. It is worth reading, and he makes some fair points (some less so), but it is perhaps worth remembering that Macfarlane was Governor at the peak of the RBA’s past standing. The starting point now is less favourable.

Finally, one of the background papers for the review was commissioned from Professor Prasanna Gai at Auckland University (and ex BOE). Gai currently serves on the FMA board, but probably should be one of those considered for our MPC, but……he would be disqualified by our Governor and Board on the grounds of an ongoing active interest in areas the MPC would actually be responsible for. Anyway, his paper is quite a good read on international models around the governance of monetary policy, and he pulls few punches about the weaknesses of the New Zealand model.

On Monday I wrote about the MPC membership of Caroline Saunders, whose four-year term had expired on 2 April 2023 and who appeared to be continuing to serve only at the day-to-day pleasure of the Minister of Finance. The Reserve Bank’s website on Monday said that her term had expired, and there was no statement from the Reserve Bank or from the Minister of Finance to the effect that she had either been reappointed or told to go away. That all seemed less than desirable (fact, and lack of transparency).

As I noted in that post, it all seemed rather odd. The election is approaching and the Minister of Finance had already last year reappointed one member, Peter Harris, to a term expiring in October. Under the conventions around elections, no new appointment could be made by the current government when the new term would start smack in the middle of the election period. It seemed reasonable to expect that at some point the Minister would use the statutory power to extend Harris’s term for one final six month period into early next year (by law, having served two proper terms he cannot be reappointed).

But there had been nothing to stop the government reappointing Saunders for up to a further full four year term. And given the (on paper) importance of these MPC positions it seemed careless at best, and a bit disconcerting, that the government had not got on and made a permanent appointment (whether Saunders of someone else – although there had been no evidence of any open search process).

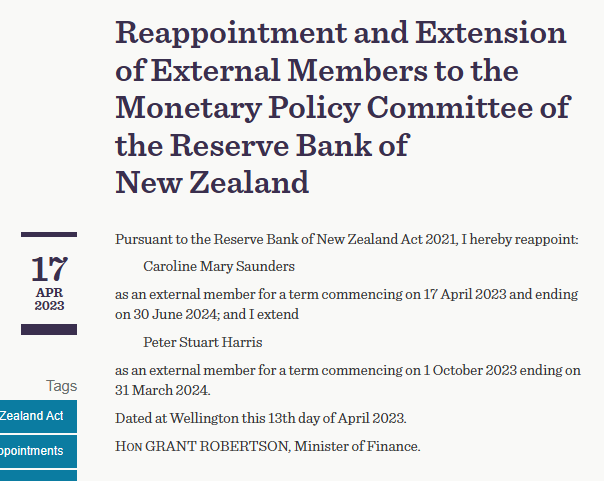

But this morning a piece on Business Desk drew my attention to the fact that decisions had been made on both Harris and Saunders. Naturally, one looks to the Minister of Finance Beehive page for an announcement – these are, after all (and in principle) powerful or influential macroeconomic policymakers at a time when inflation is miles outside the target range the MPC was supposed to be delivering – but there was nothing. There was no press release from the Reserve Bank either, but when I checked the Bank’s website page for the MPC sure enough, there it was:

and

The suggestion being, at least in the new Saunders description, that this might have happened a few weeks ago and neither the Minister nor the Bank had thought fit to tell us.

And so then I turned to the repository of all official appointment announcements, the Gazette, where there is this

which is all good and official, but not many macroeconomists and Reserve Bank watchers routinely read the Gazette.

I have no more to say about Harris specifically. He never should have been reappointed for a short term ending in election season, but given that he was an extension to early 2024 was pretty much inevitable (although a short period with a vacancy also wouldn’t have been a problem).

But what of Saunders? She could have been appointed for a full four year term but has been given only 15 months or so. Was she reluctant and had to have her arm twisted to take an extension. Was the Bank’s Board reluctant to recommend her? Was the Minister really not so keen (having, from the papers, first appointed her mainly for her sex). And why was none of its sorted out months ago well before her first time expired. It is hardly a ringing vote of confidence in a macro policymaker, amid a serious policy failure, to be reappointed for such a short period only, especially as the result of her appointment is the end of the external member terms (and all will have done two terms and have to go) are now bunched quite tightly: Harris finishes on 31 March next year, Saunders’ term finishes on 30 June, and the third member (Bob Buckle) has a term finishing on 31 March 2025.

If there were to be a change of government later this year, this combination looks opportune. I wrote a post last year about what a new government could and couldn’t do quickly if they were serious about overhauling the Bank and MPC. They can’t get rid of the Governor (who has just started a second, but final, five year term. But they would be able to (would have to) replace all three external MPC members in fairly short order. It would be an opportunity to insist on a quite different approach (eg the repeal of the blackball on anyone with ongoing macro analytical and research interests and output).

Which from a National Party perspective looks good of the current government. But one is still left wondering why Robertson left things this way. He could have reappointed Saunders for four years, or could have replaced her with someone he was comfortable with for a four year term. Instead, he is leaving the way open for the other side if the election does not go his way.

As I noted the other day, I have several OIA requests in around these appointments, which may (or may not) shed some light. They are perhaps unlikely to tell us why the Minister, the Governor, and the Board chair were so reluctant to let us know about the appointments of these (supposedly) powerful macro policymakers. Perhaps they’d have struggled to craft an honest press release on the achievements of these policymakers in their four years so far, when – for the first time in decades – inflation blasted well away from target, and none of them was prepared to front up with a good story about the inflation outcomes they’ve delivered, let alone the massive financial losses their choices resulted in for the taxpayer.

Perhaps some journalist might seek comment from Robertson, from Orr, from Quigley or from Saunders. Or perhaps even from Nicola Willis who no doubt expects to be in a position to make all those MPC appointments before too long.

Over the last few days I’ve been reading a few pieces on UK monetary policy and high inflation. The first was a speech from the Deputy Governor responsible for economics and monetary policy, Ben Broadbent (over there senior central bankers actually give serious and thoughtful speeches on things the Bank has responsibility for), and the second was a new paper by long-term adviser, analyst and researcher Tim Congdon. There is a lot of overlap because Congdon’s paper is broader (“Why has inflation come back”) but his analytical approach has tended to emphasise the monetary aggregates, while Broadbent’s speech which is narrower in focus is specifically on the question of what information value for monetary policymakers there is (or isn’t) in the monetary aggregates over the longer term and in the specific context of the inflation of the last couple of years. Both are worth reading.

My own view on the monetary (and credit) aggregates is, I think, pretty much the same as that of most central bankers these days, that the indicator value of these aggregates is typically fairly limited in the world we inhabit (low or – at present – moderate inflation), that any really serious breakout of inflation (think, eg, Argentina) is likely to be accompanied, in some sense or other, by rapid growth in the quantities of money, and that for now while one should never ignore any indicator there isn’t much about inflation developments of the last couple of years that is best explained through the lens of monetary aggregates. Specifically, if bond-buying programmes like the LSAP did anything much to boost inflation, it was not primarily (or at all) through a monetary quantities channel.

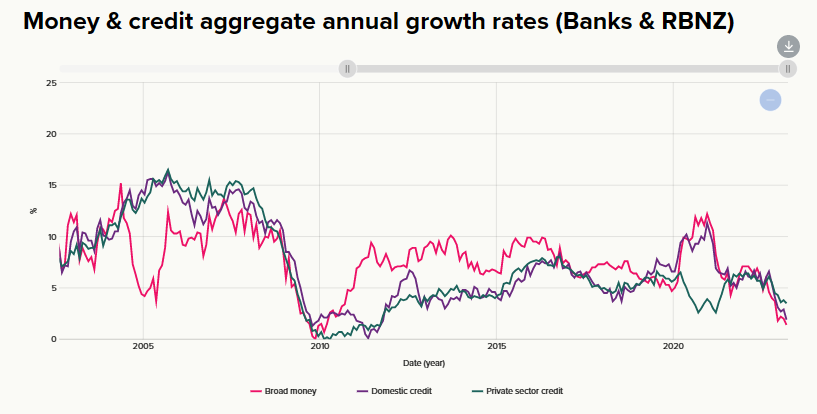

Here is some New Zealand data (and an RB chart) on the growth rates of the monetary and credit aggregates over the period since September 2002 when the current inflation target was adopted.

At the Reserve Bank we always used to put more weight on credit developments than on money measures, and credit growth dipped quite materially in the early months of the pandemic, but no model using either monetary or credit aggregates is isolation would have given policymakers (or other forecasters) reason for serious concern about an outbreak of core inflation to rates unprecedented for decades, Indeed – and since we don’t run a price levels targeting system, and thus bygones are treated as bygones – an analyst looking solely or mainly at these indicators would have noticed by mid 2021 that all the annual growth rates were back to around 5 per cent. No one was going to be sounding inflation alarms if their analysis was based largely on those growth rates. Even in the short period when annual money growth exceeded 10 per cent, the growth rates were not very much higher than had been seen not infrequently over 2011-2016 when core inflation was materially undershooting the target.

Each country’s data and experiences are a bit different but as a general proposition I’d be surprised if many central bankers have become any more positive on the short-term indicator value of the monetary aggregates in the last couple of years.

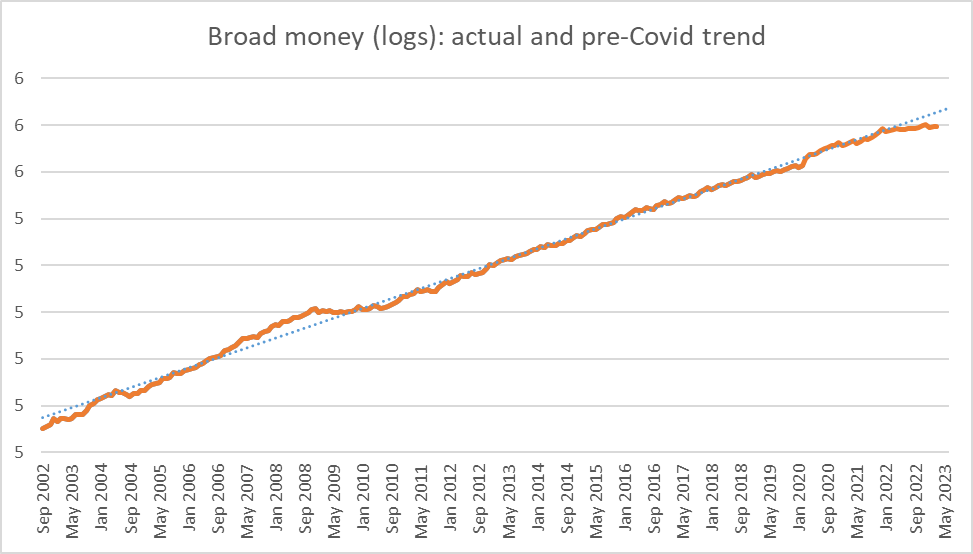

As one final money aggregate chart, here is the level of the New Zealand broad money series relative to the trend over the pre-Covid period since the 2 per cent inflation target was set. Over that almost 18 year period, core inflation averaged 2.2 per cent. At present, broad money is sitting below the trend, and although views currently differ on how much disinflationary pressure is now in the system I’m not aware of anyone who thinks we are about to have a 8-10 per cent drop in the price level, to get back to price levels consistent with long-term average inflation of around 2 per cent.

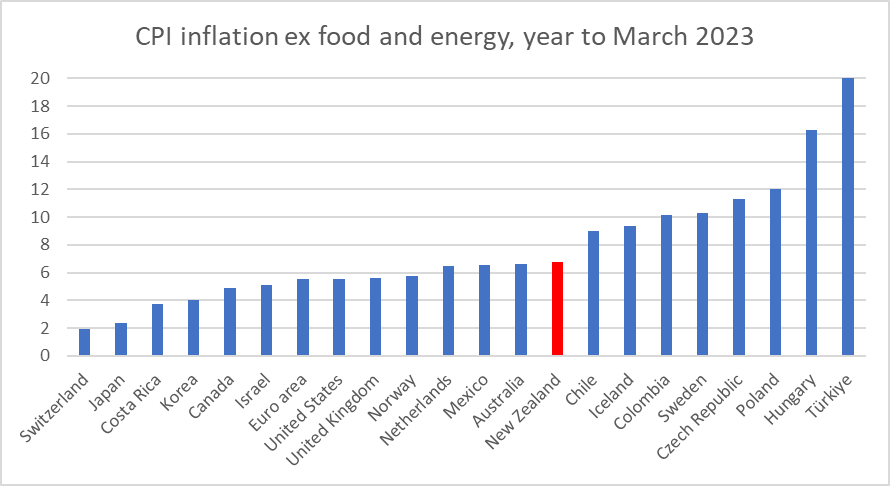

The UK has become a bit of a poster boy for bad inflation outcomes. Some of the headline numbers have been very bad (up around 10 per cent), but some of that is what happens when a gas price shock hits you (and no monetary policy framework tells a central bank it should try to offset the direct price effects of such a shock). But if we use a common measure of core inflation (CPI ex food and energy), the UK is far from the worst of the advanced economies and has a bit less-bad core inflation outcomes at present than New Zealand (or Australia).

If their central bank hasn’t done a great job, ours has done a bit worse. And the diverse outcomes in this chart remind us – as Congdon explicitly does in his paper – that inflation outcomes are ultimately national in nature, choices by central banks and (by default usually) their political masters. That we have similar core inflation to several countries on the chart – but quite different outcomes to sound and responsible countries towards either ends (Switzerland, Korea, Sweden, Czech Republic eg) – speaks more to similar mistakes made by respective central banks than to anything that was out of the control of the Bank of England or the Reserve Bank of New Zealand.

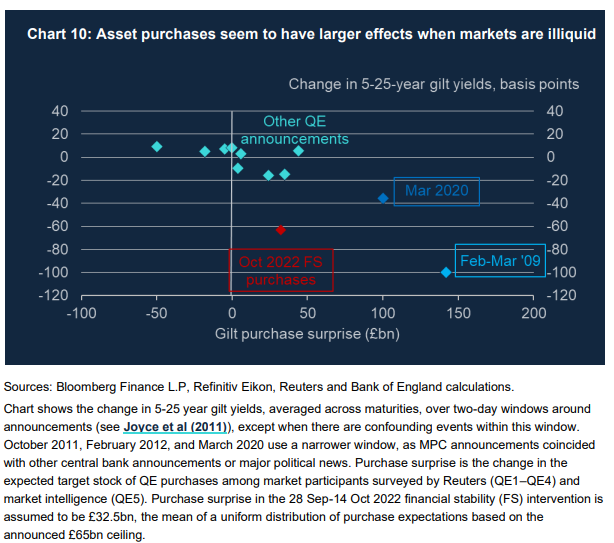

Two charts in Broadbent’s speech caught my eye. The second (which I’ll come to in a minute) was directly relevant to the inflation mistake. But this was the first on the interest rate effects of central bank bond purchase programmes. The Bank of England, like the RBNZ, believes that QE has macroeconomic effects primarily through interest rate effects (rather than the quantities of fully-remunerated settlement cash balances that are created in the process).

Broadbent reckons that bond purchase programmes have a material announcement effect (what is measured here) when markets are very illiquid. That is no surprise, and probably everyone would agree. But what caught my eye was those “Other QE announcements”. The average of the interest rate effects of those nine announcements is close to (and not significantly different from) zero. Perhaps this particular estimation is wrong, but wouldn’t it be nice if our central bank was producing such charts, and the research supporting them, rather than just handwaving estimates of large number effects, that often conflate March 2020 (and the effects of what the Fed was doing at the same time) with the rest of their highly risky and costly programme?

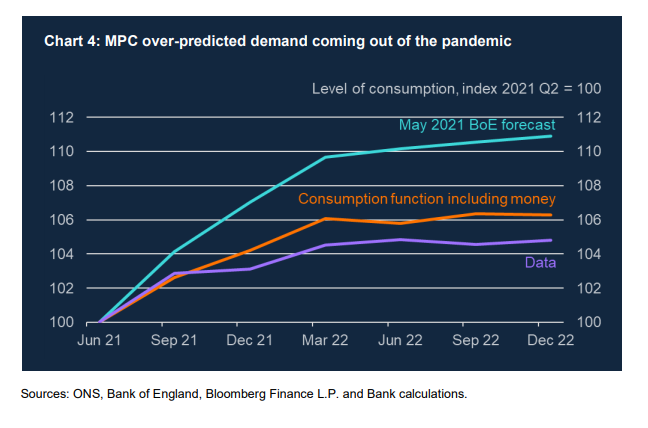

The other Broadbent chart that caught my eye was this one

Broadbent is using it primarily to make the point that the BOE actually forecast growth in real private consumption stronger than would have been implied by a model incorporating data from the monetary aggregates. But what interested – surprised – me was that they had ended up materially over-forecasting real consumption growth (from the point where the UK’s last lockdown ended). Normally, over-forecasting a key component of domestic demand would probably have been associated with over-forecasting inflation. But not this time (and the biggest error was before, not after, the severe adverse terms of trade shock associated with the Ukraine war)

That got me wondering about the Reserve Bank of New Zealand’s forecasting.

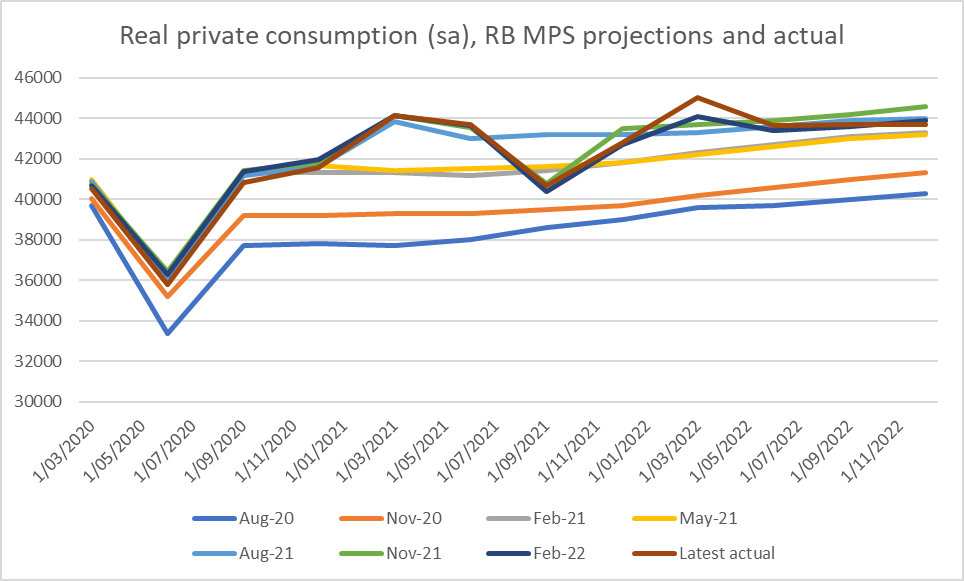

Here are their successive MPS forecasts for real private consumption, starting from the August 2020 MPS which was done after the first and worst national lockdown was over.

The errors in the forecasts for 2022 being made in late 2020 are really huge (for consumption, which is not a particularly volatile component). By mid-2021 (when those BoE forecasts above were done) there were still quite big errors, but not so much about the medium term forecasts but about what the level of consumption spending was at the time the forecasts were being done.

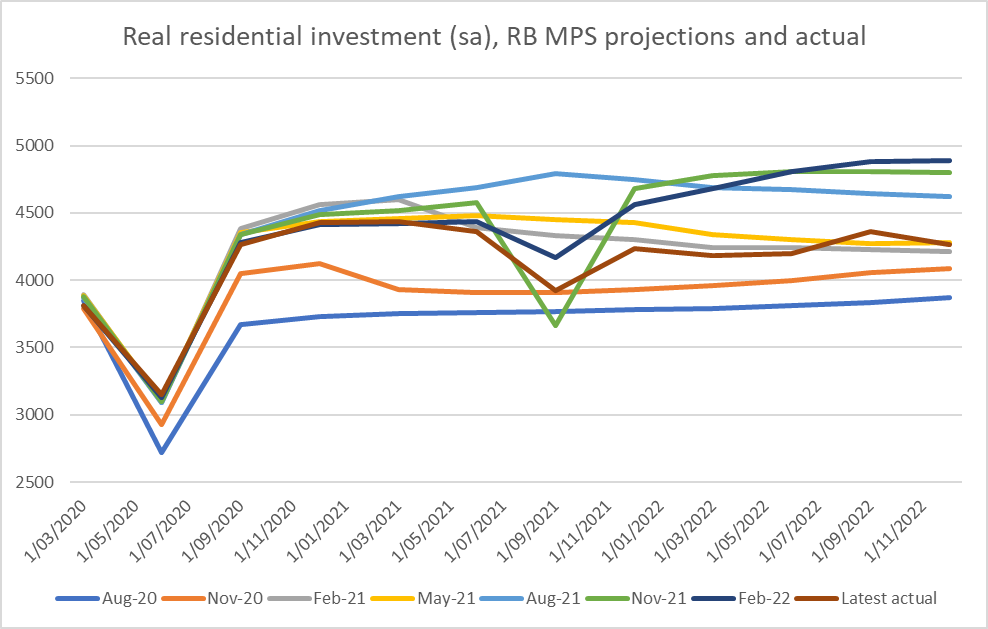

What about real residential investment?

Their forecasts for late 2020 and 2021 undertaken in late 2020 were miles off the mark, substantially understating the level of activity happening already and in the following few quarters. More recently, actuals have undershoot the forecasts done in the second half of the period, probably because of the much higher interest rates that proved to be needed relative to what the Bank had expected a couple of years ago.

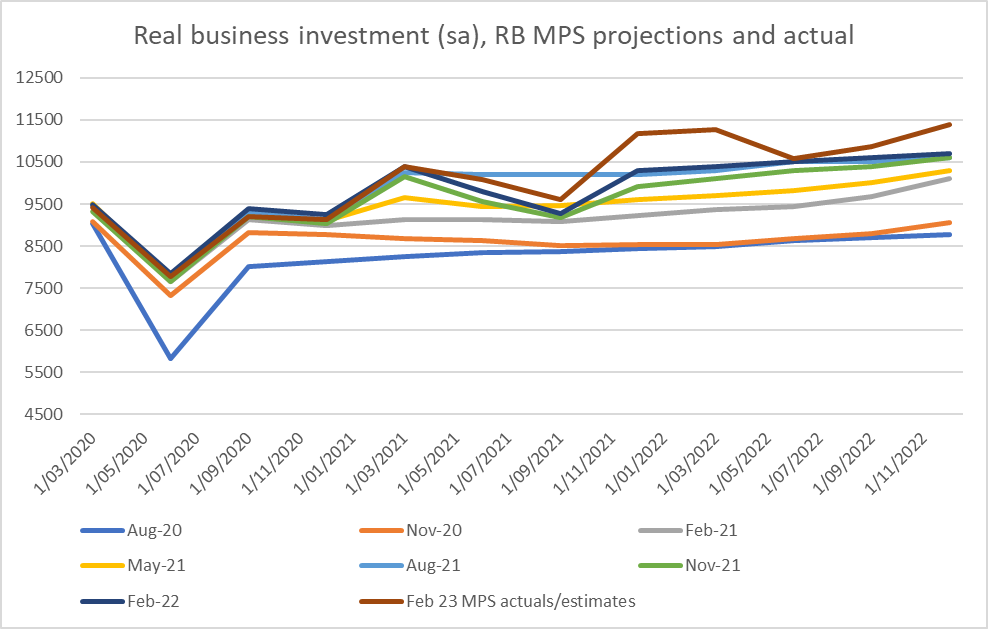

And here is real business investment

The Bank was badly misjudging the recent and contemporaneous situation in their August 2020 forecasts. That gap had closed substantially by the November 2020 MPS (a key date because the Bank then had such extremely low medium term inflation forecasts), but as with the private consumption chart shown earlier the forecasts for 2022 were still miles too low. Those errors probably go together, since high consumption demand and activity is typically likely to support high business investment spending. What is interesting is that business investment continued to surprise the Bank on the upside right through to the forecasts being made early last year.

I won’t clutter the post with a comparable GDP chart, but will quote just one illustrative number. In May 2021 I found myself in the curious position: for the first time in a decade, I had become more hawkish than the Bank. With hindsight it is abundantly clear that they should have been raising the OCR by then (and earlier). But their GDP forecasts made in May 2021 for December 2022 proved to be off (under-forecasting) by almost 3.5 per cent. Those are big mistakes.

If there is some mitigation for the BoE in having actually over-forecast the private consumption bounceback (one would want to know more about other components on demand) there is nothing like that in the New Zealand numbers. The Reserve Bank simply misjudged (badly) the strength of key components of domestic demand (and you’d see something similar in for example the unemployment rate forecasts and outcomes), and with it core inflation. One could fairly point out (and I have in previous posts) that many (perhaps almost all) private forecasters made similar mistake. But we – taxpayers and citizens – don’t employ private forecasters to keep core inflation near target; we employ and mandate the Reserve Bank (Governor and MPC) to do so, and they failed.

Which brings me back to those UK papers that started this post. One of the best bits of the Congdon piece was the call for some serious accountability for central bankers.

No one forced top central bankers to take their jobs (most would probably have had little problem getting other roles), and if they thought the mandates they had been given (in both the UK and NZ the finance minister sets the goal) were unachievable or unrealistic they were free to have said so and, if they felt strongly enough, to have resigned. Nobody was compelled to take on a task they believed was simply unachievable. And yet we’ve ended up with (core) inflation well outside target ranges in quite a wide range of countries, including both the UK and New Zealand, with no apparent consequences for any individual central bankers

Congdon proposes (in the UK context) that when inflation is sufficiently far outside the target range, both the Governor and the Deputy Governor should be required to offer their resignation. He doesn’t say so explicitly, but I presume he must mean this as more than the sort of pro forma charade one could imagine it descending to (“of course, I have to offer my resignation but we all know you Chancellor have no intention of accepting it”), involving actual departure from office. And one could, and probably should, broaden the expectation of real sanctions to include all the MPC members. There is (a lot) more scope already in the UK model for individual MPC members to express and record their disagreement with the majority view, but there is room for more, and the serious threat of sanction helps to sharpen incentives to think differently and not simply to (as is an easy incentive in any committee context) to hide behind the committee, and the (in recent cases) badly wrong consensus or majority view. In New Zealand, we have no idea whether any MPC member ever seriously questioned where the Bank’s forecasting and policy were going in 2020 and 2021. We should.

Perhaps what grates most about central bankers (and their masters, who go along with this behaviour) is the utter refusal of almost all of them to ever accept any serious personal responsibility. Here, Orr has repeatedly run his “no regrets” line and when he occasionally departs from it it is just to say that he is sorry New Zealand faced a pandemic and the Ukraine war (ie nothing about anything he or his colleagues are responsible for). He and his chief economist have also tried the line that they couldn’t have done much different – of course raising the OCR one meeting earlier wouldn’t have made much difference, but that isn’t the appropriate test – and there is quite a hint of that sort of defence in Broadbent’s recent speech (where he uses a straw man alternative of looking at what it would have taken to keep headline inflation at target, when the policy focus has never been primarily on headline).

The other day someone sent me a column from a UK newspaper in the wake of various recent BoE comments. The column ended thus

In the spirit of openness that an independent Bank of England is supposed to represent, it should offer a full and frank apology for letting down the British people.

Well, quite. And exactly the same could be said for our Governor and MPC. They made a really big and costly series of mistakes, which cost us (but not them particularly) a great deal of disruption and real economic loss. They failed in a mandate they had voluntarily chosen to accept (and been well-remunerated for). I’m a Christian and so contrition and repentance are pretty central to my world view, and whatever mistakes have been made in the past contrition and repentance go a long way. In public life – and nowhere more than among central bankers – it now seems alien and inconceivable that people could simply front up and acknowledge their mistakes, acknowledge the costs and consequences of those mistakes, and ask for forgiveness.

Instead, we pay the price – massive redistributions, big fluctuations in real purchasing power, overfull employment and then a probable recession, (oh, and don’t forget the $10bn of LSAP losses – an amount that would otherwise have more than covered the Crown’s recent cyclone costs) – and the central bankers just sail onwards enjoying their position, status, salary and so on, not even offering a serious accounting, let alone serious engagement, or any personal loss . Great power (which is what central banks wield) misued with no personal consequences whatever is a very long way from the model of delegated responsibility and accountability that shaped the design of both the UK and New Zealand central banking reforms in recent decades. In New Zealand, that isn’t just the responsibility/failure of Orr and the MPC, but of the Bank’s Board (appointed by the Minister supposedly to serve the public’s interest), the Minister of Finance, and ultimately – as with everything important in a system of government like ours – the Prime Minister.

Decades ago I worked for a central bank in another country. I woke up one morning to learn that the Governor had been sacked, and by the time I got to work he was clearing his desk. He hadn’t done a bad job – and was one of the more inspiring people I ever worked for – but had fallen foul of the government (Minister of Finance and his colleagues/bosses). The law as it was meant that Governor could be removed whenever the government felt like it. for whatever reason the government felt like. It wasn’t a good model.

In the numerous attempts to capture just how independent various central banks are, one of the dimensions that usually appears is something around the dismissal provisions for key decisionmakers (in these days of committees and board, not just the Governor). Many older pieces of central banking legislation make it very hard to remove the Governor (in particular), removal often requiring things like the bankruptcy, severe mental or physical breakdown/incapacity, or imprisonment (and perhaps even a vote of Parliament). The Reserve Bank of New Zealand Act 1989 was quite unusual for its time, in that it made it easier to remove the Governor, but not because the Minister didn’t like the Governor’s policy calls (and all power was vested in the Governor personally) but if the Governor had failed to deliver on the policy targets he had agreed with the Minister that the Bank would pursue. Under the Act (and rightly so) the Bank didn’t get to define its own goals: the Governor got independence at an operating level to pursue an agreed policy target, and could be removed (at least in principle) if he did a poor job of using the operational independence. The Governor could not be sacked simply because the Minister got annoyed with him, or because the Governor had been appointed or reappointed by a ministerial predecessor of a different party.

That is pretty much as it should be. You can argue (and I long have argued) that even with a well-written law it is hard to make such accountability effective, and the dismissal of a Governor on policy grounds is almost inconceivable (reappointment could, in principle, be another issue) but the balance on paper is probably more or less right.

But these days we have a Monetary Policy Committee to make monetary policy decisions. The government chose to adopt a model in which several external members serve on the MPC, and I’m pretty sure it would not be hard to find speeches from the Minister of Finance championing this innovation and the important contribution people with a diverse range of views and experience would bring to monetary policy decisionmaking.

In principle, appointments to the MPC are at a considerable arms-length from the Minister (the Board proposes candidates and the Minister can’t substitute people he or she prefers). On paper, members of the MPC can’t be removed because the Minister doesn’t like them or because they advocate monetary policies the Minister doesn’t like. It is hard to remove an MPC member

(Actually doing monetary policy in accordance with the Remit is one of the “collective duties”.)

What is more, at least on paper MPC members can only serve two terms, so if there is a bit of an incentive to stay on the right side of the Minister in the run-up to reappointment, at least any such period shouldn’t last long.

If you believe in an operationally independent central bank (and, on balance, I still probably favour one), the basic framework looks good. The Act does actually allow the Minister to explicitly override the Bank on monetary policy, but that has to be done openly and formally, not by the dangling threat of dismissal.

But then the Caroline Saunders term came to end (or so it appeared) and we were sent back to check the statute books. I wrote about it here. There we were reminded that there was a provision for an MPC member to have their term extended for up to six months. This appeared to be a more or less sensible provision given that election timing sometimes interferes with the making of permanent appointments or reappointments to significant government roles (although other than for the Governor hardly a vital provision given that there are seven MPC members in total, and the MPC could probably function just fine for a few months with 5 or 6 members), and it was quite similar to a position in the UK central banking law.

What probably few of us noticed was that the law also contained a provision under which when an MPC member’s term of office ends they can simply remain in office unless or until the Minister of Finance actively appoints another person or tells the person whose term in ending to go.

Caroline Saunders’ first term as an external MPC member expired a month ago and she is still in office (it is now May and the Reserve Bank website shamelessly continues to describe her term ending in April). There has been not a word from the Minister of Finance or the Bank (Board or Governor) as to what is going on. In effect, the Minister of Finance has transformed Saunders’ position from one that looked like an explicit fixed term one to one in which she serves from day to day at the pleasure of the Minister of Finance. Just like my story in the first paragraph. It is a terrible way to be doing things (and a month on is clearly a conscious and deliberate choice by Robertson, not a matter of a few days until last minute reappointment loose ends could have been tied up).

To be clear:

there is nothing to have stopped the Minister of Finance formally reappointing Saunders to a further full four year term (at least, so long as the Minister’s handpicked underqualified Board was willing to recommend here),

there would have been nothing to have stopped the Minister formally extending Saunders’ term for up to six months (seems not to even require a Board recommendation), a term that itself would have been short but fixed.

But there is no sign that the Minister or the Board have put in place any process to reappoint or replace Saunders (although I have various OIAs in which may shed some light), and instead the Minister has setted for a de facto “dismissable at will, serving at the pleasure of the Minister” model. It has got no coverage, but it should have, including because it sets a terrible precedent.

Since he has said nothing,and has been exposed to no media or parliamentary scrutiny, I have no idea what is going on in Robertson’s head here. I don’t really believe that he has done it to exert policy leverage over Saunders (“keep voting a way I’m comfortable with or you’ll be gone tomorrow) both because no one believes the external members wield or attempt to wield any clout, and because Saunders has a day job in other fields (she doesn’t really need the MPC role). It is also odd because the election is approaching and you’d have assumed this government wouldn’t want to risk leaving an open seat for an incoming Minister to fill early on (they will already be unable to appoint pre-election a replacement for another external MPC member, Peter Harris, whose term expires in October). Perhaps I’m being too charitable, but whatever the explanation (a) we should be getting one, and (b) if small things are allowed to slide it opens the way to more serious abuses and pressure by others later. MPC members simply should not be dismissible at will, and at present Caroline Saunders is. The current situation reflects poorly on the Minister, but also on the Board and the Governor (who have presumably gone along), and actually on Saunders, who if she cares at all about operational independence for monetary policymakers should have insisted that she be reappointed formally or, if not, should have walked (which she could have done with no drama whatever). An incoming government that was serious about fixing the deficiencies in Robertson’s legislative reform of the Reserve Bank should simply repeal the “serve at the pleasure of the Minister” provision (I am not aware that comparable advanced country central legislation elsewhere has that sort of provision, especially when there is already statutory provision for a short fixed-term extension to deal eg with election timing issues).

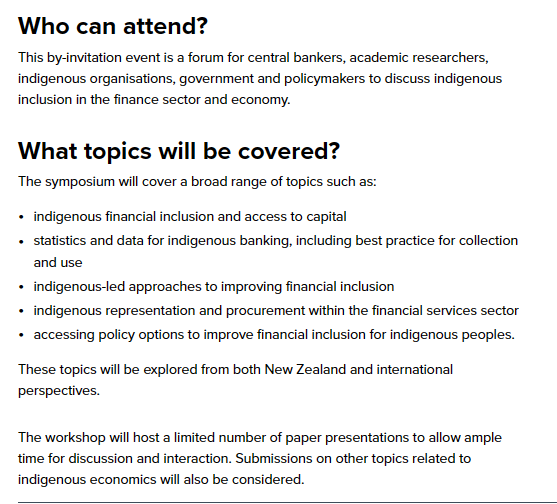

Changing tack, I stumbled on this call for papers on the Reserve Bank website the other day

Were it the website of a university sociology department or policy centre it might all be rather unexceptional, but this is the central bank.

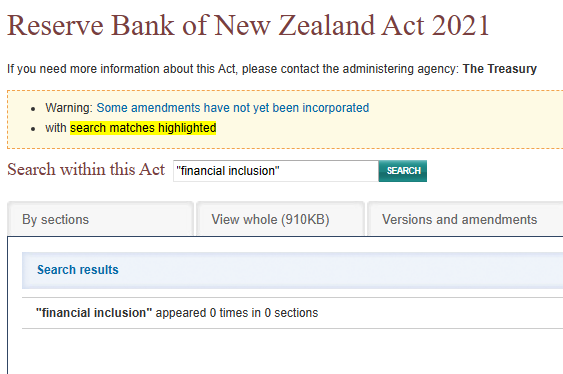

The Reserve Bank of New Zealand Act, freshly minted, sets out objectives for the central bank and functions for the Reserve Bank. I won’t bore you with another big cut and paste. Suffice to say, neither of those sections mention, or even hint at, “financial inclusion”. In fact, the words don’t appear in the Act at all.

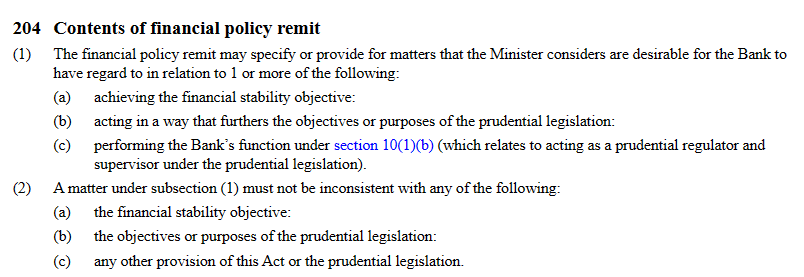

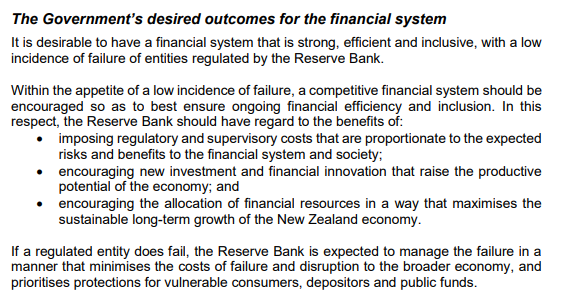

Now, the Reserve Bank would no doubt point out the under the new Act there is a new document, the Financial Policy Remit. The first one is here. But the legislation itself makes it clear that whatever the Minister puts in the Remit, it is all about the exercise of the Bank’s statutory powers, fulfilling its statutory functions and purposes. It isn’t licence for the Bank to go spending public money and scarce management focus on just anything it, or even the Minister, might like.