This is mostly a follow-up to my post last Saturday on the LSAP losses.

In that post I noted that while the LSAP was still running, the monthly line item on the Reserve Bank balance sheet recording the Bank’s mark-to-market claim on The Treasury under the indemnity was a reasonable proxy, on prevailing market prices, of the direct fiscal losses the LSAP programme would result in. And it was an official number.

The Reserve Bank published its monthly balance sheet for the end of March. The Bank’s claim under the indemnity as at 31 March stood at $7821 million.

However, as I also noted in Saturday’s post, this number is no longer even an approximate estimate of the direct fiscal losses from the LSAP programme. It is still a best guess, on market prices, of the unrealised losses on the bonds the Bank is still holding.

But the Bank’s holding of bonds are now much lower than they were at peak. In the programme as a whole, the Bank purchased government bonds with a face value of $53480 million and LGFA bonds with a face value of $1735 million. All of those purchases were covered by the indemnity.

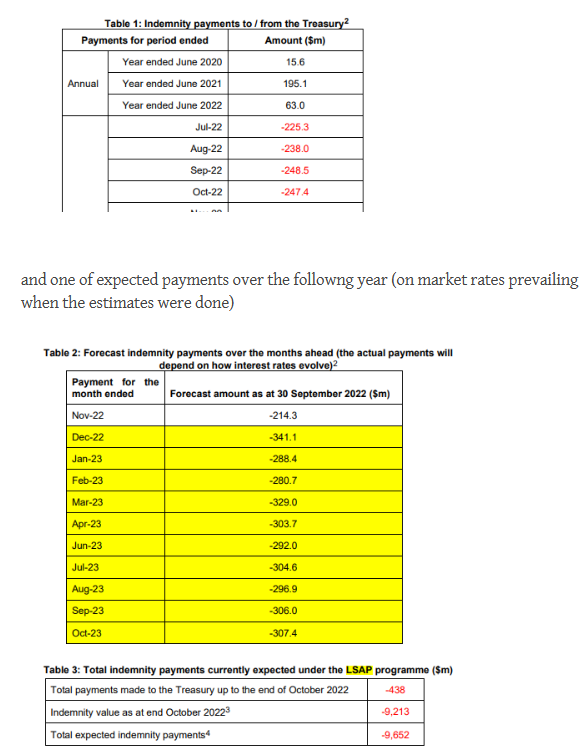

However, since July last year the Bank has been selling back to The Treasury each month government bonds with a face value of $415 million. Total sales to date – most recently a parcel on Monday – total $4150 million. The resales programme is starting with the longest-dated (most risky) bonds, on which the largest percentage losses will typically have been made. As those bonds are sold back to The Treasury the Reserve Bank’s losses are realised, and their claim on the indemnity is met each month by The Treasury. (In addition, as the table below records, there were some payments from the RB to Treasury in the period before resales began, which may represent higher coupon payments to the Reserve Bank exceeding the Reserve Bank’s (OCR) funding costs during the very low OCR period.)

There appears to be no easy place to find the monthly indemnity payments (I have suggested to Treasury that in the interests of transparency it would be good if they or the Bank provided such a table), but there were some hard numbers, and some indications, in a November 2022 Treasury paper that I drew from in Saturday’s post

Actual market rates have changed since then, but the total payouts to date could be almost $2 billion.

In addition to the sales back to The Treasury, some of the bonds the Reserve Bank purchased have matured in their hands.

On the LGFA side, $216m (face value) matured in May 2021, $250m in April 2022, and another $250m this month.

In respect of government bonds, $1300m matured in May 2021 (and on those bonds the Crown appears to have roughly broken even from having done the LSAP purchases – the OCR, the Bank’s funding cost, having been 0.25 per cent throughout the period the May 2021 bonds were held), and another $7471 million (face value) matured a few days ago, 15 April 2023.

As a reminder, here is what the Reserve Bank is indemnified for

Whatever claim the Reserve Bank had in respect of the April 2023 bonds will presumably drop out of the reported indemnity claim balance sheet item in the next balance sheet and will have been met by Treasury in their monthly payment.

Total LSAP bond purchases were $55215 million (face value). Maturities and resales mean that the face value has been reduced by (face value) $9487 million [correction $13637m – the original number was just maturities]. The monthly reported indemnity claim item on the Reserve Bank’s balance sheet captures only the market-implied loss on the bonds still held. But the total direct fiscal losses on the programme – not reported very transparently – include the substantial realised losses already settled by The Treasury. Each month – while market bond rates remain high – the realised losses will mount and the indemnity claim item (while fluctuating from month to month) will be trending down. When the last bonds mature or are sold (several years away yet on current plans), the Reserve Bank balance sheet indemnity item will drop away to zero. But large losses will have been met by the taxpayer – on what we know at present, probably something like $10bn of them.

to get to the real numbers you will have to enter the smoke filled room and have a look behind the mirrors.

LikeLike

$10bn is $2,000 cost for every man, woman and child in the country. Personally, I’d like a refund. Of course, 99% of the population is blissfully unaware that their hard earned taxes were completely wasted in this manner.

I suppose that (like the Covid response) the best that we can realistically hope for is that this policy is never repeated. An apology would also be nice, but I sense that this isn’t likely.

Mr Reddell, you do great work by seeking accountability from the RB et al, for their terrible decisions. As a taxpayer, I appreciate your efforts.

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

The RB has increased the OCR fairly aggressively to try to tackle inflation. It noted at the last increase that this was partly to prevent bond rates from falling, particularly longer term bonds, as the market seemed to think inflation will come down fairly quickly and not persist.

Yields on longer term bonds are still soft (<5%) and the yield curve is inverted.

In terms of perceptions the OCR has an influence on mortgage rates and NZ banks are heavily oriented towards mortgage ending. So a 5% OCR seems about right to me longer term in order to moderate additional money growth from this lending.

Unemployment is still low and you note that high immigration in the short term will just add to demand, which the Govt continues to keep high by spending. Also that settlement balances are still relatively high, indicating that the money is just sitting there (getting OCR) because its a better return than on long term bonds…

So why is RB not more aggressively selling its LSAP holdings to keep bond yields up, and take more money out of the system. It’s currently just trickling sales on a monthly basis and letting some short term bonds just mature.

The LSAP purchases were aggressive and quick. That amplified inflation rather than countered it. So why not sell the holdings just as aggressively? The ~$9b loss on them is a reality. What does it matter if that increases a bit from realising it more quickly, or does RB/Govt hope that if they just let them mature the “losses” will just seem to have never happened?

LikeLike

In their defence I suspect the Bank would argue that (a) they are getting rid of the longest-dated and riskiest bonds first and (b) that the rate of sales now probably wouldn’t make much difference to bond yields (they now argue that even by late in the LSAP purchase programme they weren’t have much influence).

I agree the thing should be wrapped up sooner, including because doing so would clarify the total losses and (marginally) increase the scope for some accountability.

Whether any more tightening is needed is probably best left this morning until after 10:45!

LikeLike

What do you think the chances are that the bond market is being price gamed while the LSAP neutralisation is being undertaken? Why? Obviously to depress capital pricing of those bonds as sales back to private market occurs, at least for ones not maturing.

A second non-related question… How much more decline in movement in ratings’ critical supporting metrics such as levels of debt, tax take etc would be required before ratings agencies put up Govt debt on negative credit watch or actual move?

LikeLike

On your first question, I don’t think it is likely to be much of an issue, esp when the RB is not selling the LSAP bonds back on market but only to Tsy, so that the effect is captured in changes in the overall Crown borrowing programme. You’d have to take a lot of risk for low expected return to make much difference I’d have thought.

I’m a bit sceptical of the ratings watch/downgrade risk. Both main parties seem committed to reasonably restrained fiscal policy from here on in, and the current account deficit, while v large, is also a symptom of the demand excesses of the last couple of years that are probably now exhausting themselves under the weight of a 5%+ OCR. But another year of 8-9% current account deficits would change my take.

LikeLike