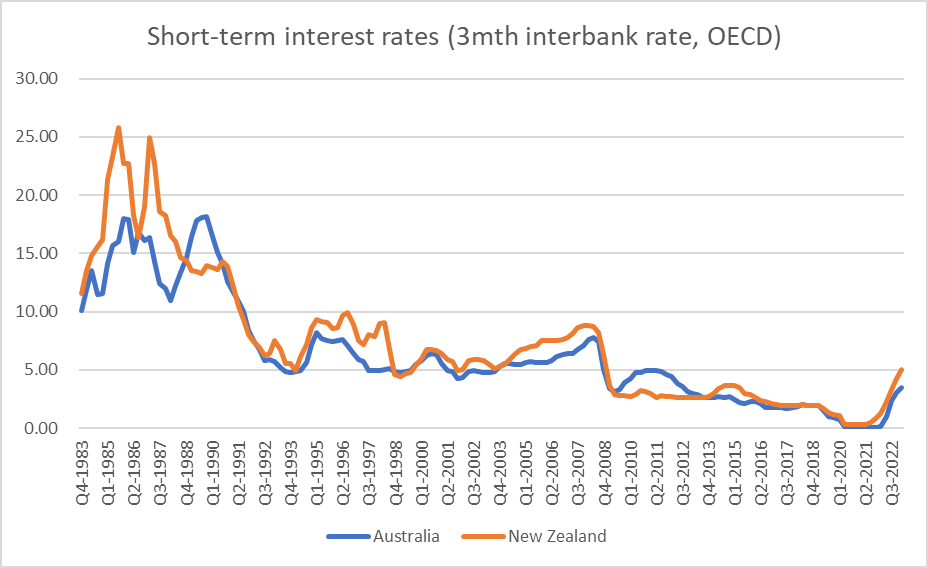

The Reserve Bank of Australia yesterday left its policy rate unchanged at 3.6 per cent. The Reserve Bank of New Zealand’s MPC is generally expected to today raise its OCR by another 25 basis points to 5 per cent.

In the broad sweep of decades it isn’t an unusually large gap. Most of the time, New Zealand short-term nominal interest rates are at least a bit higher than those in Australia (Australia’s inflation target is a little lower than New Zealand so the real interest differential tends to be a bit larger).

Sometimes economic circumstances in the two countries are very different. Thus, that period a decade or so ago when the RBA cash rate was higher than the RBNZ OCR coincided with the later stages of the Australian mining investment boom, for which there was nothing comparable in New Zealand.

But over the last two or three years, the similarities have seemed more evident. Both countries of course went through Covid, with overall quite similar virus/restrictions experiences. Prolonged closed borders affected both countries, notably the important tourism and export education sectors. Both had very expansionary macro policies. In the scheme of thing, both opened up at about the same time. Both have been characterised by labour shortages and very low rates of unemployment. And both have seen inflation sky-rocket, whether on headline or core measures.

There are differences of course. Take commodity prices as an example. If world prices have recently been falling for both countries, relative to levels just a couple of years back Australian incomes are still being supported much more by the high level of commodity prices.

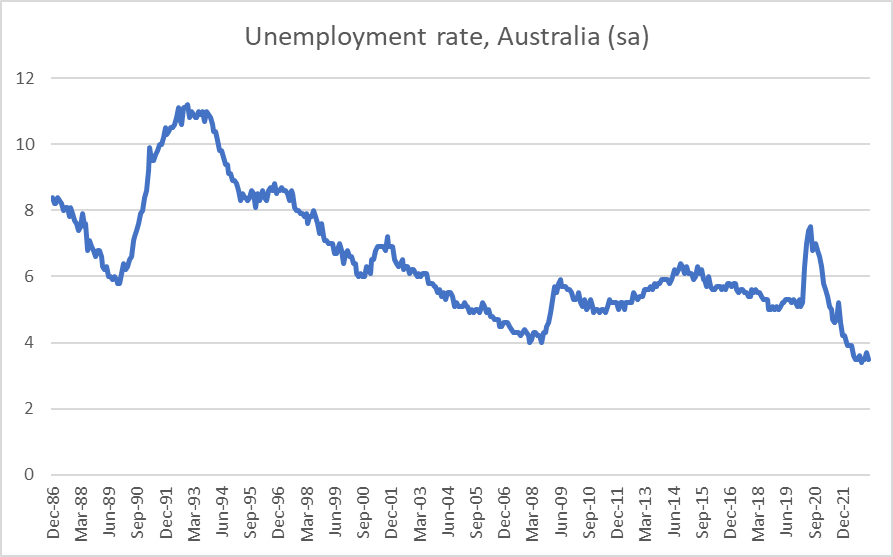

What of the respective unemployment rates? Both are very low, but if anything Australia’s seems lower relative to (a) history and (b) likely NAIRU. Australia’s current unemployment rate is a half percentage point lower than the previous cyclical low, and has not yet shown any sign of lifting.

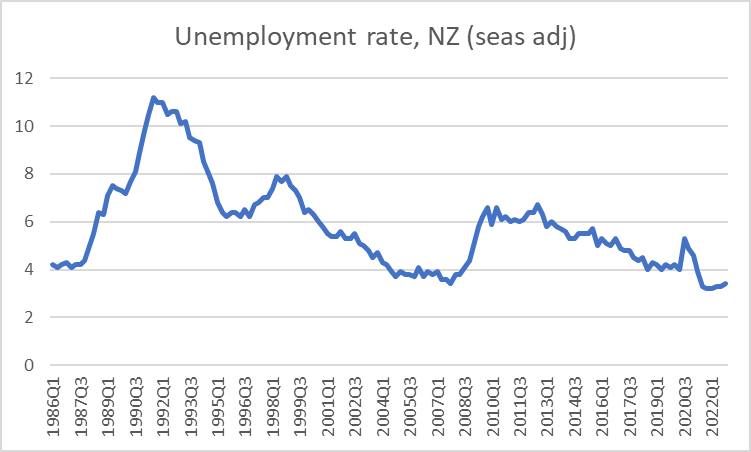

New Zealand’s unemployment rate (quarterly only) seems already to be off its trough and is now about the same as the unsustainably low level reached late in the 00s boom.

One can’t make much of that difference – and the unemployment rate isn’t the only relevant labour market indicator – but the comparison doesn’t obviously point to the RBA needing to do less than the RBNZ. As far as I can see, business survey measures suggest that difficulty of finding labour may have been easing a bit more in New Zealand than is yet apparent in Australia.

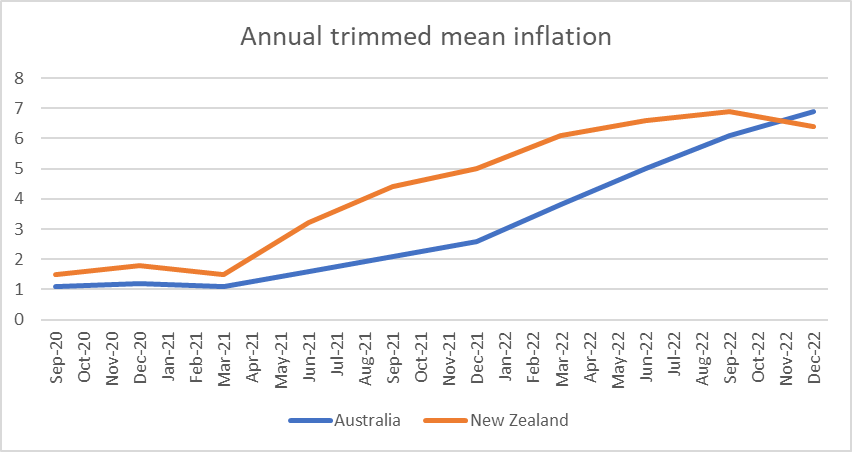

What about (core) inflation measures themselves? Bear in mind that the Australian inflation target is centred on 2.5 per cent and the New Zealand one is centred on 2 per cent.

Here is the annual trimmed mean measure of core CPI inflation for the two countries

And here are the annual weighted median measures

Core inflation started higher in New Zealand than in Australia (the RBA had been badly undershooting the target in the late 10s) but on both annual measures (a) New Zealand annual core inflation appears to have levelled out and (b) Australian core CPI annual inflation now appears to be higher than that in New Zealand. The differences between the two countries core inflation rates in the most recent quarter are more or less in line with the differences in the respective inflation target.

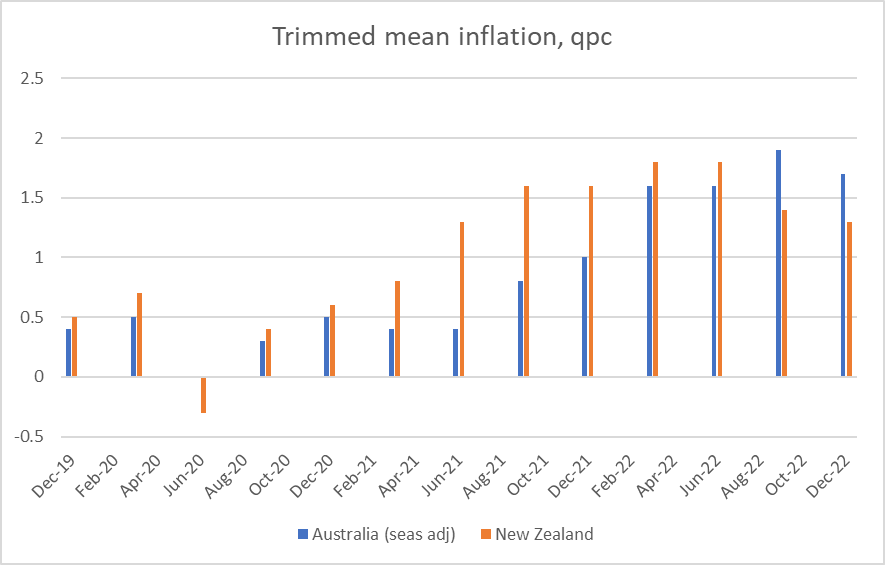

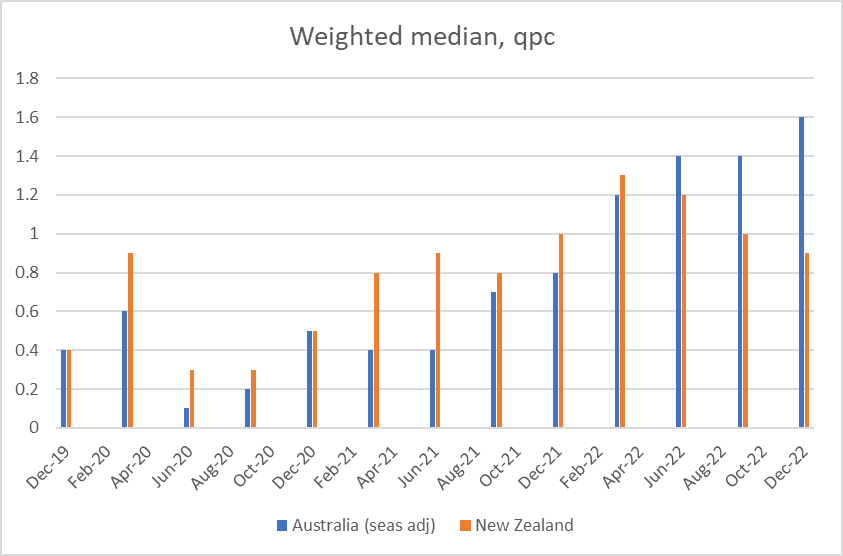

What about the quarterly measures? Here there is some difficulty because the ABS produces seasonally adjusted measures and SNZ does not. Eyeballing the New Zealand series there appears to be some seasonality, although not terribly strong.

Here are the quarterly trimmed mean inflation rates

and here are the weighted medians

The latest observations for the two series for Australia are quite similar (1.6 and 1.7) but there is quite a divergence in the two NZ series (0.9 and 1.3). But in both series there are signs the NZ peak has passed (if you worry about seasonality, even the latest quarterly observations are lower than those a year earlier), while there is no such sign in the Australian quarterly data. And while one can’t meaningfully annualise these data, the differences in the quarterly inflation rates look like more than is really consistent with the differences in the respective inflation data.

I’m not here running a strong view on whether one of these two central banks is right and the other wrong. But it remains a challenge to see how both can be right at present. The two central banks tend to articulate somewhat different models (I’m always surprised at the weight the RBA appears to continue to place on wage inflation, in rhetoric that sometimes seems misplaced from the 1980s), central banks are shaped by their past (the RBA was badly undershooting the inflation target pre-Covid), the political climates are now different (the RBA Governor’s term expires shortly, and governance reforms are in the wind) and there are other material differences in the demand pressures in the two economies that I’ve not touched on here (eg New Zealand has had a bigger housebuilding boom and may be exposed to a deeper bust).

Neither central bank has handled the last three years particularly well – or we wouldn’t have that unacceptably high core inflation – and I am far from being the RBNZ’s biggest fan, but for now my sense is that they are probably closer to right than the RBA is. That may, of course, mean that the near-inevitable recession is nearer at hand here than in Australia.