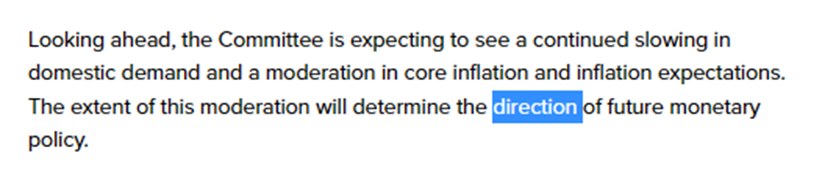

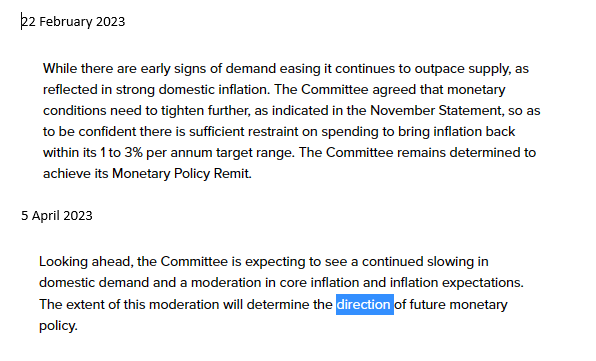

I obviously haven’t seen, or read, the best advice expert commentators have been providing to their wholesale market clients over the last 24 hours but in what I have heard and read I’ve been struck by how little attention seems to have been paid in the more popular/accessible part of the market to this from the MPC’s statement (emphasis added). Looking at some of the changes in market prices, it isn’t clear how much weight markets have put on it.

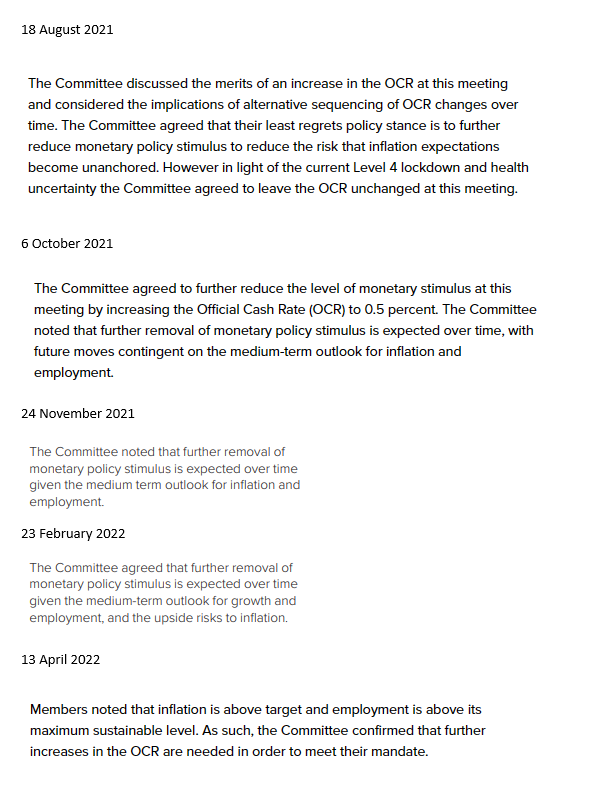

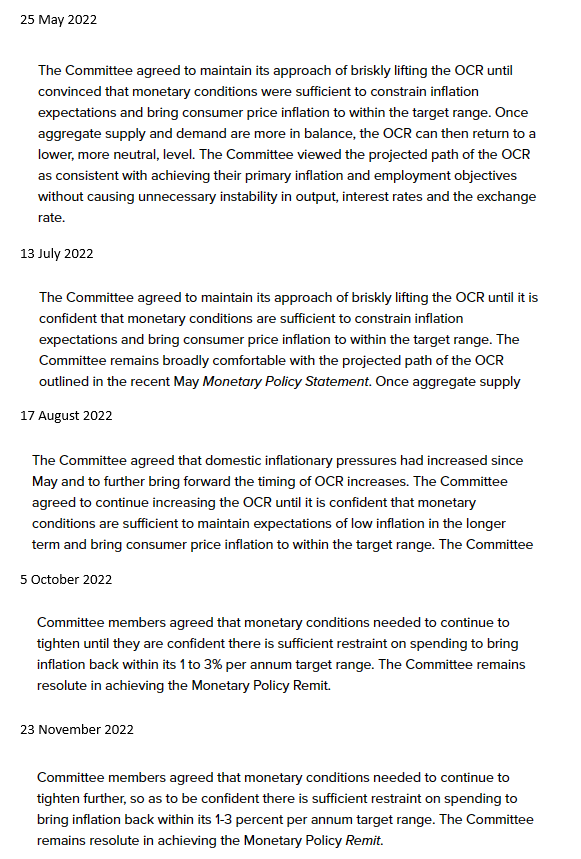

Below, by contrast, are the “bias statements” (comments about what might happen next) from the OCR decisions back to August 2021. Yesterday’s statement – for all the gung-ho 50 basis point move – ends on a very different note. They seem genuinely open minded on whether the next move might be up or down, and whether any such move might be soon or far away. The MPC are no better at forecasting than anyone much else, but since they get to set rates what they think might happen next, and what they do next (whether with hindsight those are the right views or calls) matters. It is a curious change of direction, without a full set of forecasts, and with no real idea what has happened to inflation or unemployment more recently than as at mid-November. But a change of direction it appears to be.

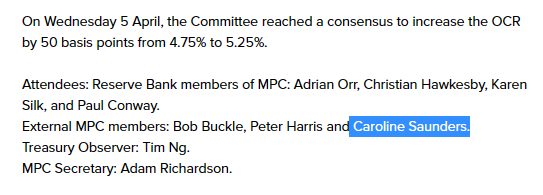

There was a mistake in Monday’s post about the Reserve Bank’s MPC external member Caroline Saunders’ term (and I am grateful to Brad Olsen of Infometrics, on Twitter, for pointing me back in the right direction).

Saunders’ 4 year term, from 1 April 2019, expired last Friday. She is eligible to be appointed for one more term (the law sensibly limits external members to no more than two four-year terms) but she has not, it appears, been reappointed (by contrast, the other two externals were reappointed when their first terms expired this time last year).

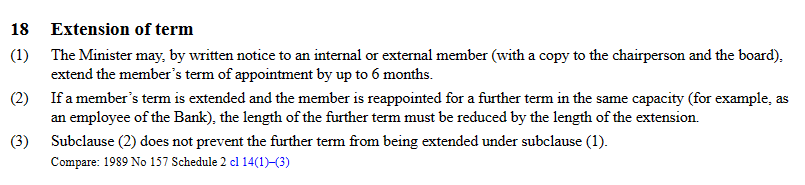

As I noted in Monday’s post, the Minister of Finance has the ability to extend the term of an MPC member (each of the clauses referred to here are from Schedule 3 of the Reserve Bank Act)

Any such extension to a first term sensibly counts against the total time a member can be appointed to a second term for (so extensions can’t be used to lengthen the total time a first term MPC member is appointed for).

Any such extension has to be notified in the Gazetteand given the significance of the MPC you might expect either or both the Reserve Bank and the Minister to put out a press release informing people, including markets, of any such extension.

The extension provisions make a lot of sense in principle, especially when elections roll round quite frequently and the convention is that new permanent appointments should not be made close to, or to commence even after the time of the election. (Interestingly, given that MPC members can only be people nominated by the Bank’s Board, there seems to be no requirement for the Minister to consult the Board – perhaps reasonable since only a maximum of a six month extension seems to be envisaged.)

There is no sign that Saunders’ term has been officially extended either (I checked again just now and there is still no mention of an extension on the Bank’s page detailing all the MPC members and their terms).

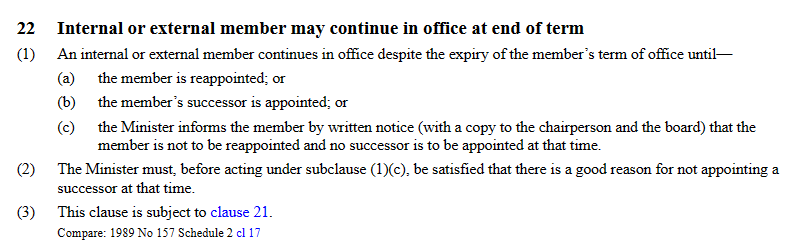

And so I assumed that Saunders would not be able to participate in yesterday’s OCR decision. And that is where I was wrong. She could, and she did. On did

And on could

In other words, having put in the law an explicit provision for formal notified (ie transparent) temporary extensions, deliberately designed not to add to the total term if the member is latter formally reappointed, they also slipped in a clause a bit further down the Schedule that lets the Minister of Finance leave in place any MPC member indefinitely (in the case of internal members only as long as they remain Reserve Bank employees – clause 21), with no formal actions, no consultation with the Board, no transparency, and at best greatly diminished accountability. It seriously undermines the idea of fixed terms or term limits (both of which were sensible innovations adopted by this very same Minister of Finance). It is also corrodes the role of the Board – not something I’m opposed to either in principle or (with current membership) in practice, but it was this Minister who decided to retain the central role of the Board in determining membership of the MPC.

There is simply no need for this provision once a formal temporary extension provision was in place, and its use undermines just a bit more any confidence in the MPC regime.

A fair bit of the way the New Zealand MPC model was designed (strengths and weaknesses) was taken from the Bank of England model. That isn’t too surprising and the Bank of England model is, I think, generally regarded as one of the better models around (the main weakness in it, replicated here, is the in-built majority for Bank of England staff, although the appointment processes in the UK mean that is less troublesome and risky than here). But the Reserve Bank version – law and practice – is a pale shadow of the British model, from designers who liked the form of the Bank of England and the substance of the RBA.

Recall that the Governor, Board chair and Minister here have got together to blackball as potential externals anyone with current or potential future research and analytical excellence in macroeconomics and monetary policy.

Recall too the practice under which the externals neither record their views in the minutes nor – except on the rarest, hardly seen at all, occasion – give speeches or interviews.

By contrast the Bank of England has had many able, informed, energetic, active, and open expert external MPC members, whom we hear from.

In the UK, external MPC members front up at the relevant (Treasury) select committee and are expected to answer questions on their views. As importantly, although the select committee has no veto rights, MPC members are expected to appear before the Treasury select committee for a pre-commencement hearing before their term starts. In at least one case such a hearing resulted in an appointee not taking up their position.

In New Zealand, nothing is heard at all from these not-very-expert – in one case appointed mostly because of her sex – external members at any point ever. We know nothing of their views, nothing of their contribution, little or nothing of their capability for and in the role. And whereas the UK goes through a pretty open selection process, with the Chancellor advised by The Treasury making the final calls, in New Zealand there is little sign Treasury has any substantive involvement (OIA evidence suggested none when reappointments were done last year) and the formal power largely rests with the Reserve Bank Board – a bunch of lightweight non-experts apparently appointed mostly to meet diversity criteria.

But at least, or so it appeared, when their term was up they’d be gone – or formally reappointed with appropriate paper trail. After eight years at worst, we could be sure they were gone (unless, say, promoted to Governor). That is how the UK legislation works.

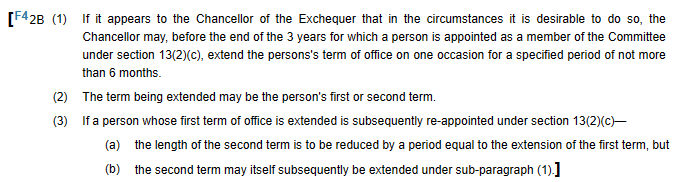

From the relevant schedule of the Bank of England Act 1998

In the UK, members are limited to two three year terms. I don’t have too much problem with New Zealand’s two four-year terms approach – at least if we were going to have actual expert external MPC members – given the smaller pool of potential people here (although three year terms here would minimise election year reappointment issues).

Note also that in the UK legislation – clearly the model for New Zealand – the Chancellor is explicitly restricted to extending a term for a particular individual only once. That seems a prudent restriction – otherwise the Chancellor could extend a person indefinitely (six months at a time, all the while holding a whip hand over the individual to vote the way the Chancellor might prefer). But that restriction has not been carried over to the New Zealand law (see above), and one is left wondering if read strictly the New Zealand law may actually allow repeated six month extensions, I’m no lawyer, but might a court interpreting the New Zealand law look to the UK model and suggest that ministers and Parliament made a conscious choice not to impose such a prudent restraint?

And there is no suggestion anywhere else in the Schedule that any member can just remain in office indefinitely so long as the Chancellor does nothing. As you would expect, because in a well-run system there is no need – officials and ministers get on with making permanent appointments and if for some rare reason, eg election timing, it isn’t appropriate or possible to make an appointment immediately there is a tightly-limited and transparent provision for one time-limited extension.

It isn’t clear what was going on here when the law was drafted. Was it an oversight to have both formal and transparent time-limited extension provisions and a default non-transparent indefinite right to remain provisions. Perhaps, but if it was a deliberate choice, what possible good reason did the Minister and his advisers have?

It also isn’t clear quite what is going on now. There is no obvious reason why a proper appointment – or reappointment of Saunders – could not have been made (they managed it last year). There is no obvious reason why, if some spanner got in the bureaucratic works, Saunders could not have been formally extended for six months (it is entirely in the Minister’s power). And there is no evident reason for letting her simply remain indefinitely, with no notice or transparency (and it seems particularly odd in the current context, drifting ever closer to a tight election where the Minister may lose his ability to appoint a permanent MPC member). There must be an answer – for a position involving on paper a major macro policy decisionmaker at a time when monetary policy is rightly under a lot of scrutiny – but none of the public are favoured with the facts.

(I idly speculated that perhaps there had been some run-in with the Minister’s appointees on the Board. Perhaps they want someone, or some type (race/sex/whatever) of person, and the Minister doesn’t? But even if there was something to that there is still nothing to stop the Minster having given Saunders a formal extension for up to six months.)

Neither the law nor the practice are very satisfactory at all. This MPC member has exercised considerable power (at least on paper) through several years of serious monetary policy mistakes, and not only has there been no public or parliamentary accountability at all, but now we find that the Minister can, by doing nothing, just leave her in place indefinitely, with no transparency, no accountability, and no end date at all. The same option exists for Peter Harris’s second term which expires on 30 September. There should be some clarity from the Minister as to whether – in view of the proximity then of the election – he proposes to extend Harris (the appropriate option in the circumstances) or simply do nothing and let him stay in office.

It is yet another example of how the New Zealand MPC model – law and working practice – needs overhauling, and should be a matter of some focus for any incoming Minister of Finance. Yes, there are always going to be more pressing issues, but getting the governance of monetary policy right isn’t a trivial or unimportant matter either.

(For those wondering about the Governor – and taking some heart from the fact that he is term-limited and, having begun his second term last week, now has less than five years to run in office – his term as Governor can be extended for six months (same provision as for MPC members) BUT I can’t see any provision allowing him to remain in office by default if the then Minister takes no action to appoint a new Governor.)