I obviously haven’t seen, or read, the best advice expert commentators have been providing to their wholesale market clients over the last 24 hours but in what I have heard and read I’ve been struck by how little attention seems to have been paid in the more popular/accessible part of the market to this from the MPC’s statement (emphasis added). Looking at some of the changes in market prices, it isn’t clear how much weight markets have put on it.

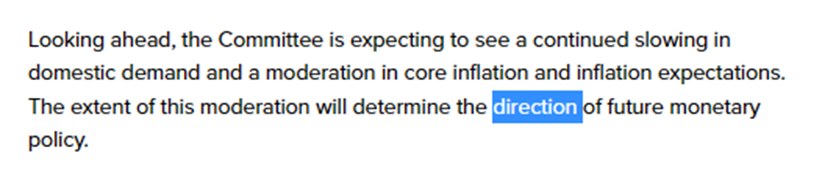

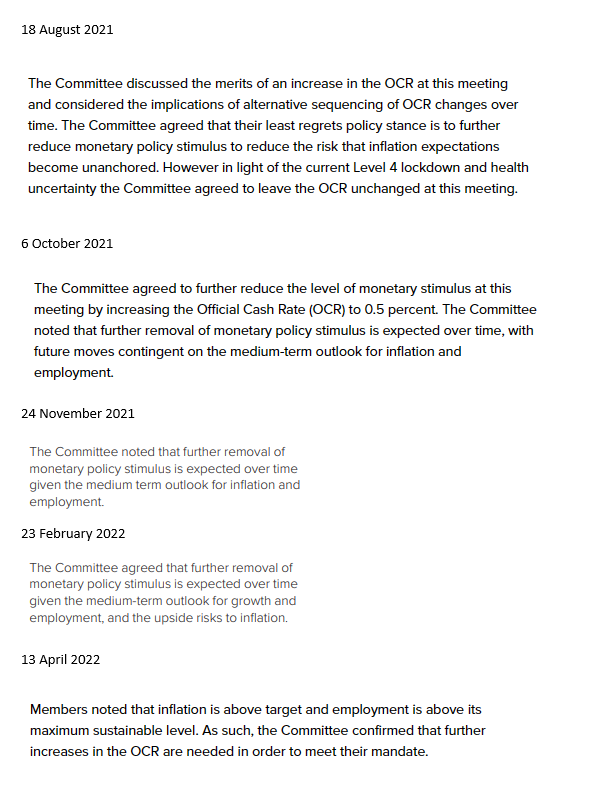

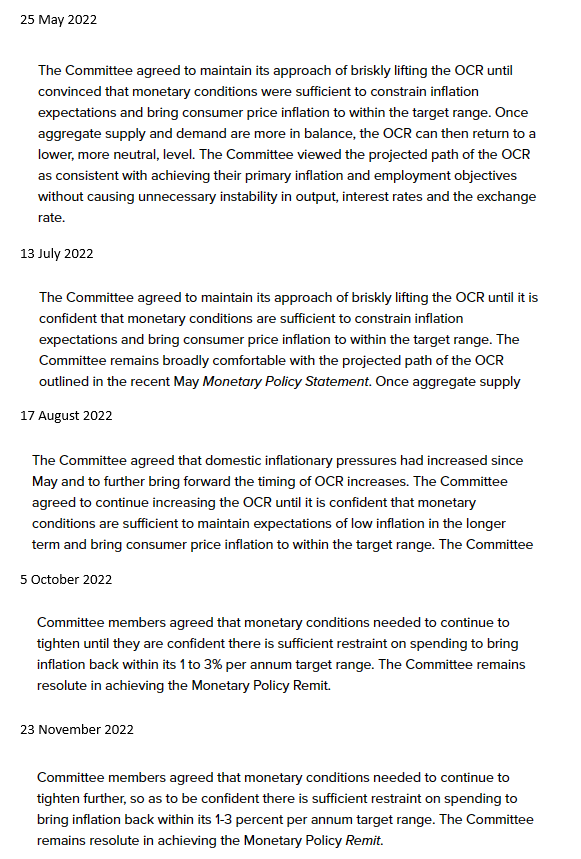

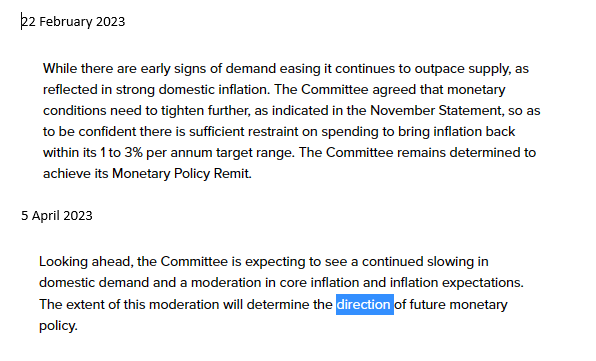

Below, by contrast, are the “bias statements” (comments about what might happen next) from the OCR decisions back to August 2021. Yesterday’s statement – for all the gung-ho 50 basis point move – ends on a very different note. They seem genuinely open minded on whether the next move might be up or down, and whether any such move might be soon or far away. The MPC are no better at forecasting than anyone much else, but since they get to set rates what they think might happen next, and what they do next (whether with hindsight those are the right views or calls) matters. It is a curious change of direction, without a full set of forecasts, and with no real idea what has happened to inflation or unemployment more recently than as at mid-November. But a change of direction it appears to be.

I agree that they are leaving the direction open. I was struck more by the comment that they did not want wholesale or mortgage rates to start declining and moved to prevent that – a short term perspective as they politely try to offset the Government;s spending intiatives…

LikeLike

The RBA in Australia has already hit pause and the major Australian banks are now calling for a drop in interest rates. The trillion dollar QE programme is coming back to bite as Treasury Bond holding values have declined by as much as 40% for long dated Treasury bonds issued at 0.1% in the heyday of the QE. Interest rates any higher than 3.75% and expect a run on the Australian Banks as insolvency looms large in the horizon.

Adrian Orr should expect a call soon from his Australian counterpart to hit a pause or a drop. Don’t forget $59 billion was issued to the Australian banks by NZ Treasury at also the low end of 0.25% and it will also be hurting the Australian banks solvency now that Interest rates here has hit a dramatic high of 5.25%

LikeLike

The question now arise as to which mandate is more important to Adrian Orr. Getting inflation to 25 or Bank stability?

Don’t forget also that higher bank interest rates encourage higher deposit savings which means more cash deposits with the Bnak. Where do you invest? Sharemarkets are being battered. Bond values decline as interest rates rises. Only option? Lend out in a blind panic. Watch lending restrictions drop as Bnaks panic with an overload of savings deposits.

LikeLike

Correction: Getting inflation to 2% or Bank Stability?

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

Interesting.

Could Mr Orr be launching the 50 bps increase as a pre-emptive strike against Kommissar Robbo, in anticipation that the budget spending is likely to be wild and wasteful?

If so, can we really blame Mr Orr for this logic? Kommissar Robbo doubled government spending in nominal terms from $81bn in 2018 to $162bn in 2022. I suspect that in the upcoming budget, Kommissar Robbo will act like the largest man in a pie eating competition, gorging with both hands until he bursts. Being election year, who would bet against this?

The problem with OCR rate rises is that they are becoming increasingly ineffective, because they don’t impact New Zealand’s biggest industry. New Zealand now specializes in the mass production of bureaucrats, on a truly industrial scale. We are world leaders in this. I bet that we have more diversity wallahs per capita than any other country in the world. The central and local government employs over 500k people in NZ.

Alas, an OCR rate rise won’t stop the bureaucrats from sipping their hand-crafted latte’s in Kelburn. All rate rises will do is eliminate the small enclave of private sector businesses that have just managed to hold on through Kommissar Robbo’s increasingly frenzied assaults over the past five years or so.

The economy has already collapsed. Stagflation beckons.

Winter is coming…

LikeLike

My comment is unclear. I was suggesting that by leaving the direction of rates open, the RB might be sending a message to Kommissar Robbo about his forthcoming budget:

Cut spending – OCR rate could be cut.

Spend wildly – OCR rate could be raised.

I could, of course, be wrong about this…

LikeLike

Congratulations to Mr Orr and his team..They are doing their job without fear or favour!

The employment and inflation objectives are both subject to economic lag so we will have to wait and see the future direction.

If this Government has an “election budget” as CF1 suggests I hope the MPC has the courage to continue doing their job.

LikeLike

Kommissar Robbo will announce the next budget on the 18th May.

He will focus on Core Crown spending, to try and deflect attention from the bloated total government spending. He will gorge on new government spending, like an obese man filling his boots at an all-you-can-eat buffet. Kommissar Robbo will try to hide his total spending in appendices and alike. He will use every accounting trick that he can, to move government largesse below the line. He will babble about ‘transitory’ this and ‘one-off’ that.

The Reserve Bank has an OCR meeting on the 24th May 2023. I suspect that they will see through Kommissar Robbo’s accounting tricks.

I predict that Mr Orr will respond by increasing the OCR by 50 bps.

The economy will already be in a technical recession. Consequently, the market will be apoplectic with the RB decision. To be fair, Mr Orr has warned the government about controlling spending. Kommissar Robbo has no-one to blame but himself.

You heard it here first:

50 bps in May.

LikeLike