I was on Newstalk ZB this morning to talk about the ASB recession forecasts and this article on the Herald reporting some recent statistical analysis from Treasury staff that attempted to provide another perspective on what has caused New Zealand’s high inflation rate.

I don’t want to add anything on the ASB forecasts other than to say that (a) their story and numbers seem quite plausible, but (b) macroeconomic forecasting is a mug’s game with huge margins of uncertainty and error, so not much weight should be put on anyone’s specific forecast ever (with the possible exception of a central bank’s forecast, which may be no more accurate than anyone else’s but on which they may nonetheless act, with consequences for the rest of us).

The Treasury staff analysis was published a couple of weeks ago as a 2.5 pages Special Topic in their latest Fortnightly Economic Update. You can tell from the Herald headline why one of their political journalists might have latched onto this really rather geeky piece

But there is less to the analysis than the headline suggests. The term “government spending” doesn’t appear in the Treasury note at all (I think “fiscal policy” gets one mention). The focus of the paper is an attempt to better understand the relative contributions of demand and supply factors to explaining inflation, and while fiscal policy is one (at times significant) source of demand shocks and pressures, there is no effort in the paper to distinguish the relative roles of fiscal and monetary policy (or indeed, to distinguish either of those policy influences from other sources of demand pressures). That isn’t a criticism of the paper. The technique staff used, introduced for those purposes a few months ago by a Fed researcher (his paper is here), isn’t designed for that purpose.

Loosely speaking, the technique uses time series modelling techniques to look at both prices and volumes for (most of) the items included in the CPI. When there are surprises with the same sign for both a price and the corresponding volume that is (in their words) suggestive of a demand shock (increased demand tends to lift prices and volumes) and when the surprises have opposite signs this is taken as suggesting a supply shocks (disruptions in supply tend to see lower volumes and higher prices go together). It is a neat argument in principle.

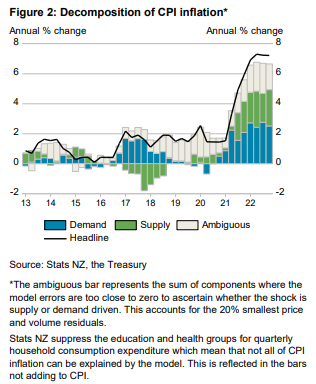

But it doesn’t look to be a very good model in practice. Here is The Treasury’s summary chart. the source of the line that (on this analysis) demand and supply shocks may have contributed roughly equal amounts to inflation over the last year, and that demand shocks were more important back in the early stages of the surge).

Not only is a large chunk of recent inflation not able to be ascribed to either demand or supply shocks, but there have been periods even in the quite short span shown here when the identified demand and supply shocks don’t explain any of the then-current inflation at all (eg 2019).

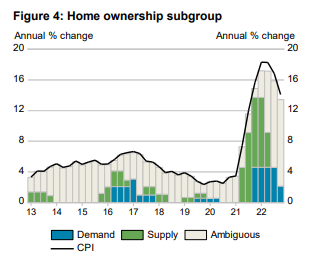

This is even more evident with some of the sub-groups they show results for. Thus, home ownership (which in the CPI is mostly construction costs)

For most of the decade, neither (identified) demand or supply shocks explain the inflation, and that is so again in the most recent data. And if the model suggests that sharp rises in construction cost inflation in recent times have little to do with demand at a time when house-building has been running at the highest share of GDP in decades, so much the worse for the model.

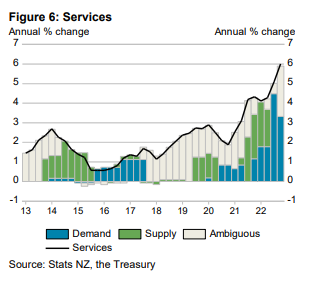

Services make up a large chunk of the economy, and a fair chunk of the CPI too. Here is the chart for that group

Not only are there periods when neither demand or supply shocks (as identified by the model) explain any of services inflation, but how much common-sense intuition is there is the idea (which the chart suggests) that for most of the period what services inflation can be explained is all either supply shocks or demand shocks and not some combination.

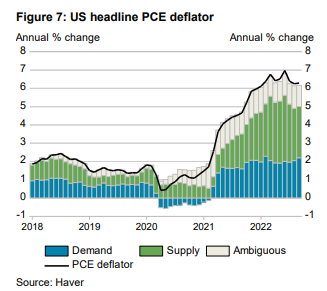

The Treasury paper notes some overseas comparisons, in particular that for the US

The results for New Zealand show lower supply-side contributions to inflation than estimates for the US and Australia. In the US, supply-side drivers account for about 60% of the annual change of the PCE deflator that the model can explain (Figure 7).4

(the footnote is to the original Fed paper)

and they show this US chart which I assume comes from the same model

Note, first, that the PCE deflator has a materially different treatment of home ownership – using imputed rents – than either the NZ or US CPIs.

But perhaps more importantly, in the original Fed paper there is this line

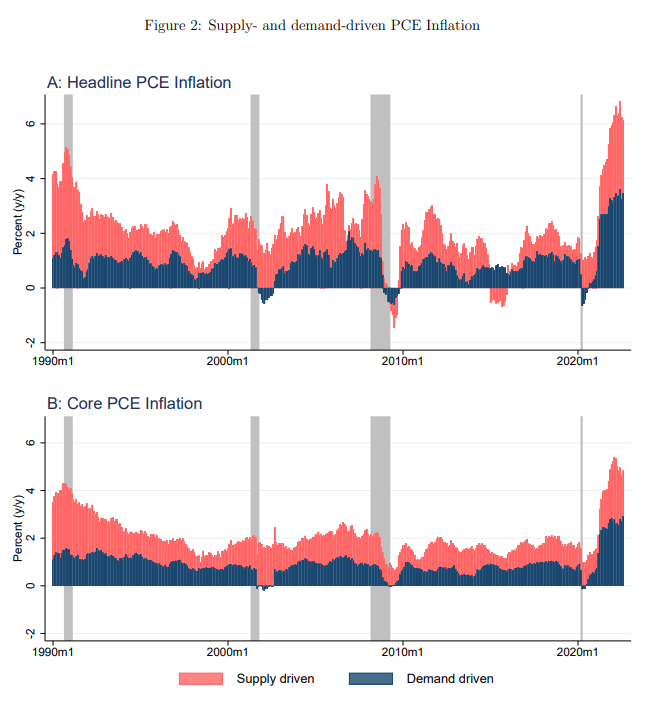

And here is a relevant chart from the same paper (grey-ed periods are NBER recessions)

Not only does it show the entire period since 1990 (one of my uneases about the New Zealand work by Treasury is showing only the last 10 years), but it also illustrates that, as defined for the purposes of these models, both supply and demand factors are large influences, almost always positive, over the entire 30+ years. In other words, if there is anything unusual about the current situation it is not the relative contributions of supply and demand influences but simply that inflation is high (both demand and supply influence). It simply doesn’t seem to add much value in making sense of why things unfolded as they did over the last couple of years. (Although it is interesting how different the last 10 years of the chart look for the US, as opposed to New Zealand in the first chart above.)

What these US charts also illustrate is that supply and demand shocks/drivers here don’t mean the same as they typically do when thinking about monetary policy. Monetary policymakers will (rightly) talk in terms of generally wanting to “look through” supply shocks – the classic example being spikes in world oil prices, which not only flow through to the CPI almost instantly (faster than monetary policy could react) but also make us poorer. The focus instead is on whether these headline effects flow through into generalised inflation expectations and price-setting more broadly. Climate-induced temporary food price shocks (from storms or droughts) are seen in the same vein.

Those sorts of shocks are generally thought of as being as likely to be negative influences on headline inflation as positive ones. Oil prices go all over the place, up and down. Much the same goes for fruit and vegetable prices. These are the two main things excluded in that simplest of core inflation measures, ex food and energy. Some of the Covid-related disruptions are probably more one-sided: there aren’t really obvious favourable counterpoints to severe supply disruptions (even if such disruptions themselves generally unwind over time). But even taken altogether they aren’t the sorts of things that will produce positive influence on core inflation over single year for over 30 years (as in the US core inflation chart immediately above).

When macroeconomists think of inflation they often do so with a mental model in their heads in which this period’s inflation is a function of inflation expectations, some influence from the output/employment gap, and then any residual (supply shock) types of items. Those supply shocks can run in one direction for a couple of years in succession (and probably did in the last couple) but the expected value over long periods of time is generally thought to be pretty close to zero. Monetary policy determines core inflation – monetary policy shapes expectations and influences and responds to developments in the output (or employment) gap. Of course, monetary policy takes account of trend supply developments – adverse shocks may not only raise headline inflation, and risk raising inflation expectations, but can lower both actual and potential output (many positive supply shocks work in the opposite manner).

I don’t want to be particularly critical of The Treasury. We should welcome the fact that their analysts are trying out interesting different approaches and keeping an eye on emerging literature, and even that they are making available some of that work in generally low-profile publications. That said, Treasury is not some political babe in the woods, and I’d have thought there should have been some onus on them to have provided a bit more context and interpretation in their write-up. For example, whereas the US is often treated as a closed economy, New Zealand clearly isn’t. I don’t have a good sense as to how general imported inflation – or that reflecting exchange rate changes – is going to affect this sort of decomposition. If, as I believe, a wide range of central banks made very similar policy mistakes, we’ll be seeing more inflation from abroad (if our Reserve Bank takes no steps to counter it) not tied to demand pressures in particular domestic sectors. I’m also not really clear how the lift in inflation expectations that we observe in multiple surveys fits into this sort of decomposition exercise.

Oh, and it was perhaps convenient that of the CPI groups Treasury showed, motor fuels was not one of them. Headline inflation currently is held down quite a bit by the NZ Cabinet shock – holding down petrol excise taxes etc.

My own approach to the question of where the responsibility lies for core inflation (and note that Treasury focuses on headline not core) tends to be simpler. When this century the unemployment rate has dropped below about 4 per cent core inflation has tended to become quite a serious problem (mid-late 00s and now). The Reserve Bank itself has been quite clear in its view that employment is running above the “maximum sustainable employment” (itself determined by other government policies), and thus, by implication, the unemployment rate – at near-record lows is below sustainable levels. That is a function of excess demand relative to the ability of the economy to supply. Core inflation – the bits we should most worry about, because we could usefully do something about them – is an excess demand story, risking spilling over into embedded higher inflation expectations.

And when ZB’s interviewer asked me this morning whether Mr Robertson or Mr Orr was to blame (fiscal or monetary policy), I was quite clear that the answer was monetary policy (Orr and the MPC). That isn’t because monetary policy loosenings in 2020 were necessarily the biggest source of stimulus to demand, but because the model is one in which (a) fiscal policy is transparent, and (b) monetary policy moves last, with the responsibility to keep core inflation at/near target. You might think (I certainly do) that less should have been done with fiscal policy, but it isn’t up to the MPC to take a view on that, it is their job simply to have a good understanding of how the whole economy, and the inflation process in particular, works, and to adjust monetary policy accordingly. In extremis, fiscal policy can overwhelm the best efforts of central banks, but that wasn’t an issue or a risk here, or most other countries, in recent years. Central banks simply got things wrong. (They had company in their mistake, but they were/are paid to get these things right.)

Dear Mr.Reddell

I am grateful to receive your assessments which I find very accurate with my minute understanding of economics however, we have also seen many billions of dollars poured into the system via projects such as the Covid payouts and Maori and other causes some which we know about and many which we dont know about but money is like drowning sorrows,they tend to float and show up in diluting values. In the innermost chambers of the Reserve Bank’s intelligencia and others in high position know that the trumpet call for change has already been sounded via the IMF’s new Unicoin.., and hence CDBC’s which will throw the markets into complete disarray of not understanding what’s is happening just as it happened in Europe when the respective currencies changed to the Euro…I happened to be living there at the time and we were baffled when paying the price for a BigMac…or how much our new money in the bank was really worth….what are your thoughts regarding Unicoin and CDBC’s, no doubt our Reserve Bank is already testing their computer systems.

Best wishes, Serge

Sergio M. Kemelmager Silverstream – Upper Hutt City 5019 Wellington – New Zealand 021 979-876

>

LikeLike

I’m much less bothered by CBDCs than many people, but also don’t expect there will be much interest in using them. Many of the abuses people worry about – possibly correctly – are already open to govts with existing bank accounts (in the extreme case, see China). Anyway, here was my submission to the RBNZ

Click to access central-bank-digital-currency-submission-4-december-2021.pdf

LikeLike

Yes, I’m not too concerned about CBDCs. I see advantages in transaction efficiencies, reducing some risks and better allocation of investment funding, but the current system works. Any private money equivalents (NFTs, crypto tokens) that become significant will get tied to national (real) currencies just like the banks have. I also submitted on the simplest way to implement real money for transactions for everyone….

LikeLike

From the Herald article:

‘The current forecast is for government spending as a share of the economy to reduce to about 30 per cent – the long-run average.’

I can’t find where these figures come from. All I can find is this out-of-date article:

https://www.interest.co.nz/public-policy/115868/budget-202223-summary-all-spending-plans

Government spending 2018 = $81 bn, 27.6% of GDP

Government spending 2022 = $162 bn, 44.7 % of GDP

45% of GDP is not even close to 30% of GDP.

Are these figures incorrect?

LikeLike

I think someone has slipped fron one definition (core Crown) to another (total Crown). in the Dec 22 fiscal update, core Crown spending was 27.3% in the Jue 2108 year,32.8% this year, dropping back to 30.9% by 2027. Total Crown expenses are about 7-9 percentage points higher, peaking at 42% in the June 2022 year. Most analysts focus on the core Crown numbers.

LikeLike

Why would anyone look at the Core Crown expenditure figure, rather than total government spending number, when considering the size of government? That is completely absurd.

Kommissar Robbo has pulled a magic trick, and got away with it. He has managed to get people to ignore one-third of his spending.

Saying government spending is 30% of GDP in 2022, when it was apparently 45% of GDP, is a material difference.

This is banana republic stuff.

LikeLike

core Crown has been the focus of all analysts and parties for decades. Total Crown includes a whole bunch of SOEs and Crown entities with their own revenue streams (thus total Crown revenue is also much higher than core Crown). core Crown captures what one is looking for in fiscal policy.

LikeLike

Your assessment seems pretty right to me Michael. Running deficits (fiscal policy) during a lockdown to put money in peoples hands they couldn’t spend was always potentially inflationary. The RB should have implemented a deflationary stance to counter that, but was expansionary instead, and seriously magnified the problem. OCR should have been raised then and the LSAP was a giant mistake. Fine to say no-one thought inflation likely at that time, but we pay the RB to know better than the rest of us! Keeping mortgage rates down when people had excess savings just encouraged purchases of existing housing stock and drove up house prices alongside the supply shortages (including labour). Govt probably had to act to offset lockdown created problems for people, but the RB should have seen that coming – they knew about the Govt $50b covid spending blowout before they jumped in with LSAP.

LikeLike

One thing I hadn’t really noticed for a while is that even by Sept 2020 (data out in Dec 2020) real GDP had already recovered to pre-Covid levels. That should have told the RB – and the rest of us – that much less stimulus was already needed than the Bank was continuing to envisage.

LikeLike

Thanks for your reply.

‘core Crown has been the focus of all analysts and parties for decades. Total Crown includes a whole bunch of SOEs and Crown entities with their own revenue streams (thus total Crown revenue is also much higher than core Crown). core Crown captures what one is looking for in fiscal policy.’

Perhaps all the analysts are wrong to do this? I worked for investment banks for quite awhile. In 2008, it transpired that virtually everyone had been wrong for decades about the risk banks were taking. Most people were wrong about the zero Covid fiasco. I prefer to analyse things independently, rather than follow a crowd.

I always wondered why the total government spending went up in nominal terms from $81 bn in 2018, to $162bn in 2022, and no analyst thought that this was an issue. Now I know.

Personally, I think that if you are going to exclude one-third of government spending from analysis or consideration, it would be wise to at least quantify exactly what you are excluding.

When I look at the $162bn total government spending in 2022, the big four are:

Treasury and Finance 17

Education 20

Health 28

Social Welfare 40

https://www.interest.co.nz/public-policy/115868/budget-202223-summary-all-spending-plans

I don’t see these as crown entities that shouldn’t be counted. The rest of the $162bn is spending by other government departments. Maybe they shouldn’t be included either?

If total government spending in 2022 was $162 bn, and Core Crown spending was $50 billion or so less than this, I’d like to see exactly what makes up this difference.

Perhaps I am too cynical? So be it…

LikeLike

$81 to $162 is apples and oranges. Total crown is the first year was $103bn. Still a huge increase of course, but not a doubling.

Of course, anyone is welcome to use any analytical approach they prefer, but I’d suggest you use the fiscal update detailed tables etc rather than an interest.co table.

LikeLike

Okay, thanks for that. The tables are interesting.

https://www.budget.govt.nz/budget/2022/data-library.htm#forecasts

For example, in 2020, ‘Crown Core Crown Expenses’ were $109bn, and ‘Total Crown Expenses’ were $139bn.

Unfortunately, I couldn’t find the table which gives the breakdown of the $30bn difference…

If you know where to find this, I’d be interested, just to satisfy my curiosity.

LikeLike

If the whole $30 billion amount is inter-entity consolidation, then it makes sense. I suppose I was just suspicious because it was named Core Crown spending, so I wondered what non core would represent…

Sorry to go take your blog off track!

LikeLike

Thanks Michael, useful as always. Are households handling cash flow pressure better than you expected? Granted, a vast topic but, for example, seems bank system asset quality is holding up. Perhaps trouble ahead but maybe (nominal) incomes have been compounding enough over the past 5 years such that the higher inflation and interest rates/debt service are being digested. Some sectors might do it tough but at the aggregate, seems like it could be steady….especially with net migration, rebuild etc. Any musings or what you are keeping an eye on welcome?! Thanks

LikeLike

I guess banking system asset quality shouldn’t be a surprise to this point, since unemployment has barely risen (the threat to mortgage books, with fallen house prices) and the shakeout in the construction sector itself is probably still in relatively early stages. Employment covers a lot: if your household is under real mortgage servicing stress one or both of you can prob get extra hours or a secondary job (and prob are getting wage increases in the primary job), but when the labour mkt turns sharply and one partner loses a job things really start to hit home.

And, as you say, the new surge of immigration is (all else equal) supporting demand/activity and undermining the anti-inflation drive.

LikeLike

Well, I’ll have one last go, since I finally understand the figures.

Mr Orr is most to blame for the inflation. It’s his job to keep inflation at about 2%. He failed dismally to do his job. However, it’s a bit too convenient to blame the high inflation completely on Mr Orr.

Honourable mention in the failure stakes must go to the entire Covid response, and therefore to the cult of Cindy Ardern. New Zealand had the harshest lockdowns in the world. Fiscal policy has been out of control since Labour was elected to govern alone. The borders were closed for years. Minimum wage levels have been ramped up unsustainably. Other wage levels have been subject to government collective centralized wage setting. There are many other government policies that have been inflationary, making Mr Orr’s job much more difficult.

We have seen economic vandalism on a grand scale these past few years. Every political party collaborated with this sad state of affairs, at least for a period of time. The citizens signed up to most of it, giving Cindy Ardern an unprecedented majority.

It has been a perfect storm, where the worst RB Governor in NZ history was in charge at the same time as NZ had the worst government that we’ve ever experienced.

Mr Orr deserves a lot of the blame, but not all of it.

LikeLike

Not to enter into a long debate, but if you are saying that fiscal policy was too loose and that added materially to inflation pressures then I agree entirely. But whatever fiscal policy was, it is Orr’s job – the one he agreed to take – to keep inflation in check anyway, adjusting monetary policy as required to offset the demand effects of fiscal policy.

LikeLike

Technically, you are completely correct in all you say.

However, this version of history strikes me as slightly revisionist, on practical terms.

I remember well the mass hysteria during the Covid hoax. The Zero Covid cult was completely fanatical and merciless. The government, aided by the lickspittle Fourth Estate, implemented a completely totalitarian machinery, which was virtually impossible to stand against. This lasted for over two years.

I agree that in theory at least, Mr Orr could and indeed should have stood against all the Covid hoopla, including the fiscal wastage. The LSAP is a notable low-point in RB performance at the time.

However, I’d say that is a pretty high bar to set Mr Orr, given the context. Outside of China, New Zealand represented the highpoint in Covid cult extremism. Virtually everyone complied with what the government demanded from them.

I’m not really disagreeing with your point of substance. I just think that was some extenuating context around Mr Orr’s generally terrible decision-making.

LikeLike

I wouldn’t use your rhetoric but of course agree that the policy response by govt, and notably the fiscal policy one, was overblown. That is on Ardern and Robertson (cheered on by Orr). But…..we have independent central banks supposedly to protect us against the inflation consequences of govt excesses, and both the RBNZ and many of their peers abroad failed to do that, so hard questions need to be asked there. I don’t think it was a moral failure – failure of will – but a huge forecasting mistake, which many private sector forecasters made too.

Of course, Robertson’s responsbility then goes wider again – not only did he appoint a weak MPC, but he reappointed Orr, effectively taking some ownership himself of the Bank’s bad choices.

LikeLike

I assume that being politics it is about another issue which the government don’t want to address?

https://journals.sagepub.com/doi/pdf/10.1177/0308518X19873673

LikeLike

I could probably toss this into the mix anywhere but Arnold Kling’s comments are interesting.

https://www.econlib.org/library/columns/y2023/klingfinancialpolicy.html

He seems to be saying Central Bank independence is a chimera (as we have certainly seen in NZ) since Governments need to keep debt/credit markets alive to feed their endless desire to spend money they don’t have (yet).

Keeping the “square of power” apparatus functioning may well be an underappreciated reason for creating crises so they they can fix them for us….. We may well face the sad prospect of Orrs for ever… 🙂

LikeLike