Over the last few days I’ve been reading a few pieces on UK monetary policy and high inflation. The first was a speech from the Deputy Governor responsible for economics and monetary policy, Ben Broadbent (over there senior central bankers actually give serious and thoughtful speeches on things the Bank has responsibility for), and the second was a new paper by long-term adviser, analyst and researcher Tim Congdon. There is a lot of overlap because Congdon’s paper is broader (“Why has inflation come back”) but his analytical approach has tended to emphasise the monetary aggregates, while Broadbent’s speech which is narrower in focus is specifically on the question of what information value for monetary policymakers there is (or isn’t) in the monetary aggregates over the longer term and in the specific context of the inflation of the last couple of years. Both are worth reading.

My own view on the monetary (and credit) aggregates is, I think, pretty much the same as that of most central bankers these days, that the indicator value of these aggregates is typically fairly limited in the world we inhabit (low or – at present – moderate inflation), that any really serious breakout of inflation (think, eg, Argentina) is likely to be accompanied, in some sense or other, by rapid growth in the quantities of money, and that for now while one should never ignore any indicator there isn’t much about inflation developments of the last couple of years that is best explained through the lens of monetary aggregates. Specifically, if bond-buying programmes like the LSAP did anything much to boost inflation, it was not primarily (or at all) through a monetary quantities channel.

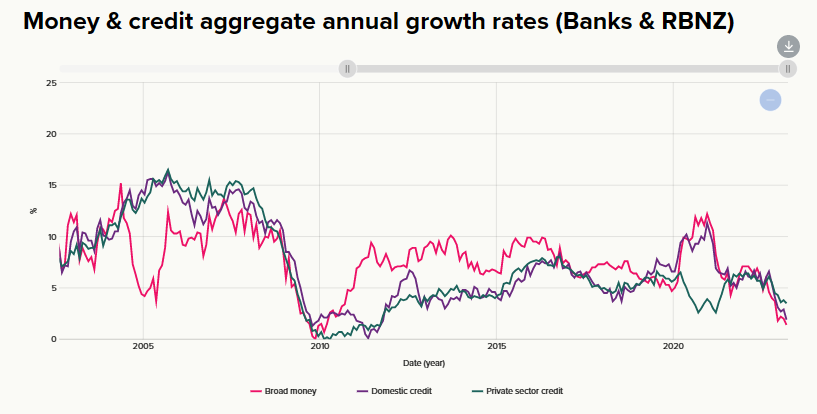

Here is some New Zealand data (and an RB chart) on the growth rates of the monetary and credit aggregates over the period since September 2002 when the current inflation target was adopted.

At the Reserve Bank we always used to put more weight on credit developments than on money measures, and credit growth dipped quite materially in the early months of the pandemic, but no model using either monetary or credit aggregates is isolation would have given policymakers (or other forecasters) reason for serious concern about an outbreak of core inflation to rates unprecedented for decades, Indeed – and since we don’t run a price levels targeting system, and thus bygones are treated as bygones – an analyst looking solely or mainly at these indicators would have noticed by mid 2021 that all the annual growth rates were back to around 5 per cent. No one was going to be sounding inflation alarms if their analysis was based largely on those growth rates. Even in the short period when annual money growth exceeded 10 per cent, the growth rates were not very much higher than had been seen not infrequently over 2011-2016 when core inflation was materially undershooting the target.

Each country’s data and experiences are a bit different but as a general proposition I’d be surprised if many central bankers have become any more positive on the short-term indicator value of the monetary aggregates in the last couple of years.

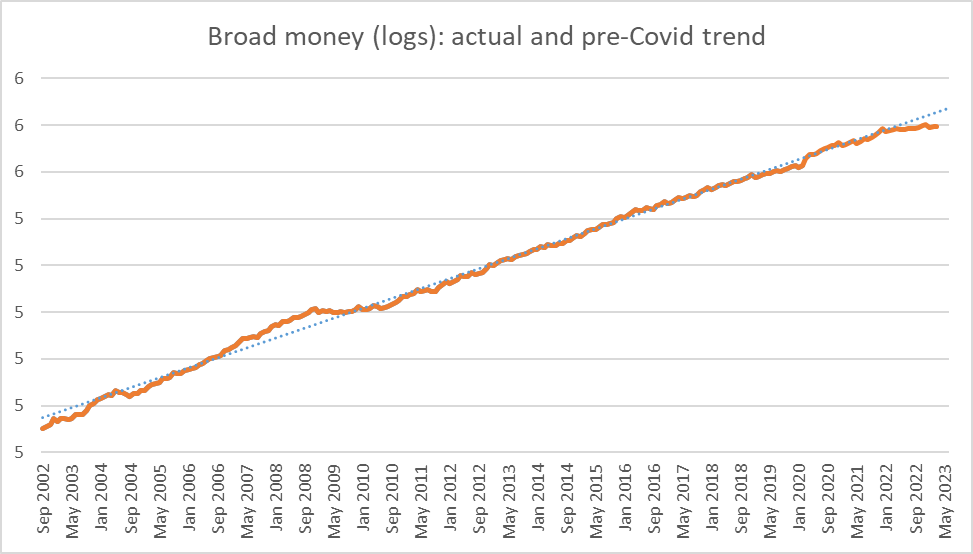

As one final money aggregate chart, here is the level of the New Zealand broad money series relative to the trend over the pre-Covid period since the 2 per cent inflation target was set. Over that almost 18 year period, core inflation averaged 2.2 per cent. At present, broad money is sitting below the trend, and although views currently differ on how much disinflationary pressure is now in the system I’m not aware of anyone who thinks we are about to have a 8-10 per cent drop in the price level, to get back to price levels consistent with long-term average inflation of around 2 per cent.

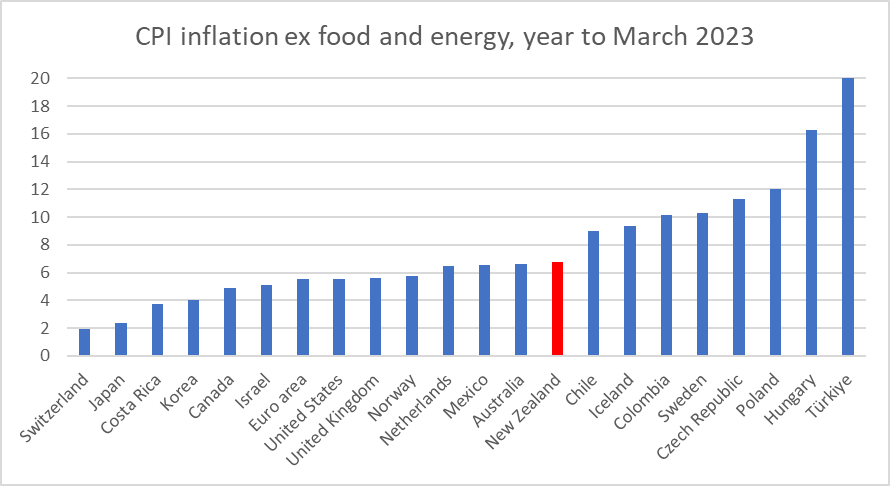

The UK has become a bit of a poster boy for bad inflation outcomes. Some of the headline numbers have been very bad (up around 10 per cent), but some of that is what happens when a gas price shock hits you (and no monetary policy framework tells a central bank it should try to offset the direct price effects of such a shock). But if we use a common measure of core inflation (CPI ex food and energy), the UK is far from the worst of the advanced economies and has a bit less-bad core inflation outcomes at present than New Zealand (or Australia).

If their central bank hasn’t done a great job, ours has done a bit worse. And the diverse outcomes in this chart remind us – as Congdon explicitly does in his paper – that inflation outcomes are ultimately national in nature, choices by central banks and (by default usually) their political masters. That we have similar core inflation to several countries on the chart – but quite different outcomes to sound and responsible countries towards either ends (Switzerland, Korea, Sweden, Czech Republic eg) – speaks more to similar mistakes made by respective central banks than to anything that was out of the control of the Bank of England or the Reserve Bank of New Zealand.

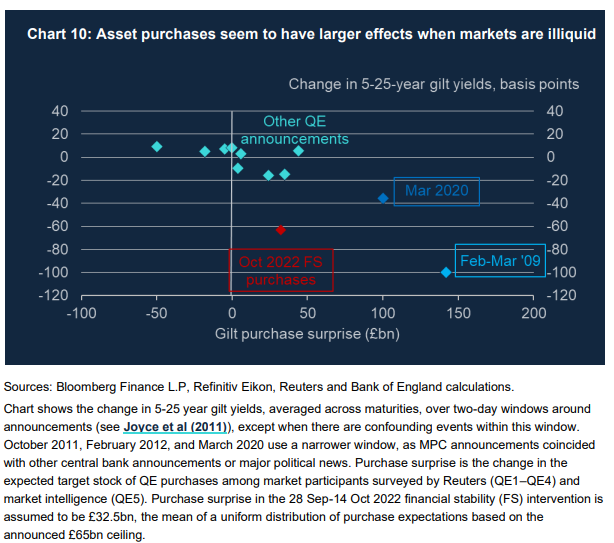

Two charts in Broadbent’s speech caught my eye. The second (which I’ll come to in a minute) was directly relevant to the inflation mistake. But this was the first on the interest rate effects of central bank bond purchase programmes. The Bank of England, like the RBNZ, believes that QE has macroeconomic effects primarily through interest rate effects (rather than the quantities of fully-remunerated settlement cash balances that are created in the process).

Broadbent reckons that bond purchase programmes have a material announcement effect (what is measured here) when markets are very illiquid. That is no surprise, and probably everyone would agree. But what caught my eye was those “Other QE announcements”. The average of the interest rate effects of those nine announcements is close to (and not significantly different from) zero. Perhaps this particular estimation is wrong, but wouldn’t it be nice if our central bank was producing such charts, and the research supporting them, rather than just handwaving estimates of large number effects, that often conflate March 2020 (and the effects of what the Fed was doing at the same time) with the rest of their highly risky and costly programme?

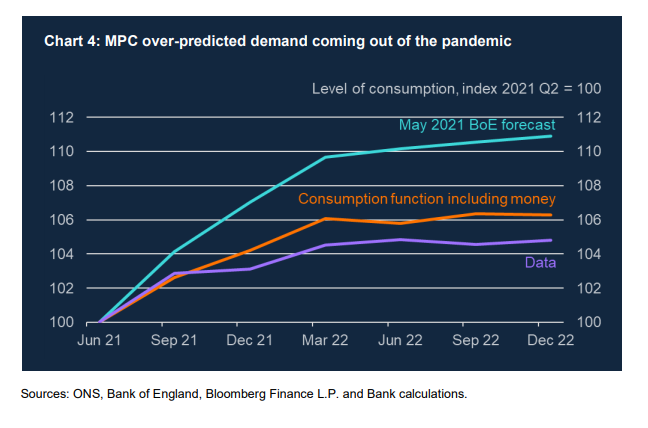

The other Broadbent chart that caught my eye was this one

Broadbent is using it primarily to make the point that the BOE actually forecast growth in real private consumption stronger than would have been implied by a model incorporating data from the monetary aggregates. But what interested – surprised – me was that they had ended up materially over-forecasting real consumption growth (from the point where the UK’s last lockdown ended). Normally, over-forecasting a key component of domestic demand would probably have been associated with over-forecasting inflation. But not this time (and the biggest error was before, not after, the severe adverse terms of trade shock associated with the Ukraine war)

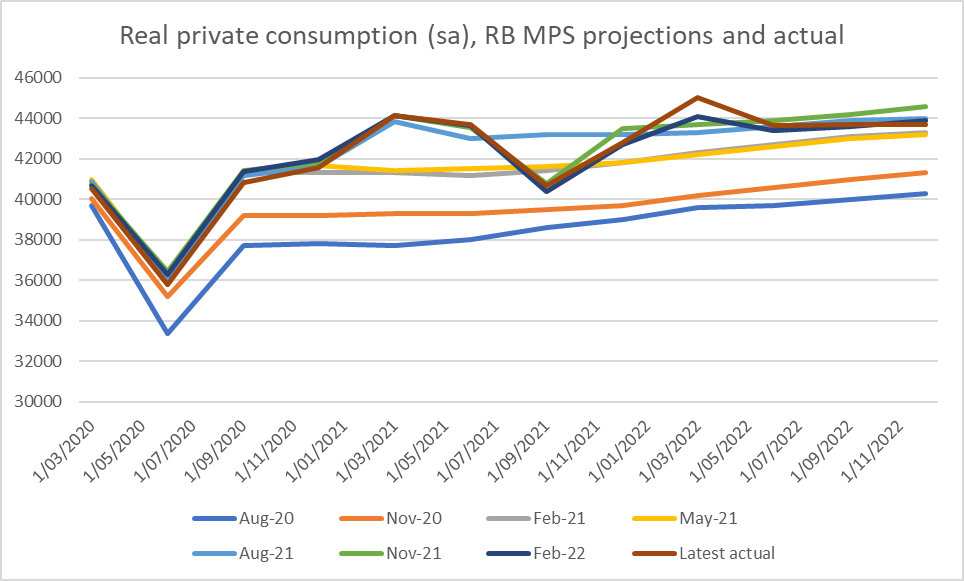

That got me wondering about the Reserve Bank of New Zealand’s forecasting.

Here are their successive MPS forecasts for real private consumption, starting from the August 2020 MPS which was done after the first and worst national lockdown was over.

The errors in the forecasts for 2022 being made in late 2020 are really huge (for consumption, which is not a particularly volatile component). By mid-2021 (when those BoE forecasts above were done) there were still quite big errors, but not so much about the medium term forecasts but about what the level of consumption spending was at the time the forecasts were being done.

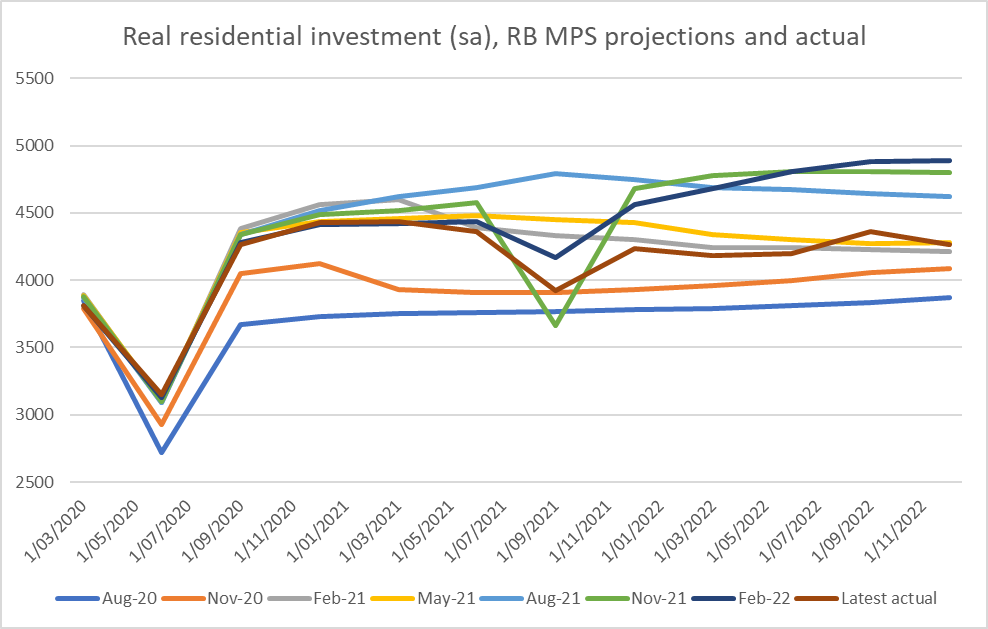

What about real residential investment?

Their forecasts for late 2020 and 2021 undertaken in late 2020 were miles off the mark, substantially understating the level of activity happening already and in the following few quarters. More recently, actuals have undershoot the forecasts done in the second half of the period, probably because of the much higher interest rates that proved to be needed relative to what the Bank had expected a couple of years ago.

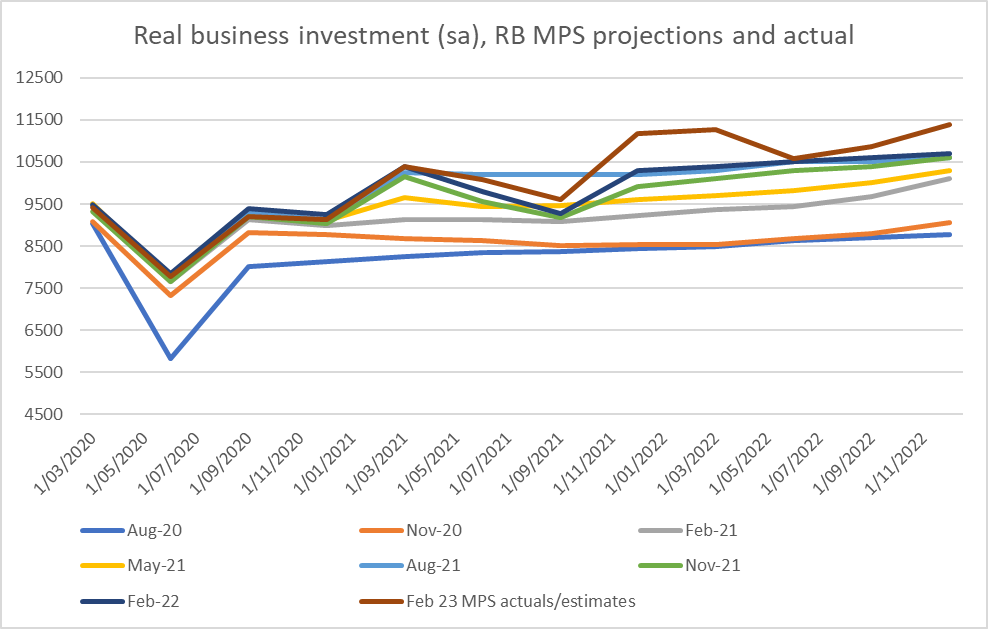

And here is real business investment

The Bank was badly misjudging the recent and contemporaneous situation in their August 2020 forecasts. That gap had closed substantially by the November 2020 MPS (a key date because the Bank then had such extremely low medium term inflation forecasts), but as with the private consumption chart shown earlier the forecasts for 2022 were still miles too low. Those errors probably go together, since high consumption demand and activity is typically likely to support high business investment spending. What is interesting is that business investment continued to surprise the Bank on the upside right through to the forecasts being made early last year.

I won’t clutter the post with a comparable GDP chart, but will quote just one illustrative number. In May 2021 I found myself in the curious position: for the first time in a decade, I had become more hawkish than the Bank. With hindsight it is abundantly clear that they should have been raising the OCR by then (and earlier). But their GDP forecasts made in May 2021 for December 2022 proved to be off (under-forecasting) by almost 3.5 per cent. Those are big mistakes.

If there is some mitigation for the BoE in having actually over-forecast the private consumption bounceback (one would want to know more about other components on demand) there is nothing like that in the New Zealand numbers. The Reserve Bank simply misjudged (badly) the strength of key components of domestic demand (and you’d see something similar in for example the unemployment rate forecasts and outcomes), and with it core inflation. One could fairly point out (and I have in previous posts) that many (perhaps almost all) private forecasters made similar mistake. But we – taxpayers and citizens – don’t employ private forecasters to keep core inflation near target; we employ and mandate the Reserve Bank (Governor and MPC) to do so, and they failed.

Which brings me back to those UK papers that started this post. One of the best bits of the Congdon piece was the call for some serious accountability for central bankers.

No one forced top central bankers to take their jobs (most would probably have had little problem getting other roles), and if they thought the mandates they had been given (in both the UK and NZ the finance minister sets the goal) were unachievable or unrealistic they were free to have said so and, if they felt strongly enough, to have resigned. Nobody was compelled to take on a task they believed was simply unachievable. And yet we’ve ended up with (core) inflation well outside target ranges in quite a wide range of countries, including both the UK and New Zealand, with no apparent consequences for any individual central bankers

Congdon proposes (in the UK context) that when inflation is sufficiently far outside the target range, both the Governor and the Deputy Governor should be required to offer their resignation. He doesn’t say so explicitly, but I presume he must mean this as more than the sort of pro forma charade one could imagine it descending to (“of course, I have to offer my resignation but we all know you Chancellor have no intention of accepting it”), involving actual departure from office. And one could, and probably should, broaden the expectation of real sanctions to include all the MPC members. There is (a lot) more scope already in the UK model for individual MPC members to express and record their disagreement with the majority view, but there is room for more, and the serious threat of sanction helps to sharpen incentives to think differently and not simply to (as is an easy incentive in any committee context) to hide behind the committee, and the (in recent cases) badly wrong consensus or majority view. In New Zealand, we have no idea whether any MPC member ever seriously questioned where the Bank’s forecasting and policy were going in 2020 and 2021. We should.

Perhaps what grates most about central bankers (and their masters, who go along with this behaviour) is the utter refusal of almost all of them to ever accept any serious personal responsibility. Here, Orr has repeatedly run his “no regrets” line and when he occasionally departs from it it is just to say that he is sorry New Zealand faced a pandemic and the Ukraine war (ie nothing about anything he or his colleagues are responsible for). He and his chief economist have also tried the line that they couldn’t have done much different – of course raising the OCR one meeting earlier wouldn’t have made much difference, but that isn’t the appropriate test – and there is quite a hint of that sort of defence in Broadbent’s recent speech (where he uses a straw man alternative of looking at what it would have taken to keep headline inflation at target, when the policy focus has never been primarily on headline).

The other day someone sent me a column from a UK newspaper in the wake of various recent BoE comments. The column ended thus

In the spirit of openness that an independent Bank of England is supposed to represent, it should offer a full and frank apology for letting down the British people.

Well, quite. And exactly the same could be said for our Governor and MPC. They made a really big and costly series of mistakes, which cost us (but not them particularly) a great deal of disruption and real economic loss. They failed in a mandate they had voluntarily chosen to accept (and been well-remunerated for). I’m a Christian and so contrition and repentance are pretty central to my world view, and whatever mistakes have been made in the past contrition and repentance go a long way. In public life – and nowhere more than among central bankers – it now seems alien and inconceivable that people could simply front up and acknowledge their mistakes, acknowledge the costs and consequences of those mistakes, and ask for forgiveness.

Instead, we pay the price – massive redistributions, big fluctuations in real purchasing power, overfull employment and then a probable recession, (oh, and don’t forget the $10bn of LSAP losses – an amount that would otherwise have more than covered the Crown’s recent cyclone costs) – and the central bankers just sail onwards enjoying their position, status, salary and so on, not even offering a serious accounting, let alone serious engagement, or any personal loss . Great power (which is what central banks wield) misued with no personal consequences whatever is a very long way from the model of delegated responsibility and accountability that shaped the design of both the UK and New Zealand central banking reforms in recent decades. In New Zealand, that isn’t just the responsibility/failure of Orr and the MPC, but of the Bank’s Board (appointed by the Minister supposedly to serve the public’s interest), the Minister of Finance, and ultimately – as with everything important in a system of government like ours – the Prime Minister.

And now just to distract us from the serious stuff, Adrian has organised a Symposium on Indigenous Integration. Has the RB lost the plot completely? Dare I suggest that October could possibly see some dis-integration and some anti woke sentiments being expressed loudly?

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

From what I can work out. The actual cost of the RBNZ QE was actually only $5 billion. The other $5 billion resulted from bailing out Kiwisaver and the NZ superfund which resulted in the government taking full 100% ownership of Kiwibank. I think the Labour govt in collusion with the RBNZ stole Kiwibank for a song from the actual owners which are the contributors to Kiwisaver and the recipients of NZ Super at a mere cost of $5 billion.

Lets not be fooled by the advertised $10 billion loss. The QE exercise in NZ was a magician’s slight of hand stealing a prime bank from the public without a whimper from the public. Compare the fiasco with 3 Waters. The public was furious for the Labour government’s attempt at stealing water. Stealing a bank, not a whimper.

LikeLike