The incoming Australian Labor government last year established an independent review of the Reserve Bank of Australia’s monetary policy functions, structures and performance. The review panel (chaired by a former Bank of Canada Deputy Governor) reported a few weeks ago and their full report is here. Periodic reviews of this sort aren’t uncommon, and are often triggered by episodes of discontent around the performance of the respective central bank (in New Zealand, the 2001 review conducted by Lars Svensson was an example).

There is no clear-cut single preferred way to organise policy functions that society (as represented by government and parliament) wishes to delegate decision-making responsibility to. That is true whether one thinks globally, or just of the subset of advanced economies that countries like New Zealand and Australia usually use as benchmarks or experiences/structures that might offer insight.

If this proposition is true generally, it is no less true of monetary policy specifically. And that shouldn’t really be surprising, including because monetary policy is really quite a recent thing. In New Zealand and Australia the transition to a market-based financial system and a floating exchange rate is not quite yet 40 years old, and even among larger economies floating exchange rates more generally date back only 50 years or so. Modern monetary policy is a cyclical management function (leaning against cyclical macroeconomic fluctuations subject to a constraint of keeping the inflation rate in check), and yet our data sets are really quite limited (since 1984/85 New Zealand has had 4 or 5 business cycles, and the creation of the euro means there are really only perhaps 15 or so advanced-country monetary policy agencies). We simply do not know with any degree of confidence that one form of monetary policy governance etc structure will produce better results over time than another. Instead we (all, including the RBA review panel) argue from small select samples, from specific historical incidents (where multiple influences are always likely to have been at work), and from the mental models we carry round (some likely to have achieved a professional consensus, others not).

None of which is to suggest that such reviews should not take place. Of course they should, and with good people and a government that is interested in good future structures (as distinct, say, from just being seen to having had the review – there were dimensions of the latter around the review then then New Zealand government commissioned from Lars Svensson) useful insights, outcomes, and reforms can often emerge. There will always be aspects of current practice or legislation than benefit from someone standing back and concluding that it is really time for an update, even if in practice the old arrangements were working tolerably adequately.

But one should also be cautious about expecting too much from any particular review or any particular set of reforms.

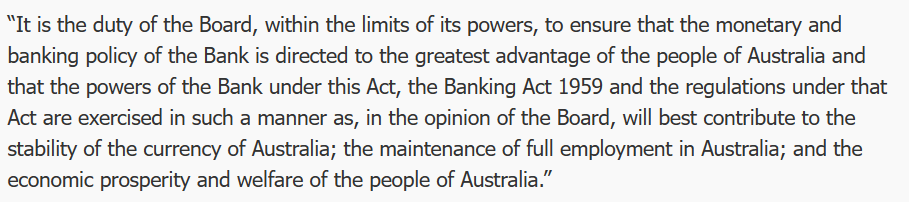

The current RBA model is not one anyone would prescribe today if they were setting up a central bank from scratch. A fair bit of the legislation dates back to the founding in 1959, including this

It has been interpreted, stretching language and concepts to a considerable extent, as encompassing the way monetary policy has been run for the last few decades, but really it was written for an age of (among other things) fixed exchange rates. No one would write it that way now.

And the governance? The Reserve Bank of Australia Board makes the monetary policy decisions (back in the day in practice the Treasurer did) and is much as constituted decades ago. The Governor, Deputy Governor, and the Secretary to the Treasury are ex officio members and there are six non-executive directors appointed by the Treasurer. The non-executive members have typically been (often quite prominent) business figures, but over recent decades it has been normal for one of the six to be a professional economist. It is a very unusual model these days for the conduct of monetary policy, although note that the sort of people appointed as non-executive directors is a matter of political choice (successive Treasurers) and I can’t see anything in the legislation that would have prevented six technical experts being appointed.

If the relevant bits of the legislation haven’t changed a lot over the decades, practice has. Monetary policy decisions are clearly made independently by the RBA, in pursuit of a target that is in practice agreed in advance with the Treasurer, they are announced transparently, there are minutes of a sort published, as well as the quarterly Statements on Monetary Policy. Senior managers appears before parliamentary committees and have fairly extensive and serious speech programmes. The RBA is a modern inflation targeting advanced country central bank, but operating on quite old legislative foundations. As an organisation, over the decades it has had considerable strengths, including typically a strong bench of very capable senior managers, and people coming up behind them. Successful organisations in many fields tend to promote mainly from within: that has been the RBA approach (and is very much in contrast, say, to the RBNZ). Note here that promoting from within is not itself a basis for a successful organisation, simply one feature that already successful organisations, continually refreshing themselves, often display.

I was an admirer of the RBA for a long time, and 20+ years ago when the Svensson review was underway (when I was both part of the small secretariat and a senior manager at the RB) thought that New Zealand should look to adopt elements of the structure and culture of the Reserve Bank of Australia. They tended to produce more stable outcomes, produce better research, communicate more effectively, and have a stronger sense of legitimacy than our “Governor as sole decisionmaker” system had achieved (or than Svensson’s preference, of a small internal decision-making committee (of which the position I then held would have been a member) was likely to be able to achieve. The RBA on the other hand saw us as somewhat strange, not always entirely fairly. I recall a time when Glenn Stevens as Assistant Governor and he came over to observe our monetary policy and forecasting week leading up to an MPS (shortly after we had started publishing forward interest rate projections), and he emerged from the week genuinely surprised that our approach was far less mechanical, nay mechanistic, than he had been led to expect. Or a visit from David Gruen, then head of research at the RBA, suggesting that the fact that our interest rates averaged higher than those in Australia suggested we had monetary policy consistently too tight (in fact prior to 2009 New Zealand inflation typically averaged in the top part of the target range).

Over recent decades, Australia has enjoyed a reasonable degree of macroeconomic stability (the review report includes a table showing the standard deviation of real GDP growth less than for any other country shown), this in any economy exposed to very big swings in the terms of trade. As noted above, the samples are small but there is nothing obvious to suggest that overall the Australian approach to monetary policy has delivered worse than other advanced country central banks. But there have been troubling episodes, notably including the one in the years running to Covid when Australian core inflation ran consistently well below target (much more so than anything seen at the time in other countries, including New Zealand where core inflation by then was getting close to the target midpoint). There are also more recent episodes of concern – about specifics of the RBA Covid response and latterly about the sharp rise in core inflation – but through that period it is perhaps hard to differentiate the RBA’s failure (underperformance) from that of a wide range of other advanced country central banks (themselves with a wide range of governance models).

This was one of the things that troubled me about the review report. The first substantive chapter is focused specifically on these recent episodes. It is easy to highlight areas where things could have been done better in (almost any) specific episode – and some of the material cited is pretty disconcerting – but that is almost certainly true of every central bank, and there is no attempt I saw in the report to illustrate that anything would have been very much different with a different governance/committee structure. We might hope it would have been, but the panel offers little reason (and realistically they couldn’t offer more) that it would have been. New Zealand, after all, has introduced a committee, and the panel notes favourably (too favourably) the expertise of its members relative to RBA external board members, but many or most of the same mistakes or weaknesses the panel highlight in Australia over the last three years were also evident in New Zealand – as far as we can tell, as less material has been released here than there, us not having had a recent external review and the Reserve Bank’s own review was largely defensive and unenlightening in nature). Should there have been a proper cost-benefit analysis, and serious questioning from the Board, before the RBA bond-buying programme was launched? No doubt (and the review report is properly critical about the absence, and the likely weak case) but there is no evidence of anything even slightly better in New Zealand. Or, as far as I’m aware, in any or many other advanced countries. Perhaps the RBA case was less excusable, since they started bond buying a lot later, rather than in the heat of the crisis, but the practical difference ends up being slight.

The review panel proposes a new model with these important features

- monetary policy decisions would in future be made by a Monetary Policy Board (with a separate RBA governance board, and the existing Payment Systems Board),

- the MPB would have nine members, the Governor, the Deputy Governor, the Secretary to the Treasury, and six expert non-executives appointed for non-renewable terms of five years, extendable for up to one year)

- non-executive members would be expected to devote about one day a week to the role (around eight monetary policy decisions a year)

- there would be a press conference for each decision,

- votes would be disclosed but not attributable (ie a decision might be made 7:2, but the two would not be identified by name)

- non-executive members would be expected to do at least one public engagement or speech a year,

- non-executive vacancies would be advertised, but recommendations to the Treasurer (who would make the final appointments) would be by the Governor, the Deputy Governor and a third person (presumably to be chosen – altho by whom, Treasurer or the officials? – from time to time).

If you were starting from scratch, one could think of worse systems. But this proposal seems to have a number of weaknesses and reason to suspect that unless a strong political consensus developed early around making things work really differently (rather than differently in appearance) it is far less good a system than could have been devised. Even then, I would not be overly optimistic. More generally, my impression is that the report tends to underweight the relative importance of the Governor and very senior management to how central banks operate.

Starting with the small stuff, as the report notes it is highly unusual for the Secretary to the Treasury to be a full voting member of a central bank monetary policy decision-making body. It was one thing in 1959 – at that time New Zealand also had the Secretary to the Treasury as a full member of the (largely toothless) central bank board – but it is 2023. Other countries – including the UK and New Zealand – have preferred the model of a non-voting Treasury observer, which seems bit suited to (a) the desire to ensure at the highest levels that information flows freely between monetary and fiscal agencies) and (b) the Secretary’s own primary responsibilities and loyalties. The report proposes amending the legislation to make clear that the Secretary is voting his/her own judgement, but if so that tends to defeat the purpose of their place on the Board (being there solely ex officio), and in times of tension – and one should build system for resilience in tough times, not for when everyone is getting on fine and everything is going swimmingly – will likely complicate the Secretary’s own position (including as adviser to the Treasurer in holding MPB members to account for performance).

In general I am in favour of a model in which external members outnumber executives, but 6:3 in a nine person board doesn’t feel right (even if it parallels current numbers). 4:3, with the third executive being the Assistant Governor responsible for economic policy, seems a better size overall, and also more realistic about the ability of the system to continue to generate a steady stream of able people to fill (only) five year non-executive terms. And a 7 person committee is more likely to limit the risk of free-riding by individual non-executives.

It is difficult to see how a “day a week” model is likely to work IF the goal really were one having a powerful role, including as expert counterweight to staff, if non-executives were devoting only one day a week to the role. I am not aware of any precedents for such a small contribution, which seems to sit closer to the current RBA Board model (might such board members devote 2 days a month to the role, one to the meeting, one to the papers?) than to other advanced country MPCs. At the Bank of England MPC, probably still the best model, non-executives are paid for 3 days a week work, and at a rate that (least by academic standards would be a reasonable fulltime income). On a day a week model, not only is the actual amount of time any member can devote to RBA matters limited, but the remuneration would that for any non-retired person it would have to be just one part of the member’s employment/income. Most plausibly, they would be current academics, who might otherwise not spend a vast amount of time keeping track of data or of the literature in the specific fields relevant to central banking. We might assume that people will not be disbarred (as is NZ) for doing ongoing research in relevant fields, but even in Australia the numbers of such people are not limitless. One day a week looks like a recipe for an ongoing dominance of management and staff. Consistent with this, while the report suggests that externals should have direct access to staff, if they do not have dedicated analytical support staff of their own their ability to make a difference and shape what is in front of the MPB is likely to be limited. This is, incidentally, one argument for a quite different system – as in Sweden or the US – in which outsiders become full insiders while they are MPC members.

The appointment process is also a concern. One of the weaknesses of the New Zealand MPC system is that the Governor exercises considerable effective control on who serves on the MPC. A really good Governor would have a strong interest in promoting genuine diversity of view and real ongoing intellectual and policy challenge. Real world bureaucrats, running their own bureau, perhaps less so. No doubt there will be arguments about “fit” etc, but the value of outsiders is often in the extent to which they are willing to bring fresh thinking and not be easily deterred by management flannel and weight of paper. With a strong “third person”, perhaps it would work out okay, especially if a Treasurer was clearly committed to viewpoint diversity, challenge etc, but many potential “third persons” might be inclined just to defer to the perceived expertise of the Governor and Secretary.

Accountability does not appear to be a key element in the RBA reform proposal. That seems unfortunate – perhaps especially coming hard on the heels of the massive financial losses central bankers have run up and the scale of their inflation forecasting and policy mistake. If as a society we delegate great discretionary power to unelected officials – and that is what we do in MPCs – accountability is a key counterbalance, including in maintaining the long-term legitimacy of the model. At very least, MPB members should be required to have their named votes recorded and disclosed. Ideally – but it is probably only an ideal – people should be able to be removed from office for non-performance. In fact, one of the other weaknesses of the proposed single term model for externals is the complete absence of accountability. Their views don’t have to be disclosed, their votes don’t have to be disclosed, and since they can’t be reappointed, there is really no accountability at all. Lack of accountability doesn’t exactly encourage members to devote intense energies to getting things right. Some no doubt will, but it will be all too easy to defer to management and treat membership of the MPB as a prestige appointment (like being on the RBA Board now), this time narrowed down to being for economists, rather than a role in which one will make a difference and expect to be held to account.

As I said earlier, there is no one ideal structure. In the end, one is trying to combine technical expertise, experience, judgement, ability to communicate, and something around accountability to produce good policy outcomes taken in ways consistent with our open and democratic societies and under structures that are resilient to bad times and to bad people All in a field where uncertainty is pervasive.

Many of these requirements might well be met with no outsiders at all. You won’t see it highlighted in the review report but the Bank of Canada is one in which, formally and legally, the Governor himself wields the monetary policy powers (akin in that feature to the RBNZ system pre-2019). But in practice the BoC has built a strong internal culture and an effective system where a Governing Council of senior internal managers makes monetary policy decisions by consensus. I don’t think it is ideal – there is no individual accountability except (presumably) to the Governor – but the BoC has built partially compensating mechanisms with extensive research programmes, self-review programmes, and extensive engagement with academic and other wider communities. Indeed, the Bank of Canada model – which I do not champion – highlights just how important the quality of staff and internal processes are. It isn’t necessarily a problem if decisionmakers typically defer to staff and management expertise – in fact it is what you would expect in a normal corporate board – so long as those decisionmakers can continually assure themselves that staff and management have robust and resilient processes in place, including those that encourage, generate and accommodate, genuine diversity of view and openness to alternative perspectives. In that sort of context, some expert external MPC members can be very helpful (especially if they are familiar with, engaging with, perhaps contributing to) emerging literature, but they aren’t the only type of member who could add value. The willingness to actually ask the idiot question, and never to be content with management bluster, is valuable in any governance context. Thus, in an RBA context, one might wonder whether it is really worth having a whole new Board (especially when the RBA is not a “full service central bank” (doing prudential supervision)), when one could have left the RBA Board responsible for monetary policy but with a requirement say that several members should have directly relevant professional expertise. One could argue that being a board member, responsible for all the RBA functions and governance, might make for a person better able to contribute effectively as a monetary policy decisionmaker (and note that there is plenty of role for outside expert advisers anyway, and the report does suggest a more active macro research programme for Australia generally). And of course, in all our systems Ministers of Finance – rarely very expert at all – make major contentious economic policy decisions in climates of extreme uncertainty, drawing on expert advisers but rarely handing decision-making power to such experts.

Overall, I can’t help feeling that if the Australian government goes ahead and legislates all these changes, none of them (not all taken together) will matter quite as much as who gets appointed as Governor, and the sort of internal culture and people, the Governor (and his/her successors) build. That is a critical choice – in Australia, in New Zealand, probably anywhere – and is likely to far outweigh any potential difference that a few day-a-week academics, cycled through the decisionmaking system on five year terms, might make. A great Governor (and we can’t build systems that assume one) will build and maintain a culture that delivers most of what the review panel (often rightly) seems to be looking for.

This post has gone on long enough. It is about someone else’s country so why my interest? Two reasons I think. First, it is a significant report on a central bank in the midst of troubled times, and there are few of those yet. And second because the choices Australia makes are always likely to be an important backdrop to any future reforms in New Zealand. We have had extensive reforms, clearly designed to look different rather than be different, and any new government needs to look to do over quite a few of the aspects of the New Zealand model.

I was going to engage specifically with the AFR article last Friday by Ian Macfarlane, former RBA Governor, criticising the review (and I thank the two readers who sent me copies). Time and space is limited, so I won’t. It is worth reading, and he makes some fair points (some less so), but it is perhaps worth remembering that Macfarlane was Governor at the peak of the RBA’s past standing. The starting point now is less favourable.

Finally, one of the background papers for the review was commissioned from Professor Prasanna Gai at Auckland University (and ex BOE). Gai currently serves on the FMA board, but probably should be one of those considered for our MPC, but……he would be disqualified by our Governor and Board on the grounds of an ongoing active interest in areas the MPC would actually be responsible for. Anyway, his paper is quite a good read on international models around the governance of monetary policy, and he pulls few punches about the weaknesses of the New Zealand model.