There have been a few posts here recently about Professor Caroline Saunders, whose initial term on the Reserve Bank MPC expired at the end of March and who was eventually, belatedly, and with no announcement at all, appointed by the Minister of Finance to a short second (and final) term on the MPC. The most recent of those posts was here.

When there was no announcement before the Saunders term expired, I had lodged OIA requests with both the Reserve Bank and the Minister of Finance for material relating to her reappointment (or otherwise). Responses to both emails have now come back.

If it is now clear that the bottom line reason why Saunders was not reappointed before her term was expired was administrative slackness (between the Minister’s office and Treasury mainly), the documents that were released don’t put any of those involved in a particularly good light.

My request to the Bank was fairly broadly phrased

I am writing to request all and any material (including any advice to the Minister) relating to the expiry of the MPC term of Caroline Saunders and any discussions or decisions to reappoint her (or not) or to extend her term

and since the Bank says it has not withheld any documents, it seems fair to assume that what I have is all there is.

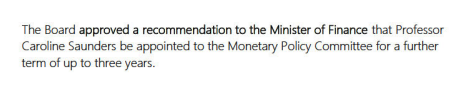

This was the first document they released, from the minutes of the Reserve Bank’s 7 December 2022 Board meeting/

In other words, there was no paper analysing the record of the MPC or the personal contribution to the MPC made by Saunders, even though the decision to recommend reappointment was being made in the midst of the worst monetary policy failure in the decades since the Reserve Bank was given operational independence around monetary policy. There was also apparently no paper discussing the best balance of the MPC in the period ahead, or the appropriate length of time for a reappointment (not even, apparently, a discussion as to why the recommendation is for an extension of “up to three years” when the law would allow up to a four year second term. There is also no sign in those minutes of any substantive discussion or hard questions being posed by Board members (unsurprisingly perhaps given the lack of relevant background of all but the chair, who presumably had any conversations with the Governor in private, unminuted).

It was, it should be noted, no better when the other two external MPC members were reappointed (for terms from 1 April 2022), but the inadequacy of the process is all the more glaring by late 2022 when the extent of the monetary policy failure, for which MPC members are responsible, was much clearer than perhaps it was to the previous Board in late 2021.

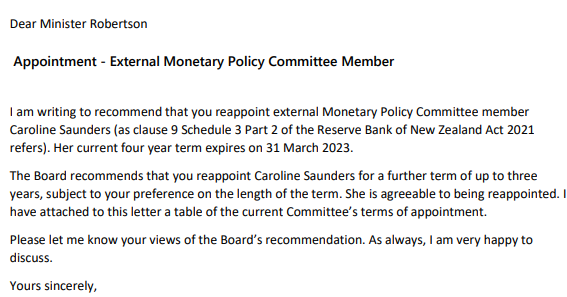

The Board chair then seems to have moved fairly expeditiously, sending a letter of recommendation to the Minister dated 16 December 2022.

although it is not entirely clear whether this was sent directly (it is signed and dated) or only as an attachment to a memorandum to the minister from Quigley dated 9 January 2023. This is the entire substance of that memo

Note several things

- (trivially) there is actually a mistake in the letter (Buckle’s second term expires in March 2025 not September 2025

- there is no advice (not a word) to Minister about the contribution Saunders had made over her (by then) 3.75 years on the MPC, a period in which (a) the regime was new, and (b) monetary policy was sorely tested.

- despite explicitly noting to the Minister that Saunders could be reappointed for four years, the Board chair offers the Minister no information as to why the Board thinks the extension should be only “up to” three years.

- presumably after discussions with Treasury, the Minister is told that the process for reappointment should take about two months (this in a document submitted on 9 January). Elsewhere in the formal recommendations the Minister is asked for a decision by 23 January.

And then there are no other documents (and the Minister has also not indicated that he has withheld whole documents) for more than two months. The next document is dated 8 March, only three weeks before the Saunders term expires.

In any country with serious scrutiny of the MPC – and a belief that external MPC members made any difference whatever – serious questions would have been being asked by now, by market participants and by journalists. After all, on paper MPC members wield a great deal of power, and things hadn’t been going that well with monetary policy. But there weren’t.

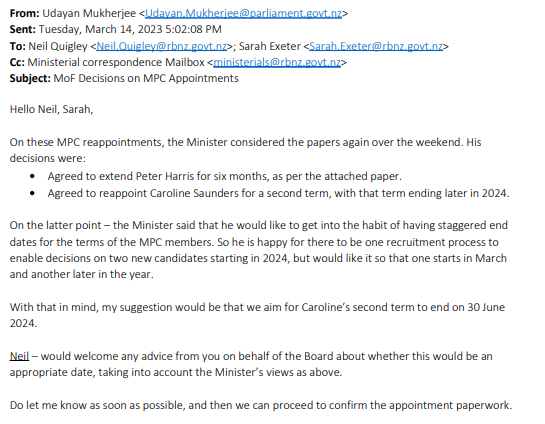

In an internal Reserve Bank email (to the Governor) we learn that on 2 February “the MoF’s office asked for a clarification to be made to the letters/report which we provided (that CS be reappointed ‘up to 3 years’ subject to the preference of the MoF”.

And again nothing until 4 March when the timeline in this same email records that “MoF’s office call Neil Quigley to seek clarification on Caroline Saunders’ reappointment. On 6 March, the Reserve Bank learns “from MoF’s office that the recommendation will go in the weekend bag….and we should get an outcome early next week”.

And they did

which is strange again, because while the Minister is reported as favouring staggered terms for MPC members (and very sensibly so) he deliberately, and with no officials’ recommendation plumped for a term for Saunders which will mean that the terms of all three external members expire between 31 March 2024 and 31 March 2025. It would have been easy to have given Saunders a three year term or even a four year term and really stretched things out. But he did not, and there is no indication why in any of the papers.

Quigley reverts to the Minister accepting the general idea and a very short extension to 30 June 2024 is agreed. Quigley observes that “Caroline’s term ending at that time is entirely workable from my point of view. As you say, the search for a replacement can still be part of the same search that we undertake to fill the other vacancy from 1 April 2024”. Since it is already May, one might suppose that a new search process – since both Saunders and Harris cannot be reappointed again – will be getting underway fairly shortly.

At this point it is realised that they are too late to get the Saunders reappointment confirmed before her term expires (it needed to go through the Cabinet Appointment and Honours Committee and to be confirmed by the full Cabinet) but nobody seems very bothered by this. As the documents note, and as I initially missed, the (dubious) statutory provisions for MPC appointments allow an MPC to stay in place after their term ends unless advised otherwise by the Minister. But there is no sense of urgency, no sense (perhaps accurately) of any likely media or market interests (despite the on-paper power these positions wield), at least until I wrote a post on 3 April, which prompted the Reserve Bank comms staff to (a) prepare a draft statement if at that late point there were to be any media questions (which there weren’t) and (b) quickly update their website to make clear that members could remain in office after the expiry of their term,

There is no hint in any of the papers released as to why the Minister of Finance chose not to announce formally the reappointment of Saunders (or the extension of Harris, to get around election timing) and rather leave the fact to be discovered either by chance or by assiduous readers of the Gazette.

In the grand scheme of things, perhaps none of this matters a great deal, but the promise was, in reforming the Reserve Bank Act, that MPC members really would matter, and would make a difference. Over four years, there has not been the slightest evidence for it.

But it still seems to be a very bad look, given that the government chose to keep on with the curious appointment model in which the Minister can only appoint people his hand-picked (and not for relevant expertise) Board recommends, that there is no evidence the Board itself engaged in (or received) any serious analysis or review of Saunders’ contribution to the MPC through such a challenging period, and that there is no evidence that any serious substantive advice was being provided to the Minster on her contributions, strengths and weaknesses. It doesn’t reflect much better that there is no sign that the Minister cared, or sought such advice (despite how far outside the target range core inflation has been). The Minister’s office processes seem to have been slack, to say the least. No doubt he is a busy man, but he has a fully staffed office, and there is much justification for sitting doing nothing for two months on a recommendation for an appointment that really should be somewhat market sensitive.

As for Saunders, were she really making a stellar contribution to the MPC (a) the Board might have been expected to have highlighted that and recommended a full four year term extension, and (b) the Minister might have been expected to have enthusiastically agreed (she was after all his preference four years ago). Instead, nothing, and about the shortest credible extension it was possible to have given her.

Finally, there are some issues for any incoming government later this year. As I often point out, a new government that was unhappy with how the Reserve Bank and MPC have been operating cannot simply get rid of the Governor. They can however make appointments around him (including Board and MPC members). Any different government has been given quite a gift by Robertson, in that all the external MPC member positions will expire by 31 March 2025 and all have to be replaced. The Board chair’s own term expires on 30 June 2024 (he was given only a two year (presumably final, transitional) term on the new Board. Given the mediocre appointments to date, and lack of evidence of serious scrutiny and review, if an incoming government really cares about making things better at the Reserve Bank, they will need to take the issue in hand early and make it clear to the Board – themselves quite unqualifed to judge – just what sort of people the Minister will consider appointing (removing, for example, and one would hope, the current blackball on anyone actually engaged now or in future in any serious macroeconomic analysis and research). It is most unlikely that better outcomes (people, process, policy) if Orr and Quigley are simply left to do things as they’ve been done for the last four years.

The question of course is whether the Opposition parties really do care. It is easy to run lines now about “cost of living crises” and high inflation, but (core) inflation is a Reserve Bank outcome and the Minister of Finance is ultimately responsible for, and wields more than a few levers over, the Reserve Bank (people, processes, budgets, and policy goals).

In the meantime, what this little episode reveals again is the empty charade the new MPC is, and always was. We have a minister who was interested in the appearance of change rather than the substance of change, and who has shown no interest at all in holding policymakers to account for signal policy failures. And a Governor who could live with (perhaps even embrace the rhetoric of ) the appearance of change so long as his actual dominance of the process and institution was left substantively unchallenged. A double coincidence of wants, just not one well aligned with the wider public interest.

Reblogged this on Utopia, you are standing in it!.

LikeLike

[…] Source link […]

LikeLike

Brilliant, Michael, you have the tenacity of a bulldog, although I imagine the ‘cognocente’ of the Wellington Establishment might have a different description of one ‘Michael Reddell’!

Your description of this sorry saga, reinforced by the OIA response doesn’t indicate actual corruption, but the sheer slackness in appointing people to taxpayer funded positions of significance, is surely right up there in terms of poor practice.

It also indicates the possibility at least, that the appointment of dozens of other persons to the boards of our many commissions, task forces and quangos is done on a similar casual basis.

Poor old Sir Geoffrey Palmer who dedicated himself to substantially prune the huge number of these semi out of control taxpayer bodies, must be rolling his eyes…at the very least!

Keep your teeth in the backside of the body politic, Michael.

LikeLiked by 1 person