As the wild gyrations around the sharp decline in Chinese share prices dominate the business news headlines, the chart of the Shanghai share price index was reminding me of another chart, from our own history.

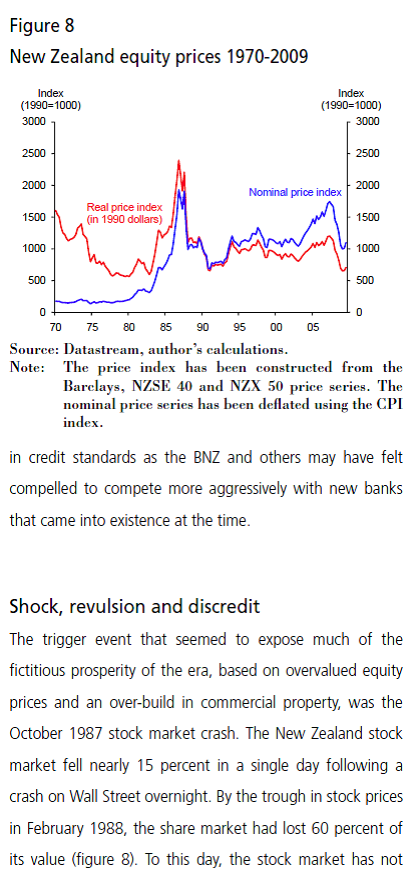

The historical data are hard to come by so I’ve had to use this chart, which covers a rather long period, from a good Reserve Bank Bulletin article about past New Zealand financial crises (mostly, the 1890s and the 1980s). In China’s case, a 150 per cent increase in share prices in a year or so, most of which has now been given back in only a few months (of course, it is perhaps worth remembering that there was an even bigger boom, to even higher peaks, in 2006/07). In New Zealand’s case, the boom in real prices was even larger – if it took a slightly longer period of time – and the bust was complete.

There is lots of discussion at present – often from US-centric people – about how the Chinese share market is somewhat peripheral to the economy. And, in some senses, no doubt it is. The share market has always been relatively peripheral to the New Zealand economy too, and market capitalisation as a share of GDP has typically been low. Between farms, farmer co-ops, wholly foreign-owned companies, and state-owned companies, most economic activity simply wasn’t represented by listed companies. Take state-owned companies as an example. In 1986/87, the government still owned several banks, insurance companies, the post and telephone system, the one TV company, the railways, the airlines, the largest petroleum company, and the steel mill. There were no New Zealand listed banks, and no vehicles for direct equity exposures to our largest export industries (sheep and dairy products). Forestry was probably the only major export industry with material listed exposure.

And yet the market went crazy, and when it burst it was the start of some very tough years for New Zealand. The whole post-liberalisation mania has not been adequately documented (unlike, say, the Nordics booms and busts of much the same time), but it was characterised by much more than just crazy share prices for the minority of people with any material direct exposure to the market. These things rarely happen in isolation. We had a massive credit boom – private sector credit growing at 30 per cent per annum – and a massive commercial property boom, skewing real resources into places that proved not really to offer economic returns. The absurdity of some of what went on during that period was captured in the suggestion of one (brief) high flyer, that New Zealand had a comparative advantage in takeovers. Few bankers had any experience in disciplined credit risk analysis in a liberalised market economy – and nor did their shareholders (whether government or Australian private). And, in any case, bonuses weren’t being paid to people who stayed clear of the boom for long. Highly leveraged investment companies were all the rage – often the principal asset was overvalued shares in other investment companies.

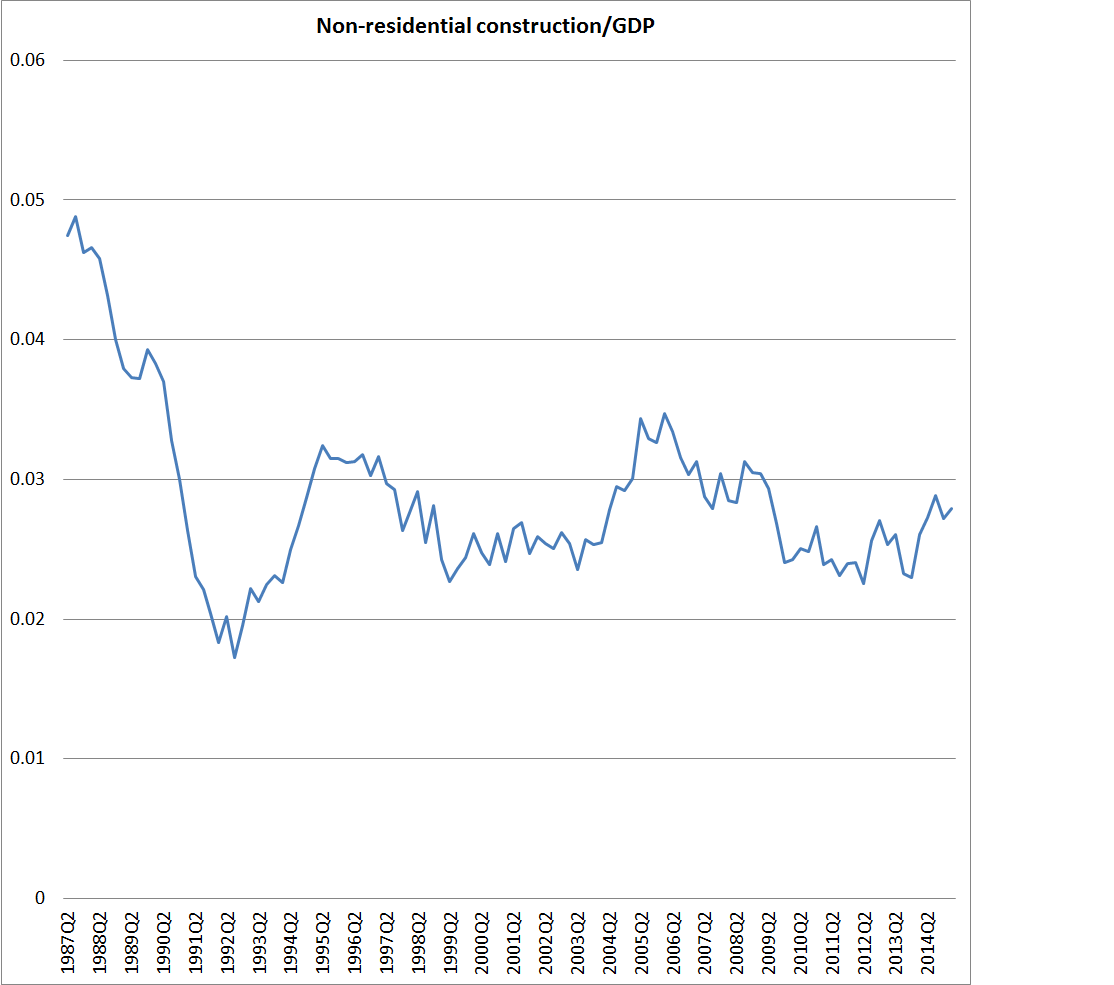

As one illustration of what went on, here is the commercial property picture. A 3 percentage point of GDP fall is huge, and of course the boom-times share of GDP has never been regained, suggestive of how overblown that market had become.

As they often are, central bankers were slow to recognise what was going on. The section I managed wrote a paper to the Minister of Finance a few weeks before the crash arguing (as I recall) that the strength of the share market was a pointer to the underlying strength of the economy (and hence a reason to tighten monetary policy). A week or two after the crash, my boss and I were visited by a firm of economists we were often dismissive of – they urged us to recognise that a savage commercial property and banking shake-out was about to get underway. We were polite but pretty dismissive.

Those are the sorts of episodes that leave financial crises in their wake, and which often have nasty and prolonged real economic consequences. Some of us at the Reserve Bank might have initially been a little sceptical, but the liquidity stresses soon became very apparent. Within weeks we had acquiesced in a sharp fall in short-term interest rates (we didn’t directly set them then), which eventually totalled 400-500 basis points. The exchange rate came down as well. And it still took years for the economy to really recover.

No two situations are ever quite the same. New Zealand was trying to vanquish double-digit inflation, a situation few countries these days find themselves in. But ill-disciplined credit booms, of the sort we had in the 1980s, and of the sort the Chinese have had – on a far larger scale and with fewer market disciplines – are often enormously damaging. Often there is an equity market mania dimension to these things, but the mania is often the epiphenomenon rather than the main event; symptoms of something deeper going on. And the timing will never be quite precise – we had a mania in 1986 around a company (investment and finance) whose shareholders, in their private capacity, were backing what appeared for a time likely to be a successful tilt at the yachting America’s Cup. Of itself, it probably did little or no real economic harm, but it was symptom of the excesses, and of the undisciplined nature of the times.

So count me as a little sceptical of the notion that because not many Chinese hold shares, we don’t need to worry about what is going on there. As here, it is a matter of looking to the phenomena behind the headlines – in their case, several years of one the largest, least-disciplined domestic credit and investment booms in history.

Oh, and there are simply no parallels between the 1987 New Zealand position – which brought down several major financial institutions, including our largest bank – and the New Zealand position now. I wrote about that (lack of) parallel a few months ago.

Great post. It’s easy to forget how big the late 1980s boom and bust was.

Would be interested to hear any of your recollections of the Think Big era and any parallels with China today.

LikeLike

I’m not quite that old (didn’t start at the Rb until the end of 83). But, yes, curiously (?) the only time in the last 50 years when business investment as a % of GDP got materially above the OECD median was during that state-prompted artificial investment boom, which the credit boom came in on top of once we liberalised.

The person who could be interesting on Think Big would be Graeme Wheeler – he was in the energy section of Tsy at the time. A former Dep Sec at Tsy told me that half of Tsy favoured Think Big and half opposed, which has always stood as a reminder to me about how very smart people can get things so completely wrong.

LikeLike