When the Bank of England launched its new blog a while ago I suggested that, despite the promotional material suggesting it would publish materially challenging current orthodoxies, that seemed unlikely – unless, that is, it was to be a vehicle for challenging orthodoxies that senior management themselves wanted to challenge.

I haven’t seen any sign of orthodoxies challenged so far. But, on the other hand, the blog has proved an excellent vehicle for Bank of England staff to give greater visibility to work on a range of interesting, mostly empirical, economics and finance issues. And to do so in bite-sized, not overly technical, chunks.

A while ago I ran a series of posts (eg here and here) on why New Zealand’s real interest rates had been so persistently high relative to those in other advanced countries. Our real interest rates are much lower than they were 20 years ago, but so are those pretty much everywhere.

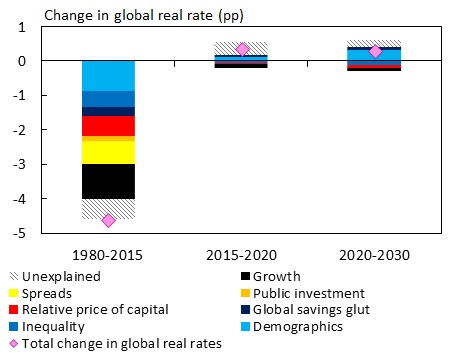

Over the last few days, two Bank of England blog posts (here and here) have looked at what lay behind that global trend decline – of around 450 basis points since 1980. They use as a framework the idea that observed real interest rates, at least at a global level, reflect the interaction of desired savings rates and desired investment rates. At the global level, actual savings and actual investment are equal ,and the real interest rates adjust to reconcile any ex ante differences.

The authors identify a number of factors which they estimate can explain perhaps 90 per cent of the fall. These includes slowing global population growth, falls in desired public investment spending, the falling price of capital goods, an emerging markets “savings glut”, rising income inequality, slower growth rates, and so on. Here is their summary picture.

And here is how they apply the framework to thinking about the next few years.

Our framework allows us to speculate what will happen next (Figure 6, above). The big picture message is that the trends we have analysed are likely to persist: we do not predict a big further drag, or a rapid unwind of any of these forces. Some are likely to drag a little further (global growth is set to decline further out; the relative price of capital is likely to continue to fall; and inequality may continue to rise); but this will be broadly offset by a rebound in other forces (particularly demographics). What happens to the unexplained component depends on what’s driving it. In Chart 6 we illustrate the implications of assuming it is largely cyclical. Despite that, this would still imply global neutral rates will stay low, perhaps around 1% in real terms over the next 5 years.

I don’t find every detail persuasive, but the broad story rings true. Interest rates (short or long term) are not low because of central banks, but because of rather more fundamental forces. And few of those seem likely to reverse any time soon.

Perhaps it would be helpful if the authors had been able to interpret their results for the last 35 years in a much longer historical context. Even if we can explain the fall in real interest rates since 1980, it is much harder (I suspect) to provide a compelling reason for why interest rates are now so much lower (in most countries) than at any time for hundreds of years. Rapid population growth, for example, was substantially a post-WWII story. But perhaps that reconciliation is one for another author.

In a New Zealand context, I remain fairly convinced that demographics have played a material role in explaining interest rate pressures here. In particular, the policy-driven component, of our immigration policies over the decades. As one small component of a world economy, the argument is not as straightforward as for the world economy as a whole. But with one of the faster population growth rates in the advanced world, it should not be any great surprise that we have seen persistent pressure on our real interest rates (and, hence, on the real exchange rate). We’ve shared in most of the fall in global interest rates, but there has been no sign of any closing in the large trend gap. In the 1950s and 1960s those pressures showed up in tight credit controls and import controls etc (to suppress demand by fiat). Since liberalisation they have shown up as persistently higher average interest rates than those in the rest of the advanced world. As a result, business investment has been quite subdued, and what business investment there has been has been concentrated more heavily in the non-tradables sector than one might have otherwise expected in an economy that had undergone the sort of liberalising reforms New Zealand undertook in the 1980s and early 1990s.