I’ve been continuing to reflect on Graeme Wheeler’s repeated observation that New Zealand’s exchange rate “needs” to come down. I’m still not entirely sure what he means. The exchange rate is an asset price and presumably should reflect all expected future relevant information, not just spot information about current dairy prices. And the market has no particular reason to focus on stabilising the net international investment position at around current levels. Indeed, although it is a convenient reference point, neither does the Reserve Bank.

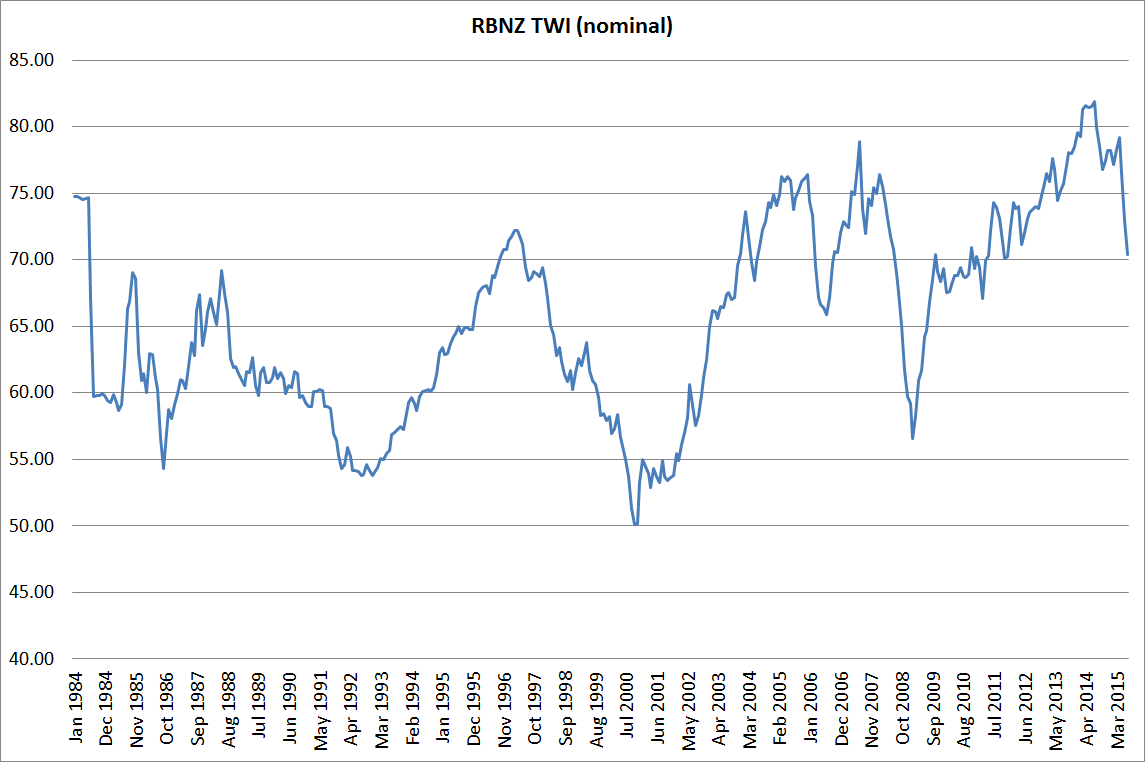

“Need” or not, I’d have thought it was likely that the exchange rate would fall further.

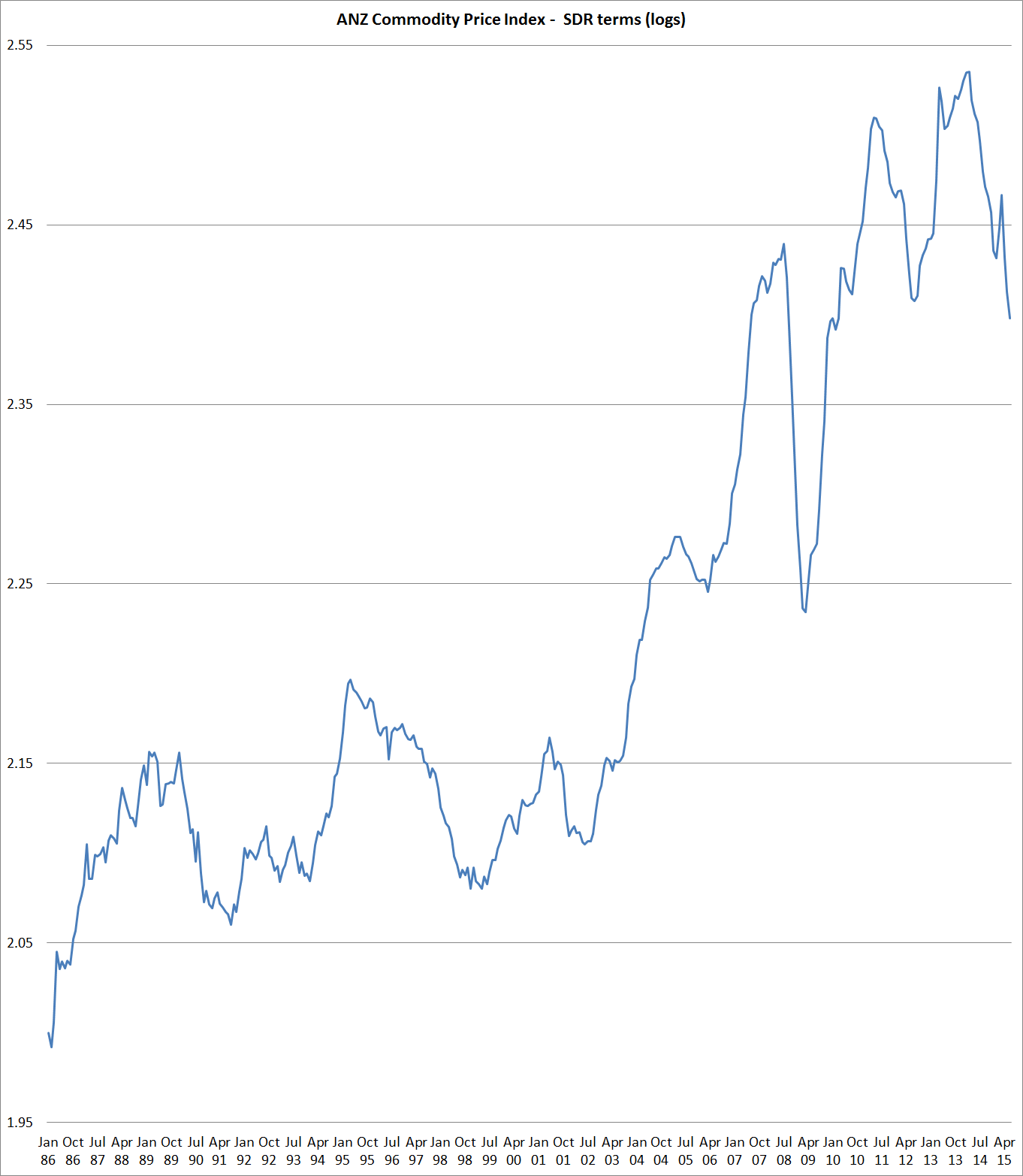

The ANZ Commodity Price Index, which lags behind (for example) falling GDT and futures dairy prices, has already had one of the larger falls in the history of the series.

Meanwhile, the fall in the exchange rate, while material, remains pretty small by the standards of past New Zealand adjustments since the float in 1985. At the moment, the adjustment is comparable to what we saw in the shortlived growth (and risk) scare in 2006.

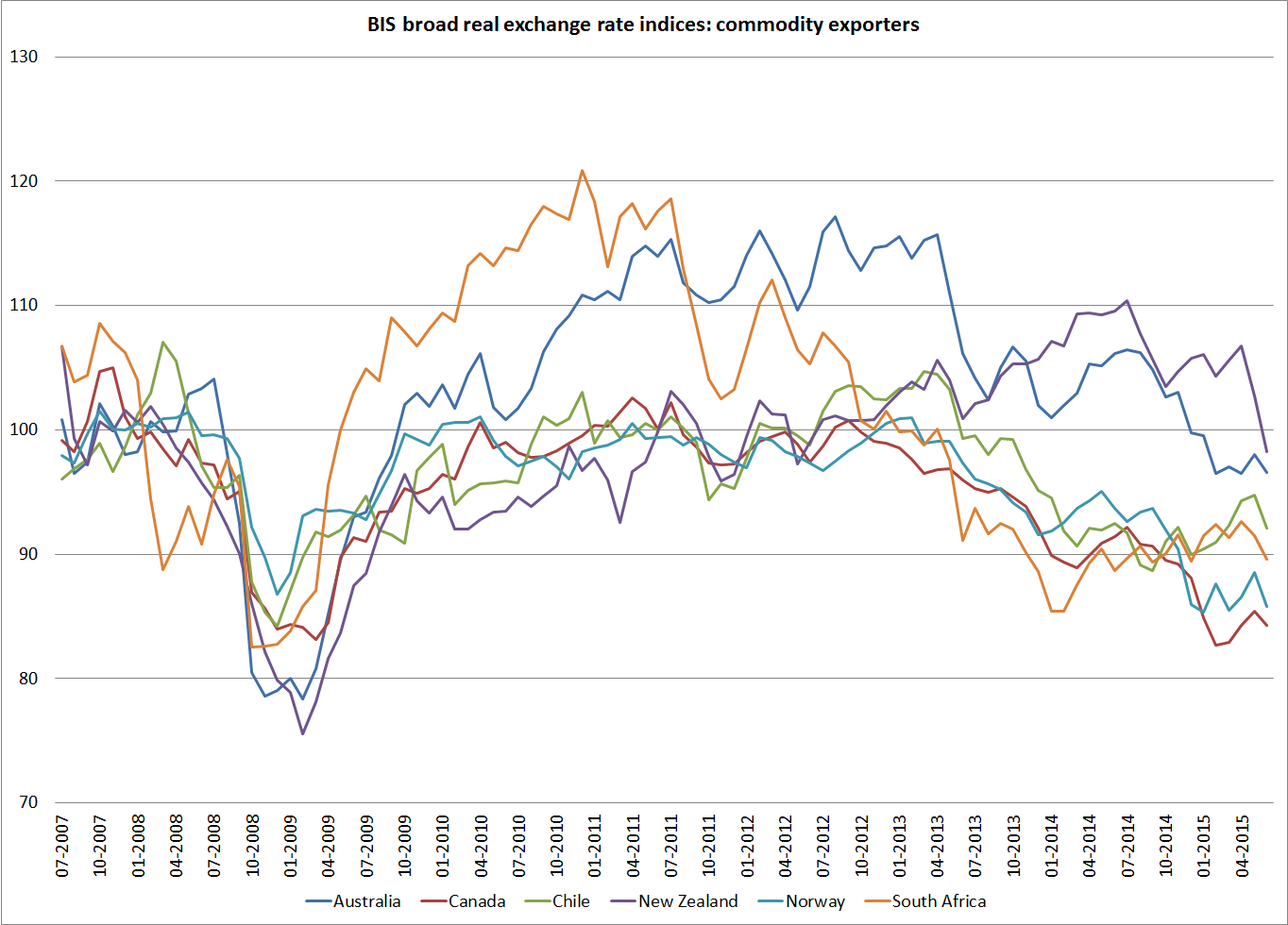

And here are the BIS real exchange rates for the five OECD commodity exporting countries, and South Africa. Each has experienced rather different commodity price pressures and opportunities. Here the exchange rates are each based to 100 at the average for each country in the year to June 2008 just prior to the global recession and crisis.

New Zealand’s exchange rate doesn’t stand out dramatically, but it remains higher, relative to pre-recession levels, than in these other countries. In part that is likely to reflect yield differentials. New Zealand is the only one of these six countries still to have policy interest rates higher than they were 18 months ago. That is Graeme Wheeler’s choice, and while data may eventually force him to change his view, it is his view that for now determines short-term interest rates on offer in New Zealand