I’ve been continuing to reflect on Graeme Wheeler’s repeated observation that New Zealand’s exchange rate “needs” to come down. I’m still not entirely sure what he means. The exchange rate is an asset price and presumably should reflect all expected future relevant information, not just spot information about current dairy prices. And the market has no particular reason to focus on stabilising the net international investment position at around current levels. Indeed, although it is a convenient reference point, neither does the Reserve Bank.

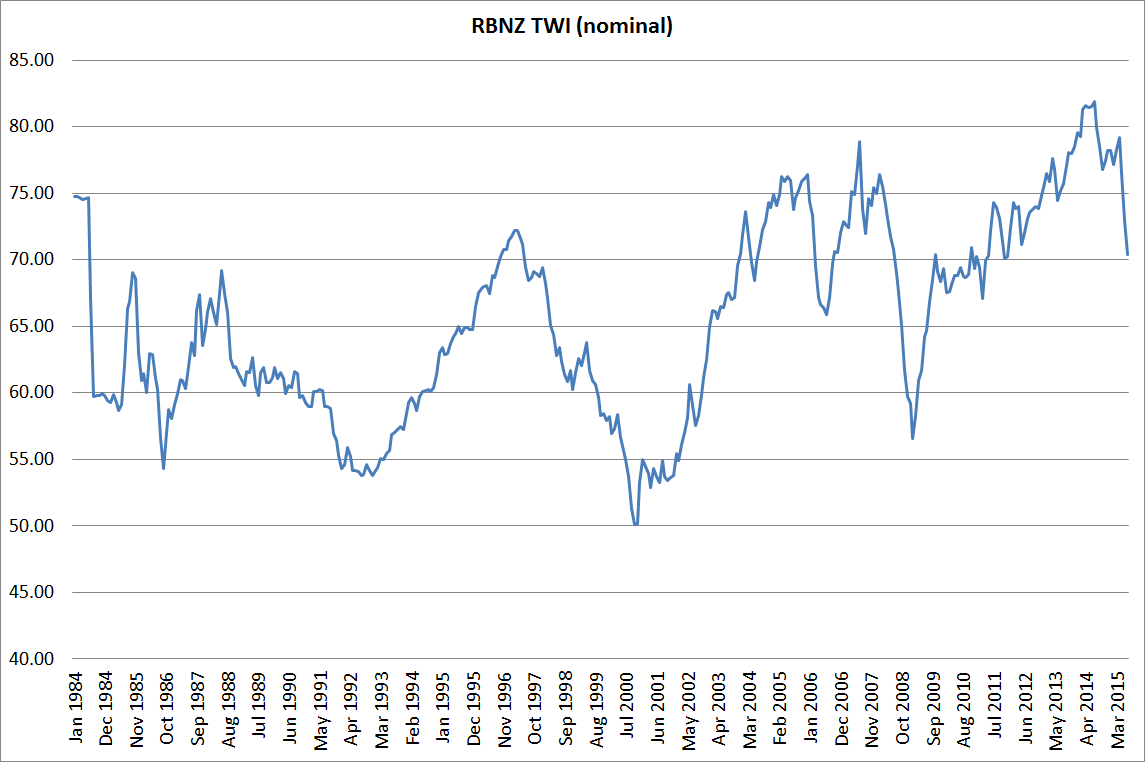

“Need” or not, I’d have thought it was likely that the exchange rate would fall further.

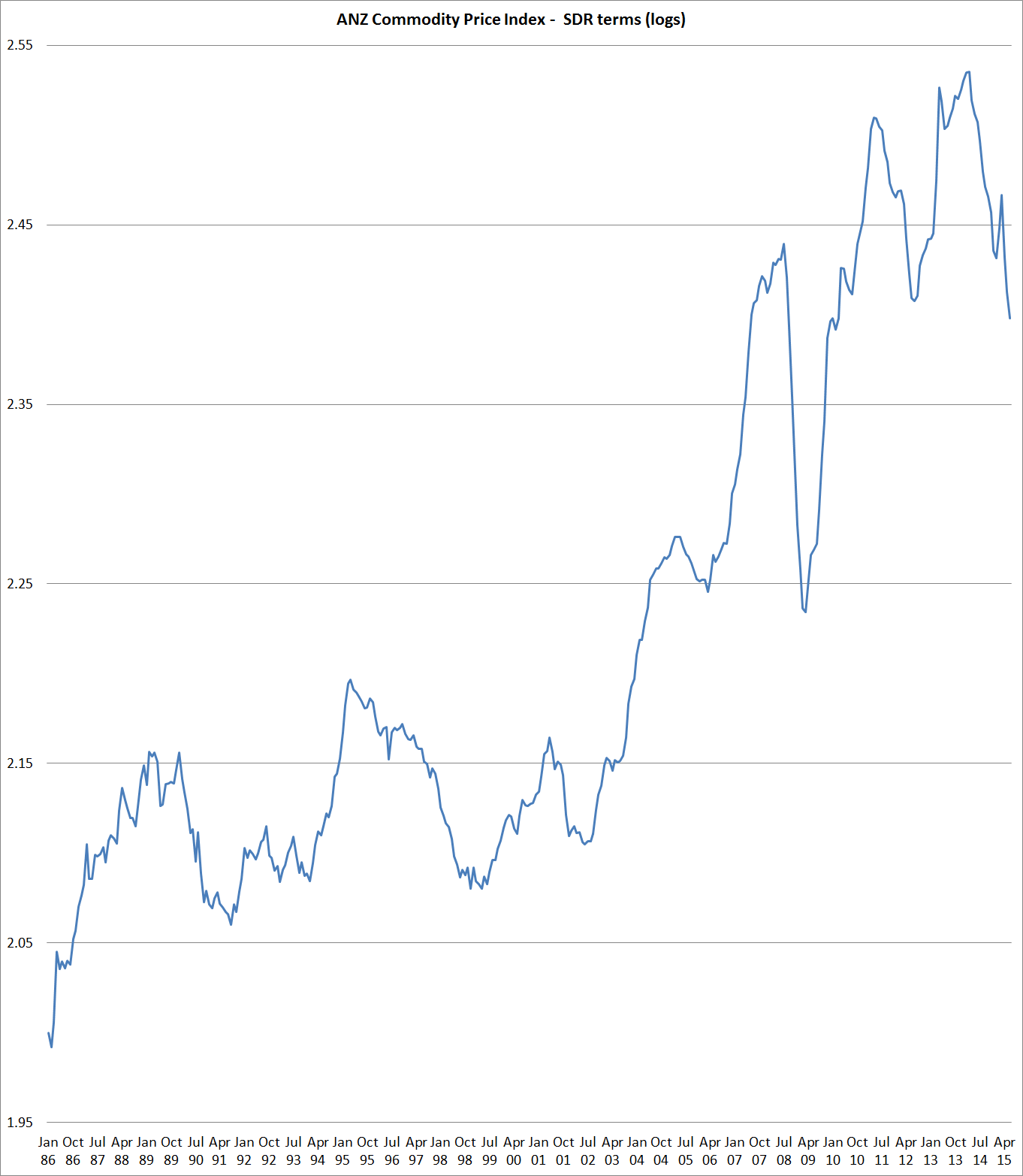

The ANZ Commodity Price Index, which lags behind (for example) falling GDT and futures dairy prices, has already had one of the larger falls in the history of the series.

Meanwhile, the fall in the exchange rate, while material, remains pretty small by the standards of past New Zealand adjustments since the float in 1985. At the moment, the adjustment is comparable to what we saw in the shortlived growth (and risk) scare in 2006.

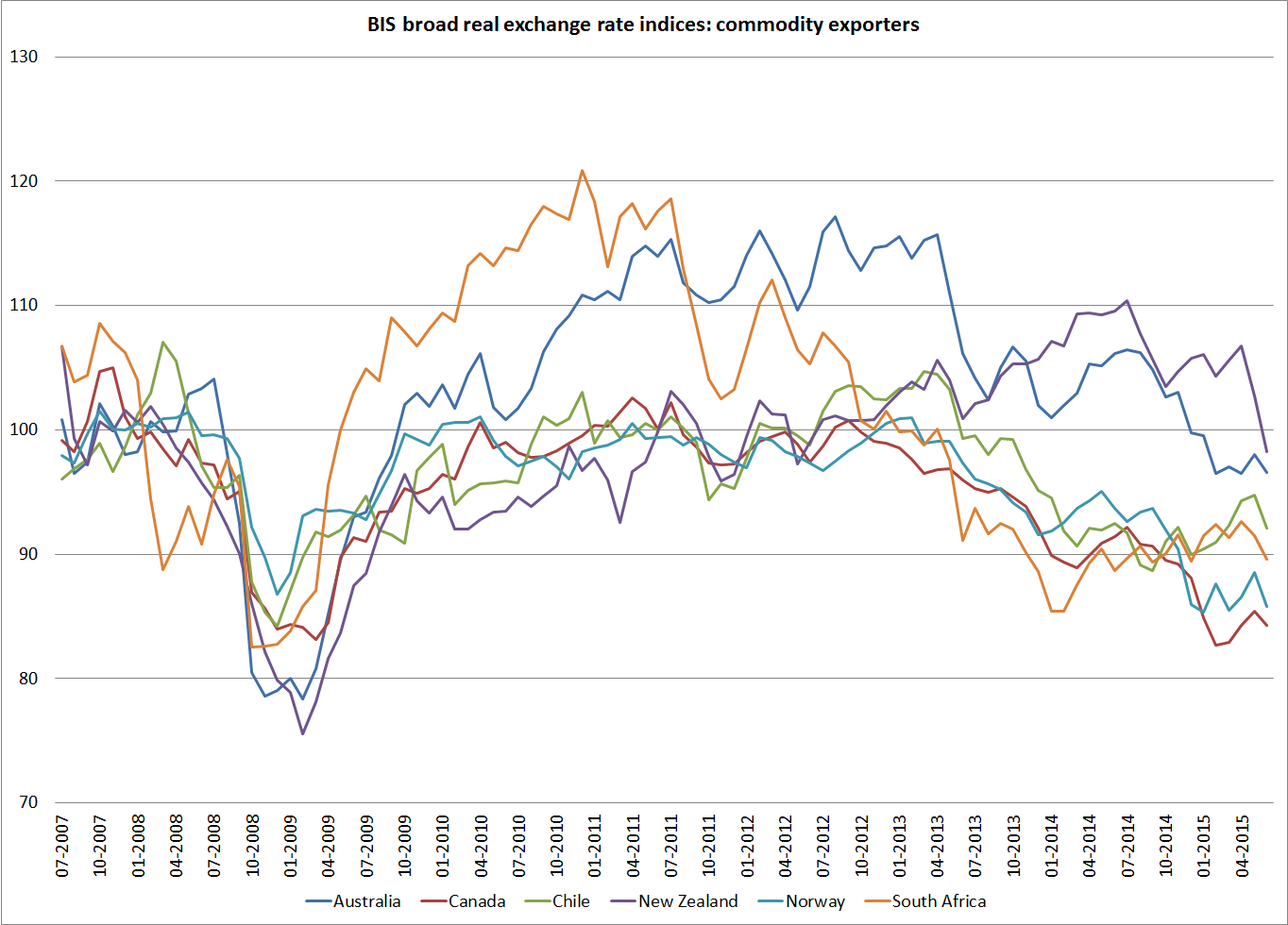

And here are the BIS real exchange rates for the five OECD commodity exporting countries, and South Africa. Each has experienced rather different commodity price pressures and opportunities. Here the exchange rates are each based to 100 at the average for each country in the year to June 2008 just prior to the global recession and crisis.

New Zealand’s exchange rate doesn’t stand out dramatically, but it remains higher, relative to pre-recession levels, than in these other countries. In part that is likely to reflect yield differentials. New Zealand is the only one of these six countries still to have policy interest rates higher than they were 18 months ago. That is Graeme Wheeler’s choice, and while data may eventually force him to change his view, it is his view that for now determines short-term interest rates on offer in New Zealand

Enjoying you blog. sometimes a bit techy for me jsut and average old Kiwi but always thought that our RBNZ was not well founded in what’s needed to be done. right from Brash Days,

Read Rodneys ravings for a longtime and again good stuff.

Today I read through this blog and considering the current debate thought it was rather instructive about currencies.

http://breakingviewsnz.blogspot.co.nz/2015/08/matt-ridley-icelands-lesson-for-europe.html

My future concern would be China because if it suits them and it could they will devalue at a time that suits them. They have a big population to keep happy and stable and if life gets tough they are not shy about acting in their own interests.20% could screw the scrum again for them

LikeLike

Thanks Robert. I suspect many of my old colleagues always thought I wasn’t technical enough. I’ll try to keep a bit of a balance.

I always enjoy Rodney’s pieces, altho I suspect he is wrong about monetary policy now, having been right about Bollard.

A Chinese devaluation, probably in their own national econ interests, would be a serious deflationary shock to the entire rest of the world.

LikeLike

My understanding is that China has purposely kept its currency covertly undervalued for a long time now, and an overt devaluation would probably lead to outright war with the US, especially if the latter was headed by a Republican.

Sometimes, living at the bottom of the ocean is not so bad.

LikeLike

Whether the yuan is over or undervalued is still disputed, but there has been a huge increase in the real exchange rate in the last decade, not matched by any apparent new surge in productivity growth. And the export share of China’s GDP has shrunk markedly, as the economy has become more reliant on a domestic credit fuelled investment boom. As that fades it looks to me increasingly as though a devaluation would be a normal policy response. But politics intrudes – the threat of countervailing actions, but also “pride” aspects such as the desire to have the yuan in the IMF SDR basket.

LikeLike

We should remember that china (like a few more countries in the pipeline), started from a very l;ow base and as you up that base each year the higher rates take more achieving. Japan was the same, Now Vietnam and so it goes, soon be some African turn as the big guys shift about for labour rates etc.

LikeLike