Having finished the last post, I flicked over to Kiwiblog and found a slightly flippant post, suggesting that Andrew Little’s comments about the dairy sector being in “crisis” could be safely discounted, in view of earlier Labour worries about the manufacturing sector having come to nothing. Indeed, on this take,

Their manufactured manufacturing crisis has seen record job growth in manufacturing.

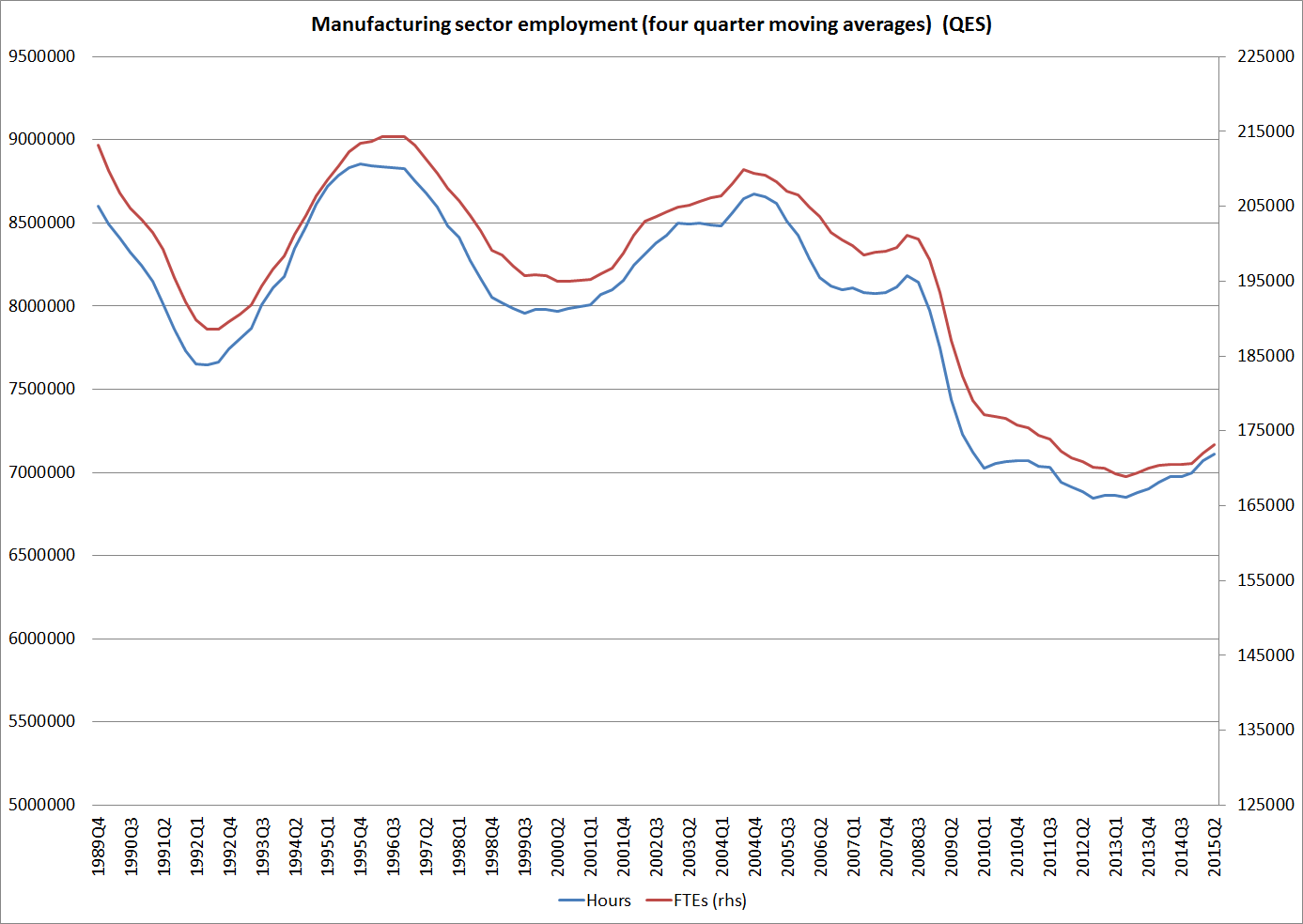

I don’t follow sectoral employment data closely, so presumed I’d missed something. Indeed, since much of manufacturing activity is a derived demand from construction activity (which has been very buoyant) and dairy processing makes up another component, and milk production has been growing strongly (even if agricultural value-added hasn’t), some strength in manufacturing employment sounded plausible.

But here is the chart of the Quarterly Employment Survey data, showing hours worked and number of full-time equivalent employees for the manufacturing sector as a whole. The QES is a survey of firms, and probably quite reliable for these sorts of questions.

Given the strength of construction activity over the last couple of years, these seems quite remarkably weak data.

The HLFS (a survey of individuals) has a shorter series, and only for the total number of employees. It has shown greater strength in the last few quarters, but even on this measure the numbers employed in manufacturing are still not up to pre-recessionary levels.

There is a long-running debate on the importance of manufacturing, both here and abroad. Here was my summary take from a couple of months ago.

I’m not one of those who thinks that the relative decline of manufacturing is a tragedy, but on the other hand I also don’t think that it is a matter of total indifference. Most likely, the relatively weak manufacturing sector performance in recent years, despite the buoyant construction sector, is a reflection of the persistently high real exchange rate. Like Graeme Wheeler, I think the real exchange rate is out of line with medium to longer–term economic fundamentals. A more strongly performing New Zealand economy, one making some progress in closing the gaps to the rest of the OECD, would be likely to see a stronger manufacturing sector. It might still be shrinking as a share of a fast-growing economy, but a manufacturing sector that has seen no growth at all in almost 20 years doesn’t feel like a feature of a particularly successful economy.

The weak manufacturing sector, despite the support from construction sector demand, seems to be yet another symptom of an underperforming New Zealand economy. If there were clear signs of rapid growth in investment and productivity in other parts of the tradables sector, we might reasonably be unbothered by the manufacturing numbers. As it is, I don’t think we can be that relaxed. And it isn’t a matter of targeting measures directly to boosting manufacturing, but about removing obstacles that have held up the real exchange rate (over decades), and which undermine the attractiveness of business investment across the economy as a whole.