The quarterly manufacturing survey came out this morning. Noticing that growth in the sector seemed to be levelling off I was curious as to how things looked relative to levels just prior to the recession.

As is well known, the manufacturing share of GDP has been falling for decades in most advanced countries. China, for example, has picked up a big chunk of global manufacturing, and services have become progressively more important everywhere.

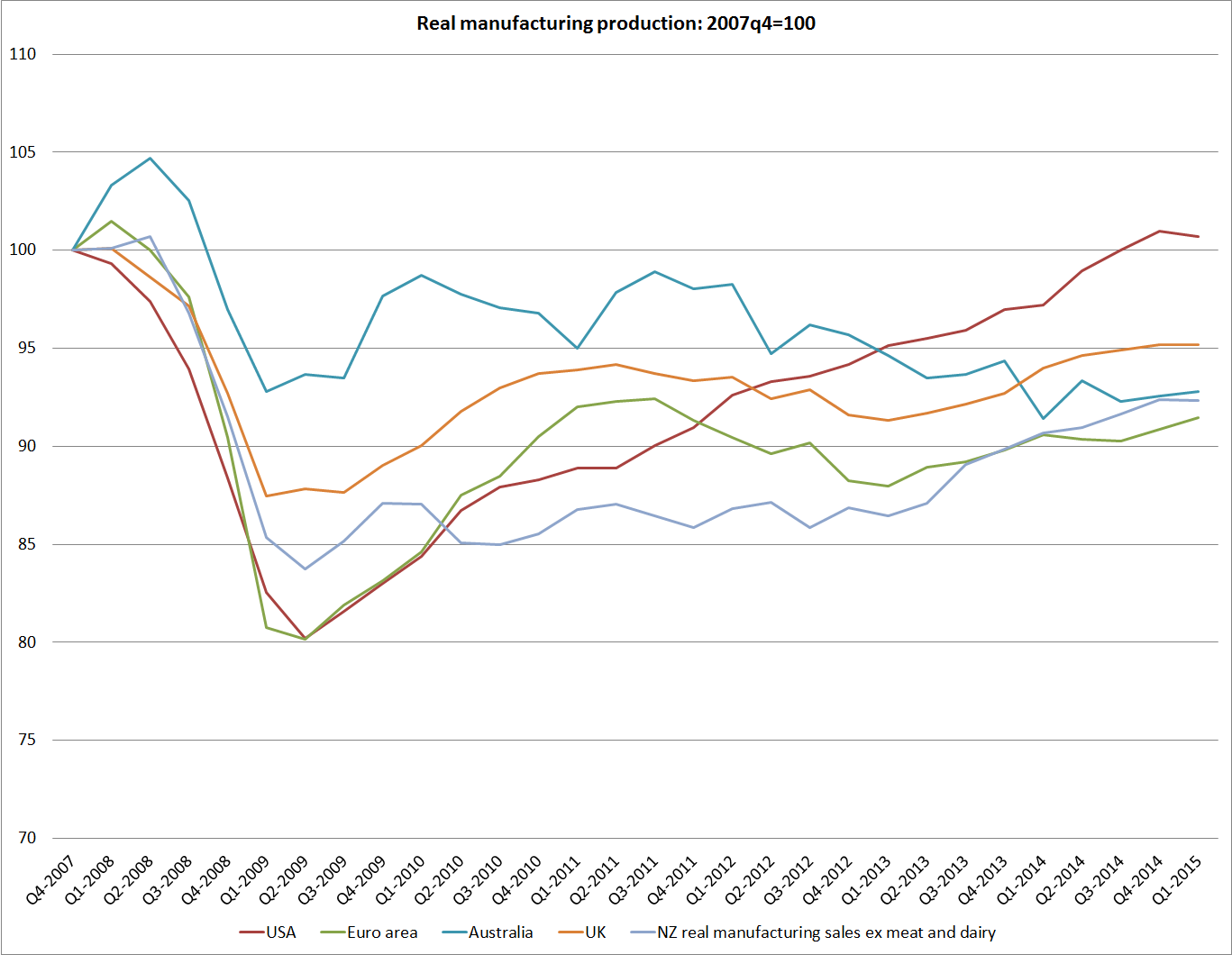

But this chart shows the volume of manufacturing activity (not as a share of GDP, not per capita, just the level) for a few countries/areas since 2007q4. For the other countries, it is OECD data, while for New Zealand I’ve used the volume of manufacturing sales ex meat and dairy (the rather less noisy series SNZ also publishes).

I haven’t been paying much attention to these data in the last year or two, but I was interested how far below 2007 activity levels New Zealand manufacturing still is. As previous Reserve Bank work pointed out, once one strips out meat and dairy, a lot of the activity in New Zealand manufacturing is a derived demand off the back of construction-sector activity. And the construction sector here has been pretty robust, particularly on the back of the huge volume of work in Christchurch.

But I was also somewhat sobered by how similar the path of manufacturing activity has been in New Zealand and in the euro-area as a whole. Note that these are not per capita measures, and euro-area population is pretty flat while ours has risen 6 per cent of so since 2007.

The US performance looks relatively good, but in fact is still slightly less good than (flat to falling population) Germany.

I’m not one of those who thinks that the relative decline of manufacturing is a tragedy, but on the other hand I also don’t think that it is a matter of total indifference. Most likely, the relatively weak manufacturing sector performance in recent years, despite the buoyant construction sector, is a reflection of the persistently high real exchange rate. Like Graeme Wheeler, I think the real exchange rate is out of line with medium to longer–term economic fundamentals. A more strongly performing New Zealand economy, one making some progress in closing the gaps to the rest of the OECD, would be likely to see a stronger manufacturing sector. It might still be shrinking as a share of a fast-growing economy, but a manufacturing sector that has seen no growth at all in almost 20 years doesn’t feel like a feature of a particularly successful economy.

Using the same data series as above, I had a look at what has happened since 1995q1. Six OECD countries have had weaker manufacturing sector activity than New Zealand. At least three are current cyclical basket cases (Spain, Italy and Greece), and the gap between the growth rates in manufacturing volumes and in population has been weaker only in Italy, Spain, and France.

Numbers like this certainly don’t suggest immediate policy remedies, but they probably should continue to prompt thinking about just what explains New Zealand’s disappointing economic performance.

| Growth 1995 to 2015 | ||

| Manufacturing | Population | |

| Italy | -17.6 | 7.8 |

| Spain | -10.7 | 20.2 |

| France | -5.3 | 11.3 |

| Greece | 0 | 3.3 |

| Japan | 0.2 | 1 |

| UK | 1.6 | 9.9 |

| New Zealand | 4.3 | 22.7 |

I think it has to do with the life cycle of the firm. If you imagine a manufacturing startup, initially it has no distribution, no brand and no economies of scale. Initially it sells in the small domestic market, but as it grows it begins selling into the deep global market, getting economies of scale and enabling it to invest in the branding and tied distribution networks from which pricing power (and by extension productivity) derives. In NZ, apart from a few very common items like building materials, the domestic market for specialist products is tiny, so the need to export comes very early on. But if the exchange rate is above fair value, the startup has no cost advantages to overcome its lack of scale and branding, and so it can’t get past the domestic market stage. (I am talking here to this post and the previous posts on productivity).

LikeLike