As people often point out when I run charts like those in yesterday’s post, real or volume measures of value-added are all very well, but they don’t capture the direct effects of fluctuations in the terms of trade. We can spend what we earn, and what we earn is a combination of volume and price.

For some purposes, ignoring the terms of trade effects can be more useful. After all, a country like New Zealand is exposed to quite volatile terms of trade, and those terms of trade are almost wholly outside our control, year to year. Some firms probably have price-setting power in world markets, and there is some evidence that New Zealand droughts have a short-term impact on world dairy prices, but our overall terms of trade are largely beyond our control. By contrast, productivity measures (labour or multi-factor) are about what New Zealand (firms) do with the hands we are dealt, and the opportunities we make for ourselves. It is exceptionally rare (probably unknown) for countries to get sustainably rich just – or even primarily – on changes in the terms of trade.

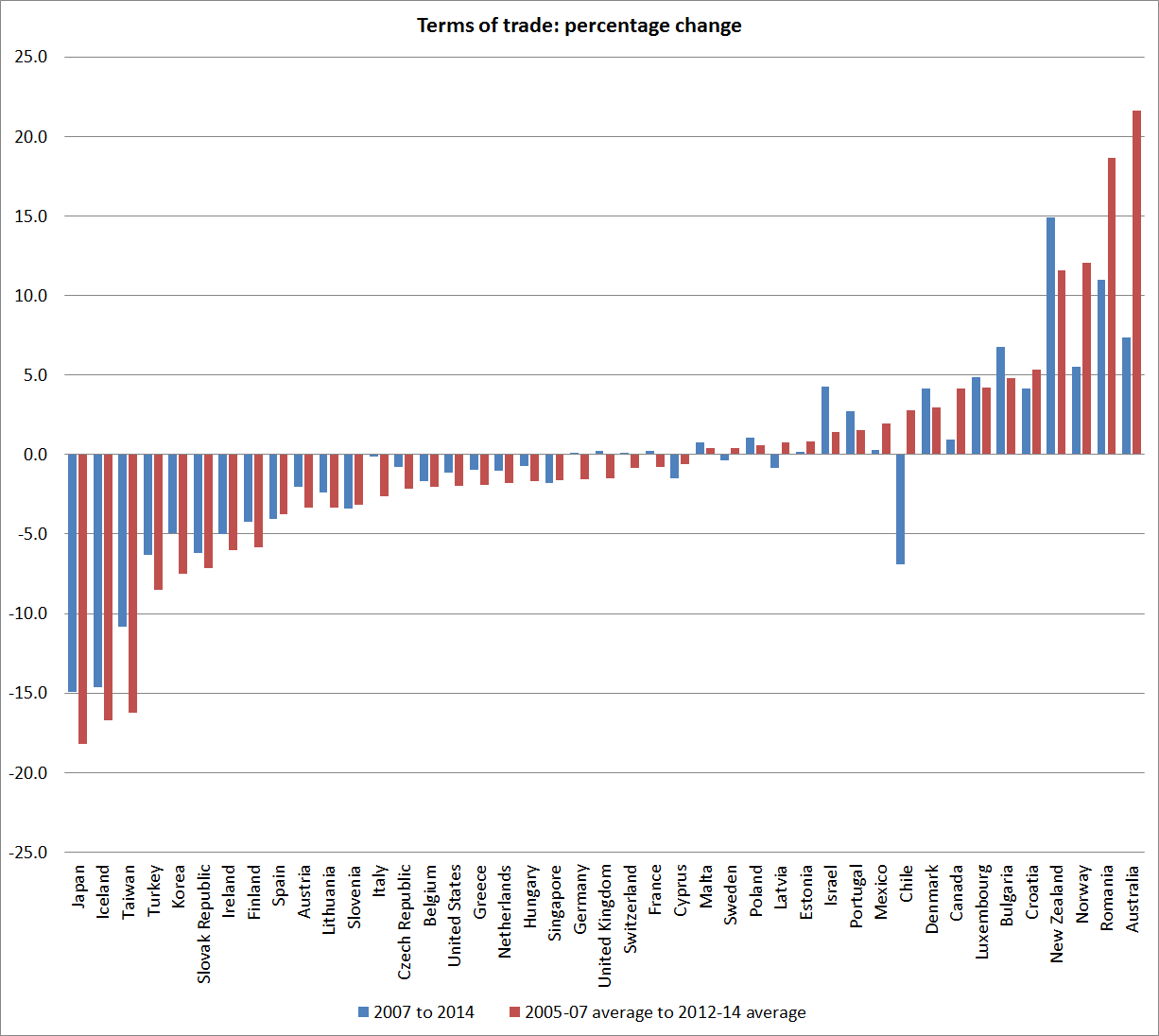

But New Zealand’s terms of trade have done quite well over the last decade or so, reflecting a combination of falling real import prices and good prices, on average, for dairy products in particular. Here is one chart showing changes in the terms of trade for the 43 advanced countries I discussed yesterday. There are two different cuts here: the percentage change from 2007 to 2014 and the percentage change from the average level for 2005-2007 to the average level for 2012-2014. On both New Zealand shows up as having done well. Indeed, on the measure from 2007 to 2014, we’ve had the largest increase in the terms of trade of any of these countries (no doubt it will fall back somewhat in 2015).

How much difference does the terms of trade make? Well, we export and import amounts equal to around 30 per cent of GDP, so a 15 per cent boost to the terms of trade is roughly equivalent to an increase of another 5 percentage points, on top of any growth in the volume of output. That is certainly a useful boost, but if you look at the first chart in yesterday’s post, it is hardly enough to dramatically transform our ranking. Looking at the terms of trade does not materially alter the story of how disappointing our overall economy performance has been since 2007.

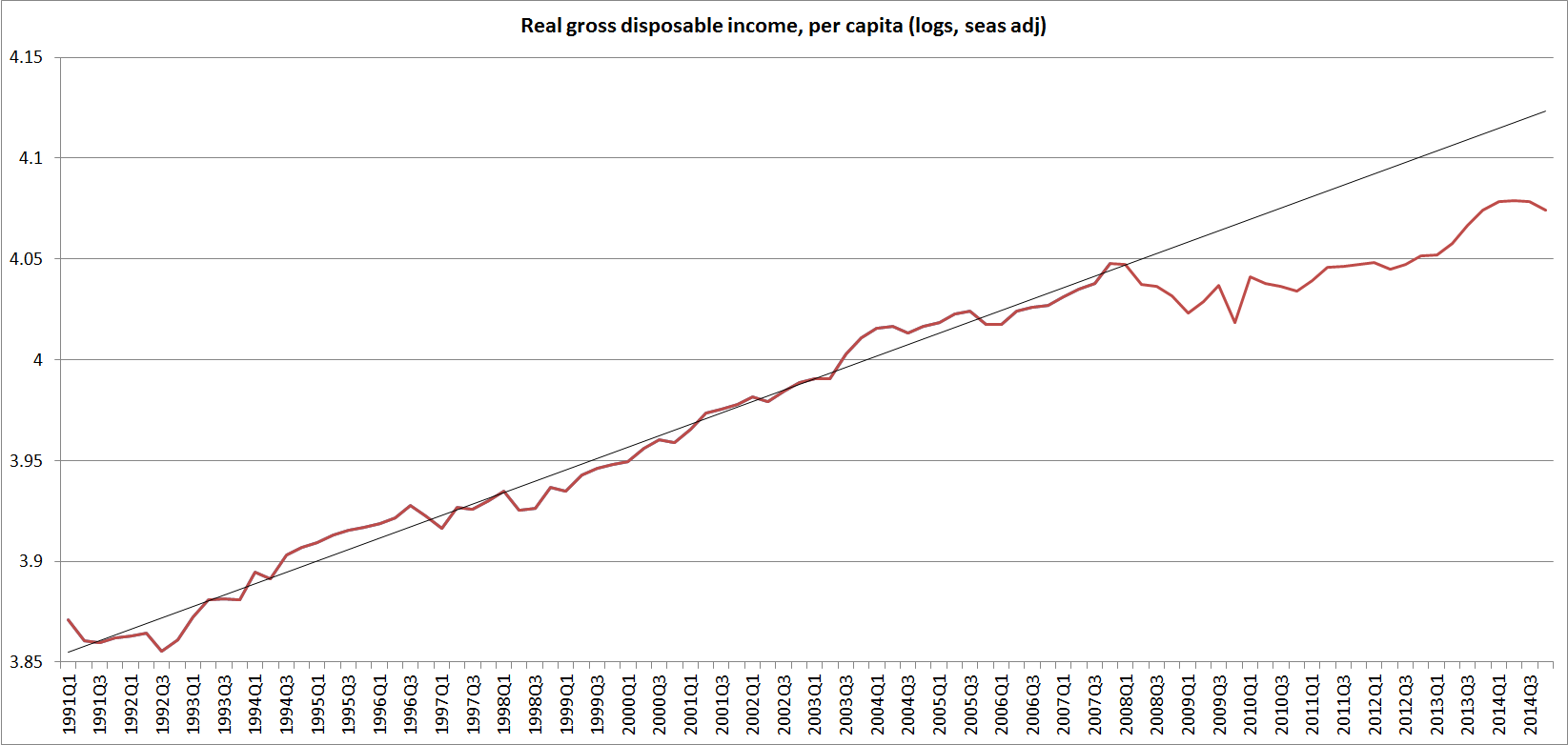

Statistics New Zealand produces a series of per capita Real Gross Disposable Income. This series tries to estimate New Zealanders’ real purchasing power. It takes account of both the direct effects of the terms of trade, and of changes in how much of what is produced here has to be paid to foreign providers of (mostly) capital. Over the period since the recession New Zealand has enjoyed a strong terms of trade, and low interest rates – as a country with a high level of external debt, we had an unexpected lift in purchasing power as the servicing costs of that debt fell sharply and stayed low.

Here is a chart of that RGDI series. At present, RGDI per capita is still around 15 per cent below where it would have been if the 1991-2007 trend had continued.

So far I’ve focused on the direct effects of the terms of trade. But it is a little surprising that the strong terms of trade, boosting incomes and relative prices, has not provided more of a boost to real activity in the economy. A rising terms of trade (and especially an unexpected lift) would typically be expected to stimulate business investment: higher prices for the goods and services New Zealand firms sell will encourage more investment in those industries. As Daan Steenkamp has illustrated, the terms of trade boom in Australia helped prompt an enormous surge in business investment, which had no counterpart in New Zealand. Of course, our exchange rate has been very strong, which might have offset much of any additional incentive to invest in the tradables sector in aggregate. But the higher incomes (higher real purchasing power) might still have been expected to generate a significant boost to investment in the non-tradables sector. We haven’t seen much sign of it.

As I’ve noted before, if the lift in the term of trade proves quite short-lived it might prove to be a boon that there was not an investment boom, putting in place long-lived projects on the back of a temporary lift in relative prices in our favour. But most observers do not seem to expect New Zealand’s terms of trade gains of the last decade to fully unwind.

So I’m still puzzled as to why New Zealand has not done better given the very favourable terms of trade. At the margin, overly tight monetary policy in the last few years has not helped. And one other factor is the role of the Canterbury earthquakes and the associated repair and rebuilding process. As the Reserve Bank recognised right from the start, this represented a major non-tradables shock, and all the more so because most of the cost was being covered by offshore reinsurers. Real resources had to be devoted to the work in Canterbury, and for the most part we New Zealanders did not have to save more to pay for the work (we’d already paid the insurance premia). Real resources – especially labour – can’t be used for two things at once. Without the earthquakes and the subsequent repair process, those resources would have been freed up for other uses. Lower interest rates would have been likely to have resulted in a lower exchange rate, improving the attractiveness of investment in New Zealand’s tradables sectors.

Is it enough to explain why New Zealand has not done better? I don’t really think so, but the impact of the earthquake is certainly one constraint on New Zealand that Australia has not faced, and may be one reason why we have done less well than Australia on most measures since 2007.

Michael,

When I tested the effect of TOT on investments in NZ I found none. I am not puzzled. We can explain all that. If interested see, W A Razzak, “An Empirical Study of Sectoral-Level Investments in New Zealand,” Journal of Reviews on Global Economics, 2014, 3, 140-155. (Open access). In another forthcoming research we show that most of our growth is due to TFP, which is a good growth in my view. Australia’s growth is due to growth in factors rather.

LikeLike

Thanks Weshah. An interesting empirical result, but still a little surprising in my view. How does one take full advantage of a favourable change in relative prices if not by increasing investment? But, as you say, it hasn’t happened in NZ. I agree that TFP is good, and sustainable growth, so it is only shame ours has been so lousy over 45 years!

LikeLike

The effect of TOT shocks on investment then investment effects on GDP seem to take a long time. If projects are large and require a lot of capital then it might take a very long time for capital stock to change. TFP, at the sectoral level, country level, and global TFP affect investment in NZ. Even though most of our growth comes from TFP growth, our TFP growth has been relatively slow and that is why we have a relatively lower GDP per capita growth. I do not think TOT shocks affects GDP growth, if it does it takes a very long time perhaps.

LikeLike