Terry Hall’s column in the Dominion-Post this morning is headed “Auckland housing ‘bubble’ has worrying shades of 1987”.

This just seems wrong. Following 1987 New Zealand experienced a pretty severe financial crisis in which many corporates collapsed, and several major financial institutions either collapsed, or had to be bailed out by shareholders (including, in the BNZ’s case, the government).

It came, as financial crises typically do, on the back of several years of extremely rapid credit growth, far outstripping the rate of growth in incomes (or nominal GDP). Private sector credit growth exceeded 30 per cent per annum for several years (charts here) It was an environment of debt-fuelled craziness, of a massive commercial construction boom, and credit extended to “investment companies” with, it seemed, nothing behind them either than the hope-and-credit-fuelled values of other investment companies. Claims were heard that New Zealand had a comparative advantage in takeovers. Newly deregulated New Zealand and Australian lenders seemed to have few disciplined skills in credit or analysis, and as happened in several other countries at around the same time (eg the Nordics) it ended badly.

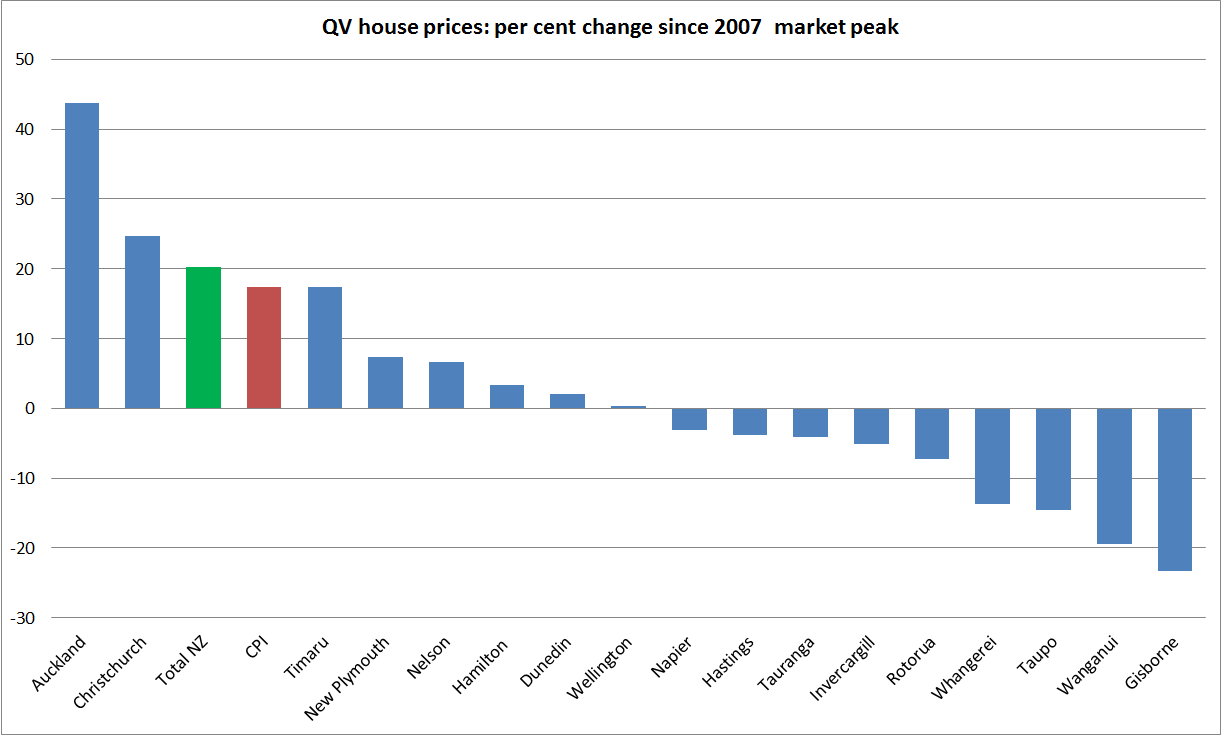

Take the current situation by contrast. Yes, Auckland house prices are a social and political scandal, but they seem quite easy to explain on the basis of some simple fundamentals: restricted effective supply of developable land on the one hand, and rapid population growth (fuelled by cyclical differences between here and Australia, and an aggressive government programme of inward migration). Where that combination of pressures isn’t apparent (which is most of the rest of the country) there is no particular or unusual upward pressure on house prices. Indeed, in large parts of the country real house prices are lower than they were in 2007, the peak of the previous boom and just prior to the recession.

It is difficult to think of a serious or systemic financial crisis anywhere that has not been preceded by rapid credit growth. There may be exceptions – and I’ve urged the Reserve Bank to document those cases for us, if they can find them – but it is wise for regulators (and investors/shareholders) to be more uneasy than usual when credit is growing rapidly. In those environments, lending standards tend to drop, and poor quality borrowers too readily get credit for propositions that won’t look good in the cold light of day. But if credit growth is subdued, and has been for some years, the risk of any sort of financial crisis is likely to be very small. In a New Zealand context, a prudential regulator might reasonably have been worried in 2007. As it happened, without cause: despite very rapid credit growth in the preceding years, bank lending decisions turned out to have been pretty robust. Funding structures were a different matter.

But what is the situation now?

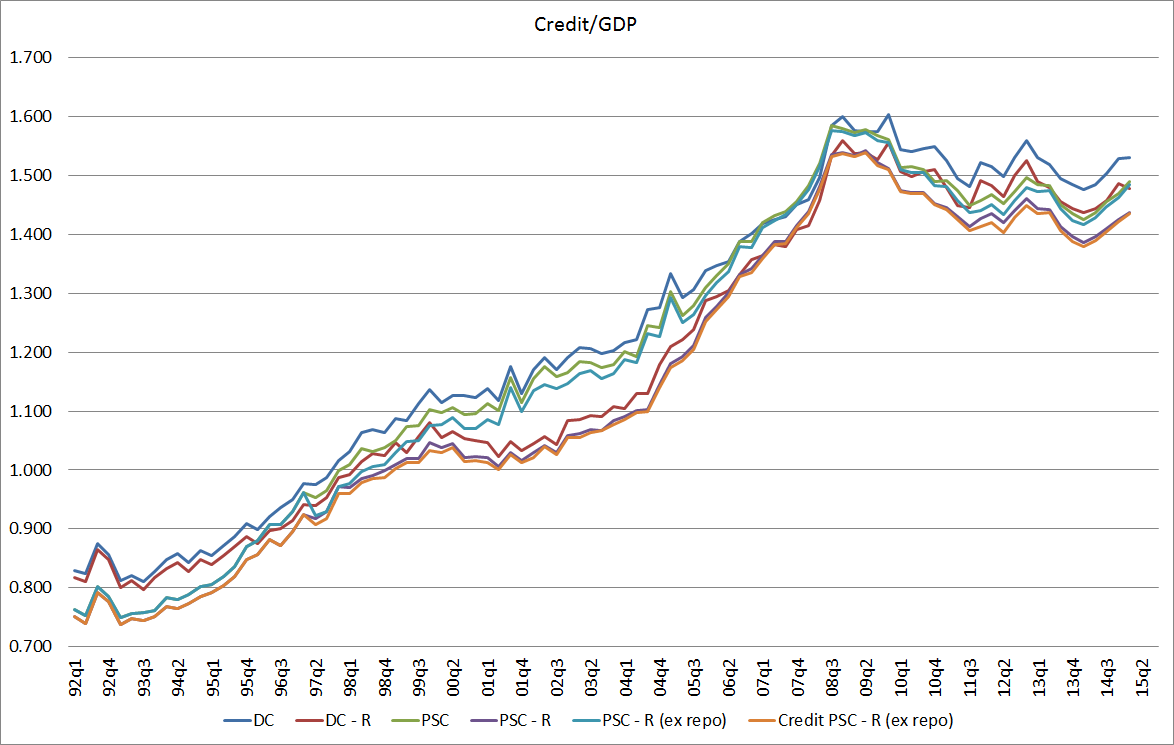

The Reserve Bank has six credit aggregates on its website. Each has its advantages and disadvantages, but the overall picture is much the same whichever one one looks at. This chart shows all six, as a ratio to nominal GDP, up to March 2015 (I’ve included a guess for nominal GDP growth in March quarter). Credit to GDP peaked back in 2008, and in the seven years since then has shown no hint of moving to new peaks. Given the sharp upward trend over the 15 or so years prior to 2008, this is a huge change.

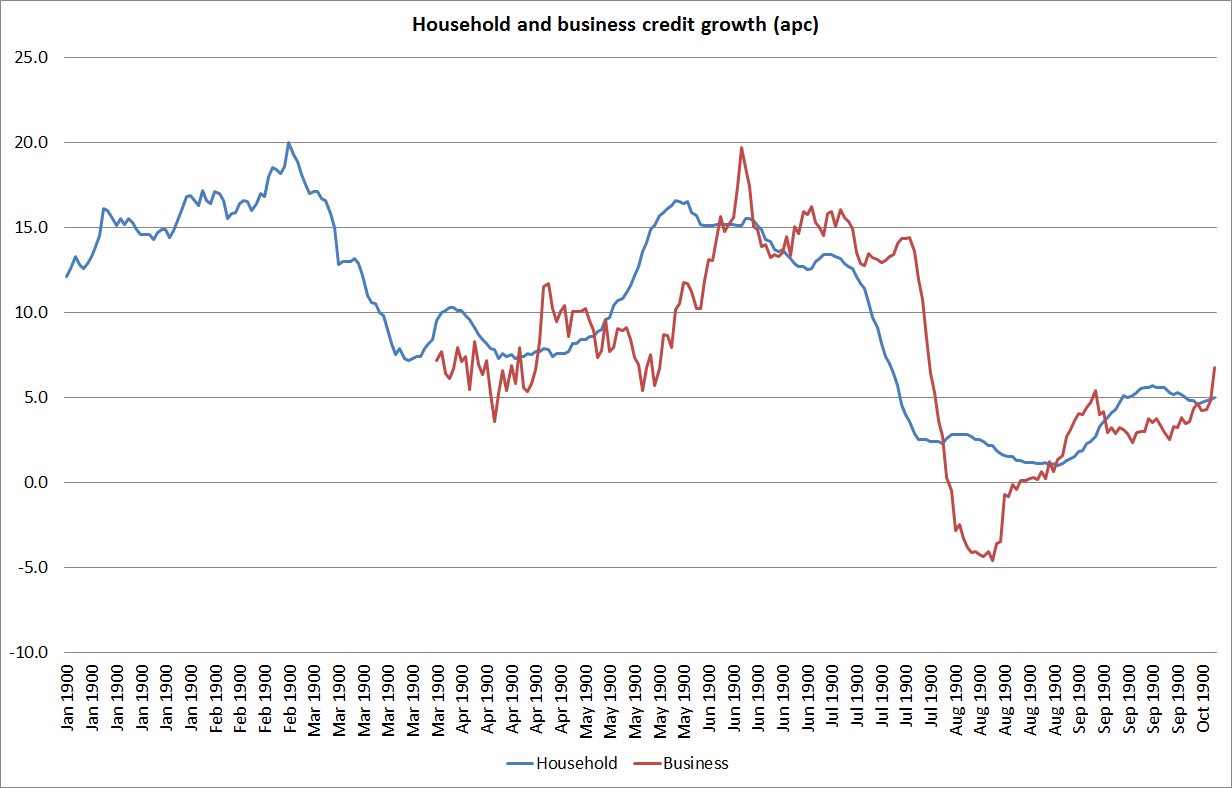

And what of annual growth. This chart shows lending to households and the businesses (the latter including agriculture). Lending growth to households has only been materially lower than it is now during the 2008/09 recession.

And it is often forgotten that there is still momentum behind the stock of household credit as a result of the increase in house prices last decade. Houses don’t turn over that frequently and many properties being purchased today, in parts of the country with little or no new house price inflation, are being bought at prices higher than the vendor bought the house for (and took a mortgage for) perhaps 10 or 20 years ago.

For the current situation, consider the volume of new mortgage approvals – in recent months running below last year’s level, and well below levels seen in the boom years.

All of which brings us back to the Reserve Bank’s own stress test, reported in the last Financial Stability Report. This was the most interesting scenario

In scenario A, a sharp slowdown in economic growth in China triggers a severe double-dip recession. Real GDP declines by around 4 percent, and unemployment peaks at just over 13 percent. House prices decline by 40 percent nationally, with a more marked fall in Auckland. The agricultural sector is also impacted by a combination of a 40 percent fall in land prices and a 33 percent fall in commodity prices. The decline in commodity prices results in Fonterra payouts of just over $5 per kilogram of milksolids (kg/MS) throughout the scenario.

And this was the result

Higher credit losses, combined with a decline in net interest income due to increased costs for bank funding, resulted in a significant decline in bank profitability. However, reflecting strong underlying earnings in the New Zealand banking system, these factors were only sufficient to cause negative profitability in a single year in each scenario

A repeat of 1987 is just not remotely in prospect at present. If bank balance sheets start growing rapidly it might be time for some more concern, but at present issues around Auckland housing should be seen for what they are – the outcome of policy blunders in which restricted supply runs into rapid population growth – rather than any sort of material threat to financial or macroeconomic stability.

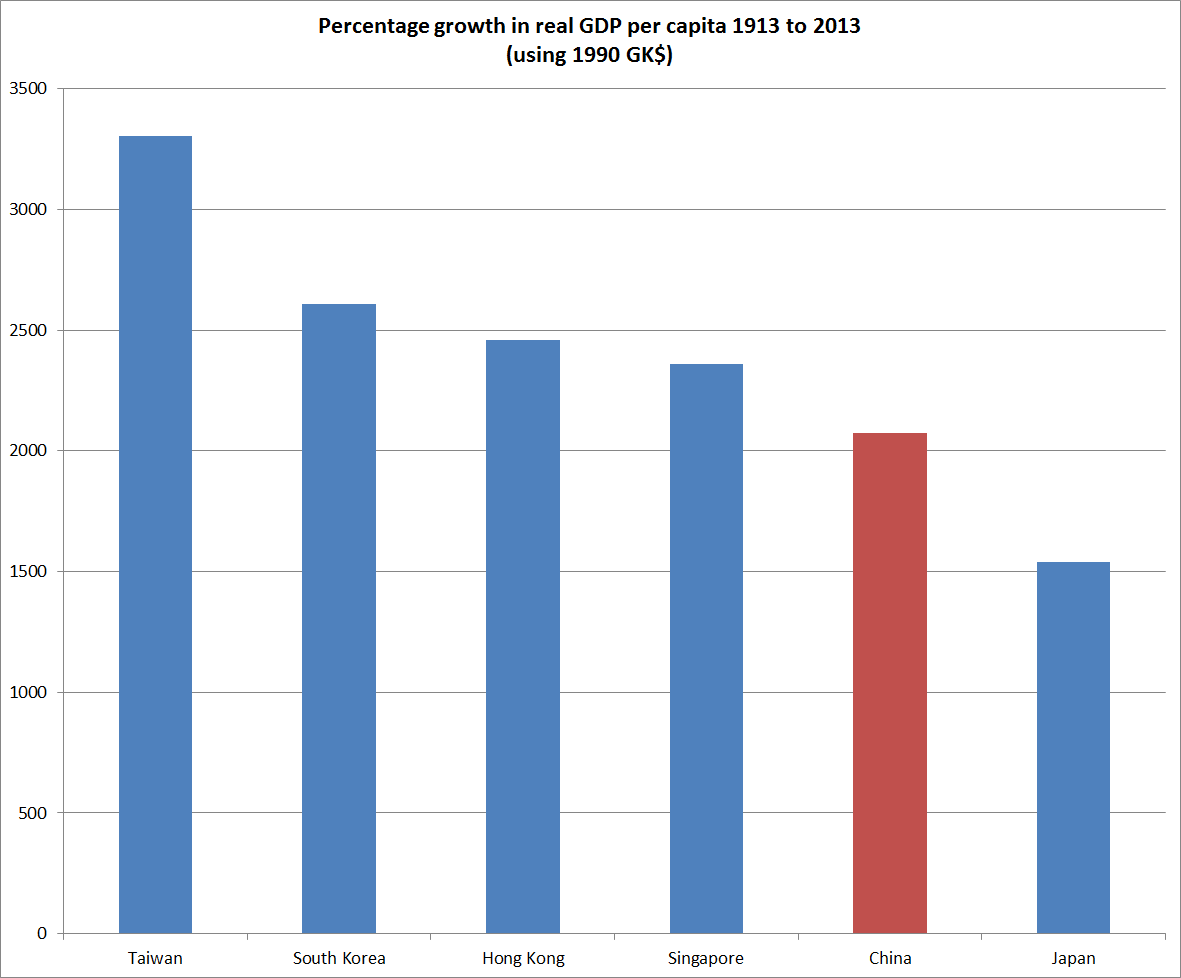

I also noticed Liam Dann’s column in the Herald on a similar topic – the headings are so similar the two papers could be sharing sub-editors. Dann is clearly very influenced by his recent trip to China, with his explicit hankering for new controls and restrictions. It is worth remembering not just that China is coming off a huge government-fuelled credit boom – outstripping anything ever seen in New Zealand, even in the heady pre-1987 period – but also that the People’s Republic of China remains the outstandingly poor performer of the group of Chinese economies in East Asia. Over the long haul it is an underperforming middle income country with few or no policy lessons for New Zealand.

Love the last chart. When was the last time someone wrote an article on what the Taiwanese have done right?

The first chart begs the question, why only Auckland? Perhaps immigrants are just ignorant of the rest of the country. But I suspect there are better paid and more interesting jobs in Auckland.

LikeLike

International experience is that immigrants disproprtionately gravitate towards existing big cities (be they London, New York, Vancouver, Sydney/Melbourne or Auckland) for a variety of reasons: many will have come from big cities abroad (typically bigger than Auckland); they are more likely to find people (and food/restaurants etc) from their home country/culture, and of course the econ opportunities are probably better too. I think people are fooling themselves when they talk about trying to steer migrants to other cities: either we accept that with current migration levels Auckland becomes more and more dominant, or we cut the target inflow. Reasonable arguments can be made for either approach, but if we choose to keep the high target migrant numbers something really transformative needs to be done about housing supply restrictions.

LikeLike

I agree. The only way I can think of to create population growth outside Auckland would be if a special economic zone were tried, perhaps in Northland or Bay of Plenty. I don’t know if this has ever been seriously looked at.

LikeLike

The first question which jumps out at me from the first graph, is ‘what is driving the increase in attractiveness of Christchurch and Auckland at the expense of the rest of NZ’?

This effect is just as obvious in Australia; capital cities growing at the expense of regional cities. Notionally I know people talk about increased economic returns from intellectual capital, and perhaps that’s true. But I haven’t seen anything which really convinces me – in particular why that effect would have become more pronounced in the last generation.

LikeLike

Sorry, just re-read the comments above. Reading back through the response there, I’d reiterate my original comment. Why the recency of the capital city phenomena?

LikeLike

My guess is it has to do with the Credit/GDP graph above, ie the increased financialisation of the world economy. So wealth is produced in the regions in the form of real goods but accumulates in the major cities in services and banking.

LikeLike

Michael.

Very presicent of you to project growth from 1913 for 190 years out to 2103 in your final graph.

Surely we are just a bit past the middle of that range?

Population growth differences matter as well.

China’s will slow markedly in coming years.

LikeLike

Oops

Re population, China had the slowest population growth of any of China, Taiwan, Singapore, and Hong Kong over the last century.

LikeLike

Hi Michael:

Could you outline why you think out-of-control credit is *necessary* for an asset bubble? This theme underpins this and your previous posts on the topic. Credit expansions have often coincided with asset bubbles, but not always. Credit expansion is not usually part of the NASDAQ bubble narrative, for example.

BTW, I agree with the main point of your post – that it isn’t 1987 again.

LikeLike

Ryan

I wouldn’t say that it was necessary for an asset bubble, but empirically/historically, it has been necessary for a systemic financial crises to result from a bubble. In principle, people could certainly bid the price of an asset ever higher, without any credit being involved. When that “bubble” popped, it might be painful for the individuals left holding the asset (Impressionist paintings, tulip bulbs?) but wouldn’t be for the financial system as a whole.

In practice tho, the two often go together: for “bubbles” in widely-held (and reproducible) assets to run on for long there is almost inevitably credit involved, and if the bubble mood is pervasive (as it felt in NZ in 86/87?) it is likely to affect all sorts of decisions across the economy, including bank lending standards. Banks won’t think they are taking crazy risks – rather they will think risk has gone away – and they only find out much later that things weren’t so different after all.

Re NASDAQ, I guess that is a fair point, and of course the 2001 recession was a reasonably mild one.

Michael

LikeLike

Hmm, you may be being a bit complacent there. Yes, I agree there is not the level of stupidity about in New Zealand as there was before previous crises, but:

1 The level of indebtedness has doubled over the period of your Credit/GDP graph, which presumably means the level of risk has gone up much more (four times?) as these things seem to follow some sort of power law.

2 The next event will probably be triggered by an overseas event, as were previous crises. This graph gives serious pause for concern: http://www.advisorperspectives.com/dshort/charts/markets/nyse-margin-debt.html?NYSE-investor-credit-SPX-since-1995-inverted.gif.

LikeLike