The Reserve Bank Monetary Policy Committee works to a “Remit” set down for them from time to time by the Minister of Finance (the current one is here). It is a different (and better) system than the previous approach of Policy Targets Agreements between the Governor and the Minister, and in particular makes it clear (as is appropriate in our system of government) that the (elected) Minister and government set the targets for monetary policy, while the MPC is the accountable (at least on paper) body responsible for setting monetary policy to deliver the government’s goal.

Under the Reserve Bank Act the law now reads

And several weeks ago the Bank kicked off the first stage in a consultative process designed to inform the advice they will eventually provide to the Minister of Finance. If you want to have a say, submissions close next Friday (15th).

Consultation with the public (of some sort or other) is required by law.

The idea of this sort of five-yearly review appears to have been drawn from the Canadian process, where in the lead-up to the five-yearly review of their inflation target the Bank of Canada has done a huge amount of analytical work reviewing the issues and options. Now, Canada is a much bigger country than New Zealand – but it is still one country, with its own set of specific experiences and issues – but the range of material they have put out, and research they have undertaken, is typically very impressive. Here is the link to the most recent review, and here specifically the link to the 24 formal research papers.

By contrast, what we have seen so far from the Reserve Bank of New Zealand is a pale shadow. There is a 60 page document, but lots of graphics, but there is no fresh analysis or research at all. It is possible that this first round consultation is designed simply to draw out the questions people think should be looked at more closely, but even if so that doesn’t leave much time before the second stage of the consultation is due (I think they said October or November). It really doesn’t look as though they have in mind doing much, if any, fresh research, whether commissioned or by their own staff. Against the backdrop of some of the biggest disruptions to monetary policy in the 30+ year history of inflation targeting, that suggests a lack of real seriousness about the review. Perhaps the Minister has already suggested (see 5(2)(c) above that he isn’t interested in much, but there is no hint in the document of such an external constraint. It has the feel more of the diminished Reserve Bank we’ve seen over and over again in the last few years – little published research, weak senior appointments (remember the marketing executive now responsible for macroeconomics, monetary policy and markets), and resources spent on (eg) comms staff, “stakeholder liaison”, and climate change, rather than on core areas of Bank responsibility.

As the review of the Reserve Bank legislation has proceeded I’ve observed on a number of occasions, including in submissions to FEC, that there are aspects of the new legislation that are a mess. The Remit review process, especially coming against the backdrop of the new Board announced last week, helps illustrate some of the problems.

Who is responsible for this Remit review advice? Why, “the Bank”. And “the Bank” here clearly does not include the Monetary Policy Committee, since (as you can see in the extract above) “the Bank” is required to consult the MPC before the advice is given to the Minister. And “consult” (standing alone) is about as weak as legislation gets: you can see by contrast that ‘the Bank’ is required to “consult and have regard to” (a materially stronger standard) the views of the public.

It is simply weird. We have a dedicated Monetary Policy Committee responsible for the formulation of monetary policy and working to carry out the current Remit, but they are treated (by the legislation) as distinctly marginal to the entire review process. There is no obligation on them to provide analysis and advice to the Minister, and “the Bank” is not even required – although it may choose to – to have regard to comments the MPC members might have on “the Bank’s” proposed advice or analysis.

Now, of course, the MPC is dominated by management anyway (the law requires a majority of executive members, each of whom owe their position. departmental resources etc to the Governor) but there are the three external members, and on a good day the Minister and The Treasury will try to tell us they have a valuable contribution to make to the monetary policy formulation process (on other days, the Minister will repeat the blackball he and Orr and Quigley put in place whereby anyone with current or future expertise and research agendas in areas relevant to monetary policy is automatically disqualified from serving on the MPC).

By construction, management always has the numbers so long as they stick together, but wouldn’t a much more sensible approach to have been to have made the MPC responsible for the Remit advice to the Minister, drawing on expertise and perspectives from both staff and outsiders?

The current structure seems especially problematic when one remembers who “the Bank” is. Until last week, unless otherwise stated (ie around the MPC) it was the Governor. But now it is the Board – the same Board of ill-qualified, in some cases conflicted, people I wrote about last week. Not one of the non-executive members of the Board has any experience or demonstrated expertise in monetary policy or macroeconomics. I guess in reality they will delegate it all to the Governor….but delegating such a major issue (or just putting it through the Board with no serious scrutiny or discussion) makes a mockery of the new governance structure.

(Amazingly, if the Minister – this one or a new one – wishes to change the Remit, the law requires consultation (but not “have regard to”) with “the Bank” but not at all with the MPC, who really do seem to be there mainly to make up numbers and eat their lunch (creating in 2018 the illusion of reform over the substance).)

As I noted earlier, there was no fresh analysis or research in the consultative document. What particularly caught my eye was that there was no attempt at a rigorous or systematic review of how monetary policy has been conducted, under the current Remit, in the last 2.5 turbulent years, in which the Bank has run up massive losses and seen (core) inflation blow out. I attended an online consultation session a few weeks ago and I raised this with staff. They told me that there is such a review underway, and they will even have it externally reviewed, but observed that they could not promise it would even be available before the next round of consultation on the Remit advice. That seems far short of adequate, even if your prior is (as mine currently is) that the specification of the Remit probably doesn’t explain a lot about what went wrong.

The Act requires that a review of monetary policy be undertaken (by “the Bank”) every five years or so, and perhaps the current exercise they have underway is the first of these reviews.

But again note how marginal the MPC is (must be consulted – apparently late in the process (“on a draft”) – but no obligation to have regard to their comments). And meanwhile responsibility for the review rests not with the MPC, but with that generic ill-qualified Board. There might be a certain logic in an independent review (done by proper external reviewers) but it is just a weird model – explicable only by a desire to preserve the Governor’s absolute dominance – to marginalise the MPC (who actually had responsibility, and so some self-scrutiny and reflection could be of value), while leaving the power with the Board but ensuring that no one appointed to the Board has the expertise to add much value at all.

This is the Board, you may recall, that Grant Robertson tried to tell us last week had no responsibility for monetary policy.

The legislation is a mess, and I hope that if there is a change of government next year that the new government makes some legislative time available to tidy up some of these provisions, and completing a transition to a model in which a proper MPC has the core responsibility, collectively and individually.

As for the substance of the consultation, I have made a short submission, the text of which is here

Some of my points are already dealt with above, and several are fairly minor in nature. I am broadly happy with the basic shape of the Remit, and it would ot be the end of the world were it simply to be rolled over as is.

I continue to favour a reduction in the inflation target, returning to the 0-2 per cent formulation we had in the 1990s, which is much closer to “a stable general level of prices” (the statutory formulation – and note that the Act is not up for grabs in this review). To make that feasible the effective lower bound on the nominal OCR (perhaps around -0.75 basis points) has to be addressed and either removed or substantially eased (doing so is not a difficult technical matter, but no central bank has yet done so). But even if the target is kept at a range of 1-3 per cent with a focus on the midpoint of 2 per cent it is important that the lower bound issues are addressed. We are in some respects fortunate that the 2020 downturn proved not to be primarily an adverse demand shock, but demand-led recessions will be back, and central banks are not adequately prepared for them. Meanwhile, the consultative document treats the lower bound issues as a given, even though as a technical matter they are entirely under the control of “the Bank” (how well equipped do you suppose that Board is to deal with these conceptual, legal, and monetary economics issues?)

Here are the last few paragraphs of my short submission

(And other economics agencies of government, but the Reserve Bank should be the highest priority given the extent of the decline and the substantive importance/powers of the institution.)

On Friday my post focused on the (severe) limitations of the members of the new Reserve Bank Board. Together, they look as though they would be a well-qualified (perhaps a touch over-qualified) group for the board of trustees at a high-decile high school……but this is the central bank and prudential regulator.

I had a couple of responses suggesting that, if anything, I was pulling my punches, understating the severity of the situation, when it came to the Reserve Bank. One person, who preferred to remain nameless (having high level associations with entities the Bank regulates), indicated that I was free to use their comments provided it was without attribution. These were the comments:

The situation is parlous: inept, multi-focussed but wrong focus, terrible judgement, appalling hires, complete absence of appropriate governance, woeful expertise, [backside]-covering of the regulator rather than interaction. I have zero confidence in their leadership, judgement, processes, balance of hires, and particularly governance which has been enabling of dross.

I guess the Governor could, in response, point to the recent NZ Initiative survey (of the regulated) suggesting the Bank’s standing among that community had improved in recent year (it was never clear to me why, other than the decision to move one key individual who had had significant responsibility for prudential policy).

So views will differ, and if – based mostly on what we all see – my views are a bit less harsh than those of some, it seems clear to me that there is a significant problem, and that with the new Board appointments the situation is worsening. The entire new governance and decisionmaking structure – overhauled over several years – is now in place with an MPC where serious expertise is explicitly a disqualifying factor for appointment as an external member (the people who are supposed to represent a check on management), and a Board where in practice serious subject matter expertise (financial stability and regulation or macro) also seems to have been treated by the minister as a disqualifying factor. And all this with a senior management team that is inexperienced (3 of the 4 internal members) or in the case of the Governor mediocre on a good day and more interested in other things (“patently inadequate” for the job was the stronger description of my commenter). Oh, and a Minister of Finance who doesn’t seem to have much interest in building excellent institutions or achieving excellent policy outcomes, who falls short of the standard citizens should be entitled to expect.

What we don’t know is how the National Party Opposition see things. They and their partner now lead in the polls and seem to have a pretty good chance of forming a government after the next election. Since Simon Bridges late last year, just after becoming the Finance spokesperson, said that National would not back reappointing Orr and was shut down within hours by his new leader, we’ve heard nothing much at all from National. You get the sense that the Governor is not exactly their cup of tea, but what (if anything) do they propose to do and say. They (and the other parties) were required to be consulted on the Board appointments. But whether they were happy, or pushed back vigorously, we have heard not a word from the new Finance spokesperson. Silence risks counting as (perhaps resigned) assent.

The Governor’s current five-year term expires in late March next year (ie less than 9 months from now). The process for filling the slot is likely to be getting underway very soon, and it would surprise me if the government (and the Bank) did not want to have everything resolved before Christmas. Under the Act, the Minister can turn down any candidate the Board nominates, but the Minister cannot impose his or her own candidate – ultimately whoever is appointed must be nominated by the Board. There is, of course, nothing to stop the Minister telling the Board in advance that he would not accept a nomination of a particular person or class of persons. In practical terms, there is also nothing to stop the Minister telling the Board who he might like them to nominate – although with a capable and independent Board that approach would risk backfiring.

Most RB-watchers treat the reappointment of Orr as pretty much a foregone conclusion (assuming the Governor has not found greener pastures in which to labour). At present, I agree. But that is partly because of the silence where one might have hoped there was an effective political Opposition. If National is content to resign itself to another five years of Orr – using his platform as head of a technocratic non-partisan institution to champion personal left-wing causes, operating with his bullying and divisive style, presiding over a sharp downgrading of the Bank’s research and analysis capability, losing billions of dollars for the taxpayer and then (together with the surge in core inflation) brushing it all off with a “I have no regrets” – they should just keep right on as they are.

But if they aren’t content, they should be saying so, forcefully and often, now. If Labour really insists on reappointing Orr, there is not much formally that can be done to stop it – a brand-new board, selected in part by Orr, is simply not going to decline to recommend reappointment. The only chance of him not being reappointed (assuming he still wants the job) is for Labour (Robertson) to decide it isn’t worth it for Labour to continue to back Orr. We should hope for Governors who are broadly acceptable across the spectrum (not necessarily the ideal candidate for the other side, but broadly tolerable nonetheless) – after all, they wield a great deal of power, can’t easily be dismissed, and Labour itself inserted the new clause in the law requiring the Minister to consult other political parties in Parliament before appointing a person as Governor. “Consult” does not mean “obtain consent or support”, but in a context like this it should mean “take seriously very strong opposition, especially from a range of parties, or perhaps from the largest other party”. It was, after all, Labour that just introduced the provision. But waiting until December to privately express concern is a pathway towards just being ignored – by then the reappointment process would have a lot of momentum behind it already. Now is the time to start speaking out, carefully but forcefully. If they care.

In the New Zealand system, most official appointees have fixed terms and cannot simply be dismissed and replaced immediately by a new government. Mostly, that is a good thing. The position of Governor of the Reserve Bank is one of those positions. So, it seems, are appointees to the MPC and the Board.

Each of these individuals or classes of people can be replaced at any time, but only “for (just) cause”, and what counts as “just cause” is defined in the Act. In the case of the Governor

The provisions around removal the Governor from office seem more tightly drawn than they were under the previous legislation (which may have something to do with the formal responsibility for many things the Bank does having been shifted to the Board).

Much as I am critical of a lot of what has happened at the Bank during Orr’s tenure, none of it (individually or collectively) adds up to enough to represent a credible basis for removing him. Are $8bn of LSAP losses dreadful and without excuse? Sure, but it was the Minister of Finance who agreed to the policy and the risks. Is it bad that inflation is at about 7 per cent? Sure. Could the Bank have prevented core inflation getting above 4 per cent? Most probably, and I think there should be searching criticism of the Bank’s failure, and lack of transparency/accountability. But it just isn’t enough to sack a Governor mid-term, especially when (a) so many other countries are seeing something similar, and (b) the median market economist/commentator wasn’t much better when it mattered (last year). One might reasonably lament the decline in the analytical and research output, some poor appointments and massive losses of senior staff. One might lament the diversion of focus onto non-central banking things like the tree gods and climate change. But no one is ever going to sack an incumbent Governor mid-term over such failings (and the Minister often seems to have welcomed the diffusion of effort), bearing in mind the risk of being judicially reviewed, and the attendant lengthy period of (market) uncertainty. It just won’t happen (and probably shouldn’t).

Which is why, if National were to be seriously bothered about Orr they need to be speaking out now and focusing on the looming reappointment.

Fortunately, even if reappointment is the key, there are other levers for promoting change. The Monetary Policy Committee’s Remit can be altered (and, no doubt, the forthcoming financial policy one), including to take out the woolly and irrelevant (to monetary policy) references to sustainable and low carbon economies. National is proposing to delete the employment limb of the target (on this, I agree with the Governor, that the amendment adding it hasn’t made more than cosmetic difference, and nor would reversing it). Ministerial letters of expectations aren’t binding, but they are one more lever, and a new government could make clear from the start that it expects the Bank to focus on its core responsibilities, expects a lift in the quality and range of research outputs etc. The Minister could also amend the rules around the MPC to, for example, require individual votes and reasons for those votes to be disclosed, and to create an expectation that individual MPC members could be expected to make speeches, give interviews, front FEC, and generally be accountable for their view. Small legislative changes to move the responsibility for MPC appointments purely to the Minister (not mediated by the Board) would also be a step in the right direction, weakening what is now a heavy degree of gubernatorial control over monetary policy and the committee.

And then there are the appointees themselves. By the time a possible National government takes office, Orr may be just 6-8 months into a second five year term. But quite a few of the new Board members have been appointed for terms that expire in mid-2025. A new government should begin looking early for high quality people, with strong subject expertise, to replace them. And what of the MPC? There are three external members. One has a term that expires next April, and will have either been reappointed or replaced by the current government. But one member – Peter Harris, who has had close Labour Party associations – has an extended term expiring next October. That should be a date that disqualifies a permanent appointment being made prior to the election (it still puzzles me why Labour chose that date – he could easily have been extended for 2 years rather than 18 months). And the final member has a term expiring in April 2025. It should be made clear to all involved that there will no longer be a bar on appointing people of demonstrated ongoing excellence and capability in macroeconomics and monetary policy, and that the Minister would have a strong preference to appoint at least one such person at the earliest opportunity.

And then there is the budget. The Bank is an unusual government agency, in that it is not funded by annual appropriations (in the way many important – with aspects of independence – agencies are) but through a five-yearly funding agreement, governing how much of its own earnings can be used as operational spending. There are a number of flaws in this procedure but it is what it is, for now at least.

The Bank was given a massive increase in funding in the agreement approved in 2020. But one of the interesting (broadly incentive-compatible) aspects of the arrangement is that permitted spending is specficied in nominal terms for five years. Above target or unexpectedly high inflation makes nasty inroads on the Bank’s real capacity to spend. As wages and salaries rise faster than originally allowed for, that bite is likely to be coming on soon. Moreover, although the agreement wasn’t signed until late Feb 2020, by the time a possible new government takes office (say next November) the Bank will be very conscious that the next round of negotiations will be looming before too long. The final year covered by the current funding agreement is 2024/25, but if you were the Bank (management and Board) you would be wanting some clear signals from the Crown fairly early as to how much the Bank might have available to spend in the following five years. An early signal (say by the time of the 2024 government Budget) from an incoming Minister of Finance that s/he was minded to materially reduce real Reserve Bank spending in the future funding agreement would affect choices the Bank was making from them. National seems to be struggling to identify expenditure savings, and while the Reserve Bank is not that big in the scheme of things, it is much bigger and more expensive that it was five years ago, and ripe for trimming down. The basic functions of the Bank haven’t changed, but the size of Orr’s empire has blown out. It should be pulled back. Ideally, the legislation should be amended to allow the Minister to better specify what money is spent on, but it should be made clear to the Governor and the Board that the Minister expects a ruthless focus on core functions (not, eg, a proliferation of comms or climate change people). The office of Governor might be much less appealing to someone like Orr if he was compelled to manage in that way. That, on this scenario, would not be a bad thing.

And all this without even touching on those mind-numbing documents like the Statement of Intent. The Minister can require a new Statement of Intent at any time, and the Bank must take seriously (“consider”) the Minister’s comments on a draft.

All this is by way of saying that while, if National cares about the Bank, it should focus now on building a climate where it is not worthwhile for Labour to stick by Orr (or where if they do it just looks like a poor and partisan appointment), there are plenty of avenues open to a new Minister to put pressure on to constrain the Governor’s behaviour, his dominance of the MPC process, his empire, his focus, his style and so on. But a new Minister has to want change, and be prepared to follow through consistently.

Finally on the Bank, it is fair to note that it is one thing to argue that Orr should not be reappointed, but quite another to identify an excellent potential replacement. There are no immediately obvious potential nominees of the stature required to begin credibly rebuilding the institution (Bank and MPC). That itself is a poor reflection on the way the Bank has been run for at least the last decade (contrast say the RBA or the Bank of Canada), and perhaps symptomatic of wider weaknesses now at the upper levels of the New Zealand public sector more generally. But just because there is no obvious single name now, isn’t a reason to stick with such a poor incumbent (and if there isn’t an obvious replacement, I can think of several who could, at least as part of a new team, do the job, and we should at least be open to the possibility of a foreign Governor (even if such an appointment might be less easy than it sounds)).

This post has been focused on the Reserve Bank. But there are other agencies a new Minister of Finance will have to pay attention to. There is little point expecting different outcomes if you leave the same people (and sorts of people) in place (and there is a wider question there about what sort of person a new government will replace Peter Hughes, the Public Service Commissioner) with in mid 2024). But the open question still is whether National really cares much about different outcomes, or is primarily interested just in gaining and holding office. Voters might like some idea of the answer.

Today marks the end of an era at the Reserve Bank, as the last of the “Governor as single decisionmaker” model is dismantled, and tomorrow the new Board takes over the primary responsibility for the Bank’s affairs. The single decisionmaker model was an experiment, but with time it was increasingly apparent that it was a poor one, increasingly unfit for purpose. No other country reforming its central banking and bank etc regulatory arrangements followed us. It is to the government’s credit that they have moved the governance model for the Reserve Bank back towards the international mainstream (even if the specifics of the 2018 and 2021 are less than ideal, and in some respect a dog’s breakfast).

(NB note that most of the new Board, to take up office tomorrow, has not yet been appointed – or at least announced. With the new Board reportedly supposed to be meeting tomorrow, perhaps there is some launch announcement planned, but it is all a bit strange and not really that satisfactory.)

In this post I wanted to focus, perhaps for the last time (although they still apparently have an Annual Report to come), on the old Board. This should be the last day we see this graphic topping the Bank’s “Our Board of Directors” page

For 32+ years, taxpayers have paid a Board to (come for lunch and the cocktail do and) monitor and hold to account the Governor (and more latterly the MPC). They controlled who could be appointed as Governor and to the MPC, and – consistent with those accountability responsibilities – could recommend dismissal. The rules and responsibilities have changed a bit over time. For the first decade or more, the Governor chaired the Board, and even though there was a non-executive directors committee that was supposed to do the holding to account, the messaging implied by the structure wasn’t exactly crystal clear. And it wasn’t until about 20 years ago that the Board was required to make its own (public) Annual Report, but even then not very much changed – and consistent with that general observation, the Board’s report was buried in the midst of the (Governor-controlled) Bank Annual Report and was given no publicity when the Bank released its Annual Report.

There have been some able people on the Board at various times over the years. And some awkward people (the two may even have overlapped), but the institutional incentives very quickly developed into a model that meant few hard questions really got asked, little serious scrutiny happened, and the public never got any serious insight from the Board’s activities on their behalf (the Board, after all, had access to papers the Bank jealously guards for years and years after they were relevant, and can engage and challenge the Governor and other decisionmakers). I say “very quickly developed” because in the earliest years of the regime there was a view – shared by the Governor – that the inflation targeting governance regime was relatively mechanical and that a Governor might reasonably expect to lose his/her job if inflation overshot the target range. The first (apparent) breaches in about 1995 prompted some hard questions, some letters to the Minister, but eventually a recognition that the whole thing involved a lot more judgement and discretion if sensible policy was to ensue. There was a recognition that the target was something to be “constantly aiming at”.

Unfortunately for the Board, had they ever aspired to do the job really well they didn’t have the resources to do so. It became customary to have one professional economist on the Board (first Viv Hall, then Arthur Grimes, more recently Neil Quigley), but Board members didn’t get paid much themselves, had no direct access to staff resources, had no budget to commission independent professional advice, and their own Secretary was for the most of time a senior staffer of the Governor. Board meetings occurred on Bank premises, and one entered the Board room past the row of oil paintings of former Governors. And once the Board got its own chair – chosen by them, not the Minister – for 13 years they opted to have as their chair former RB staffers, first Arthur Grimes, and second Rod Carr. Most of the Board members knew about being on corporate boards – where they had decision-making powers – and so there seemed to be a tendency to default towards the sorts of issues they might have dealt with as corporate board members. Monetary policy and financial stability/regulation were not high among them. Arms-length challenge and scrutiny also weren’t really among those functions – on a corporate board, the board has far more ownership of the firm’s strategy (something the Act never envisaged for the RB – the Board had no say, for example, in Policy Targets Agreements or the conduct of monetary policy).

And so acting as cover for management seems to have become the default mode – most especially externally but, as far as we can tell, often internally as well. Some Board members had their own agendas – some more laudable than others – but there was never much sign of a sustained effort to hold the Governor and Bank to account, to act as if they represented the government and people of New Zealand rather than the Bank management (notably whoever was the Governor at the time). At times, their Annual Reports even talked about helping with the Bank’s external relations (for example, at the functions held around Board meetings outside Wellington).

I could develop some anecdotes at length, including for example, the board member who used to ring me up (while I was still on staff) for inside angles on monetary policy and the Governor, at a time when that member was attempting to mark out an independent position (oops, he is now the Board chair). But I’ll largely leave it at that. I don’t think anyone – perhaps with the exception of some individual Board members – thinks the Board ever really did the job it was designed for. You could be attacked in public by the Governor – for exposing an OCR leak, resulting from weak management systems – and an approach to the Board still resulted only in them gathering in behind the Governor. Are we to suppose it was any different when Orr was attacking his critics around the bank capital plans in ways that few regarded as represented expected conduct from a Governor?

But what interested me was how they had handled the events of the last year or so. The Bank has run up massive losses on the LSAP. Inflation – headline and core – has shot through the top of the target range. All in all it is has been one of most interesting – and surely questionworthy – periods in the 30 years the Board had the monitoring and accountability responsibility. You might think the outgoing Board would want to end well.

A while ago I lodged an OIA requesting the Board minutes for the period November 2021 to April 2022. About the time those results came back I found on the Bank’s website the results of someone else’s OIA for the minutes for September to November 2021. So we have a run of several months of minutes, over a period when things moved a lot on monetary policy (actual inflation, the OCR, forecast inflation – oh, and those LSAP losses). We might have hoped for a lot of evidence of hard questioning, challenge, and serious scrutiny.

Well, might have if we had known nothing of the previous 30 years.

The Bank – or Board – is relatively open in what they release, so we get a good sense of the complete minutes. There are some questions about what they write down, but even there they seem to have improved (relative to earlier concerns that in some areas they were in flagrant breach of the Public Records Act).

What do we learn?

The first meeting was in early September, not long after the August MPS (which itself came the day after the lockdown was announced). The minutes are seven pages long, and we learn a fair bit about the People and Culture report, the Enterprise Risk Management report, the Governor’s activities, and even the RB superannuation scheme (which the Board had some particular non-statutory responsibilities for). Monetary policy gets half a page

Only one Board member is reported as saying anything (“noted” not exactly being a strong form of questioning) and none seems to have challenged the (soon to be restructured out) Chief Economist’s view that the Bank had plenty of time and didn’t need to act (much/) until it had a seen a full 12 months of data. The Governor – the most influential MPC member – is not reported as having said anything.

The late-October meeting minutes took eight pages. We learned quite a lot of various administrative and/or extraneous matters, including the Bank’s climate change strategy. There was quite a discussion on the forthcoming FInancial Stability Report, but no sign of any serious challenge or scrutiny from Board members, on requests for follow-up papers etc. And then we got to monetary policy, the OCR having just been raised for the first time.

I’m sure it was all very pleasant, but there is no sign of any hard questioning about immediately relevant issues (or perhaps the Public Records Act is being ignored again). No one seems to have challenged them as to whether, just possibly, if inflation was already above the midpoint and employment at or above midpoint, and forecasters had been taken considerably by surprise, whether a more aggressive stance might be warranted. No one seems to have challenged Ha on his complacent comment the previous month, despite (presumably) just having confirmed those minutes.

At the November meeting there appears to have been no discussion of monetary policy at all (although the Board was at pains to stress the importance of the outgoing Board having time to prepare their final Annual Report). Not a word. And, of course, still no mention at all of those mounting LSAP losses – and the Board is supposed to have been agents of the minister and the public, not of the Governor.

For the December meeting this is what the minutes record

All of which may have made for quite an interesting discussion, but as the Governor is recorded pointing out, monetary policy has to act given what is happening to fiscal policy (fiscal policy is not something the Governor or Board are responsible for). But there is no sign of any unease, of even a single Board member challenging the Bank to show that it was on the right track or that inflation would come out something like forecast. There is just no sense of holding powerful decisionmakers to account in particularly troubling times. Just a chat, with one’s friends and colleagues.

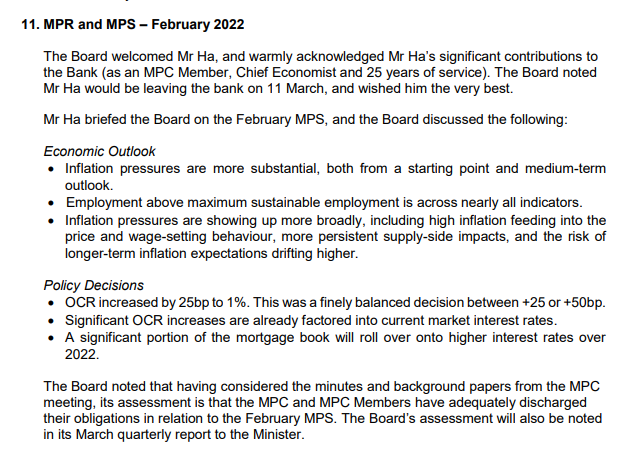

At the February meeting, this is all there was about monetary policy

Again interesting (if brief) but with not the slightest sense of unease or challenge, no pressure on the Governor or his colleagues.

In March

Were some future historian to stumble across these minutes, but not the relevant parts of the Act, they might have assumed that the Board had just a right to be briefed, but no responsibility for ensuring the Governor and the MPC are held to account.

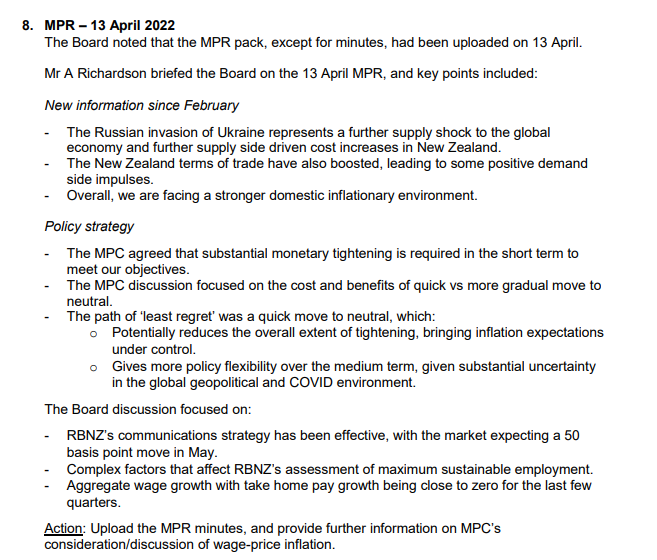

And finally in this sequence, the April meeting

It is, I’m sure, interesting enough, but it scarcely counts as evidence of accountability.

Now, it is always possible that there are secret unrecorded discussions (in breach of the Public Records Act). The other OIA requester asked for a copy of one of the Board’s reports to the Minister, which the Board/Bank adamantly refused to release

That should be unacceptable: the Governor and MPC are statutorily accountable via the Board, and the idea that management might refuse to supply information to the Board because the Board’s report – even with some redactions – to the Minister might be released (with some lag) should have been unacceptable. But we needn’t worry that there might be anything very revealing in such a report: take a look at the March Board extract above, and you’ll see they record there that they were going to tell the Minister all was fine.

At one level, knowing what we do as to how the Board has operated over 30 years, none of this should be too surprising. But it doesn’t reflect well on them (any of them). We have a chair presumably focused mostly on working with the Governor to see in the new act (questionable appointments and all), and so hardly likely to make himself awkward on current monetary policy, and other Board members with neither the expertise, inclination, nor institutional culture to ask hard questions. But still….across all those months

no record of a single hard question,

no sign of any sustained engagement at all with the external MPC members (whom they are supposed to individually hold to account)

no requests for supplementary papers,

no suggestions of commissioning independent analysis,

not a single mention of the huge (and mounting over this period) LSAP losses,

no suggestion of any regrets about anything.

It is easy to be inured to flawed frameworks and the weaknesses they generate, but this really isn’t good enough. These people took the taxpayers’ money (no much admittedly, but they each took the deal) and seem barely to have been focused at all on their monetary policy accountability duties, through one of the biggest monetary policy disruptions for decades. Perhaps I should ask for the minutes of meetings of the previous 20 months, but it would be a real surprise if anything had been different then.

The Bank itself appears little better, since there is no evidence in any of these minutes of robust or independent analyses and reviews of what had gone well, and what badly, why for examples forecasts had been so wrong, and what lessons staff and management had taken. And so we are in the weird position that the Bank has a consultation paper out at present on the future Monetary Policy Remit, and yet tells us that the review they are finally doing of the last couple of years stewardship may not even be released before the second round of consultation closes.

The Board has proved useless. It was always likely given the incentives and flawed structures, but that is no excuse for any of the members. The job was there to be done, and they have not been doing it (most notably over the dramatic times of the last 12 months).

The end of the era will be no loss. We can only wait and watch and see how the new Board does – when the Minister finally manages to dredge up enough people willing to do the job to get a full complement on board.

On Friday (1 July) the new Reserve Bank legislation comes fully into effect. The new Reserve Bank Board takes over from the Governor personally as the key governing body of the Bank, on all matters other than the conduct of monetary policy (but even there they have a big influence on the composition of the MPC). A member of the outgoing (advisory) Board told us – he sits on the RB pension fund trustees as, for my sins, do I – that the new Board is having its first meeting on Friday. And yet today is Tuesday and we still don’t know who is being appointed to this (on paper) powerful government board. Every Tuesday for the last couple of months I’ve checked Grant Robertson’s Beehive page, and still there is no announcement.

The Governor is a Board member ex officio. And several months the Bank slid onto their website the information that two members of the existing Board (including the chair) and one new person had been appointed to a “transition board” and would be appointed formally to the new Board. But the same web page still says

Neither the government nor the Bank seem to have been entirely straight on the matter, since an OIA release of Board minutes says that Suzanne Snively has also been appointed to the transition board, and has been attending meetings of the outgoing board. It is a curious appointment, both for her age (I’m not keen on a trend towards US-style gerontocracies) and for the fact that it is almost 40 years since Roger Douglas first appointed her to the Reserve Bank Board (back in the previous era when the Board held the formal powers). Media reports suggest she fell out with Douglas, and is much more ideologically aligned with the current version of the Labour Party and its not-Douglas Minister of Finance.

The other newbie we know about is Rodger Finlay. I wrote about his appointment a few weeks ago and there has since been some media coverage. Recall that the Bank was quite open in advertising that Finlay had been appointed to the transition board and was being appointed to the full Board even though he is chair of NZ Post, majority-owner of a New Zealand bank (Kiwibank) that just happens to be the weakest of the large banks in the system. The unadorned label “He is currently Chair of New Zealand Post” is still there this morning.

It was a highly inappropriate appointment, even though in response to questioning from a journalist the Minister of Finance’s office eventually advised that Finlay was ending his term with NZ Post on 30 June. [UPDATE: I’m advised this was actually passed on to the journalist quite readily by NZ Post itself.] If his appointment to the Reserve Bank early was really vital to the success of the new regime, he should have stepped down from the NZ Post role immediately, and neither Orr, Quigley nor Robertson should ever have countenanced anything different. Quigley told media that Finlay had been developing “new governance systems” for the Board, but if he had any real suitability for such a role – where ethics count hugely – he should have known from the start how inappropriate it was, and would look, for him to be serving the Reserve Bank in such a role while chairing the company that majority-owned a bank regulated by the Reserve Bank. For all that Quigley says they were aware of the issue all along, everything about how they operated suggests they took the narrowest legal interpretation, in a way they would no doubt look on askance if a regulated entity tried it on. (It doesn’t strengthen their case that NZ Post is also majority owner of Kiwi Wealth, a significant funds management operation even though that body is not regulated by the Reserve Bank.) As it is, documents released under the Official Information Act confirm that Finlay has been regularly attending meetings of the existing Reserve Bank Board and thus been party to all the information that board has had before it.

It is a poor look and reflects poorly on everyone involved – Minister, Governor, chair, Finlay, and (less severely) the other members of the outgoing board. Among other things, it raises doubts about the approach that these players might take in future. And also leaves us with the question as to how the consultation with other political parties – now required for Board appointees – went down as regards the Finlay appointment. I guess one day the OIA may shed some further light. It is all rather suggestive of a cavalier Wellington approach to conflicts of interest (and both actual and apparent matter).

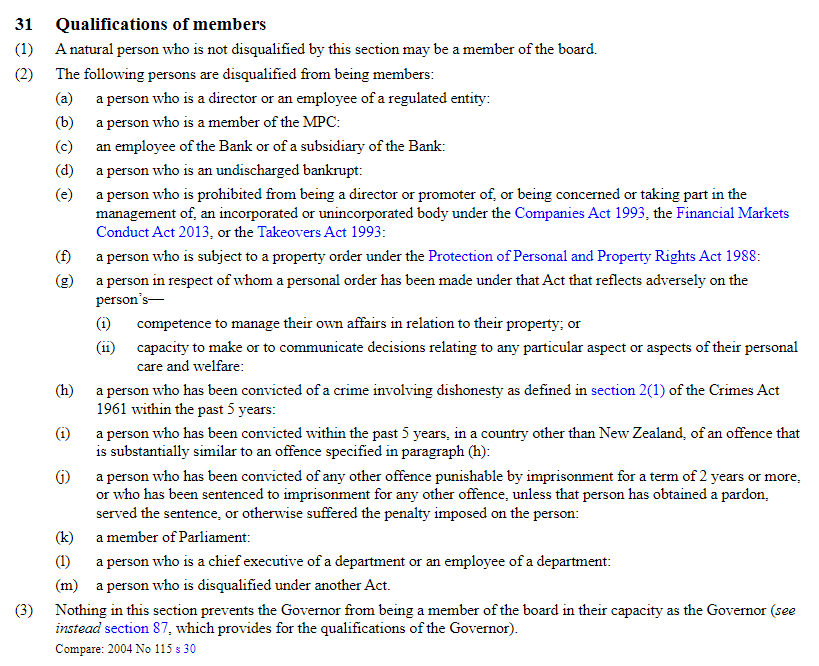

In my earlier post I included this section of the new legislation on the sort of people who can’t be Board members.

I have no problem with the provisions that are there. The problem is with what is not there. As I noted in the earlier post it is astonishing that a director or senior employee of a company that has a majority holding in a regulated entity (bank, insurer, deposit-taker etc) can be appointed to the Board, and can hold those two positions simultaneously. It is almost as concerning that someone who derived most of their income from work for one or more regulated entities (eg a partner of a law or accounting firm) can simultaneously be a director of the prudential regulatory agency.

But what I hadn’t noticed then (I guess my focus was elsewhere) was that there is no restriction at all on Reserve Bank board members holding ownership interests in regulated entities. According to this brand new law, I can’t be a director of a bank, insurer or finance company and simultaneously serve on the Reserve Bank Board (tick) but…..I could own a whole entity and do so. It is astonishing that Parliament has not protected us against the risk of such an appointment – so much so that one almost has to start asking why. Reserve Bank staff aren’t (or weren’t) allowed any such holdings, but it is the Board that makes the rules, sets priorities etc..

Before going further I should clarify two things: first, I’m sure no one wants to stop Board members (or staff) having totally passive interests through, say, a widely-offered Kiwisaver fund, or a passive NZ equities index fund. A caveat that no holding could be large enough it could credibly be regarded by a reasonable observer as likely to influence decisionmaking would seem sufficient to cover that. But that does not cover a 40 per cent stake in a finance company (say). And, second, the issue here is not a director might be engaging in deliberations specifically on a company s/he held a major stake in: I’m still willing to believe conflict of interest policies would require such a director to recuse him/herself from that specific discussion. But the Reserve Bank Board makes policy, applies policy, for broad classes of institutions, and no director with an ownership (or major income) interest in a regulated institution should be making policy for that class of institution, or contributing to internal discussion on the direction policy should go.

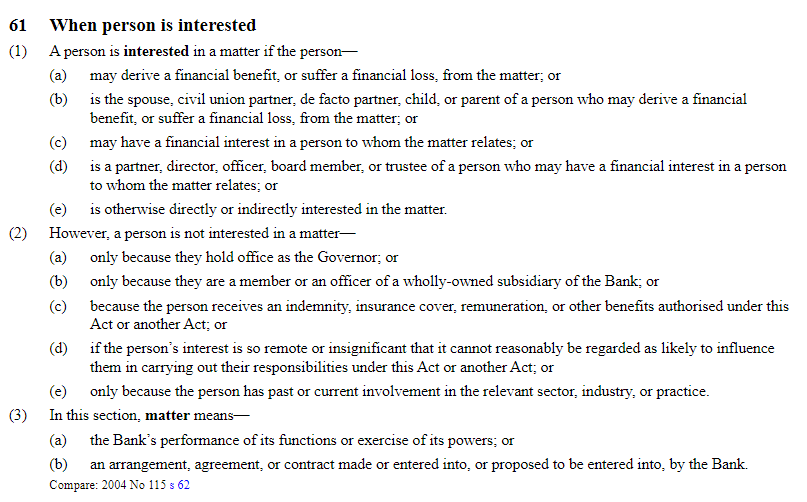

The new Act has a long list of provisions regarding conflicts of interest (from section 61). It starts reasonably enough

Any such conflict has to be disclosed to the chairperson – but not to the Board more generally, let alone the public.

And although the general provision is that a person cannot participate in a matter in which they have a conflict, there is explicit provision in the Act for the chair to waive that prohibition

Any such waiver has to be disclosed, but only in the Bank’s Annual Report, which may not be out for more than a year after such a waiver has been granted.

And one might have more confidence in the current chair, were he not complicit in the appointment of Rodger Finlay, while the latter was chair of the owner of a majority stake in a large bank.

More generally, there is a sense that these conflict of interest rules are written to cope with episodic events and conflicts that might arise, not really specifically foreseeably, in the course of a term on the Board. If the Board is looking to hire a consultant who is the husband or child of a Board member most probably that Board member would stand aside for that discussion/decision. But a Board member who owned half a finance company might reasonably claim that, having known of such an interest, the Minister had nonetheless lawfully appointed him/her, and that the conflict of interest rules would not apply to the Board’s general deliberations on policy for finance companies. Perhaps it would hold up, or perhaps not, but the government and Parliament should never have left such scope for uncertainty, the risk of highly inappropriate appointees (however capable), in the legislation. Section 31 (see above) should have been written a lot more restrictively.

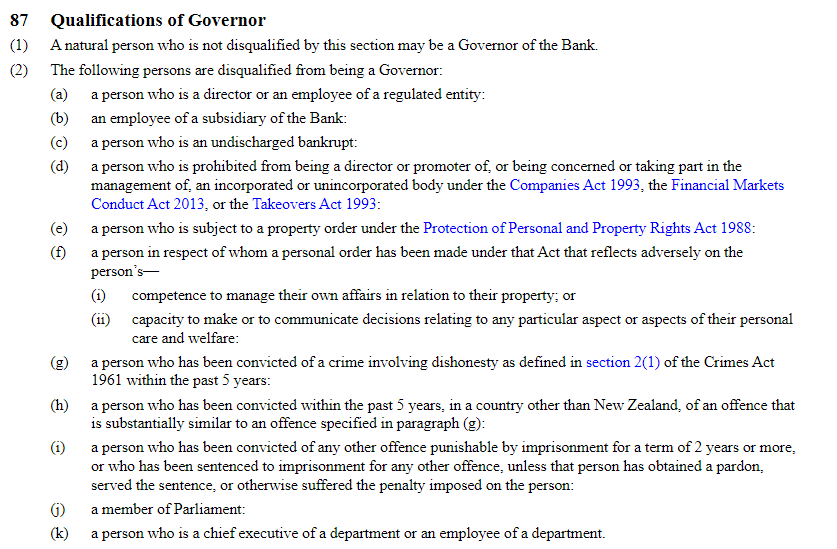

My concerns were only heightened when I happened to have a look at the clause in the Act governing the removal/dismissal of a Governor. These are the things that disqualify you from being Governor.

But notice that being a director of an entity that owns a regulated entity isn’t a disqualification. And neither is having a direct ownership interest in a regulated entity.

Was this an oversight? It appears not. These are just causes for which the Governor can be dismissed

1(g) looks like it should be reassuring. But, there is more

Parliament has explicitly written the Act to allow the Minister of Finance to agree with the Governor that the Governor can hold an “ownership interest in a regulated entity” while serving as Governor (all compounded by the fact that no such provision would be public information).

I am not, repeat not, suggesting anything shady between the current incumbents, but why would Parliament put such a provision in the Act (without at least one of those “trivial or incidental holdings arising from passive holdings in broad-based investment funds” type of caveats)? It is just a dreadful look.

Will any of these provisions necessarily be abused? No, not necessarily. But things have not gotten off to a good start with the Finlay appointment, which makes it difficult to have much confidence in the rigorous integrity of the people involved in these appointments etc, now and in the future. Maintaining a honest and uncorrupt system depends in no small part on sweating the small stuff, but Parliament should just never have left these matters in any doubt, apparently entirely reliant on successive ministers, Governors, Board members being interested in bending over backwards, even when it is inconvenient, to avoid the substance or appearance of conflict in our prudential regulator.

Meantime minister, where are the Board members for this shiny new goverance model? And where, in particular, are the members with real and in-depth expertise in banking, financial system regulation and so on?

There is an extraordinary column in the Herald this morning, by their excellent Kate MacNamara (complete with nice biblical allusions in the online version headlines, which may be lost on a younger generation of readers) on the travails of the Productivity Commission. If you can get access, and you care at all about economic policy and institutions in this country, you really should read it.

The Productivity Commission was set up a decade or so ago by the previous government. Inspired by the Australian Productivity Commission – which has done some good work over several decades – there were both cynical and genuine motivations behind it. On the cynical side, it was a cheap win for ACT (this was during the 2008 to 2011 term), and it offset the premature termination of the 2025 Taskforce. But on the more serious side, there was a recognition of the long-running New Zealand productivity failures, and a genuine recognition of the contribution of the Australian commission. There was, of course, no willingness by either the previous government or the current one to do anything serious about productivity-enhancing reform, but perhaps a small fairly inexpensive Commission might come up with some useful nuggets.

One can debate what value the Commission added in its first decade (a mixed bag on my telling), but this story starts 18 months or so ago when the government appointed Ganesh Nana as the new chair. Things seem to have gone dramatically downhill from there, and article reports several waves of staff departures, as well as reminding us of the departure of two commissioners (so bad has the government’s handling got, that one commissioner has had to agree to stay on a bit just so that the Commission has a quorum). Independent HR consultants had been hired (MacNamara got their report) and she has various staff (former and, quite probably, current) speaking to her. The Productivity Commission (PC) is a small organisation, and must be an even more unhappy place this morning.

Nana was clearly appointed by the Minister of Finance to bring a quite different ideological (charitably, analytical) approach to the Commission, but surely even Robertson must be surprised at how poorly Nana has handled the transition from running his own consultancy, to leading an established public sector agency. Some cynics reckon the intention all along was to gut the Commission. Perhaps, but state-funded commissions producing ideologically sympathetic – but perhaps good quality – reports have value to political parties, and it seems they probably aren’t even getting that. Instead, following on from the systematic degradation of the capability of the Reserve Bank, Robertson now seems to have done it to the Productivity Commission as well. Both have the hallmarks of a man who openly says he went into politics to be not Roger Douglas, and who really cares barely at all for the longer-term capability of our economic agencies, let alone the longer-term performance of the New Zealand economy.

But the main reason for this post was that I got mentioned in the article, in a way that may read a little unfairly to Nana (of whom I have been consistently critical since he was appointed, and whom I do not think is fit to hold that particular office). The context was the recent immigration inquiry.

First, it should be noted that the Productivity Commission, as is usual, invited submissions from anyone on both their issues paper and their draft report. I did not make a submission in the first round (although I did make a fairly short submission on the draft report) and, as far as I can recall, neither Eric nor the New Zealand Initiative made submissions at all. I did not make an initial submission for two reasons: first, that my views had long been on the record (and I knew Commission staff were aware of papers/speeches) but also because I had little trust in the willingness or ability of the Commission to grapple seriously with the analytics of the New Zealand experience with large scale policy-led immigration. Among other things, several years earlier Nana had openly championed a “big New Zealand” model in an RNZ discussion we had both participated in.

However, over the course of last year there were several interactions. In June, Commission staff invited me in to articulate my story (which had been outlined again in a recent speech) and to offer any perspectives on the Issues Paper they had released. I had a session at the Commission on 8 July where I noted (my diary)

…to my slight discomfort [given my past open criticism of him] even Ganesh turned up. Seemed to go quite well – Bill Rosenberg in particular quite tantalised – and I think I at least got them to the view that some sort of cross-country and historical analysis will be needed to do the job even remotely well.

I followed up the meeting by sending them a series of further observations, links to posts etc.

Several weeks later I had this unprompted email from a senior Commission staffer, cc’ed to the inquiry director

I wasn’t keen, for various reasons

Despite my expressed reluctance, Commission staff pursued the matter, and I had a phone discussion with Geoff Lewis. My diary records

Talked to Geoff Lewis about the paper the PC want me to write. I’m not keen – don’t think it would work for them or me (or my cause) – but Geoff has gone to sound out Graham Scott [former Commissioner] & might see if they can get parallel papers from Eric and me – which could work.

I don’t have records of this, but memory suggests it being mentioned at some point that Scott had shared my doubts. I don’t know whether staff ever approached Eric, but as you can see I was never keen, and frankly had I been Ganesh Nana I probably wouldn’t have been keen either. (Note that the views of both Eric and I on New Zealand immigration policy and economic performance were already well-documented in various references, speeches etc, including a couple in which we had shared a platform.)

But that wasn’t the end of my engagement with the Commission (staff or commissioners).

And we had that session on 1 October. From memory all the Commissioners attended, and most of the Commission staff. Arthur Grimes is pretty open about his general sympathy for an open-borders approach, and a big believer in large scale immigration to New Zealand (telling the Commissioners that the big gain from immigration was the higher house prices existing New Zealanders got to sell their houses at). Despite our vast differences on the wider issue, Arthur and I combined to strongly disagree with the suggestion the Commission was floating for trying to calibrate the non-NZ citizen inflow to changes in the net flow of NZ citizens. It was a simply unworkable scheme, even if in principle it had had any substantive merit (which I suspect neither of us thought it did).

I concluded my diary comments observing that

But the real problem is that not really any of the Commission people had a strong macro orientation and so much of the discussion appeared ill-anchored (and often not that aware of other experiences etc etc),

Ganesh Nana’s own comments and observations was particularly superficial. Staff seem to have had good intentions, but not necessarily the capability, and the Commission as a whole seems not to have been willing to hire or contract relevant expertise

Obviously I cannot speak to what was going on inside the Commission’s four walls, but I will give Nana credit for having turned up to both meetings.

The Commission’s draft report was released in November. It was a dog’s breakfast, and thus suggestive of real tensions with the Commission. I wrote about the draft here under the heading “Productivity Commission at sea”.

In a background paper there was a reasonable discussion of aspects of what has become known as “the Reddell hypothesis”, but you would hardly have known it from the main draft report

As for the “Reddell hypothesis” itself , the Commission says

At this stage of its inquiry, the Commission is not taking a definite view on the Reddell story

Which, I suppose, is a legitimate stance for them to take, but there is nothing much in the report even indicating where their key uncertainties are, let alone a provisional overall interpretation that submitters could scrutinise and review. I don’t suppose that will seem very satisfactory to anyone, from any side of the debate, considering making a submission. It speaks of a Commission that just has not exercised the intellectual grunt to critically analyse, assess, research and review conflicting arguments and interpretations.

There seemed to be both weaknesses in analytical grunt, and the likelihood of disagreements within the Commission, and yet there was no sign of any serious effort to get to the bottom of the issues. It might have been an entirely reasonable conclusion, having thought hard about the New Zealand experience (past and present, abstractly and in light of literature of other countries’ experiences), that they could show that large scale immigration had in fact produced substantial economic gains for New Zealanders. Or to have become persuaded by something akin to my story. But they never showed any sustained sign of making the effort, either way.

I did make a submission at this point (link in this post), partly for the record and partly to back up a couple of other submitters (one of whom was running more or less my story).

In many respects, the final report was even worse than the draft. It was more or less devoid of any serious analysis of the economic implications of New Zealand’s experience with large scale policy-led non-citizen immigration. Even for those of a serious analytical bent who basically like something like the pre-Covid status quo, it can’t have been at all satisfactory – making no attempt to do anything more than offering up quite glib lines about there being small economic benefits from the New Zealand policy approach. Understanding was not advanced one jot – fallacious stories (whether mine or the policy-establishments) are not shown to be wrong, true stories (whichever) have no serious evidence advanced, or fresh analysis undertaken to strength our confidence in those stories.

It was, in the words of a former Treasury deputy chief economist (not at all sympathetic to my specific story) on Twitter the other day, the sort of thing one might easily have gotten an MBIE policy team to churn out: a few charts, a few bromides, a few minor bureaucratic recommendations, and no real added value – from an independent Productivity Commission – at all. Whether one is inclined to agree with their prejudices or not.

For me, it was perhaps summed up in a lunchtime seminar a couple of weeks back organised by Motu on the Commission’s report. The speakers/panellists were all pretty keen on large scale immigration to New Zealand, but what really caught my ear was Nana who (a) wanted to take politics out of immigration policy (what planet is he on, for such a significant structural policy choice) and (b) describing any doubts about a large scale policy-led migration to New Zealand could only sneer that any scepticism reflected a concern about “nasty migrants”.

And that sort of summed up a deeply inadequate inquiry from a seriously inadequate Commission.

The Productivity Commission should simply be wound up. It adds no obvious value and can never have the institutional depth and specialisation of the Australian version. It isn’t obvious that either Labour or National want serious rigorous in-depth economic analysis and research, but if they do we might as well concentrate public sector resources at The Treasury, who are supposed to be the government’s main advisers on such things.

In the meantime, you wonder which left-wing economists the government will eventually persuade to take on a Commissioner role, especially under Nana.

The Reserve Bank Governor appears to have been communing with his tree gods again, and last week released a speech he’d delivered online to an overseas audience headed “Why we embraced Te Ao Maori”. It isn’t clear quite how many people were in the audience for this commercial event run by the Central Banking (private business) publications group, but I’m guessing not many. The stream Orr spoke in featured just him, a panel discussion on how “digital finance can drive women’s inclusion”, and a presentation on “how can central banks put climate change at the core of the governance agenda”. While it was called the “governance stream”, a better label might be the woke feel-good stream, far removed from the purposes for which legislatures set up central banks.

In many ways, the smaller the overseas audience the better, and I guess his main target audience was probably domestic anyway. He claims to be keen on the concept of “social licence” (personally, I prefer parliamentary mandates, deliberately adhered to and closely monitored) and no such “licence” flows from second or third tier central bankers abroad.

There are several things that are striking about the speech. Sadly, depth, profundity or insight are not among them.

Orr has now been Governor for just over four years (his current term expires in March). In his time as Governor he has given 23 on-the-record speeches (fewer as time has gone on)

The speeches have been on all manner of topics – although very rarely on the Bank’s core responsibility, monetary policy and inflation, a gap that has become more telling over the last year or so. Unfortunately, coming from an immensely powerful public official, it is hard to think of any that are memorable for the valuable perspectives they shed on the Reserve Bank’s core policy responsibilities or its understanding of, and insights on, the macroeconomy and the financial system. His Te Ao Maori speech is no exception, and is probably worse than average. From a central bank Governor.

In the speech, we get several pages of a quite-politicised black-armband take on what might loosely be called “history”. Perhaps it will appeal to elements on the left-liberal electorate in New Zealand (eg the editors and staff on the Dominion-Post). I’m not going to try to unpick it – it simply has nothing to do with central banking or the Governor’s responsibilities – although suffice to say that if one wanted to traverse history in a couple of pages, one could equally choose quite different points to emphasise. In essence, we have the Governor using his official platform to (again) champion his personal politics. That is – always is, no matter the Governor, no matter their politics – inappropriate, and simply corrodes the confidence that should exist that the Reserve Bank is a disinterested player serving in a non-partisan way the narrow specific responsibilities Parliament has given it independence over.

The speech burbles on. The audience is reminded of the tasks Parliament has given the Bank to do

But this is immediately followed by this sentimental bumpf

But – and rightly – “environmental sustainability, social cohesion and cultural conclusion” (whatever their possible merits) are no part of the job of the Reserve Bank. Parliament identifies the Bank’s role and powers, not the Governor. And all this somehow assumes – but never attempts to demonstrate – that some (“a”) Maori worldview is better for these purposes that either some other “Maori worldview” or any other “worldview” on offer. As for the “long-term”, a key part of what the Reserve Bank is responsible for is monetary policy, where they are supposed to focus on cyclical management, not some “long term” for which they have neither mandate nor powers.

Get right through the speech and you’ll still have no idea what the Orr take on “a” Maori worldview is. Thus, we get spin like this

Except that, go and check out the Bank’s Statement of Intent from 2017, the year before Orr took office, and the values (those three i words) were exactly the same. All they’ve done is add some Maori translations on the front. If anything, it seems more like a Wellington public-sector worldview (“sprinkle around some Maori words and then get on with the day job”), but Orr seems to sincerely believe……something (just not clear what).

Then we get the repeat of the “Reserve Bank as tree god” myth. The less said about it the better (and I’ve written plenty before, eg here). But even if it had merits as a story-telling device, it is substance-free.

We get claims about “the Maori economy”. Orr cites again a study the Bank paid BERL to do, the uselessness of which was perhaps best summarised by the report’s author at a public seminar at The Treasury last year, of which I wrote briefly at the time

Even the speaker noted that “the Maori economy” is not a “separate, distinct, and clearly identifiable segment” of the New Zealand economy

The last few pages of the speech purport to tell readers about their Maori strategy. There are apparently three strands. First, is culture

To which I suppose one might respond variously (to taste), “well, that’s nice”, “what about other world views?” and “wasn’t that last paragraph rather suggestive of the public sector worldview above – scatter some words and get on”.

Then “partnering”

There is more of that, but none of it seems to have anything to do with the Bank’s statutory goals, it is more about officials using public money to pursue personal political objectives. Incidentally, it also isn’t obvious how any of it reflects “a Maori worldview”. I’d think it was quite a strange if the Reserve Bank were to delete “Maori” from all these references and replace, say, Catholics (another historic minority in Anglo-oriented New Zealand).

The final section is headed “Policy Development” and you might think you were about to get to the meat of the issue – here finally we would learn how “a” “Maori worldview” distinctively influences monetary policy, banking regulation, insurance regulation, payment system architecture, the provision of cash etc. The section is a bit long to repeat in full, but you can check the speech for yourself: there is just nothing there, of any relevance to the Bank’s core functions. Nothing. No doubt, for example, there are some real issues – and real cultural tensions – around questions of the ability to use Maori customary land as collateral, but none of it has anything to do with anything the Reserve Bank is responsible for. And nothing in the text suggestions any implications of this vaunted ill-defined Maori world view for the things the Bank is supposed to be responsible or accountable for. And still one would be left wondering why, if there were such implications, Orr’s personal and idiosyncratic take on “a Maori worldview” would take precedence over other worldviews, or (indeed) the norms of central banking across the world.

It is a little hard to make out quite what is going on and why. A cynic might suggest it was all just some sort of public service “brownwash”, designed to impress (say) the Labour Party’s Maori caucus and/or the editors and staff at Stuff. But it must be more than that. They seem sincere, about something or other. Recent minutes of the Bank’s Board meetings released under the OIA show that all these meetings now begin with a “karakia”, a prayer or ritual incantation. It isn’t clear which deities or spirits these incantations are addressed to, or whether atheists, Christian or Muslim Board members get to conscientiously object to addressing the spirits favoured by Messrs Orr and Quigley (the Board chair). But whoever they address, these meetings happen behind closed doors, only rarely given visibility through OIAs, so I guess we have to grant them some element of sincerity, about something or other.

But it seems to be about championing personal ideological agendas, visions of New Zealand perhaps, not policy that this policy agency is responsible for, all done using public funds, public time. And would be no more appropriate if some zealous Catholic-sympathising Governor were touting the importance of “a” Catholic worldview to this public institution, even if – as with the Governor and his “Maori worldview” – it made no difference to anything of substance at all. There is pomp and show, but nothing of substance that makes any discernible difference to how well or badly the Bank and the Governor do the job Parliament has assigned them.

Go through the Bank’s Monetary Policy Statements and the minutes of the MPC meetings. They might be (well, are) fairly poor quality by international standards, but there is nothing distinctively Maori, or reflective of “a Maori worldview” about them. Do the same for the FSRs, or Orr’s aggressive push a few years ago to raise bank capital requirements. Read the recent consultative document on the future monetary policy Remit, and there is nothing. Read – as I did – six months of Board minutes recently released under the OIA, and there is no intersection between issues of policy substance and anything about “a Maori worldview”.

The Bank has lost the taxpayer $8.4 billion so far (mark to market) on its LSAP position.

The Bank has published hardly any serious research in recent years

The Bank and the Minister got together to ban well-qualified people from being external MPC members

Speeches with any depth or authority on things the Bank is responsible for are notable by their absence.

We have the worst inflation outcomes for several decades

And we’ve learned that Orr, Quigley and Robertson got together and appointed to the incoming RB Board – working closely now on Bank matters – someone who is chair of a company that majority owns a significant New Zealand bank.

The Bank has been losing capable staff at an almost incredible rate, and now seems to have very few people with institutional experience and expertise in core policy areas

There is one failure or weakness after another. But there is no sign any of it has to do with Orr’s (non-Maori) passion for “a Maori worldview”; it is simply on him. His choices, his failures (his powers – the MPC is designed for him to dominate, and until 30 June all the other powers of the Bank rest solely with him personally). If the alternative stuff (climate change, alternative worldviews, incantations to tree gods) has any relevance, it is as a symptom of his unseriousness and unfitness for the job – distractions and shiny baubles when there was a day job to do, one that has recently presented the biggest substantive challenges in decades.

Shortly after the speech was delivered, another former Reserve Banker Geof Mortlock, who these days mostly does consultancy on bank regulation issues abroad, wrote to the Minister of Finance and the chairman of the Reserve Bank Board (copied widely) to lament the speech and urge Robertson and Quigley to act.

I agree with most of the thrust of what Geof has to say, and with his permission I have reproduced the full text below.

But asking Robertson and Quigley to sort out Orr is to miss the point that they are his enablers and authorisers. A serious government would not reappoint Orr. A serious Opposition would be hammering the inadequacies of the Governor’s performance and conduct on so many fronts. In unserious public New Zealand, reappointment is no doubt Orr’s for the asking.

Letter from Geof Mortlock to Grant Robertson and Neil Quigley

Dear Mr Quigley, Mr Robertson,

I am writing to you, copied to others, to express deep concern at the increasingly political role that the Reserve Bank governor is performing and the risk this presents to the credibility, professionalism and independence of the Reserve Bank. The most recent example of this is the speech Mr Orr gave to the Central Banking Global Summer Meetings 2022, entitled “Why we embraced Te Ao Maori“, published on 13 June this year.

As the title of the speech suggests, almost its entire focus is on matters Maori, including a potted (and far from accurate) history of the colonial development of New Zealand and its impact on Maori. It places heavy emphasis on Maori culture and language, and the supposed righting of wrongs of the past. In this speech, Orr continues his favourite theme of portraying the Reserve Bank as the Tane Mahuta of the financial landscape. This metaphor has received more public focus from Orr in the last two years or so than have the core functions for which he has responsibility (as can be seen from the few serious speeches he has given on core Reserve Bank functions, in contrast to the frequent commentary he makes on his eccentric and misleading Tane Mahuta metaphor).

For many, the continued prominent references to Tane Mahuta have become a source of considerable embarrassment given that the metaphor is wildly misleading and is of no relevance to the role of the Reserve Bank. For most observers of central bank issues, the metaphor of the Reserve Bank being Tane Mahuta fails completely to explain its role in the economy; rather, it confuses and misrepresents the Reserve Bank’s responsibilities in the economy and financial system. It is merely a politicisation of the Reserve Bank by a governor who, for his own reasons (whatever they might be), wants to use the platform he has to promote his narrative on Maori culture, language and symbolism.

If one wants to draw on the Tane Mahuta metaphor, I would argue that the Reserve Bank, as the ‘great tree god’ is actually casting far too much shade on the New Zealand financial ‘garden’ and inhibiting its growth and development through poorly designed and costed regulatory interventions (micro and macroprudential), excessive capital ratios on banks (which will contribute to a recession in 2023 in all probability), poorly designed financial crisis management arrangements, and a lack of analytical depth in its supervision role. Its excessive and unjustified asset purchase program is costing the taxpayer billions of wasted dollars and has fueled the fires of inflation. In other words, the great Tane Mahuta of the financial landscape is too often creating more problems than it solves, to the detriment of our financial ‘garden’. Some serious pruning of the tree is needed to resolve this, starting at the very top of the canopy. We might then see more sunlight play upon the ‘financial garden’ below, to the betterment of us all.

There is nothing of substance in Orr’s speech on the core functions of the Reserve Bank, such as monetary policy, promotion of financial stability, supervision of banks and insurers, oversight of the payment system, and management of the currency and foreign exchange reserves. Indeed, these core functions are treated by Orr as merely incidental distractions in this speech; it is all about the narrative he wants to promote on Maori culture, language, the Maori economy, and co-governance (based on a biased and contestable interpretation of the Treaty of Waitangi).

I imagine that the audience at this conference of central bankers would have been perplexed and bemused at this speech. They would have questioned its relevance to the core issues of the conference, such as the current global inflation surge, the threat that rising interest rates pose for highly leveraged countries, corporates and households, the risk of financial instability arising from asset quality deterioration, and the longer term threats to financial stability posed by climate change and fintech. These are all issues on which Orr could have contributed from a New Zealand perspective. They are all key, pressing issues that central banks globally and wider financial audiences are increasingly concerned about. Instead, Mr Orr dances with the forest fairies and devotes his entire speech (as shallow, sadly, as it was in analytical quality) on issues of zero relevance to the key challenges being faced by central banks, financial systems and the real economy in New Zealand and globally.