On Friday (1 July) the new Reserve Bank legislation comes fully into effect. The new Reserve Bank Board takes over from the Governor personally as the key governing body of the Bank, on all matters other than the conduct of monetary policy (but even there they have a big influence on the composition of the MPC). A member of the outgoing (advisory) Board told us – he sits on the RB pension fund trustees as, for my sins, do I – that the new Board is having its first meeting on Friday. And yet today is Tuesday and we still don’t know who is being appointed to this (on paper) powerful government board. Every Tuesday for the last couple of months I’ve checked Grant Robertson’s Beehive page, and still there is no announcement.

The Governor is a Board member ex officio. And several months the Bank slid onto their website the information that two members of the existing Board (including the chair) and one new person had been appointed to a “transition board” and would be appointed formally to the new Board. But the same web page still says

Neither the government nor the Bank seem to have been entirely straight on the matter, since an OIA release of Board minutes says that Suzanne Snively has also been appointed to the transition board, and has been attending meetings of the outgoing board. It is a curious appointment, both for her age (I’m not keen on a trend towards US-style gerontocracies) and for the fact that it is almost 40 years since Roger Douglas first appointed her to the Reserve Bank Board (back in the previous era when the Board held the formal powers). Media reports suggest she fell out with Douglas, and is much more ideologically aligned with the current version of the Labour Party and its not-Douglas Minister of Finance.

The other newbie we know about is Rodger Finlay. I wrote about his appointment a few weeks ago and there has since been some media coverage. Recall that the Bank was quite open in advertising that Finlay had been appointed to the transition board and was being appointed to the full Board even though he is chair of NZ Post, majority-owner of a New Zealand bank (Kiwibank) that just happens to be the weakest of the large banks in the system. The unadorned label “He is currently Chair of New Zealand Post” is still there this morning.

It was a highly inappropriate appointment, even though in response to questioning from a journalist the Minister of Finance’s office eventually advised that Finlay was ending his term with NZ Post on 30 June. [UPDATE: I’m advised this was actually passed on to the journalist quite readily by NZ Post itself.] If his appointment to the Reserve Bank early was really vital to the success of the new regime, he should have stepped down from the NZ Post role immediately, and neither Orr, Quigley nor Robertson should ever have countenanced anything different. Quigley told media that Finlay had been developing “new governance systems” for the Board, but if he had any real suitability for such a role – where ethics count hugely – he should have known from the start how inappropriate it was, and would look, for him to be serving the Reserve Bank in such a role while chairing the company that majority-owned a bank regulated by the Reserve Bank. For all that Quigley says they were aware of the issue all along, everything about how they operated suggests they took the narrowest legal interpretation, in a way they would no doubt look on askance if a regulated entity tried it on. (It doesn’t strengthen their case that NZ Post is also majority owner of Kiwi Wealth, a significant funds management operation even though that body is not regulated by the Reserve Bank.) As it is, documents released under the Official Information Act confirm that Finlay has been regularly attending meetings of the existing Reserve Bank Board and thus been party to all the information that board has had before it.

It is a poor look and reflects poorly on everyone involved – Minister, Governor, chair, Finlay, and (less severely) the other members of the outgoing board. Among other things, it raises doubts about the approach that these players might take in future. And also leaves us with the question as to how the consultation with other political parties – now required for Board appointees – went down as regards the Finlay appointment. I guess one day the OIA may shed some further light. It is all rather suggestive of a cavalier Wellington approach to conflicts of interest (and both actual and apparent matter).

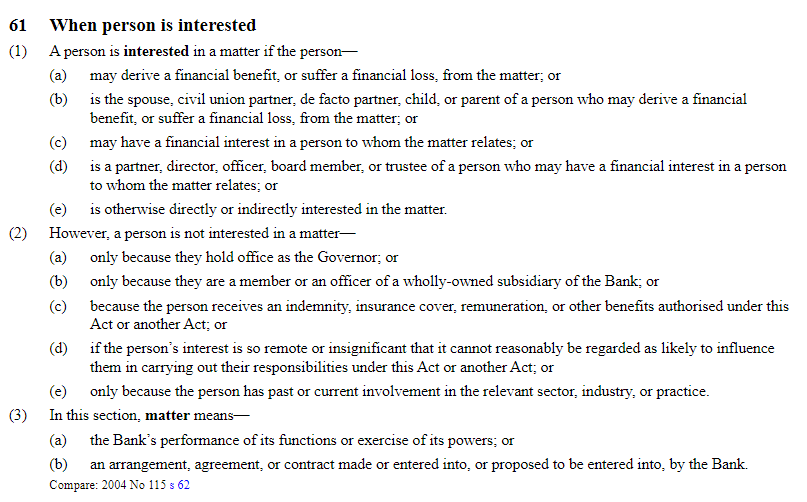

In my earlier post I included this section of the new legislation on the sort of people who can’t be Board members.

I have no problem with the provisions that are there. The problem is with what is not there. As I noted in the earlier post it is astonishing that a director or senior employee of a company that has a majority holding in a regulated entity (bank, insurer, deposit-taker etc) can be appointed to the Board, and can hold those two positions simultaneously. It is almost as concerning that someone who derived most of their income from work for one or more regulated entities (eg a partner of a law or accounting firm) can simultaneously be a director of the prudential regulatory agency.

But what I hadn’t noticed then (I guess my focus was elsewhere) was that there is no restriction at all on Reserve Bank board members holding ownership interests in regulated entities. According to this brand new law, I can’t be a director of a bank, insurer or finance company and simultaneously serve on the Reserve Bank Board (tick) but…..I could own a whole entity and do so. It is astonishing that Parliament has not protected us against the risk of such an appointment – so much so that one almost has to start asking why. Reserve Bank staff aren’t (or weren’t) allowed any such holdings, but it is the Board that makes the rules, sets priorities etc..

Before going further I should clarify two things: first, I’m sure no one wants to stop Board members (or staff) having totally passive interests through, say, a widely-offered Kiwisaver fund, or a passive NZ equities index fund. A caveat that no holding could be large enough it could credibly be regarded by a reasonable observer as likely to influence decisionmaking would seem sufficient to cover that. But that does not cover a 40 per cent stake in a finance company (say). And, second, the issue here is not a director might be engaging in deliberations specifically on a company s/he held a major stake in: I’m still willing to believe conflict of interest policies would require such a director to recuse him/herself from that specific discussion. But the Reserve Bank Board makes policy, applies policy, for broad classes of institutions, and no director with an ownership (or major income) interest in a regulated institution should be making policy for that class of institution, or contributing to internal discussion on the direction policy should go.

The new Act has a long list of provisions regarding conflicts of interest (from section 61). It starts reasonably enough

Any such conflict has to be disclosed to the chairperson – but not to the Board more generally, let alone the public.

And although the general provision is that a person cannot participate in a matter in which they have a conflict, there is explicit provision in the Act for the chair to waive that prohibition

Any such waiver has to be disclosed, but only in the Bank’s Annual Report, which may not be out for more than a year after such a waiver has been granted.

And one might have more confidence in the current chair, were he not complicit in the appointment of Rodger Finlay, while the latter was chair of the owner of a majority stake in a large bank.

More generally, there is a sense that these conflict of interest rules are written to cope with episodic events and conflicts that might arise, not really specifically foreseeably, in the course of a term on the Board. If the Board is looking to hire a consultant who is the husband or child of a Board member most probably that Board member would stand aside for that discussion/decision. But a Board member who owned half a finance company might reasonably claim that, having known of such an interest, the Minister had nonetheless lawfully appointed him/her, and that the conflict of interest rules would not apply to the Board’s general deliberations on policy for finance companies. Perhaps it would hold up, or perhaps not, but the government and Parliament should never have left such scope for uncertainty, the risk of highly inappropriate appointees (however capable), in the legislation. Section 31 (see above) should have been written a lot more restrictively.

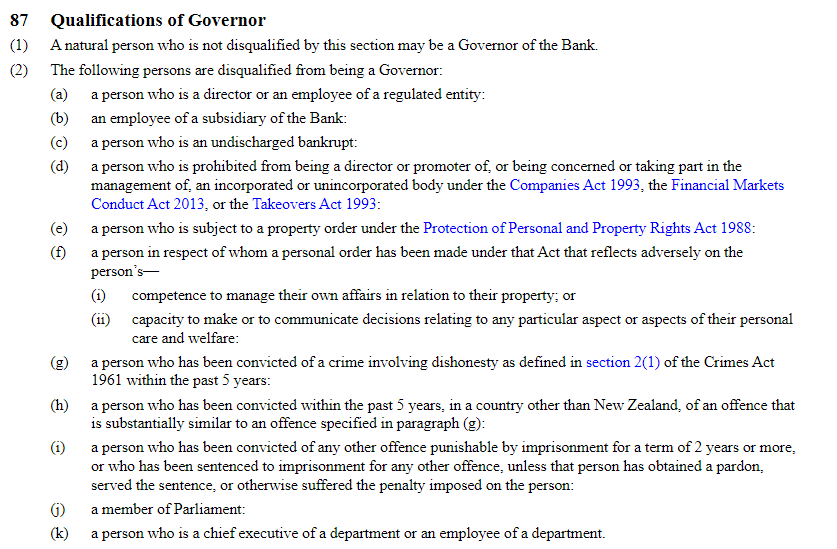

My concerns were only heightened when I happened to have a look at the clause in the Act governing the removal/dismissal of a Governor. These are the things that disqualify you from being Governor.

But notice that being a director of an entity that owns a regulated entity isn’t a disqualification. And neither is having a direct ownership interest in a regulated entity.

Was this an oversight? It appears not. These are just causes for which the Governor can be dismissed

1(g) looks like it should be reassuring. But, there is more

Parliament has explicitly written the Act to allow the Minister of Finance to agree with the Governor that the Governor can hold an “ownership interest in a regulated entity” while serving as Governor (all compounded by the fact that no such provision would be public information).

I am not, repeat not, suggesting anything shady between the current incumbents, but why would Parliament put such a provision in the Act (without at least one of those “trivial or incidental holdings arising from passive holdings in broad-based investment funds” type of caveats)? It is just a dreadful look.

Will any of these provisions necessarily be abused? No, not necessarily. But things have not gotten off to a good start with the Finlay appointment, which makes it difficult to have much confidence in the rigorous integrity of the people involved in these appointments etc, now and in the future. Maintaining a honest and uncorrupt system depends in no small part on sweating the small stuff, but Parliament should just never have left these matters in any doubt, apparently entirely reliant on successive ministers, Governors, Board members being interested in bending over backwards, even when it is inconvenient, to avoid the substance or appearance of conflict in our prudential regulator.

Meantime minister, where are the Board members for this shiny new goverance model? And where, in particular, are the members with real and in-depth expertise in banking, financial system regulation and so on?

Reblogged this on Utopia, you are standing in it!.

LikeLike

Gravedodger over at No Minister summed things up like so:

Rogernomics has been replaced by Robber nomics. (Spell checker would not let me run it as one word.)

What you say above makes this ring very true.

LikeLike