Today marks the end of an era at the Reserve Bank, as the last of the “Governor as single decisionmaker” model is dismantled, and tomorrow the new Board takes over the primary responsibility for the Bank’s affairs. The single decisionmaker model was an experiment, but with time it was increasingly apparent that it was a poor one, increasingly unfit for purpose. No other country reforming its central banking and bank etc regulatory arrangements followed us. It is to the government’s credit that they have moved the governance model for the Reserve Bank back towards the international mainstream (even if the specifics of the 2018 and 2021 are less than ideal, and in some respect a dog’s breakfast).

(NB note that most of the new Board, to take up office tomorrow, has not yet been appointed – or at least announced. With the new Board reportedly supposed to be meeting tomorrow, perhaps there is some launch announcement planned, but it is all a bit strange and not really that satisfactory.)

In this post I wanted to focus, perhaps for the last time (although they still apparently have an Annual Report to come), on the old Board. This should be the last day we see this graphic topping the Bank’s “Our Board of Directors” page

For 32+ years, taxpayers have paid a Board to (come for lunch and the cocktail do and) monitor and hold to account the Governor (and more latterly the MPC). They controlled who could be appointed as Governor and to the MPC, and – consistent with those accountability responsibilities – could recommend dismissal. The rules and responsibilities have changed a bit over time. For the first decade or more, the Governor chaired the Board, and even though there was a non-executive directors committee that was supposed to do the holding to account, the messaging implied by the structure wasn’t exactly crystal clear. And it wasn’t until about 20 years ago that the Board was required to make its own (public) Annual Report, but even then not very much changed – and consistent with that general observation, the Board’s report was buried in the midst of the (Governor-controlled) Bank Annual Report and was given no publicity when the Bank released its Annual Report.

There have been some able people on the Board at various times over the years. And some awkward people (the two may even have overlapped), but the institutional incentives very quickly developed into a model that meant few hard questions really got asked, little serious scrutiny happened, and the public never got any serious insight from the Board’s activities on their behalf (the Board, after all, had access to papers the Bank jealously guards for years and years after they were relevant, and can engage and challenge the Governor and other decisionmakers). I say “very quickly developed” because in the earliest years of the regime there was a view – shared by the Governor – that the inflation targeting governance regime was relatively mechanical and that a Governor might reasonably expect to lose his/her job if inflation overshot the target range. The first (apparent) breaches in about 1995 prompted some hard questions, some letters to the Minister, but eventually a recognition that the whole thing involved a lot more judgement and discretion if sensible policy was to ensue. There was a recognition that the target was something to be “constantly aiming at”.

Unfortunately for the Board, had they ever aspired to do the job really well they didn’t have the resources to do so. It became customary to have one professional economist on the Board (first Viv Hall, then Arthur Grimes, more recently Neil Quigley), but Board members didn’t get paid much themselves, had no direct access to staff resources, had no budget to commission independent professional advice, and their own Secretary was for the most of time a senior staffer of the Governor. Board meetings occurred on Bank premises, and one entered the Board room past the row of oil paintings of former Governors. And once the Board got its own chair – chosen by them, not the Minister – for 13 years they opted to have as their chair former RB staffers, first Arthur Grimes, and second Rod Carr. Most of the Board members knew about being on corporate boards – where they had decision-making powers – and so there seemed to be a tendency to default towards the sorts of issues they might have dealt with as corporate board members. Monetary policy and financial stability/regulation were not high among them. Arms-length challenge and scrutiny also weren’t really among those functions – on a corporate board, the board has far more ownership of the firm’s strategy (something the Act never envisaged for the RB – the Board had no say, for example, in Policy Targets Agreements or the conduct of monetary policy).

And so acting as cover for management seems to have become the default mode – most especially externally but, as far as we can tell, often internally as well. Some Board members had their own agendas – some more laudable than others – but there was never much sign of a sustained effort to hold the Governor and Bank to account, to act as if they represented the government and people of New Zealand rather than the Bank management (notably whoever was the Governor at the time). At times, their Annual Reports even talked about helping with the Bank’s external relations (for example, at the functions held around Board meetings outside Wellington).

I could develop some anecdotes at length, including for example, the board member who used to ring me up (while I was still on staff) for inside angles on monetary policy and the Governor, at a time when that member was attempting to mark out an independent position (oops, he is now the Board chair). But I’ll largely leave it at that. I don’t think anyone – perhaps with the exception of some individual Board members – thinks the Board ever really did the job it was designed for. You could be attacked in public by the Governor – for exposing an OCR leak, resulting from weak management systems – and an approach to the Board still resulted only in them gathering in behind the Governor. Are we to suppose it was any different when Orr was attacking his critics around the bank capital plans in ways that few regarded as represented expected conduct from a Governor?

But what interested me was how they had handled the events of the last year or so. The Bank has run up massive losses on the LSAP. Inflation – headline and core – has shot through the top of the target range. All in all it is has been one of most interesting – and surely questionworthy – periods in the 30 years the Board had the monitoring and accountability responsibility. You might think the outgoing Board would want to end well.

A while ago I lodged an OIA requesting the Board minutes for the period November 2021 to April 2022. About the time those results came back I found on the Bank’s website the results of someone else’s OIA for the minutes for September to November 2021. So we have a run of several months of minutes, over a period when things moved a lot on monetary policy (actual inflation, the OCR, forecast inflation – oh, and those LSAP losses). We might have hoped for a lot of evidence of hard questioning, challenge, and serious scrutiny.

Well, might have if we had known nothing of the previous 30 years.

The Bank – or Board – is relatively open in what they release, so we get a good sense of the complete minutes. There are some questions about what they write down, but even there they seem to have improved (relative to earlier concerns that in some areas they were in flagrant breach of the Public Records Act).

What do we learn?

The first meeting was in early September, not long after the August MPS (which itself came the day after the lockdown was announced). The minutes are seven pages long, and we learn a fair bit about the People and Culture report, the Enterprise Risk Management report, the Governor’s activities, and even the RB superannuation scheme (which the Board had some particular non-statutory responsibilities for). Monetary policy gets half a page

Only one Board member is reported as saying anything (“noted” not exactly being a strong form of questioning) and none seems to have challenged the (soon to be restructured out) Chief Economist’s view that the Bank had plenty of time and didn’t need to act (much/) until it had a seen a full 12 months of data. The Governor – the most influential MPC member – is not reported as having said anything.

The late-October meeting minutes took eight pages. We learned quite a lot of various administrative and/or extraneous matters, including the Bank’s climate change strategy. There was quite a discussion on the forthcoming FInancial Stability Report, but no sign of any serious challenge or scrutiny from Board members, on requests for follow-up papers etc. And then we got to monetary policy, the OCR having just been raised for the first time.

I’m sure it was all very pleasant, but there is no sign of any hard questioning about immediately relevant issues (or perhaps the Public Records Act is being ignored again). No one seems to have challenged them as to whether, just possibly, if inflation was already above the midpoint and employment at or above midpoint, and forecasters had been taken considerably by surprise, whether a more aggressive stance might be warranted. No one seems to have challenged Ha on his complacent comment the previous month, despite (presumably) just having confirmed those minutes.

At the November meeting there appears to have been no discussion of monetary policy at all (although the Board was at pains to stress the importance of the outgoing Board having time to prepare their final Annual Report). Not a word. And, of course, still no mention at all of those mounting LSAP losses – and the Board is supposed to have been agents of the minister and the public, not of the Governor.

For the December meeting this is what the minutes record

All of which may have made for quite an interesting discussion, but as the Governor is recorded pointing out, monetary policy has to act given what is happening to fiscal policy (fiscal policy is not something the Governor or Board are responsible for). But there is no sign of any unease, of even a single Board member challenging the Bank to show that it was on the right track or that inflation would come out something like forecast. There is just no sense of holding powerful decisionmakers to account in particularly troubling times. Just a chat, with one’s friends and colleagues.

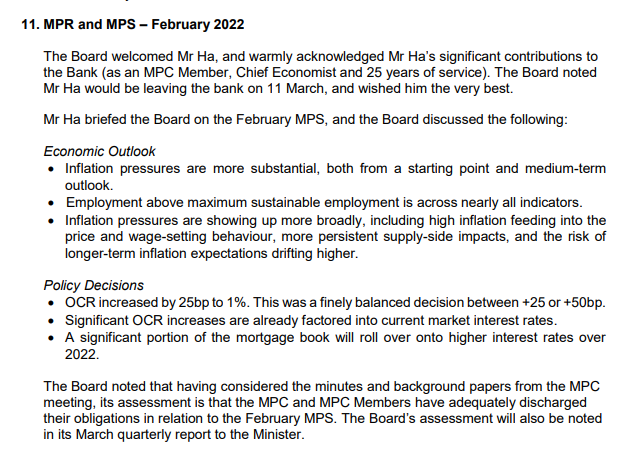

At the February meeting, this is all there was about monetary policy

Again interesting (if brief) but with not the slightest sense of unease or challenge, no pressure on the Governor or his colleagues.

In March

Were some future historian to stumble across these minutes, but not the relevant parts of the Act, they might have assumed that the Board had just a right to be briefed, but no responsibility for ensuring the Governor and the MPC are held to account.

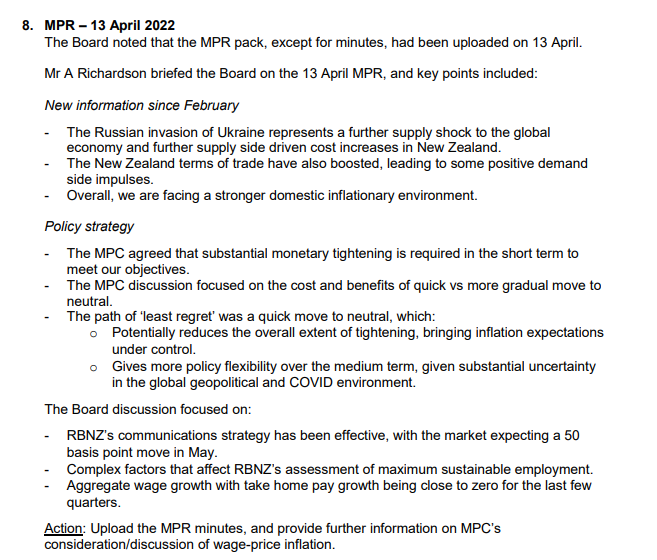

And finally in this sequence, the April meeting

It is, I’m sure, interesting enough, but it scarcely counts as evidence of accountability.

Now, it is always possible that there are secret unrecorded discussions (in breach of the Public Records Act). The other OIA requester asked for a copy of one of the Board’s reports to the Minister, which the Board/Bank adamantly refused to release

That should be unacceptable: the Governor and MPC are statutorily accountable via the Board, and the idea that management might refuse to supply information to the Board because the Board’s report – even with some redactions – to the Minister might be released (with some lag) should have been unacceptable. But we needn’t worry that there might be anything very revealing in such a report: take a look at the March Board extract above, and you’ll see they record there that they were going to tell the Minister all was fine.

At one level, knowing what we do as to how the Board has operated over 30 years, none of this should be too surprising. But it doesn’t reflect well on them (any of them). We have a chair presumably focused mostly on working with the Governor to see in the new act (questionable appointments and all), and so hardly likely to make himself awkward on current monetary policy, and other Board members with neither the expertise, inclination, nor institutional culture to ask hard questions. But still….across all those months

- no record of a single hard question,

- no sign of any sustained engagement at all with the external MPC members (whom they are supposed to individually hold to account)

- no requests for supplementary papers,

- no suggestions of commissioning independent analysis,

- not a single mention of the huge (and mounting over this period) LSAP losses,

- no suggestion of any regrets about anything.

It is easy to be inured to flawed frameworks and the weaknesses they generate, but this really isn’t good enough. These people took the taxpayers’ money (no much admittedly, but they each took the deal) and seem barely to have been focused at all on their monetary policy accountability duties, through one of the biggest monetary policy disruptions for decades. Perhaps I should ask for the minutes of meetings of the previous 20 months, but it would be a real surprise if anything had been different then.

The Bank itself appears little better, since there is no evidence in any of these minutes of robust or independent analyses and reviews of what had gone well, and what badly, why for examples forecasts had been so wrong, and what lessons staff and management had taken. And so we are in the weird position that the Bank has a consultation paper out at present on the future Monetary Policy Remit, and yet tells us that the review they are finally doing of the last couple of years stewardship may not even be released before the second round of consultation closes.

The Board has proved useless. It was always likely given the incentives and flawed structures, but that is no excuse for any of the members. The job was there to be done, and they have not been doing it (most notably over the dramatic times of the last 12 months).

The end of the era will be no loss. We can only wait and watch and see how the new Board does – when the Minister finally manages to dredge up enough people willing to do the job to get a full complement on board.

We have far too many boards, commissions and other public sector bodies run by committees. This means there are literally hundreds of appointments that have to be made every year, and it is a real struggle finding decent people for all these positions.

Then, like you have discussed, they usually have the wrong incentives with a pretty much guaranteed tenure and no link to the performance of the organisation they are governing. Typically they spent far too much time debating trivial issues and indulging in one-upmanship (the women as well) than discussing the important issues.

I would argue that for most of the organisations with such ‘boards’ that all the day-to-day decisions should be made by a committee of senior staff (who usually have more expertise than ‘board members’).

The RB is unusual, though, in how much power has been vested in the Governor – CEs of public entities are not normally as involved in all aspects of operations and decision making.

LikeLiked by 1 person

Qui tacet consentire videtur, ubi loqui debuit ac potuit

LikeLiked by 1 person

Reblogged this on Utopia, you are standing in it!.

LikeLike