From a macroeconomic point of view, that title for this post really sums things up nicely.

Take policy first. The government has brought down a Budget that projects an operating deficit (excluding gains and losses) of 1.7 per cent of GDP for the 2022/23 year that starts a few weeks from now. Perhaps that deficit might not sound much to the typical voter but operating deficits always need to be considered against the backdrop of the economy.

Over the last couple of years we had huge economic disruptions on account of Covid, lockdowns etc, and fiscal deficits were a sensible part of handling those disruptions (eg paying people to stay at home and reduce the societal spread of the virus). Whatever the merits of some individual items of spending over that period, hardly anyone is going to quibble with the fact of deficits.

But where are we now (or, more specifically, where were we when Treasury did the economic forecasts that underpin yesterday’s numbers, and which Cabinet had when it made final Budget decisions)? Treasury has the terms of trade still near record highs, it has the unemployment rate falling a bit further below levels the Reserve Bank has already suggested are unsustainable, and over 22/23 it expects an economywide output gap (activity running ahead of “potential”) of about 2 per cent of GDP. In short, on the Treasury numbers the economy is overheated. And when economies are overheated revenue floods in. Surprise inflations – of the sort we’ve seen – do even more favours to the government accounts in the near-term: debt was issued when lenders thought inflation would be low, and although the revenue floods in (GST and income and company tax), it takes a while for (notably) public sector wages to catch up. On this macro outlook, the government should have been making fiscal policy choices that led to projected surpluses in 22/23 (perhaps 1-2 per cent of GDP), consistent with the idea – not really an right vs left issue – that operating balances, cyclically-adjusted – should not be in deficit. Big government or small govt, on average across the cycle operating spending should be paid for tax (and other) revenue.

Instead in an economy that is grossly overheated (on the Treasury projections) the government chooses to run material operating deficits. It is the first time in many decades a New Zealand government (National or Labour) has done such a thing, and should not be encouraged. It risks representing slippage from 30 years of prudent fiscal management by both parties, and once one party breaches those disciplines the incentives aren’t great for the other once it takes office.

And this indiscipline isn’t even occurring in election year (and already I’m getting an election bribe). It is fine to talk up projections of smaller deficits next year, but slotting a number in a spreadsheet is a rather different than making the harder spending or revenue decisions to fit within those constraints. Perhaps they’ll do it. Who knows. The political incentives may be even more intense by then. And the economic environment could be (probably will be) quite different.. What any government should be directly accountable for is their plans for the immediately-upon-us fiscal year.

You will hear people suggest that fiscal policy isn’t anything to worry about. Some like to quote The Treasury’s fiscal impulse measure/chart. But it just isn’t a particularly useful or meaningful measure at present (at least unless you line up against it a Covid “impulse” chart). But even if you want to believe that the overall direction of fiscal policy wasn’t too bad – and my comments on the HYEFU/BPS were not inconsistent with such an interpretation – the real impulse we should be focused on is how near-term fiscal policy has changed since December.

In December, the operating deficit for 2022/23 was projected at 0.2 per cent of GDP (allow for some margins of uncertainty and you could call it balanced). Now the projected deficit is 1.7 per cent of GDP, in an economy projected to be even more overheated that was projected in December.

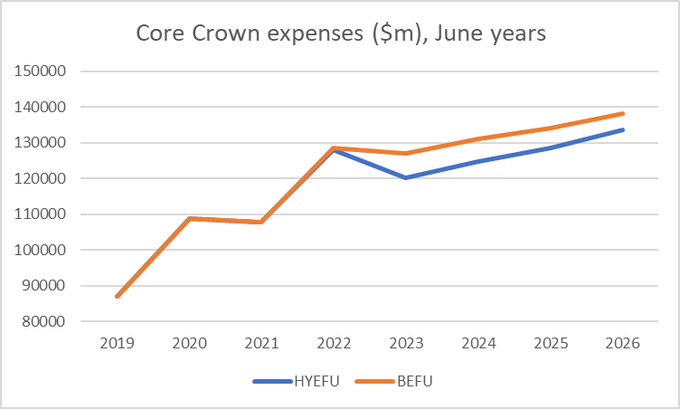

What about spending? Well, here are the projections for core Crown spending. Back in December the government planned that spending in 22/23 would be a lot lower than in 21/22 (which made sense since no more expensive lockdowns were being planned for). Yesterday’s projections for 22/23 are $6.8bn higher than what was projected only six months ago – and only about a billion less than last year’s heavy Covid-driven spending.

Some of it is inflation, but whereas in December Treasury projected that spending would be 30.5 per cent of GDP, now it is projected to be 31.6 per cent of GDP. It is a lot more spending and, all else equal, a lot more pressure on the economy and inflation. In case you are wondering, in both sets of projections tax revenue is projected to be 28.9 per cent of GDP.

Perhaps there is a really robust case for all this extra spending, making it so much more valuable and important than the private spending that will have to be squeezed out. But the evidence for any such claim is slight to non-existent, and the general presumption should be that if you want to spend a lot more you do the honest thing and make the case for higher tax rates. Instead, the Cabinet has chosen operating deficits amid a seriously overheated economy. It is cavalier and irresponsible.

That is policy, things ministers are directly accountable for. But there is also a full set of economic projections, amid which there are some quite disconcerting numbers. Now, before proceeding, it is worth stressing that these economic projections were finalised a long time ago, on 24 March in fact. If anything, that only makes things more concerning.

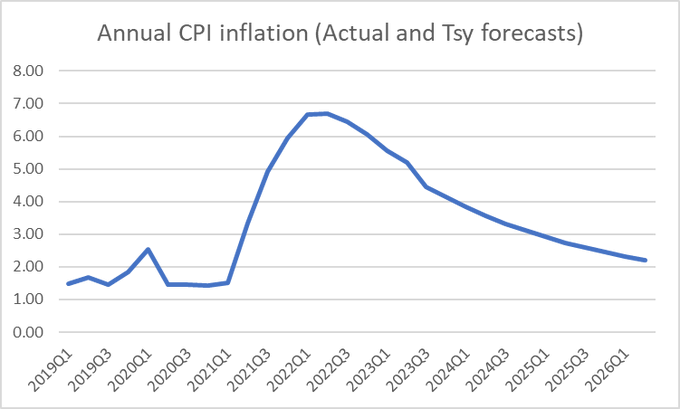

Here are The Treasury’s inflation forecasts

You will recall that the government has given the Reserve Bank an inflation target range of 1-3 per cent per annum but with an explicit instruction to focus on the midpoint of that range, 2 per cent annual CPI inflation. You should be aware that monetary policy doesn’t work instantly, with the full effects on inflation of monetary policy choices today not being seen for perhaps 18 months or even a bit longer. You should also be aware that The Treasury (and other forecasters) generally don’t include future supply etc shocks in their forecasts, because they are basically unknowable (and could go either way). So (a) any annual inflation forecasts more a few quarters ahead will be wholly a reflection of fundamentals (expectations, capacity pressures, and perhaps some small exchange rate effects), and (b) any forecast annual inflation rate 18 months or more ahead is almost wholly a policy choice. Actions could be taken now to get/keep inflation around the midpoint of the target range.

But Treasury forecasts inflation for calendar 2023 at 4.1 per cent – as it happens reasonably similar to many estimates of core inflation right now – and 3.1 per cent for calendar 2024 (December 2024 was the best part of 3 years ahead when Treasury finished the forecasts). Only at the very end of the forecasts – four years away – is inflation back to 2.2 per cent, close enough to the target midpoint that we might reasonably be content. It is a choice to forecast that the Reserve Bank’s MPC will simply not be serious in showing any urgency in getting inflation down, and seems barely to engage with the risk of entrenching expectations of higher future inflation. If one takes the annual numbers on the summary table, it is still a couple of years before they even expect the Reserve Bank to be delivering an OCR that is positive in inflation-adjusted (real) terms.

Now, The Treasury does not set the OCR, the Reserve Bank does that. But the Secretary to the Treasury is a non-voting member of the MPC, The Treasury is the government’s chief adviser on macroeconomic policy including monetary policy targets and performance. And they finished these projections two months ago, and will have shared them with the Minister of Finance and with the Reserve Bank. At very least, there should have been a “please explain” from the Minister to the Governor/MPC. Treasury might have been quite wrong, but if so the Bank should have had a compelling response. But it doesn’t seem likely that anything of the sort happened, and you may recall that when the Bank last reviewed the OCR they explicitly said they weren’t seeing any more inflation than they’d projected in February.

The Treasury numbers are doubly disconcerting because – finished in March – they are persistently higher than the expectations (late April) of the Reserve Bank’s semi-expert panel in the quarterly survey. For the year to March 2024, the survey of expectations reported expected inflation of 3.3 per cent, but The Treasury projects 3.8 per cent inflation.

Now, maybe this will all be overtaken by events. The forecasts were completed in late March, and since then the economic mood – here and abroad – has deteriorated quite markedly, with a growing focus on the likelihood of a recession (almost everywhere significant reductions in core inflation have involved recessions). Quite possibly, if the projections were being done today they would be weaker than those published yesterday (and the RB’s will be finalised about now) But I hope journalists and MPs are getting ready to compare and contrast the RB and Treasury forecasts and to ask hard questions about the differences.

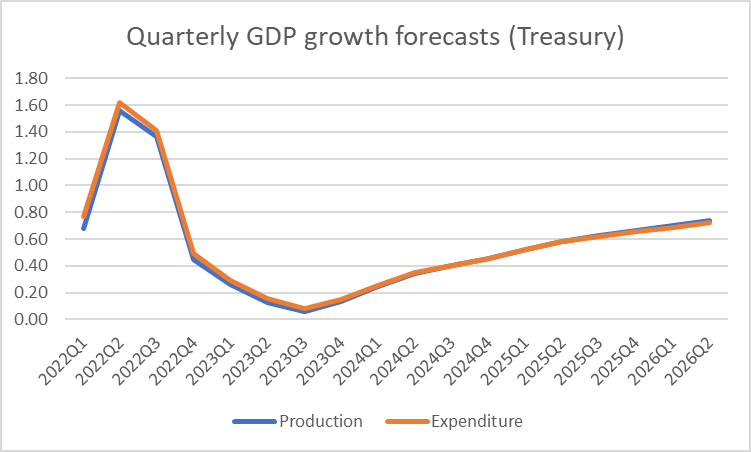

Soft-landings rarely ever happen once core inflation has risen quite a bit (as it clearly has this time). That doesn’t stop forecasters forecasting them, but if forecasters knew the true model well enough we probably wouldn’t have had the inflation breakout in the first place. I was, however, particularly struck by The Treasury’s quarterly GDP growth forecasts, which ever so narrowly avoid a negative quarter in Q3 next year (as the election campaign is likely to be getting into full swing). I’m not suggesting Treasury overtly politicised the forecasts, but had they assumed a monetary policy reaction more consistent with returning inflation to target quickly (say, under 3 per cent for 2023, which seems a reasonable interim goal at this point), the headlines might have been rather different.

I’m going to end with two charts that have little or nothing to do with short-run macroeconomic policy management.

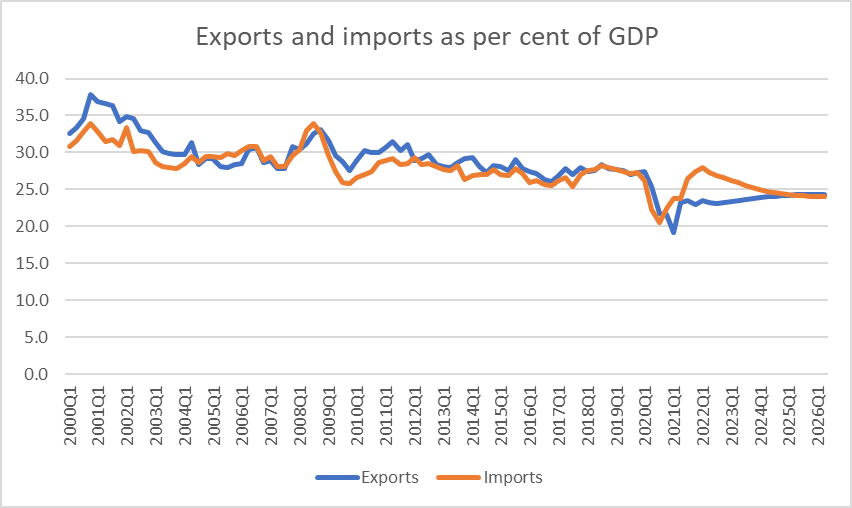

This one shows The Treasury’s projections for (nominal) exports and imports as a share of GDP.

Of course, with closed borders for the last couple of years we saw a sharp dip in both exports and imports as a share of GDP. But the end point for these projections is four years ahead. For both imports and exports, the shares settle materially below pre-Covid levels, in series that have been going backwards for decades. No doubt the Greens would prefer we all stopped flying, but successful economies have tended to feature – as one aspect of their success – rising import and export shares of GDP.

The Budget talked of a focus on creating a “high wage economy”. Sadly, all I could see in the documents that might warrant that claim was the expectation of continued high inflation – which will raise nominal wages a lot, but do nothing for actual material living standards.

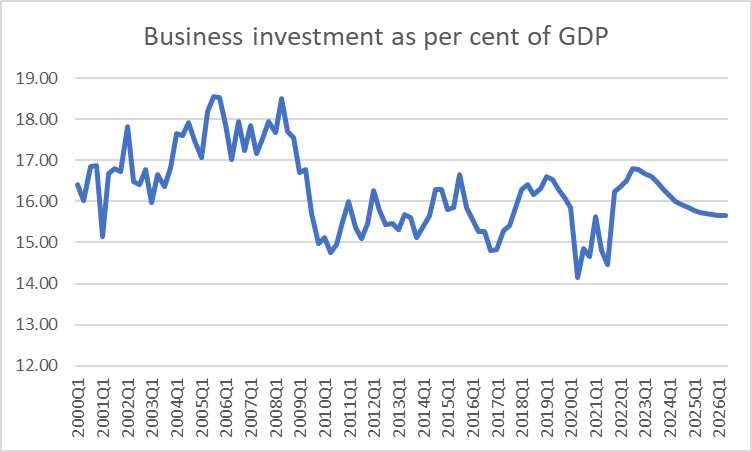

One of the striking features of the last decade was how relatively weak business investment as a share of GDP had been. Firms invest in response to opportunities, and the absence of much investment is usually a reflection on the wider economic and policy environment (much as bureaucrats like to think they know better, few firms just leave profitable opportunities sitting unexploited). For what is worth – and all the corporate welfare notwithstanding – The Treasury doesn’t see the outlook for business investment any better this decade than last.

And so in time will pass yet another New Zealand government that has done nothing to reverse decades of productivity growth underperformance. If that is depressing enough, this government seems to be in the process of unravelling the foundations of what had been a fairly enviable reputation for fiscal discipline and overall macroeconomic management. The situation can be recovered, but there is no sign in this Budget that the government much cares. And it isn’t even election year yet.

Reblogged this on Utopia, you are standing in it!.

LikeLiked by 1 person

Well, let’s look on the bright side shall we? At least the government has generously provided by means of helicopter money the price of a one way ticket to Australia for the many who will choose to leave the sinking ship.

LikeLiked by 3 people

I know you are an economist – interested basically in how money works or does not work for the good of all – but… I don’t recall a single word from you on the existential issues of our times, global warming, loss/destruction of the biosphere and our relentless consumption of planet Earth. It is abundantly apparent that right now the world is moving into an exponential phase as the consequences of our unrestrained consumption, but the fundamental tenet of your blogs points to the importance of maintaining/encouraging/growing consumption for the benefit of the economy.

India/Pakistan suffer from an unprecedented heatwave and threatens to become uninhabitable, Aust. from extreme flood consequences of the current la Nina cycle, our own East Coast has had a succession of destructive flood events, Westport 2 floods in 18 months threatens its future, the north polar icecap is melting away, unprecedented ocean heat wave is killing off an underwater ecosystem in our Fiordland as well as threatening the existence of the Great Barrier reef.

Meanwhile you and the whole world of economists (with a few notable exceptions) talk of nothing but how to maximise growth and consumption. Our grandchildren will want to know why.

LikeLike

There are a lot of potential responses to that, but perhaps I’d just observe that a political party that came out campaigning on making NZers poorer, or even just settling for no growth from here, would seem unlikely to do very well, and revealed preference also suggests that countries that lag behind see many of their own people leaving for greener pastures (well, browner but still richer ones in the case of the NZ flow towards Australia).

LikeLiked by 1 person

Geoff Prickett: I share your concern about consumption of finite resources; I share your belief in man-made global warming; I agree we should be doing something about both. However, it really bugs me to yet again see confusion between weather and climate change. Spectacular weather events will occur with or without mankind – they are a purely statistical phenomena; take enough measurements over a large enough area and spikes will occur.

When hurricane Katrina hit New Orleans in 2005 the media said it was a sign of global warming and only the beginning of worse to come. They never mention that the next decade had fewer hurricanes hit USA than ever before. Using recent weather events as support for a theory of climate change is wrong because it opens the debate to counter-arguments (the biggest storm to hit Europe was 1703; the areas burnt in forest fires was worse before the war; the number of people killed by weather events is declining; if Auckland warmed by an average of 8 degrees it would still be cooler than Cairns; etc). Please stick to the underlying science: the CO2 readings at Mauna Loa Observatory; the very slow but only recently perceptible change in deep ocean temperatures. These are facts that scare me whereas your floods just remind me of the floods that hit East Anglia when I was very young.

There are historical examples of finite resources being fully consumed. The Romans prized silphium as worth its weight in gold; it was traded and they made it extinct. How should finite resources be rationed – what is the economists answer?

LikeLike

“the existential issues of our times, global warming”

Where did you get that idea Geoff, even the IPCC, cheerleaders for the catastrophists have not said that. Considering that humanity survives, flourishes even, from polar areas to steaming tropical rain forests you don’t think “existential” is overdoing it a bit. I don’t blame you for having been mislead, have you considered the possibility that you’re the victim of a pervasive propaganda campaign. Our entire legacy news media have signed up as partners with the Covering Climate Now outfit; an outfit solely committed to instilling the terror you’re expressing.

Even questioning the narrative is verboten on the pages and screens of our self declared “one source of truth” media.

Here is their hall of shame, our lot amongst them: https://coveringclimatenow.org/partners/partner-list/

The real danger lies in the mad ideas being put forward in attempts to control the climate. The Green New Deal proposed effectively ending fossil fuel use and extraction, aviation, long haul trucking, modern agriculture and much more. We don’t hear much about that now; someone has run the numbers and the truth is that those proposals would lead to a catastrophic, and possibly terminal, economic and social collapse. Adoption of those policies and we really would have an existential crisis.

The disastrous results of the Sri Lankan (delusional socialist) government’s decision to impose just some of those measures gives an idea of the likely problems. At least there is some resilience in folk that can fall back on subsistence agriculture. The population of our cities are as dependant as babies, dependant on a complex web of supply that is itself dependant on abundant, inexpensive energy. It might be comforting, to some, to imagine that dicking around in an office, producing little or nothing useful entitles them to the abundance we ungraciously expect. They’re wrong.

,

LikeLike

If I were minister, id want to know why the Treasury forecasts are so bullish on growth. Private consumption is about 60% of GDP and consumers are in a foul mood, for good reason.

Total economy wide employment cant really increase much given the high participation rate and low unemployment but real wages are falling with wage growth running well below inflation; so real disposable income growth is falling. Households can smooth consumption via transfer payments – and the government has provided a small top up but net, the withdrawal of COVID support means transfer payments are a drag on income too. They can consume out of wealth, but with house and stock prices falling, interest rates rising and banks unwilling to provide credit, that channel is probably also contracting. And they can consume from savings, but the savings rate is low, those who have savings are probably likely to want to hold onto them while those who don’t have savings are credit constrained.

So why the optimism? Real wages, fiscal transfers, house prices, interest rates, consumer confidence all point to a potentially bone crushing recession. And the payment shock to the mortgage belt is only just starting. Moreover, if forward starting swaps are realised and lending spreads normalise, the one year fixed rate is going to 6-6.5% in a year.

For mine, NZ looks utterly stuffed.

LikeLike

One would hope that Tsy’s view now would be quite a lot more pessimistic than it was 2 months ago when the BEFU forecasts were finalised. One caveat to your take on households is that wage inflation does now appear to be picking up quite fast.

LikeLike

Michael

I think your points about Government showing a lack of interest in business investment and the relaxed attitude to inflation are well made, but Im not so sure about your view that Government is remiss for not having slammed on the brakes on spending in FY23.

Treasury figures indicate that spending will be down in FY23 relative to FY22 and as a % of GDP the drop is from circa 35% to 32%. I take your point that there isnt a macro case for government deficits right now, but governments can’t just stop spending.

Your point about FY24-26 spending increases seem more reasonable, although the increases in spend are less than projected GDP growth which sees Government’s share of the pie fall to 30% (recognising that several things have to go right for that to happen).

I feel the bigger issues with this budget are the quality of spend. Ive not seen a breakdown of where the money is going but it certainly feels that more is heading for handouts (and interest) than hand-ups.

Tim

LikeLike

Certainly agree re the quality of the spend (said, inter alia, as a not-at-all needy recipient of the $350 handout).

On overall spending, I’m not suggesting they should have “slammed on the brakes” on spending. Had they stuck with their plans in Dec, spending as a share of GDP for 22/23 would have been materially lower than is now projected. The big drop from 21/22 would have happened more or less naturally – Covid support spending itself ended as lockdowns/MIQ did – but on the other hand the ending of Covid restrictions etc freed up private spending again (the point I was, somewhat cryptically, trying to get at with my comment that Tsy’s fiscal impulse measure would need to be read alongside a “Covid restrictions impulse measure”).

LikeLike

Agree with your comments

In addition:

Use of “ printed “money for pandemic relief is one thing,Using the same money tor other mostly poor quality spends as in the annual budget is totally another.

This is this governments self acknowledged action ,to use the funding put aside for the pandemic and not used for that . This can only make inflation worse.

It seems they are trying to inflate their way out of the economic hole they themselves dug!

LikeLike

In reply to Bob Atkinson. I am well aware of the difference between climate and weather but is is nonsense to suggest that climate has no effect on weather. A 1degree increase in atmospheric temp means the atmosphere can hold 7% more water – that’s just physics. I farmed up in the East Coast hills for 50 years thru’ events like Bola and I am well aware of fickle nature of weather.

I stick to the word exponential. The increase in atmospheric CO2 has been measured and the risks discussed here in NZ for 50 years – read Dave Lowe’s “The Alarmist” , Lowe has been measuring atmospheric CO2 for 50 years and warning of the consequences. But the consequences are not lineal, for a long time the climatic change was slower than expected because of nature’s resilience. Now we have global feed-back loops caused by Arctic ice melt, increasing forest fires, oceanic warming etc. The climatic consequences are ramping up before our eyes. Historic floods/droughts/storms of the past that you talk of are becoming commonplace. The recent floods in Germany washed away 700 year old houses.

Incidentally you comment on an 8degree rise in Auckland’s temp begs the question what will be the commensurate temperature in south Asia, the Mediterranean, Africa – the answer is probably uninhabitable.

David George – ditto. Exponential is the word for where global warming is right now. The feed-back loops are kicking in. Would it be fair to assume that most of those with the time and inclination to read dry economic discussions would be of an older demographic and won’t be around when our descendants look at the desperate situation they inherit and ask, “What the hell were they thinking of to let this happen”?

And finally Michael – I wonder if last weekends Oz election and the 9 seats taken by committed independents on a platform which included a demand for climate action didn’t offer a glimmer of hope on the political front. Yes, I know the politics is desperately difficult – people vote for the here and now. The future has no value, not helped by an economics profession which appears incapable of defining one.

LikeLike

It will be interesting to interpret the Aus election results a little down the track. As I understand it the Aus Labor Party had a fairly unradical offering (over all), and of course the Aus economy is overheated at present (as here). If (say) the Democrats have a bad year in the mid terms and (say) Labour/Greens lose here next year (and Johnson in 24) perhaps we’ll look back and see it mostly as an anti-incumbency reaction. Lots of “ifs” there – so just speculation – but I also didn’t get the sense many of the teals were actually suggesting an end to growth or reduction in material living stds.

LikeLike

I have to disagree Geoff, the conflation of climate with weather events is being actively promoted, worse it’s being presented as, ipso facto, caused by human induced climate change.

There have always been extreme weather events somewhere in the world – droughts, storms floods. They are, if anything, less common or severe now but the story that they are is the narrative. Every event is magnified and dramatised; the dreaded phrase “Climate Change” strategically inserted.

One recent example: the Australian 2019/20 bush fires were widely presented as both unprecedented and the direct result of human induced climate change. Permanent drought (subsequently there has been abundant rain), the dams will never be filled, this is the new normal, we’re on the edge of Armageddon!

The twenty odd million hectares burned in that season were never compared to the 120 million burned in the ’74/75 season, a time when the worry of the day was an approaching ice age after thirty years of global cooling.

The 2021 Netherlands floods (no Dutch fatalities) you refer to were also blatantly reported as unprecedented and CC related, never mind the 1953 event that cost the lives of 2,000 or the Great Storm of 1703 with a hundred thousand deaths. The modern flood protection efforts no doubt played a part but read the terrible statistics of prior events and perhaps exercise a little scepticism with the narrative we’re being fed.

https://en.wikipedia.org/wiki/List_of_floods_in_the_Netherlands

We are clearly being, by omission and commission, blatantly manipulated and lied to.

The global climate feedbacks are almost infinitely complex and largely unquantifiable. The big one, increased moisture vapour, is often cited. Unfortunately for the alarmist cause the moisture vapour manifests as cloud, sufficient it now appears to entirely negate the assumed warming due to the increased albedo of the greater cloud cover – natures sun shade? The CO2 effect itself is small – and severely restricted by it’s limitation to a very narrow part of outgoing infra red radiation. Far from being an exponentially increasing effect. It’s not even a linear increase but an exponentially decreasingly rate of effect – that is why the scientists use doubling rates (geometric progression) not linear (arithmetic) progression in their calculations. The CO2 temperature effect (warming) is the same going from 200 to 400ppm as it is going from 400 to 800ppm for example.

Even ignoring that we started from a pre industrial base coincident with the end of the little ice age there has been a 1.1 degree temperature change that could possibly be attributed to AGW. Assuming for now that that is the cause, we’ve used most of our bequeathment of easily obtained oil and burned off vast areas of forest to get there. Doubling atmospheric CO2 from here is not really possible. Nothing to worry about IOW.

LikeLike