From a macroeconomic point of view, that title for this post really sums things up nicely.

Take policy first. The government has brought down a Budget that projects an operating deficit (excluding gains and losses) of 1.7 per cent of GDP for the 2022/23 year that starts a few weeks from now. Perhaps that deficit might not sound much to the typical voter but operating deficits always need to be considered against the backdrop of the economy.

Over the last couple of years we had huge economic disruptions on account of Covid, lockdowns etc, and fiscal deficits were a sensible part of handling those disruptions (eg paying people to stay at home and reduce the societal spread of the virus). Whatever the merits of some individual items of spending over that period, hardly anyone is going to quibble with the fact of deficits.

But where are we now (or, more specifically, where were we when Treasury did the economic forecasts that underpin yesterday’s numbers, and which Cabinet had when it made final Budget decisions)? Treasury has the terms of trade still near record highs, it has the unemployment rate falling a bit further below levels the Reserve Bank has already suggested are unsustainable, and over 22/23 it expects an economywide output gap (activity running ahead of “potential”) of about 2 per cent of GDP. In short, on the Treasury numbers the economy is overheated. And when economies are overheated revenue floods in. Surprise inflations – of the sort we’ve seen – do even more favours to the government accounts in the near-term: debt was issued when lenders thought inflation would be low, and although the revenue floods in (GST and income and company tax), it takes a while for (notably) public sector wages to catch up. On this macro outlook, the government should have been making fiscal policy choices that led to projected surpluses in 22/23 (perhaps 1-2 per cent of GDP), consistent with the idea – not really an right vs left issue – that operating balances, cyclically-adjusted – should not be in deficit. Big government or small govt, on average across the cycle operating spending should be paid for tax (and other) revenue.

Instead in an economy that is grossly overheated (on the Treasury projections) the government chooses to run material operating deficits. It is the first time in many decades a New Zealand government (National or Labour) has done such a thing, and should not be encouraged. It risks representing slippage from 30 years of prudent fiscal management by both parties, and once one party breaches those disciplines the incentives aren’t great for the other once it takes office.

And this indiscipline isn’t even occurring in election year (and already I’m getting an election bribe). It is fine to talk up projections of smaller deficits next year, but slotting a number in a spreadsheet is a rather different than making the harder spending or revenue decisions to fit within those constraints. Perhaps they’ll do it. Who knows. The political incentives may be even more intense by then. And the economic environment could be (probably will be) quite different.. What any government should be directly accountable for is their plans for the immediately-upon-us fiscal year.

You will hear people suggest that fiscal policy isn’t anything to worry about. Some like to quote The Treasury’s fiscal impulse measure/chart. But it just isn’t a particularly useful or meaningful measure at present (at least unless you line up against it a Covid “impulse” chart). But even if you want to believe that the overall direction of fiscal policy wasn’t too bad – and my comments on the HYEFU/BPS were not inconsistent with such an interpretation – the real impulse we should be focused on is how near-term fiscal policy has changed since December.

In December, the operating deficit for 2022/23 was projected at 0.2 per cent of GDP (allow for some margins of uncertainty and you could call it balanced). Now the projected deficit is 1.7 per cent of GDP, in an economy projected to be even more overheated that was projected in December.

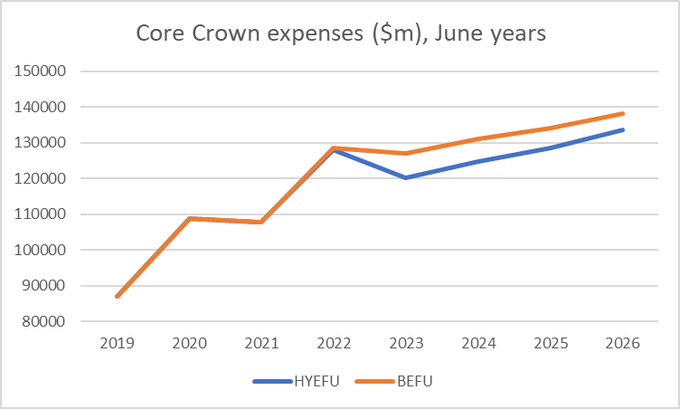

What about spending? Well, here are the projections for core Crown spending. Back in December the government planned that spending in 22/23 would be a lot lower than in 21/22 (which made sense since no more expensive lockdowns were being planned for). Yesterday’s projections for 22/23 are $6.8bn higher than what was projected only six months ago – and only about a billion less than last year’s heavy Covid-driven spending.

Some of it is inflation, but whereas in December Treasury projected that spending would be 30.5 per cent of GDP, now it is projected to be 31.6 per cent of GDP. It is a lot more spending and, all else equal, a lot more pressure on the economy and inflation. In case you are wondering, in both sets of projections tax revenue is projected to be 28.9 per cent of GDP.

Perhaps there is a really robust case for all this extra spending, making it so much more valuable and important than the private spending that will have to be squeezed out. But the evidence for any such claim is slight to non-existent, and the general presumption should be that if you want to spend a lot more you do the honest thing and make the case for higher tax rates. Instead, the Cabinet has chosen operating deficits amid a seriously overheated economy. It is cavalier and irresponsible.

That is policy, things ministers are directly accountable for. But there is also a full set of economic projections, amid which there are some quite disconcerting numbers. Now, before proceeding, it is worth stressing that these economic projections were finalised a long time ago, on 24 March in fact. If anything, that only makes things more concerning.

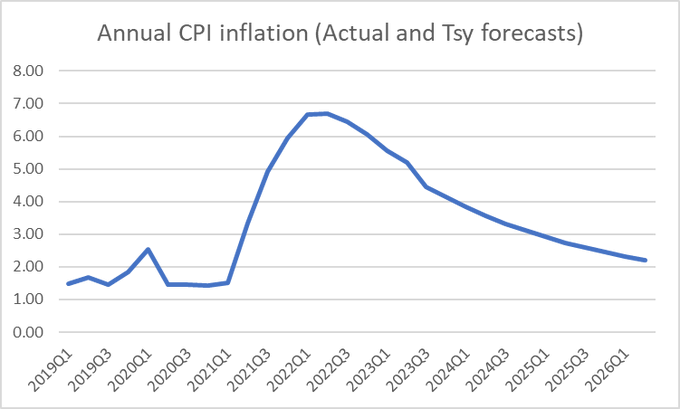

Here are The Treasury’s inflation forecasts

You will recall that the government has given the Reserve Bank an inflation target range of 1-3 per cent per annum but with an explicit instruction to focus on the midpoint of that range, 2 per cent annual CPI inflation. You should be aware that monetary policy doesn’t work instantly, with the full effects on inflation of monetary policy choices today not being seen for perhaps 18 months or even a bit longer. You should also be aware that The Treasury (and other forecasters) generally don’t include future supply etc shocks in their forecasts, because they are basically unknowable (and could go either way). So (a) any annual inflation forecasts more a few quarters ahead will be wholly a reflection of fundamentals (expectations, capacity pressures, and perhaps some small exchange rate effects), and (b) any forecast annual inflation rate 18 months or more ahead is almost wholly a policy choice. Actions could be taken now to get/keep inflation around the midpoint of the target range.

But Treasury forecasts inflation for calendar 2023 at 4.1 per cent – as it happens reasonably similar to many estimates of core inflation right now – and 3.1 per cent for calendar 2024 (December 2024 was the best part of 3 years ahead when Treasury finished the forecasts). Only at the very end of the forecasts – four years away – is inflation back to 2.2 per cent, close enough to the target midpoint that we might reasonably be content. It is a choice to forecast that the Reserve Bank’s MPC will simply not be serious in showing any urgency in getting inflation down, and seems barely to engage with the risk of entrenching expectations of higher future inflation. If one takes the annual numbers on the summary table, it is still a couple of years before they even expect the Reserve Bank to be delivering an OCR that is positive in inflation-adjusted (real) terms.

Now, The Treasury does not set the OCR, the Reserve Bank does that. But the Secretary to the Treasury is a non-voting member of the MPC, The Treasury is the government’s chief adviser on macroeconomic policy including monetary policy targets and performance. And they finished these projections two months ago, and will have shared them with the Minister of Finance and with the Reserve Bank. At very least, there should have been a “please explain” from the Minister to the Governor/MPC. Treasury might have been quite wrong, but if so the Bank should have had a compelling response. But it doesn’t seem likely that anything of the sort happened, and you may recall that when the Bank last reviewed the OCR they explicitly said they weren’t seeing any more inflation than they’d projected in February.

The Treasury numbers are doubly disconcerting because – finished in March – they are persistently higher than the expectations (late April) of the Reserve Bank’s semi-expert panel in the quarterly survey. For the year to March 2024, the survey of expectations reported expected inflation of 3.3 per cent, but The Treasury projects 3.8 per cent inflation.

Now, maybe this will all be overtaken by events. The forecasts were completed in late March, and since then the economic mood – here and abroad – has deteriorated quite markedly, with a growing focus on the likelihood of a recession (almost everywhere significant reductions in core inflation have involved recessions). Quite possibly, if the projections were being done today they would be weaker than those published yesterday (and the RB’s will be finalised about now) But I hope journalists and MPs are getting ready to compare and contrast the RB and Treasury forecasts and to ask hard questions about the differences.

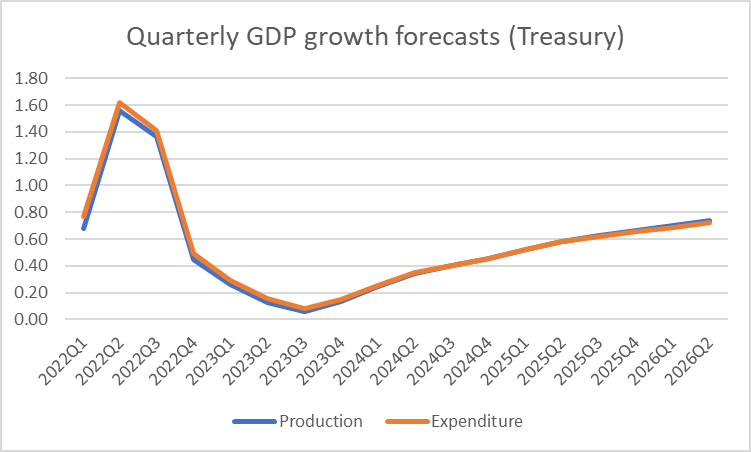

Soft-landings rarely ever happen once core inflation has risen quite a bit (as it clearly has this time). That doesn’t stop forecasters forecasting them, but if forecasters knew the true model well enough we probably wouldn’t have had the inflation breakout in the first place. I was, however, particularly struck by The Treasury’s quarterly GDP growth forecasts, which ever so narrowly avoid a negative quarter in Q3 next year (as the election campaign is likely to be getting into full swing). I’m not suggesting Treasury overtly politicised the forecasts, but had they assumed a monetary policy reaction more consistent with returning inflation to target quickly (say, under 3 per cent for 2023, which seems a reasonable interim goal at this point), the headlines might have been rather different.

I’m going to end with two charts that have little or nothing to do with short-run macroeconomic policy management.

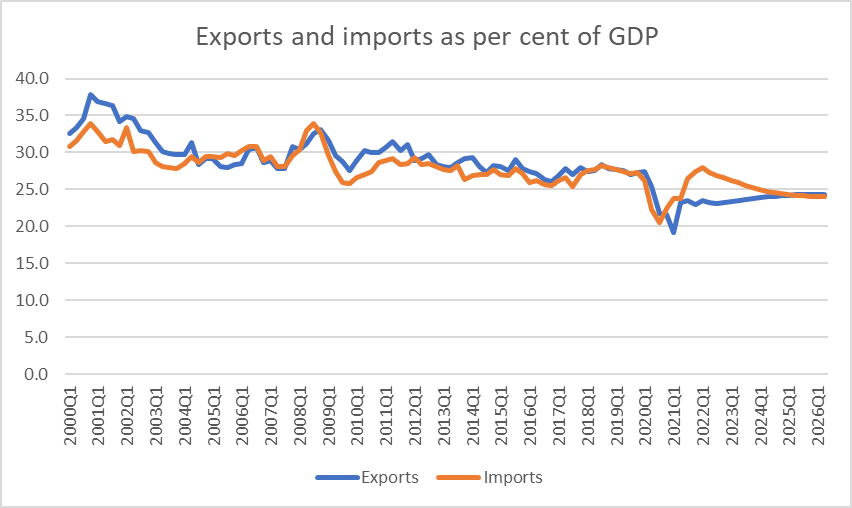

This one shows The Treasury’s projections for (nominal) exports and imports as a share of GDP.

Of course, with closed borders for the last couple of years we saw a sharp dip in both exports and imports as a share of GDP. But the end point for these projections is four years ahead. For both imports and exports, the shares settle materially below pre-Covid levels, in series that have been going backwards for decades. No doubt the Greens would prefer we all stopped flying, but successful economies have tended to feature – as one aspect of their success – rising import and export shares of GDP.

The Budget talked of a focus on creating a “high wage economy”. Sadly, all I could see in the documents that might warrant that claim was the expectation of continued high inflation – which will raise nominal wages a lot, but do nothing for actual material living standards.

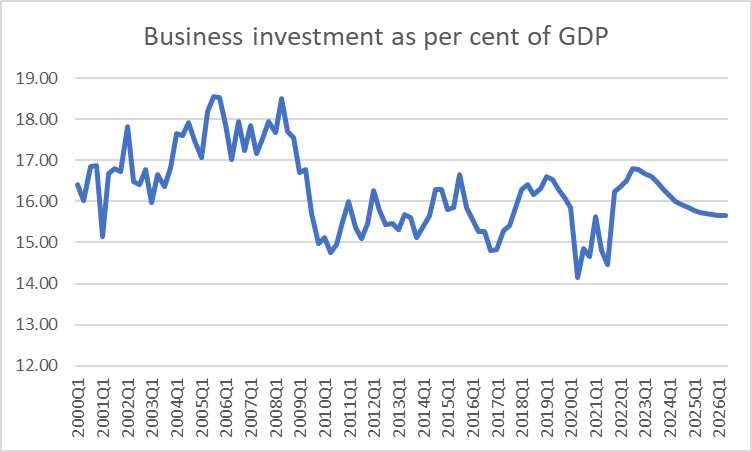

One of the striking features of the last decade was how relatively weak business investment as a share of GDP had been. Firms invest in response to opportunities, and the absence of much investment is usually a reflection on the wider economic and policy environment (much as bureaucrats like to think they know better, few firms just leave profitable opportunities sitting unexploited). For what is worth – and all the corporate welfare notwithstanding – The Treasury doesn’t see the outlook for business investment any better this decade than last.

And so in time will pass yet another New Zealand government that has done nothing to reverse decades of productivity growth underperformance. If that is depressing enough, this government seems to be in the process of unravelling the foundations of what had been a fairly enviable reputation for fiscal discipline and overall macroeconomic management. The situation can be recovered, but there is no sign in this Budget that the government much cares. And it isn’t even election year yet.