Last week I wrote a post suggesting that a rational Minister of Finance – one not unconcerned with macro stability but not particularly focused on price stability itself, one averse to severe recessions, one keen to be re-elected – might now seriously consider raising the inflation target. Such a Minister of Finance could find support among the economists abroad – quite serious and well-regarded figures among them – who have at times over the last decade or more championed a higher target to minimise the risks associated with the (current) effective lower bound on nominal interest rates.

To repeat myself, I would not favour such a move, and would quite deeply regret it were it to happen (here or in other advanced inflation-targeting countries – the UK for example). But interacting with a few commenters over the last week and reflecting further on the issue myself, I’m increasingly unsure why such politicians – and here I am talking about countries like New Zealand and the UK where the Minister of Finance has direct responsibility for setting the operational target of the central bank – would choose not to make a change. That is perhaps especially so in New Zealand, which has a history of politician-driven increases in the inflation target – changes that weren’t generally favoured by Reserve Bank staff or senior management, but which it has to be said have done little or no observable economic damage. Perhaps our Minister of Finance thinks he couldn’t fend off the tough forensic critiques that would come from the National Party? Perhaps he just thinks he can fob off any responsibility for the depth of the coming recession with handwaving about the rest of the world? Perhaps he would conclude it was already too late to get much benefit this term (not impossible)?

There isn’t yet much discussion (I’ve seen) of the possibility, whether here or abroad, although I did see last night a tweet from a former senior Bank of England researcher (and academic) championing just such a change. Of course, the most important two central banks are the ECB and the Fed, and in neither is there any provision for politicians to set operating targets, and the Bank of Japan is not yet grappling with high inflation. But it isn’t as if there is no discussion either: in this piece from late last year, by two former senior Fed officials, the case is made – or purely analytical/economics grounds – for exactly the sort of change I suggest a rational Minister of Finance might now consider. Among other things, the authors explicitly refer to the past New Zealand experience with raising inflation targets.

What disconcerts me is that, much as I would oppose an increase in the inflation target, I don’t think the case against will be particularly compelling to most people. I can highlight the distortions to the tax system, and thus to behaviour, that result from positive expected inflation, but that would be a more compelling argument were we starting from a target centred on true price stability rather than something centred already on 2 per cent inflation. I can, and do, make a strong argument for addressing the lower bound issues directly – easy enough to do as a technical matter, if only authorities would get on with doing so. There is a risk that materially raising inflation targets will lead to the public and markets being much less willing in future to take on trust the commitment of authorities to any (inflation) target they’ve announced (and one could note that the last New Zealand target change was 20 years ago – in the scheme of things still relatively early in the inflation targeting era).

So why would I oppose such a change? It isn’t impossible that some of it is just the reaction of someone who was present at the creation of (and actively engaged in forming) the current system and past inflation target. But I like to think it is more than that, and that many of the same arguments that persuaded me of the case for price stability 30-35 years ago still hold today. In the end I think it is largely almost a moral issue, and that – as we don’t tinker with our weights and measures, and look very askance on those who seek to fiddle them – there is something wrong about actively setting up a policy regime designed, as a matter of explicit policy, to debase the purchasing power of the currency each and every year.

Might it be different if – posing a hypothetical – nothing could be done about the current effective lower bound? Perhaps (although despite my advocacy for action on that front I’ve long been intrigued by the relative success of Japan in keeping cyclical unemployment low) but plenty can be done, as numerous economists have argued now for years. One can overstate the advantages of long-term price stability (there are very few long-term nominal contracts, and mostly that would be quite rationally so even if the inflation target was centred on “true” zero – ie allowing for the known modest biases in most CPIs) but it is like some gruesome triumph of the technocrats to be systematically destroying the value of people’s money by quite a bit each and every year on some proposition that doing so might produce slightly better cyclical economic outcomes, and even then only because politicians and technocrats wouldn’t address the problems at source. Sure, unexpected inflation is in many ways more troublesome than expected (targeted) inflation, but people shouldn’t have to take precautions against governments systematically eroding the value of their money.

Anyway, I would continue to be interested in alternative perspectives – either why the incentives on politicians aren’t as they appear to me to be, or why the economics-based case for pushing back strongly against increasing the target is stronger than it appears to me. Or, of course, why raising the target might just be good, on balance, economic advice.

Those comments got a bit longer than I intended. I’d really intended this post to be mainly some simple charts: given the (annual) inflation targets we’ve had, how have the cumulative increases in the price level over the decades compared with what might have been implied by the targets. I’ve seen a few charts around (for NZ and other countries) and did a quick one myself a few weeks ago on Twitter.

There are some caveats right from the start:

- neither New Zealand nor any other country has been operating a price level target system. In the New Zealand system, bygones are supposed to be treated as bygones – eg a period in which inflation has overshot the target (for whatever reason) is not supposed to be followed by targeting a period of undershooting. There are good reasons to prefer the “bygones be bygones” approach (even if some still contest it),

- the charts below will focus on the midpoint of successive target ranges. Since 2012 the Reserve Bank has been explicitly required to focus policy on the midpoint of the target range, but that was not so previously (and whereas Don Brash had quite an attachment to the idea of the midpoint, Alan Bollard did not particularly). The targets have always been formally expressed as ranges.

- while the targets have typically been expressed in terms of increases in the headline CPI, the Policy Targets Agreements (more recently the Remits) have explicitly recognised that there are circumstances in which CPI inflation not only will but should be outside the target range (a GST increase is only the most obvious, least controversial example).

- the targets have been changed several times, but policy works with a lag. In all these charts, I simply change the target when that change was formally made (even though if one were measuring annual performance – not the issue here) one could not rationally hold a Governor to account for outcomes relative to a new target even six to twelve months after the target was changed).

With all that as background, here is a chart comparing the CPI itself with the successive targets, beginning in 1991Q4 (because the first formal inflation target was for the year to December 1992). To December 1996 the midpoint of the inflation target was 1 per cent annum, rising to 1.5 per cent per annum to September 2002, and 2 per cent per annum since then.

Cumulative CPI increases have run a bit ahead of what a (very simple) reading of the successive inflation targets might have implied. It is a different picture than one would see for many other inflation targeting countries, but reflected the fact that until the 2008/09 recession (and despite lots of anti-Bank rhetoric about “inflation nutters”) we tended to produce inflation outcomes consistently quite a bit higher than successive target midpoints.

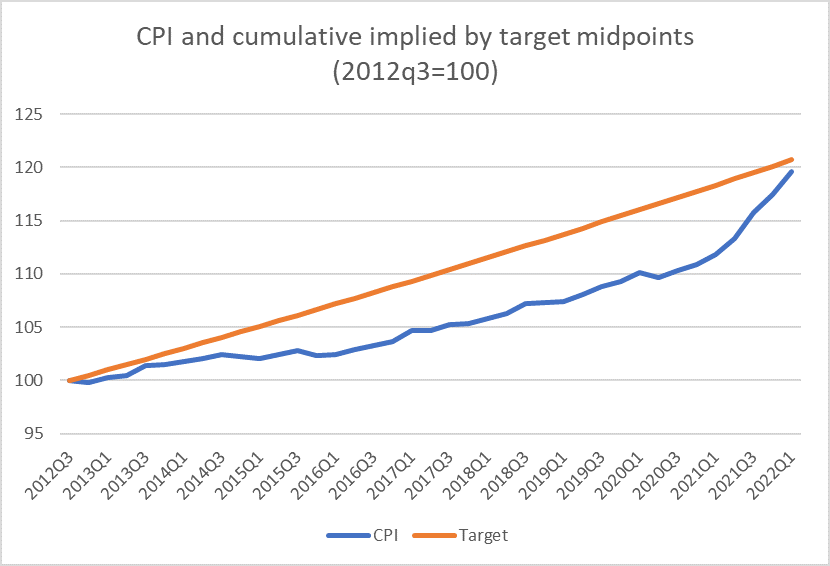

As I noted above, the Bank has only been formally been required to focus on the midpoint since September 2012 when Graeme Wheeler took office. Here is the same chart for the period since then.

Despite the newly-explicit focus on the midpoint, the annual undershoots during the Wheeler years cumulated to quite a large gap.

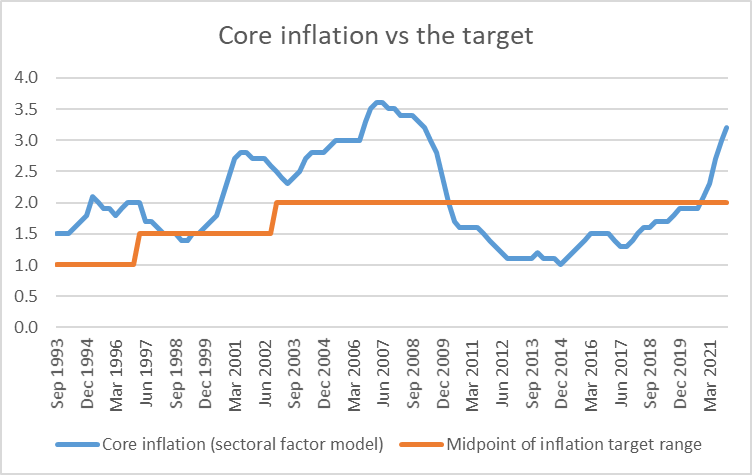

What about core inflation? The Bank’s (generally preferred) sectoral factor model has been taken back only as far as the year to September 1993. However, the Bank also publishes a factor model which goes back a couple more years (and which, although noisier year to year, has had exactly the same average inflation as the sectoral factor model in the decades since 1993).

This comparison surprised me a little. If you’d asked me I’d have guessed that over the decades the CPI might have increased perhaps 5 per cent more than a core measure (things like GST increases) but the actual difference is not much more than 1 per cent (the sort of difference best treated as zero given the end-point issues – chances of revisions – with such models).

Finally, although the Bank has never been charged with anything relating to the GDP deflator, I was curious. How would the cumulative path of the GDP deflator compare with that for the CPI? I didn’t have any priors, but was still surprised to find over 30 years the two series had increased in total by almost identical percentages.

Inflation in the GDP deflator is a lot more volatile (mostly on account of fluctuations in export prices), so not at all suitable for targeting, but still interesting that over the long haul the total increases have been so similar.

To end, I should stress that I am not attempting to draw any fresh policy lessons, or offer either fresh bouquets or brickbats to the Reserve Bank (past or present). I was just curious.