As much as I can, I try to read and engage with material that is supportive of New Zealand’s unusually open immigration policy. One should learn by doing so, and in any case there is nothing gained by responding to straw men, or the weakest arguments people on the other side are making.

At present, supporters of our unusually open immigration policy hold all the levers of power, and dominate much of the media. But what has surprised me over the years I’ve been thinking about these issues is how unpersuasive I find the pro-immigration material, perhaps especially that written in a New Zealand context. I’m not sure whether dominating elite opinion for so long has meant they no longer put the effort in, or what. But whatever the reason, I’ve expected stronger arguments and evidence – in support of a policy now run for 25 years – and haven’t found them.

At the start of the year – in a document that they were quite open about being aimed at Winston Peters, and those who might be listening to him – the New Zealand Initiative came out with a substantial publication, largely devoted to saying that there was really nothing to worry about: if they couldn’t demonstrate the economic gains to New Zealanders (a point they acknowledged) there were few or no downsides. If there was a case for any refinements, it was very much at the margins. I devoted a series of posts(captured in a collected document) to examining the case they’d made. I remain surprised at the limited extent to which an institution run by economists engaged with the specifics of New Zealand’s longer-term economic (under)performance.

A month or two ago, BWB Texts published Fair Borders? Migration Policy in the Twenty-First Century , a collection of chapters by various New Zealand authors (mostly, it would seem, of a left-liberal persuasion). I wrote earlier about the chapter on a particularly unusual feature of the New Zealand system: we are the only country with any material amount of immigration (and one of only a handful in total) allowing people to vote if they’d resided here for just a year.

But my main focus is on the economic perspectives, both because that is my own background, and because successive governments have sold the immigration programme primarily as a tool to improve New Zealand’s economic performance and the economic outcomes of New Zealanders. One doesn’t see it any more, but MBIE used to call the immigration programme a “critical economic enabler” .

And in Fair Borders there is a chapter on the economics of immigration, headed “International Migration: The Great Trade-Off”. The author is Hautahi Kingi, a young New Zealander – with a fascinating back story, that left me disquieted about aspects of our system – who has recently completed a PhD on the ‘macroeconomics effects of migration’ at Cornell, and now works for a consulting company in Washington DC.

He begins his chapter in praise of migration – not just something good, but something “central to human experience” – harking back to some mythical day when humans were free to wander savannahs and steppes, constrained only by wild animals, unfamiliar climate, and hostile people who were already there, but not by official border guards.

As he notes, actually, 95 per cent of people live in their country of birth. Probably a fairly high percentage live within 100 miles of where they were born. Given this, Kingi concedes,

immigration policies have the potential to transform not just our economies, but the structure of our societies and institutions.

Which is, of course, part of what many people worry about. Societies and institutions exist as they are for good reasons. G K Chesterton had some wise cautions to those who happily lay into such institutions.

Kingi continues “by definition, international migration is a global issue”. Well, I suppose so, in that for any international migration to occur at least two countries are involved. But there is no necessary reason why immigration policy should be considered a global issue at all. It isn’t like issues around pollution or climate change. And few countries do treat it as an international issue. They make immigration policy, as they seek to make policy in most other areas of governments, primarily in the interests of their own citizens/voters.

Kingi’s first main section is about what he describes as “the global perspective”. He is pretty persuaded by the papers which seek to show that if only all countries opened their borders and people could move wherever they wanted there would be a massive – perhaps 100 per cent – increase in world GDP. In his words “from a global income perspective, no other policy offers anything remotely as appealing”.

But, in fact, he doesn’t make much of a case. Sure, open migration would beat out foreign aid – the alternative policy he quotes – as a means to lift average incomes. But whoever supposed that most foreign aid ever did much good – Peter Bauer was writing about this stuff decades ago – or that much of it wasn’t more about foreign policy (cultivating relationships with foreign governments) than about lifting living standards in recipient countries. Free trade in goods and services does much more than foreign aid.

Perhaps more importantly, surely the most compelling and effective means to lift living standards en masse is for countries to adopt growth-friendly policies and institutitions. China is the most obvious example in recent decades. They have a long way to go – on both policies and outcomes – to get to First World living standards, but what they have achieved in recent decades is transformative, and obvious. And for hundreds of millions of people.

Unfortunately Kingi – and many of the libertarians who also run such arguments – end up running a latter-day version of the line one used to hear decades ago from people on the dripping-wet left wing side of economic debates: the poor are poor because the rich are rich. To a first approximation, it is simply false. People in New Zealand, or the UK, or France, or Denmark aren’t rich because we won some lottery, or just got lucky, but because our ancestors developed, and we maintain, cultures and institutions that develop and maintain a high level of productive capability (encouraging and rewarding people for investing in human and other forms of capital). Sadly, too many other countries have failed to do so. (The need to work hard to maintain such cultures is part of why I think Oliver Hartwich’s Herald op-ed today is profoundly wrong: character matters greatly.)

It is not as if change is imposssible – look at the convergence achieved in recent decades by a handful of east Asian countries. It is not as if our relative position is immutable either – not 1000 years ago, China was well ahead. But prosperity, en masse, is mostly about the institutions, broadly defined, that societies develop and maintain. Doing so is hard work.

Are there exceptions? Well, yes of course. In our age, if you don’t have too many people, and you do have lots of oil and gas, your people can be very rich, even without many of the supporting institutions that otherwise seem to be required. But those are windfalls, in a sense achieved by free-riding on the gains – demand and technology – developed elsewhere.

Generally, even if individuals might feel themselves lucky or unlucky, societies – and all of us exist within societies – aren’t lucky or unlucky: they are the product of successive generations of choices. Immigration restrictions don’t “elongate the misery” of poor countries: the choices of those societies are primarily what have that effect.

Can one import prosperity? To some extent one can. After all, New Zealand (and Australia and the like) are examples. Material living standards weren’t high for indigenous people pre-colonalisation. But New Zealand and similar countries had lots of land, a temperate climate, and by importing not just lots of people from the then most advanced economic culture (and all the legal and associated institutions), something a bit like Europe was created here. Maori shared – perhaps to a lesser extent than might have been desirable – in the prosperity that was created here. But – and these are Kingi’s words – “movement of people entails movement of culture and norms”. A New Zealand that was once largely the place of Maori isn’t really so any longer.

But that 19th century example – that transformed Australia, New Zealand, Canada, Argentina, Uruguay, Chile, and US – isn’t really relevant to New Zealand’s situation now. Even if we wanted to engage in such a mass transplantation, there is no economic culture hugely more advanced than what we already have.

So Kingi’s focus is the other way round – it is on the gains to migrants from being able to shift from poor countries to rich countries. There is no doubt that, for individuals at the margin they are considerable – it is why we see foreign students willing to pay $40000 for a job in New Zealand, with the aim of qualifying for a New Zealand residence visa.

But the staggering gains in the papers Kingi cites don’t result from quite modest flows, but from “massive” movements of people. In his words “movement of people entails movement of culture and norms” – and if those effects are small for modest migration flows, they are likely to be substantial for “massive” movements. In the long-run, migrants import their own economic destiny – just as we (descendants of the 19th century migrants from the UK) did. And if poor migrants in large numbers ultimately bring their own cultures and institutions, it is most unlikely that in the long run they’d be better off here to anything like the extent the academic papers suggest. After all, geographic New Zealand is no better intrinsically suited to economic prosperity for lots of people than many other parts of the world – arguably (or so I’ve argued) our remoteness makes us less so.

Strangely, Kingi’s poster-child example of large scale immigration is the Gulf Cooperation Countries, such as Qatar and Kuwait. 86 per cent of Qatar’s population is made up of migrants. Qatar has probably the highest GDP per capita in the world. It is obviously appealing to the poor migrants, who keep coming, but I’m not sure why Kingi regards it as a remotely appealing basis on which to sell mass migration to New Zealanders. For a start, these are classic states with massive natural resources and (originally very few people). It is no surprise that there are windfall gains that could be spread around. But as even Kingi acknowledges, the exploitation of lowly-skilled foreign labour in countries like this is appalling (even if one wants to engage in economists’ talk of both sides benefiting or it wouldn’t happen). It simply isn’t how we would want a society to be structured. And although he notes that this large scale migration goes on without causing any great domestic political problems, (a) the migrants have few rights, and no political rights (even fewer typically than the natives), and (b) these are societies not exactly known for freedom of speech, freedom of the press and the like, And, sadly, slavery – or its modern equivalent – can look quite appealing to the slaveholders and those who benefit from the practice. It remains morally repulsive.

If you’d only got this far in Kingi’s chapter, you might suppose he was an out-and-out advocate of open borders and free migration, here and everywhere. But it is here that he gets more interesting. Note the trade-off in his chapter title, and he seems to recognise that whatever large scale migration might do for the migrants, it could well harm at least some natives. I think he gives a fair account of the international debate about the impact of immigration on the wages of lowly-skilled natives

Although this debate continues unresolved in academia, it is at leasr conceivable that immigrants may negatively affect those native workers with whom they compete most closely for jobs. The experience of globalisation in recent decades should teach us to take this potential concern very seriously.

He looks to reconcile what he sees a a global imperative to allow high immigration (generally) with the risk of harm to vulnerable natives, favouring better-educated migrants.

But as notes, immigration is’t just an economic issue. And here too he seems torn. He’s a paid-up member of those who “embrace multi-culturalism as a cherished part of progressive society” and yet recognises that “mass migration” can have a ‘potentially corrosive effect on that society”. But as I say, he is torn.

When people cross borders, so do their cultures and norms, and we are almost always richer and stronger for it.

But

more diverse societies also tend to reduce the provision of public goods and erode support for the welfare state

Unlike some libertarians, that erosion of support for the welfare state seems to be a bad thing for Kingi.

and

[ethnic divisions] can severely undermine the social institutions sustaining an economy because, despite the assurances of modern legal systems, “virtually every commerical transaction has within itself an element of trust”

He notes

The impact of immigration on a country’s social fabric can be an uncomfortable issue to discuss because it forces us to acknowledge and confront lamentable tribal aspects of human frailty.

Institutions and societies evolve to cope with human fraility – aka “reality”.

And almost in passing he notes a Maori dimension

modern Aotearoa was founded on the principle that tangata whenua have rights to their culture that should not be overridden by settlers. At the heart of the critique against colonialism is a concern for the enforced erosion of culture.

Kingi sets out the concluding section of his chapter with the proposition that there is a moral dilemma between the global and domestic perspectives.

by restricting the entry of foreigners…we effectively accept the substantial inequality outside our borders in order to protect the veneer of equality within.

You can see where his economist instincts lie. But he is simply wrong about the trade-off, at least once large numbers of people are involved. Societies make, and sustain, their own destinies. He argues that

migration is, and always has been, the best tool for reducing suffering in our world

But demonstrably that isn’t so. Europe didn’t get rich on the back of migration – even if the 19th century outflows helped them a bit. China didn’t lead the world – and recover its standing in the last 40 years – on the back of migration. Perhaps some libertarians wish it were otherwise, but migration – country to country – has always been a distinctly minority experience. It lifts prospects for relatively small numbers – if the people of North America are generally richer than the countries of their ancestors, people of South American typically aren’t. Rising prosperity, reduced poverty, mostly result from choices, conscious or unconscious, that societies make about how to organise and discipline themselves.

I’m not sure quite where Kingi himself ends up. His chapter is strikingly high level, and despite being in a book focused on New Zealand hardly engages with the New Zealand economic experience (or New Zealand social/cultural issues) at all. It certainly doesn’t recognise how unusually large New Zealand’s residence approvals programme is by modern international standards.

Perhaps when Kingi ends this way

While international migration represents a life-changing opportunity for many, it also threatens the livelihoods of others and strikes to the core of our societies by changing their structure, their jobs, their culture, their appearance

he is still working his way towards a policy prescription for modern New Zealand.

As part of Radio New Zealand’s recent podcast series on New Zealand immigration, Kingi and I did a series of email exchanges on these issues – me as the sceptic and Kingi as the supporter. Radio New Zealand tells me that the series of letters was well-received by readers, in part for the very different angles they present on the economic issues. I want to come back to that exchange, perhaps next week, to elaborate on some of the key points we each chose to make when confronted with the other’s arguments, under pretty tight word limits.

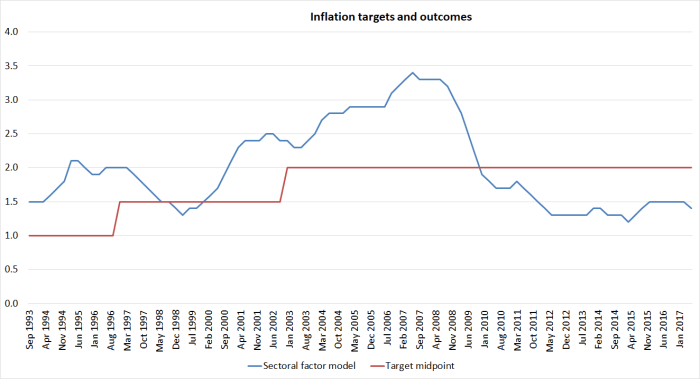

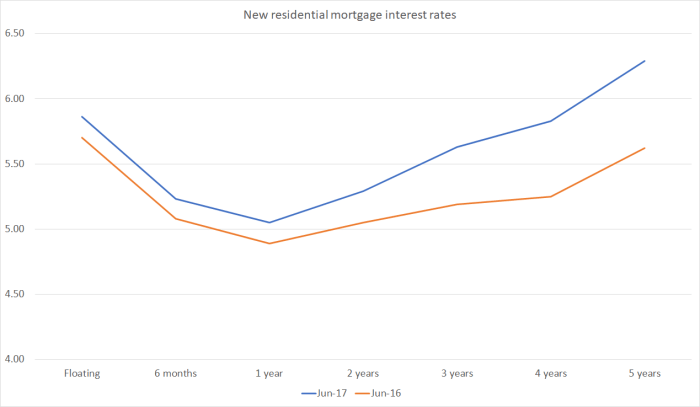

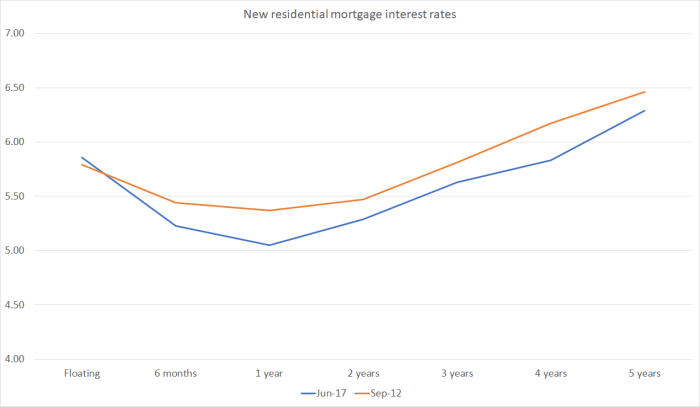

I don’t suppose anyone is taking out four or five year fixed rate mortgages, but across the entire curve, interest rates are higher not lower. Or we could go back another year or so, to just prior to when the Reserve Bank began cutting the OCR. The OCR has been cut by 175 basis points since then. Even at the shortish end of the mortgage curve, rates are down only 50-70 basis points.

I don’t suppose anyone is taking out four or five year fixed rate mortgages, but across the entire curve, interest rates are higher not lower. Or we could go back another year or so, to just prior to when the Reserve Bank began cutting the OCR. The OCR has been cut by 175 basis points since then. Even at the shortish end of the mortgage curve, rates are down only 50-70 basis points. Barely lower, even though core inflation – on their own favoured measure – is as low today as it was then (and has been consistently low throughout his term).

Barely lower, even though core inflation – on their own favoured measure – is as low today as it was then (and has been consistently low throughout his term).