The Labour Party is campaigning on a couple of changes to the Reserve Bank Act. One would make a statutory committee, rather than the Governor alone, legally responsble for monetary policy decisions, and would require the minutes of that committee to be published fairly shortly after the relevant meeting. I don’t think that change goes far enough – and it doesn’t deal at all with the extensive (and much less constrained) decisionmaking powers the Bank has around financial institution regulation – but if not everyone actively favours change, there aren’t now that many defenders of the (single decisionmaker, secretive) status quo. Even Steven Joyce got The Treasury to commission some advice on possible changes, although his officials now refuse to release that report.

There is more dispute around the other limb of Labour’s proposed changes, in which they proposed to amend the statutory goal of monetary policy from “stability in the general level of prices” only “to also include a commitment to full employment”.

Earlier this week, so NBR reports, Grant Robertson and former longserving Governor Don Brash came head to head at BusinessNZ election conference. Don thinks the proposed change is wrong and was reported as pointing to two reviews undertaken during the term of the previous Labour government, both of which saw no reason to change the statutory objective for monetary policy.

My initial reaction to the proposed Labour change was also sceptical, and I initially went as far as to describe it as “virtue signalling”. I was discussant at an Victoria University event a few months ago where Robertson launched his policy, and this is how I summarised my view in a post written the following day.

I was (and am) much more sceptical, and nothing that was said in response to questions really clarified things much. I get that full employment is an historical aspiration of the labour movement, and one that the Labour Party wants to make quite a lot of this year. In many respects I applaud that. I’m often surprised by how little outrage there is that one in 20 of our labour force, ready to start work straight away, is unemployed. That is about two years per person over a 45 year working life. Two years…… How many readers of this blog envisage anything like that for themselves or their kids?

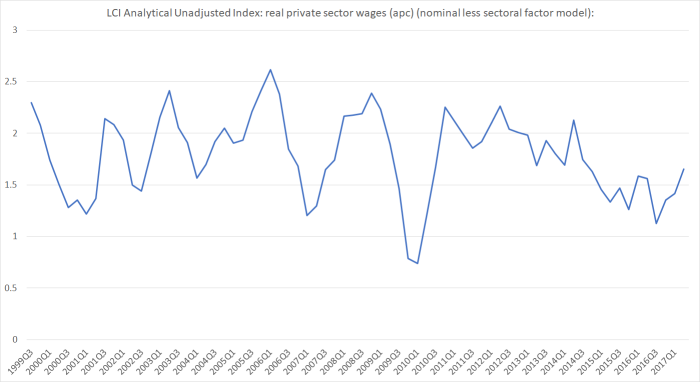

But still the question is one of what the role of monetary policy is in all this, over and above what is already implied by inflation targeting (ie when core inflation is persistently below target then even on its own current terms monetary policy hasn’t been well run, and a looser monetary policy would have brought the unemployment rate closer to the NAIRU (probably now not much above 4 per cent)).

I noted that I’m sceptical that the wording of section 8 of the RB Act is much to blame. After all, for several years prior to the recession, our unemployment rate was not just one of the lowest in the OECD, it was also below any NAIRU estimates. And when I checked this morning, I found that our unemployment rate this century has averaged lower than those of Australia, Canada, the US and the UK, and our legislation hasn’t changed in that times. Robertson often cites Australia and the US.

The last few years haven’t been so good relatively speaking. But if the legislation hasn’t changed and the (relative) outcomes have, that suggests it is the people in the institution who made a mistake – they used the wrong mental model and were slow to recognise their error and respond to it. Getting the right people, and a well-functioning organisation, is probably more important than tweaking section 8.

I stand by most of those individual comments. But as I thought about things further, I’ve come to conclude that the direction Labour is wanting to go is the right one (although details matter, and there are few/no details). If anything, one could mount an argument that defence of the current statutory formulation risks being “virtue signalling”.

Don Brash relies in part on the two enquiries undertaken in the term of the previous Labour government. The second, conducted by Parliament’s Finance and Expenditure Committee, can largely be discounted. It was set up in 2007 at time when there was quite a bit of caucus (and ministerial) discontent with the Reserve Bank – the OCR had been raised again, and the exchange rate was again strong. A lot of work went into the inquiry, and it reported in 2008, just weeks before the 2008 election. But however much grumpiness there had been, a government-dominated committee was never going to come out a few weeks before an election their party looked like losing arguing that a key aspect of macroeconomic policy had been done badly throughout their term in office.

The earlier inquiry, conducted by Swedish economist, Lars Svensson at the request of the incoming Minister of Finance in 2000/01 would normally be a more potent argument. Svensson was an academic expert in matters around inflation targeting and he was content to recommend retaining the statutory goal for monetary policy as it was.

So what has changed? Robertson is quoted in the NBR article as saying that monetary policy has “enormously changed” since the international crises of 2008/09. Here I simply disagree with him, and find myself (I think) strongly agreeing with the outgoing Governor of the Reserve Bank, who notes that for all the talk it is remarkable how little change there has been in monetary policy anywhere. Sure, interest rates are a lot lower, and various major central banks resorted to unconventional quantity-based measures to supplement their toolkit. But there is no sign of any material change in any of those countries in how the goals of monetary policy have been specified (whether in statute or in more-operational documents). As the Governor often notes, no one has abandoned inflation targeting, and no one has lowered (or raised) their inflation target.

Of course, if there was once in some circles a degree of hubris around quite how much good stuff central banks can deliver, much of that has now dissipated. And the use of unconventional tools has raised questions about accountability, given that some of those tools can verge quite close to fiscal policy, for which legislatures are typically responsible.

But perhaps two relevant things have changed. The first is Lars Svensson, who – having had several years experience as a senior policymaker – now quite openly argues that flexible inflation targeting should involve a clear and explicit specification of an inflation target and the identification of a sustainable long-run unemployment rate, with explicit weights assigned to deviations from these two variables. I wrote at some length about Svensson’s view of these things in a post in April. As I noted then

I don’t know specifically what Svensson would make of the current debate in New Zealand, or of what the Labour Party (at quite a high level of generality) is proposing. What we do know is that Labour is proposing nothing nearly as specific or formal as Svensson argues for: there would be no numerical unemployment target or an official external assessment of the NAIRU (or LSRU). My impression would be that his reaction would be along the lines of “well, of course the unemployment rate – and short to medium term deviations from the long-run level, determined by non-monetary factors – should be a key consideration for monetary policymakers; in fact it is more or less intrinsic to what flexible inflation targeting is”. He might suggest there are already elements of that in the PTA, but that making it a little more high profile, with an explicit reference to unemployment, might be helpful.

At the time, I suggested they might find it useful to get in touch with Svensson, who retains an interest in New Zealand. Should they form the government after the election next month, he would be someone that they would be wise to consult, both in making their proposed legislative change, and in articulating a social-democratic vision of what should be looked for from a central bank.

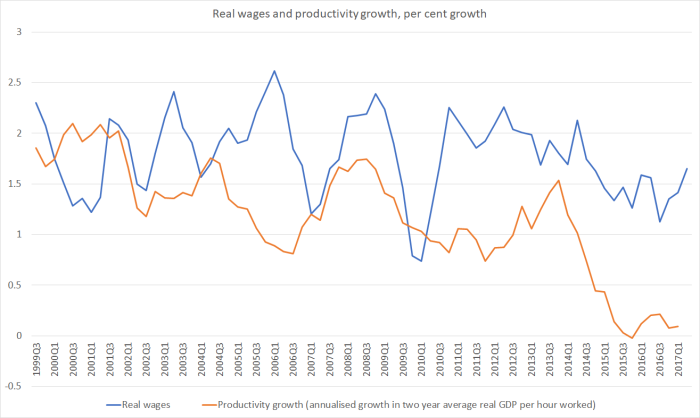

The other thing that has changed over the last 15 years or so is our own central bank. It is striking how little public attention they ever pay to unemployment, even though it is the most tangible measure of excess capacity – and one directly involving people’s lives and livelihoods. But perhaps more striking still is the way in which they have conducted monetary policy in a way that has left the unemployment rate above any reasonable estimates of the NAIRU for eight years. That would have seemed staggering to us when we were looking at getting inflation under control in the late 1980s – when we knew that temporarily higher unemployment was a price of getting inflation down. It is pretty inexcusable in today’s climate – which doesn’t stop people making excuses.

And so I come back to the point I made in the remarks quoted above. Getting the right person – and people – into the senior positions responsible for the conduct of monetary policy probably matters more than changing the statutory objective. At the moment, an incoming Minister of Finance has no way of putting his or her preferred types of people in those roles – all that power rests with the Board (the company directors and the like appointed by the outgoing government, with almost no accountability). That needs to be tackled directly, and quickly.

But the way the statutory goal is expressed should affect expectations on the new Governor (and any committee that is established as part of governance reforms). Over recent years, fear of booms seems to have driven the Governor (and his staff) – with no statutory mandate at all – and there has been no pressure on them to focus on delivering low and sustainable rates of unemployment. Changing the Act – in the generalised way Labour seems to be talking of – and not changing the sort of people making the decisions won’t have much impact at all. But changing the Act in this area, can be one part of an array of changes that lead the Reserve Bank in future to put much more emphasis on unemployment, in public and in private, in the way that many other advanced country central banks do. Policy is, after all, supposed to be about people.

What array of changes should any new government make?

- a move to a decisionmaking committee, appointed by the Minister, and subject to parliamentary hearings before taking up the appointment,

- making a low sustainable rate of unemployment (“full employment” if you must) a part of the statutory goal of monetary policy,

- require the Reserve Bank to publish estimates of the NAIRU and, in the Monetary Policy Statement, require them to explain reasons for any material deviations from those NAIRU estimates,

- require the timely publication of minutes of the decisionmaking committee and (with a longer lag) of the background analysis papers provided to the committee, and

- in the immediate future, change the Act to allow the Minister and Cabinet to appoint the new Governor directly (this is the normal way such appointments are made in other countries). Getting the right person to lead these reforms is vital and there is no reason to think people like the current Board would deliver that person.

And just briefly on the substantive issue: the reason we have active discretionary monetary policy is because people have judged, over decades, that, were we not to do so, output and employment would be much more variable, and in particular recessions – and periods of high unemployment – would be more more savage and sustained than they need to be. That is not a novel proposition now, and it isn’t even a particular controversial one (although some free bankers will point out that, say, the worst US recessions have been since the central bank was set up) – it is a standard insight of modern macroeconomics. Greeece is a particularly nasty example of the alternative approach. That’s why I’m uneasy about those defending a single price stability goal for monetary policy: it may well be the medium-term constraint on what else monetary policy can do, it is one of desired outcomes we want to preserve (I say preserve because sustained inflation is a phenomenon of the central banking era, whereas longer-term price stability was a feature of earlier centuries), but it isn’t the main reason why we have active discretionary central banks. We have such institutions primarily because we care about minimising the bad times – sustained periods of excess capacity and high unemployment. We aren’t – or shouldn’t be – averse to booms (except to the extent they portend busts) but we should be, and mostly are, very averse to significant deviations from “full employment”. Keeping unemployment as low as the other labour market institutions (welfare systems, minimum wages etc) allow could reasonably be seen as the primary goal of monetary policy. Rising inflation would then be an indicator that the central bank had overdone things, and thus price stability represents a useful constraint or check on over-optimism about how low the unemployment rate can be got at any particular point in time. At present however, defenders of the current specification of the goal can almost come across as if it is a point of virtue not to care, let alone to mention, about those who are unemployed.

Things were a little different in 1989 when Parliament was first debating the Reserve Bank legislation. Arguably it made a lot of sense then to put in a single goal of price stability – because having lost sight of the constraint (price stability) in earlier decades, it was important to establish confidence that inflation would in future be taken very seriously. That isn’t the main message we, the markets, or the Reserve Bank need to hear after years of below-target inflation, and even more years of above-NAIRU unemployment rates.

So although I have a great deal of respect for Don Brash, and these days count him as a friend, on this occasion I think he’s wrong and Grant Robertson is much closer to right.

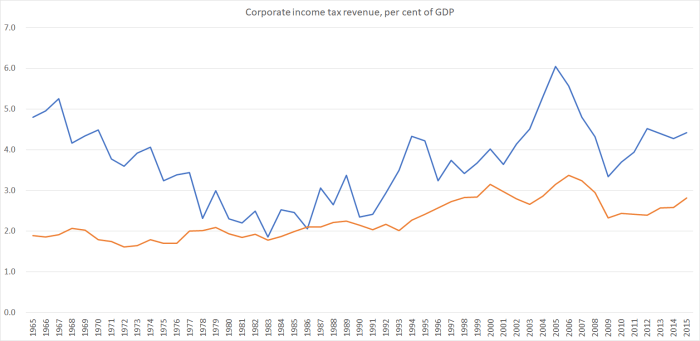

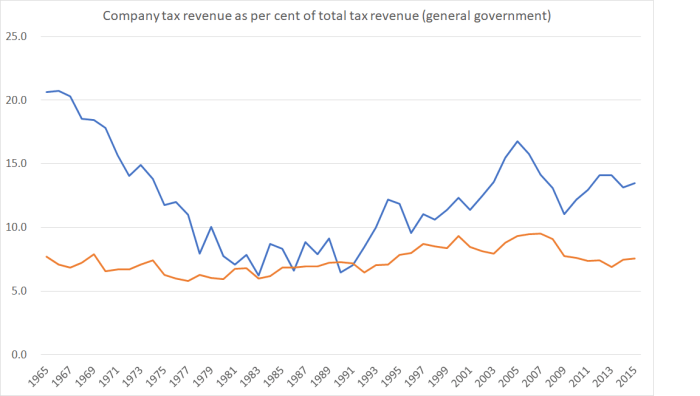

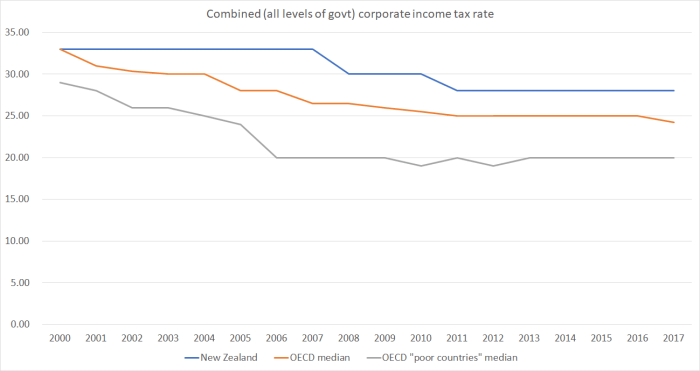

Of the “poor” OECD countries, only Mexico and Portugal now have higher company tax rates than we do. Whereas most of the “poor” countries are closing the income/productivity gaps to the richer OECD countries, Mexico and Portugal (and New Zealand) aren’t. I’m not suggesting it is the only factor by any means, just highlighting the choice that the more successful converging countries have been making.

Of the “poor” OECD countries, only Mexico and Portugal now have higher company tax rates than we do. Whereas most of the “poor” countries are closing the income/productivity gaps to the richer OECD countries, Mexico and Portugal (and New Zealand) aren’t. I’m not suggesting it is the only factor by any means, just highlighting the choice that the more successful converging countries have been making.

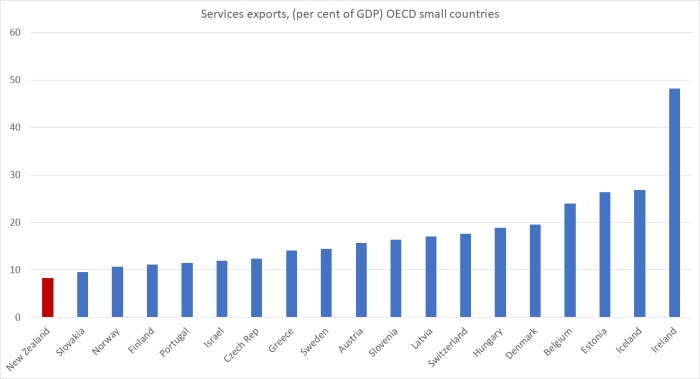

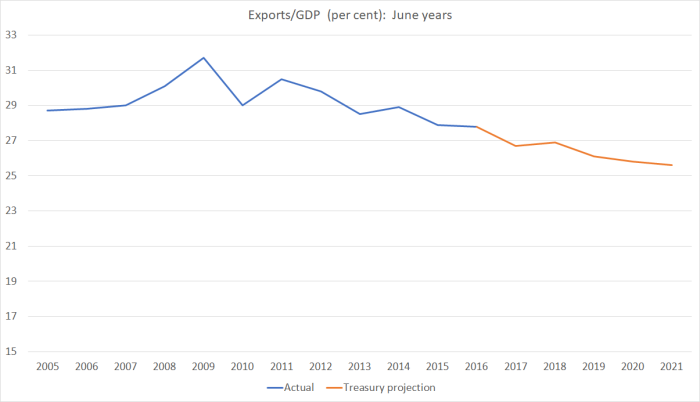

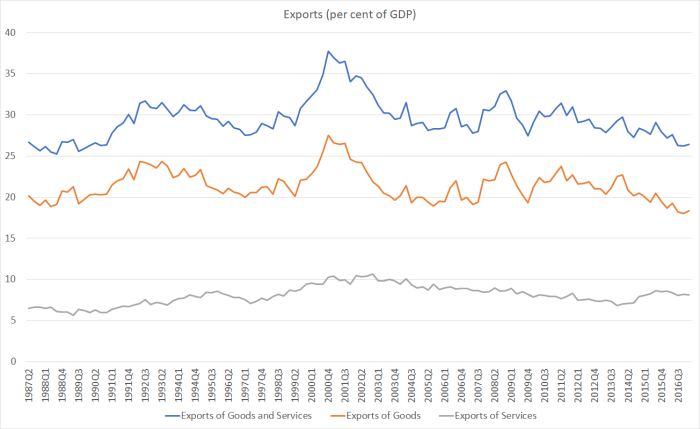

It is easy for one’s eye to go to those peaks in 2000 – at a time when the exchange rate had fallen sharply – but even much more recently the trends haven’t been favourable. Even the vaunted services exports are lower now as a share of GDP than they were 10 years ago, or than when the government came to power. The Minister talked of “high-tech value-added manufacturing” as the future, but then overall goods exports are lower as a share of GDP now than at any time in the last 30 years.

It is easy for one’s eye to go to those peaks in 2000 – at a time when the exchange rate had fallen sharply – but even much more recently the trends haven’t been favourable. Even the vaunted services exports are lower now as a share of GDP than they were 10 years ago, or than when the government came to power. The Minister talked of “high-tech value-added manufacturing” as the future, but then overall goods exports are lower as a share of GDP now than at any time in the last 30 years.