Five years ago, the then incoming Governor, Graeme Wheeler, signed a Policy Targets Agreement with the then Minister of Finance. In that document, he committed to run monetary policy with a

focus on keeping future average inflation near the 2 per cent target midpoint.

Earlier this week the CPI was published. It was the last such release that will appear while the Governor is still in office.

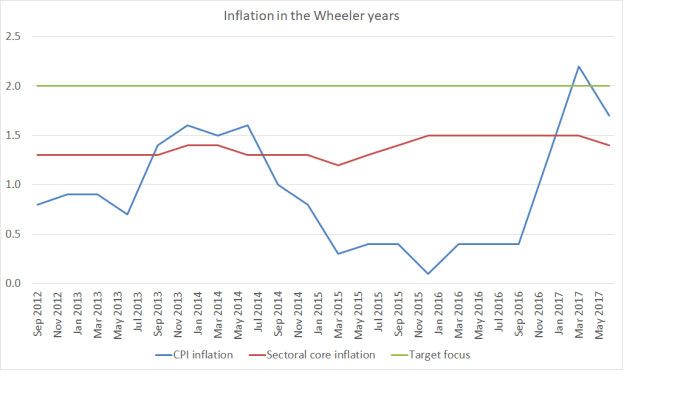

On a chart showing the 2 per cent focal point the Governor willingly committed himself and the Bank to, here are (a) the actual CPI inflation rates and (b) the Governor’s preferred measure of core inflation (the sectoral factor model measure) for the last five years.

Not once in five years has core inflation (on this measure) even come close to 2 per cent. In only a single quarter – one of 20 – did headline CPI inflation get to 2 per cent.

Of course, the Governor can’t really be held to account for inflation outcomes in the first year or so of his term – those outcomes were determined by choices made by Alan Bollard. And for the next year or so, it will be Graeme Wheeler’s policy choices that have the biggest policy influence. Nonetheless, to be so consistently far away from the newly-adopted target isn’t a great legacy. Perhaps (but probably not) the Bank’s Board will reflect on those outcomes in their forthcoming Annual Report?

The sectoral factor model is only one measure of core inflation, albeit the most stable of them (and so the dip down in the latest release should be a bit disconcerting). Here is the table I’ve run previously, of six measures of core inflation.

| Core inflation: year to June 2017 | |

| CPI ex petrol | 1.7 |

| Trimmed mean | 1.8 |

| Weighted median | 2.0 |

| Factor model | 1.7 |

| Sectoral factor model | 1.4 |

| CPI ex food and energy | 1.6 |

| Median | 1.70 |

The poor track record on inflation might have been more tolerable if:

- productivity growth was really strong, driving down costs and prices. But it hasn’t been. In fact, there has been no labour productivity growth at all in the Wheeler years (not the Bank’s fault), or

- if the unemployment rate was exceptionally low. But it hasn’t been. The current unemployment rate (4.9 per cent) is still materially above most estimates of the NAIRU, and well above pre-recessionary levels. For what it is worth, it is also now above the unemployment rates in a couple of Anglo countries with pretty flexible labour markets (the US and the UK), which had to grapple with having reached the limits of conventional monetary policy during the post-recessionary years.

- core inflation was still rising now (mistakes happen, but fixing them promptly makes up for quite a lot). But, for example, the sectoral core measure is back to the same level it was in September 2015, when the Bank was just beginning to unwind its ill-judged 2014 tightenings.

Mostly, monetary policy in the Wheeler years hasn’t been well run. When Graeme Wheeler took office core inflation had fallen quite a bit over the previous year. A sensible response would have been to have cut the OCR. The OCR increases in 2014 were never necessary (I choose the word advisedly – there was plenty of time to wait and see if core inflation was in fact just about to pick up strongly). Those increases were then unwound only rather grudgingly.

Of course, in fairness to the Bank, it did rather less badly for most of the period than most of the market economists whose views are covered in the local media. For most of the time, most (almost all) of them were forecasting higher inflation, and a higher OCR, than the Reserve Bank was delivering. But it isn’t much consolation, since (a) the Reserve Bank has far more analytical resources at its disposal than the private banks, and (b) the Reserve Bank is paid to conduct monetary policy, and market economists aren’t.

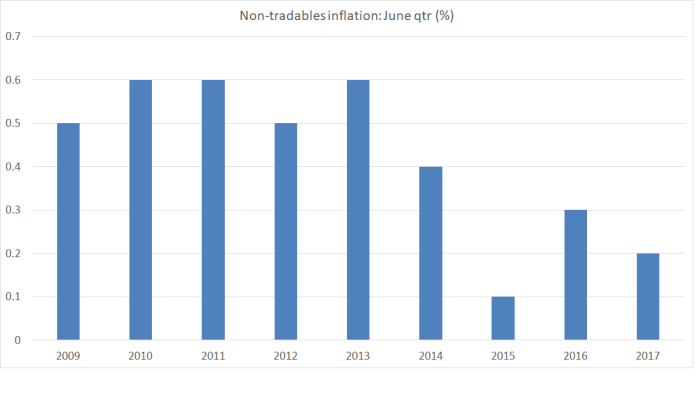

We’ll see next month what the Reserve Bank makes of the latest inflation outcomes. But the data must be quite disconcerting. There are some specific pockets of inflationary pressure – building costs notably (and not that surprisingly, given the population pressures). But here is non-tradables inflation (quarterly) for the June quarters of the last nine years. Non-tradables inflation is what the Reserve Bank has most influence over in the medium-term.

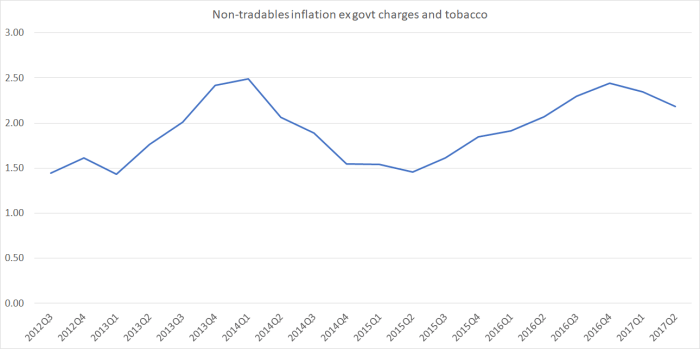

Only in 2015 was June quarter non-tradables inflation lower than it has been this year. Annual non-tradables inflation has dipped slightly to 2.4 per cent. That might not seem too bad – after all the target midpoint is 2 per cent – but as even the typically-hawkish BNZ noted in their commentary the other day one would really expect non-tradables inflation to be quite a lot higher to be consistent with delivering overall CPI inflation near the target midpoint. A simple approach to a core non-tradables inflation rate is the SNZ series that excludes government charges and the cigarettes and tobacco subgroup (where taxes are being raised substantially each year).

An annual inflation rate in this series nearer 3 per cent would be more consistent with core CPI inflation settling around 2 per cent. At present, it is nowhere near 3 per cent, and moving in the wrong direction.

So why is inflation still (a) quite a way from target, and (b) looking to be falling again? Broadly speaking, I reckon the answer is about (a) an economy that continues to run below capacity, and (b) tightening monetary and financial conditions. The Reserve Bank’s latest published estimate was that the output gap is around zero (roughly, a fully-employed economy). I noticed one local bank published an estimate the other day suggesting they thought the output gap was more like +1 per cent of GDP. With the unemployment hovering around 5 per cent – and best estimates of the NAIRU somewhere around 4 per cent, and demographic reasons to think the NAIRU might be falling, that simply seems unlikely. It is much more likely there is still some excess capacity in the system, and demand growth simply hasn’t been strong enough. The job of monetary policy is to manage interest rates in ways that deliver enough demand to keep inflation near target.

The current state of excess capacity is a long-running difference of opinion. But what isn’t really in much doubt is that monetary and financial conditions have been tightening quite substantially in the last few quarters.

The OCR was cut to the current level of 1.75 per cent last November. We might have expected inflation to pick up a little further since. But retail interest rates have been rising:

- the Bank’s measure of SME overdraft rates troughed in January 2017, and had risen by 19 basis points by June,

- the Bank’s measure of floating mortgage rates for new borrowers troughed in October 2016, and has risen 25 basis points since then,

- the Bank’s six month term deposit rate measure troughed in July last year and has risen 15 basis points since then,

- one and two year fixed mortgage interest rates are also up by around 20 basis points

These aren’t large moves, but with inflation having been consistently below target (and the Bank having been repeatedly surprised) there was no good reason for the Reserve Bank to have accommodated such tightenings.

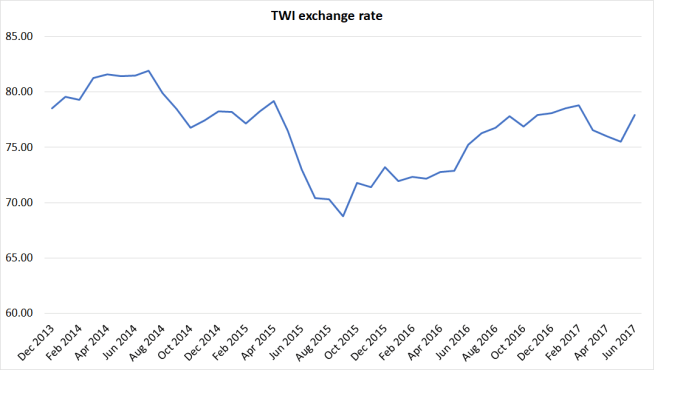

It isn’t just retail interest rates. Here is the trade-weighted exchange rate measure

The exchange rate fell quite a long way in 2015, as dairy prices fell, and the Reserve Bank began cutting the OCR. At the time, the Governor spun tales about how this would help get inflation back to 2 per cent. Exchange rates are somewhat variable, but broadly speaking the trend has been upwards since then. Yes, dairy prices and the terms of trade have improved, but it all adds up to another tightening of monetary conditions when inflation has been persistently below target.

And, of course, credit conditions have also tightened. Some of that is the Reserve Bank’s own doing – last year’s latest iteration of the LVR controls – but much of it isn’t: it is lenders reassessing their own willingness to lend. We don’t have good statistical indicators of credit conditions, but there is little doubt they’ve been tightening.

It all adds up to a picture in which shouldn’t really be very surprising at all: inflation isn’t rising and may well have begun falling again. Of course, some surprises reinforce the more systematic elements. Weaker oil prices (for example) probably will spill over to some extent into core measures of inflation. And unlike the situation in 2010 and 2014, this isn’t a case where the Reserve Bank has gone out actively seeking to tighten monetary conditions – indeed, the Governor has been commendably moderate, especially relative to most local market commentators. But it does look a lot like another case where the Bank (and the Governor personally, as single legal decisionmaker) has been too invested in a story that the economy was strong, inflation was picking up, and would continue to pick up, that it missed the way in which monetary conditions were tightening, and continued to largely (and deliberately) ignore the signals coming from the labour market. Instead of repeatedly talking – as the Governor does – about how accommodative (or even “highly accommodative”) monetary policy is, the Bank would be much better advised to treat the low level of interest rates as normal, for the time being (it has after all been more than 8 years now since they were sustainably higher), and put much more weight on seeing hard evidence that (a) inflation is settling back at around 2 per cent, and (b) unemployment is nearer credible estimates of the NAIRU, before acquiescing in any material tightening in monetary conditions. After getting it so wrong for so long, they should be willing to run the risk of core inflation heading a bit above 2 per cent for a time – after so many years of undershoots, no one is suddenly going to think the Bank is soft on inflation if core inflation is 2.2 or 2.3 per cent for a couple of years.

Looser monetary conditions now would, most likely, be more consistent with the Bank’s mandate. I’m not sure it is good form for the Governor to take the market by surprise with a cut from the blue as he heads out the door. But the case for establishing an easing bias in next month’s Monetary Policy Statement is beginning to strengthen. Hawks will, of course, cite the various business and consumer confidence measures. None is any stronger now than they’ve been over the last couple of years, and over that period inflation simply failed to pick up anything like enough to get back to target. Expecting something different now, when the background conditions haven’t changed, is either just wishful thinking, or something worse – including an inexcusable indifference to the lingering high number of people unemployed.

Agree 100% Michael.

The RBNZ consistently runs the mantra that monetary conditions are “highly accommodative” but as you rightly point out, they’re not. Banks have responded to higher wholesale market rates and higher cost of capital by raising interest rates and tightening credit conditions. The RBNZ has compounded the tightening credit environment by raising LVR restrictions and on top the NZD is substantially stronger on a real effective basis.

Activity remains below what’s required to achieve a degree of non readable inflation consistent with the target – 3.5-4% given the low level of tradable inflation – and inflation expectations are likely easing.

Makes receiving front end rates a great trade if you’re prepared for the volatility.

LikeLike

There is no higher wholesale market rates or higher cost of capital. Lending interest rates have moved much faster and higher with only a phatetic placating increase in savings deposits. The recent moves is banks showing their cartel muscles in maintaining their profits. In the current flat interest rate environment their lag time profits are being crimped.

LikeLike

Bank economists usually do not forecast correctly intentionally. Their job is about influence rather than unbiased research. It’s the same as asking a cigarette manufacturers science research on the health issues with tobacco smoking.

LikeLike

..a tricky spot; possible long run (come short run?) structural ‘Ds’ of low inflation:

Degregulion of product and labour markets (the embrace of competitive markets should lower prices…)

Debt growth relative to income since the ‘90s (can’t raise rates as impact is deflationary….)

Distribution of income/wealth (those that could spend more don’t need to…)

Disruptive technology (with a swipe of a phone, price/quality comparison is almost unlimited…)

Demographics (when you get old, acquiring ‘stuff’ gets less attractive…..)

If roughly right, perhaps central banks should rely less on NAIRU guess work, ‘wage-price’ spiral concerns, ‘normal’ levels etc….but to be fair to all of them, still somewhat finger in the air stuff!

LikeLike

At least 3 of those I’d argue are a basis for much lower interest rates than the advanced world had in the past – it took higher rates previously to keep demand in check.

Agree that NAIRUs – or any equilibrium relationships – are to a considerable extent guesswork. That is why a lot more weight should go on actual evidence of a sustained pick-up in wage/price inflation measures. If it happens, there is plenty of time to react vigorously, and avoid some future inflationary spiral. If inflation remains lower than target, cut until it isn’t (allowing for lags).

Of course, one could also look at lowering the target itself, but until the ZLB issues are effectively and credibly dealt with my view is that such a change would be foolhardy.

LikeLike

……is there anything within the current legal framework that prevents the RBNZ from expanding its balance sheet via asset purchases? Given the BOJ, Fed, BOE, ECB etc. have undertaken roughly similar actions at the effective LB (and ‘the market’ seems receptive), has the latter more or less become a non issue for other inflation tarrgeting central banks? Plenty of mortgages for the RBNZ to chip away at….

LikeLike

The RB can buy up almost anything it chooses. But I’m not aware of any central banker anywhere who is confident that QE provides options that are as effective as the conventional interest rate mechanism. That is why, for example, John Williams – head of the San Francisco Fed – was recently calling for changes to the specification of the US policy target to help deal with the ZLB challenge the US will face in the next recession. It is actually a bigger problem for the US than for NZ, both because their neutral nominal interest rates are already lower than ours, and because the exchange rate is less important in the US, and less often acts as an effective way of easing mon condiitions – the USD tends to rise in crisis periods in particular. Hence the calls from people like Blanchard and Rogoff for higher inflation targets. While i think that would be a secnd or third best solution, it would be better than drifting into the next major recession having done nothing.

LikeLike

Let’s give the governor his due — he’s more than made up for CPI ‘inflation’ being too low, with the massive house-price inflation he has overseen, whilst being to all intents and purposes powerless to do anything about it. IMHO, try as he might, he has practically no influence on banks’ rate of money creation, and it is banks’ unfettered money creation that has primarily enabled house buyers to bid up prices to the extent that they have.

IMHO, nothing much will change until we have a government with the knowledge and wisdom to switch to a Sovereign Money banking and monetary system, in which banks’ role as money creators ceases and they are forced to become mere financial intermediaries.

LikeLike

Property prices have done what it has always done and that it doubles every 10 years. People forget that 80% of sellers have already houses to sell which means that when you are buying and selling in the same market, price is not a factor. There is absolutely no difference to a buyer at $10million when he can sell at $10million because there is another buyer at $10 million.

The key ingredients of course is market confidence and market arbitration.

LikeLike

You really do have to wonder if the whole theory is deeply flawed. Correct me if I’m wrong Michael but isn’t the transmission mechanism for interest rates to inflation supposed to work by altering the propensity to borrow; low interest rate = more credit money = more inflation.

We have had a whopping 28billion (12% of GDP) of new private sector credit/debt/money mainlined into the economy last financial year yet general inflation is missing in action. Clearly there is no lack of borrowing so what possible difference is a percentage or two of interest rates going to make. Perhaps the theory doesn’t work.

QC has raised some probable causes but also we have what appears to be a glut of “stuff” everywhere you look ( due, in some part, to low interest rates?) with the obvious exception being Auckland houses – thank you out of control immigration and speculators paradise policies from “our” government.

Be interesting to see what happens to our propensity to borrow when property prices decline and the consequences for an economy habituated to astounding levels of fresh credit/money.

LikeLike

David George wrote: “We have had a whopping 28billion (12% of GDP) of new private sector credit/debt/money mainlined into the economy last financial year yet general inflation is missing in action. Clearly there is no lack of borrowing so what possible difference is a percentage or two of interest rates going to make. Perhaps the theory doesn’t work.”

Clearly. almost all of that $28billion enabled house buyers to bid up the prices of houses — which aren’t included in the official measure of inflation, i.e. the CPI.

In saying “Perhaps the theory doesn’t work”, one must first be sure as to what “the theory” actually is. The interest rate that the governor sets — i.e. the Official Cash Rate — bears no direct relationship to the interest rates that banks charge borrowers. Those rates largely depend on borrowers’ willingness and ability to pay.

The following is an excerpt from the Executive Summary of a short paper I wrote last year, explaining how the present banking and monetary system actually works:

Only about 2% of the money in circulation (the money supply, in economics jargon) is notes and coins, issued by the government-owned Reserve Bank of New Zealand (RBNZ). Notes and coins are therefore sovereign money. Unfortunately, as yet there is no such thing as electronic sovereign money. The remaining 98% of the money in circulation consists of bank deposits. The public is largely unaware as to where bank deposits come from. In fact, banks are not financial intermediaries. They do not lend out their customers’ deposits. These facts were spelled out in the unanimous Report of the 1956 New Zealand Royal Commission on Banking, Monetary, and Credit Systems. The Report explained that every bank creates money ex nihilo (out of nothing) when it grants a loan or purchases an asset, simply by creating a ‘deposit’ in its customer’s or supplier’s bank account.

Also, in the paper “Money creation in the modern economy”, in its Quarterly Bulletin for Q1 2014, the Bank of England described how money is created out of nothing as debt to banks when they grant loans and when they purchase assets, and destroyed (i.e. sent back into the nothing from whence it came) whenever any bank loan principal is repaid. This makes the present money system systemically unstable, as banks will always seek to maximise their profits by creating more money than is necessary to keep pace with economic growth.

Prof. Joseph Huber, perhaps the world’s foremost authority on money and banking, reiterates in a recent paper that banks create money whenever they make payments to nonbanks, for example when granting loans and overdrafts, or purchasing assets such as bonds, stocks, other securities or real estate, and also when paying nonbank service providers and salaries and bonuses to employees. Whilst loan principals and all other securities purchases are recorded on a bank’s balance sheet as assets, all payments to service providers and employees are charged to a bank’s P & L statement and thus its equity.

Indeed, the banking system we have is actually a parasitic ‘funny money’ one. Economic booms and bubbles are caused by the fact that the money supply expands when banks create new loans faster than old loans are being repaid. Busts, i.e. recessions, or worse, depressions, are caused when the money supply shrinks as old loans are repaid faster than new loans are being granted. From 2008 to 2013, the US money supply shrank by $4 trillion. This is why the Federal Reserve began a program of Quantitative Easing (QE). Both Prof. Huber and UK economist Adair Turner say that the fact that banks create new money ex nihilo when they grant mortgage loans is the primary driver of real estate and other asset price bubbles. Expanding the money supply faster than the economy is growing causes inflation – of house prices, if not consumer goods.

When an EFTPOS payment or a cheque from a customer of one bank is deposited with a competing bank, not only is money transferred from the payer’s account to the payee’s account, but the payer’s bank owes the payee’s bank an equal amount of RBNZ banknotes. To avoid the inconvenience of physically moving RBNZ banknotes around in the overnight settlement process, the RBNZ – and indeed all central banks, long ago created a second, higher tier of money – unavailable to anyone except the banks and some specified financial institutions, and the central bank – called “reserves”, which nowadays are RBNZ electronic digits.

Each night, a computerised settlement process takes place to net-out these inter-bank debts. So at the end of every day each bank either owes one or more of the other banks, or is owed, some reserves. Thus “reserves follow deposits”. Banks therefore need to hold some reserves, which they borrow from the RBNZ at 50 basis points (= 0.5%) above the Official Cash Rate (OCR), the OCR being the interest rate that the RBNZ pays on deposits of banks’ surplus reserves. If a bank doesn’t have enough RBNZ reserves and cannot borrow them from another bank at an interest rate below that which it would have to pay the RBNZ, that bank borrows them “on demand” from the RBNZ at the OCR + 0.5%.

It is the unenviable task of the governor of the RBNZ to attempt to control CPI inflation by continually adjusting the Official Cash Rate (OCR), which is the interest rate that the RBNZ pays banks for the excess reserves that they have deposited with the RBNZ. For for the last four years, CPI inflation has been well below the governor’s target range.

LikeLike

PJM :- “Clearly, almost all of that $28 billion enabled house buyers to bid up the prices of houses”

A very bold statement

I disagree with the inference that $28 billion was used to “bid up” house prices

In my opinion the most destructive force in Auckland house pricing was the arrival of “bolt-Hole” money laundered by Foxes arriving in Auckland paying price-no-object amounts which set prices in the favoured suburbs at the margin

Once the prices were established ans accepted and baked in, locals became reliant on bank funding to meet the market in what can only be described as catch up mode and has continued to this day – even though the Fox-Breeding season appears to have subsided – meanwhile the ensconced foxes are sitting quiet and holding on – beat them if you want

LikeLike

With the Chinese shutting down capital outflows and the 40% equity LVR rules still in place, we are seeing credit liquidity tightening fast. The RBNZ really should pay attention and start loosening before the building industry runs out of steam soon. I would not be too surprised if the economy stalls next year into a recession.

LikeLike

Thanks for the replies, the 28 billion is the net increase of debt in the private sector so includes business and farm loans and becomes real money as it is spent into the economy. It is net of repayments and obviously doesn’t include overseas money flowing into (for example) Auckland housing. There is plenty to suggest that there is a significant speculative element to the house price rises as well as very high levels of immigration and new supply delays and restrictions.

Any outstanding debt repaid by the vendor as a consequence of the sale of a house, farm or other asset would reduce the total debt increase the same as any repayment.

I take your points PJM ; my concern is that, even with this extraordinary increase in money, inflation is very subdued and what happens when it stops. This level of increase in the money supply/debt is similar to the 2000’s prior to the GFC so perhaps worthy of concern.

LikeLike

For a layman Inflation is Ronald Regan’s thief in the night. A studious article complaining that our thief is not stealing enough.

Nobody has mentioned that in the 70’s these graphs would all be empty with lines way above the top. Even moving the decimal point to the right would have left some of the peaks truncated. It is as if we are living on another planet. A target of 2% and hitting 1.5% doesn’t sound like failure, more like going for the bull and getting an inner. However I suspect the article was mainly about “”… has been too invested in a story that the economy was strong “”. Wishful thinking is a universal failing but maybe the exceptionally intelligent are better with their justifications and therefore slower to appreciate reality.

The main benefit of inflation is making management of a staff easier; anyone who is being paid above their level of competence receives token pay rises; this is so much less dramatic than either cutting wages or sacking a useful but not exceptional worker.

In my life inflation barely impinges; just a quiet retirement with no interest in boys toys (boats and cars) but my superannuation is boosted annually and seems to keep it in line with supermarket prices. Inflation is noticed when we receive our two large annual bills: rates and insurance. Watching the news explains the rational increases in insurance but Auckland council seems to exist in a different country that is ravaged by inflation.

Must not end this post grumpy: a few weeks ago I bought a shirt and some shorts at the Warehouse and realised they cost just about the same as 40 years ago – it really has been a Chinese miracle and we all have benefited from it.

LikeLike

Bob

Yes, agree inflation is, in principle, a bad thing. But we had our Minister of Finance ask our Governor to target 2%, and he didn’t come close to delivering. Perhaps the differences seem small, but over time they aren’t and especially as they’ve come to some extent at the cost of a higher than necessary number of people unemployed.

I’d be all for an inflation target centred on (true) zero – there are some modest biases in the index – but only if we fix the issues around the inability to cut nominal interest rates much below zero, which at present looks likely to be a real problem in the next recession. Sadly, neither the govt nor the Bank seem to be doing anything to get ready.

All that said, i recall coming back from working on monetary policy in Zambia, where inflation was 300%+ when i got there and still perhaps 30% when I left, and taking some considerable time back at the RBNZ before i could really care much about changes in the inflation forecasts of 0.2 or even 0.5 percentage points, around a target (then) centred on 1% inflation.

Fully take your point about the cost of basic clothes. Then again, check out the cost of a university education cf 40 years ago…..

LikeLike

My university education was 50 years ago and cost me nothing and my parents generously topped up my living allowance. Very much cheaper than now. But you are not comparing like with like – 50 years ago a degree was obtained by about 5% of school leavers and now it is nearer 50%. It used to carry far more status. No idea if it is more difficult – young graduates seem just as dumb and disinterested in the world around them as they did in the seventies.

LikeLike

like with like comparisons are always hard. 50 years ago, my mother rarely bought kids’ clothes, she made them instead.

LikeLike

My University eduction was paid for by the Australian taxpayer so I guess not all baby boomers are benefitted from NZ free education.

LikeLike

All my clothing is now pretty much plastic. My $90 discounted Kathmandu jacket is 90% polyester and 10% stretch elastane. My leisure wear black pants costs $10 on discount from Kmart and is the same polyester/elastane. My Warehouse black leisure wear long sleeve sports shirts are also $20 on discount are also polyester/elastane. My socks and boxers from Farmers are also polyester/elastane. My $60 Nike shoes from Warehouse is leather top but the rest is plastic.

LikeLike

if you wait a couple of weeks, the Warehouse would usually offer a 30% discount on the retail price. You should check out the 15 a pack plastic hangers. Last year retailed for $4 and now $2. That’s an incredible drop in price for plastic. No wonder our wool industry is struggling. plastic products are falling in line with the very low oil prices.

LikeLike