As regular readers know, I tend not to be particular upbeat about the New Zealand economic story. For anyone new, there should be a hint in the very title of the blog. If, by chance, you are still attracted to an upbeat take, only last week in a post here I critiqued a recent book chapter taking that sort of view.

And so I was a bit surprised when, more than a year ago now, I was asked to write a chapter for a forthcoming book on aspects of policymaking, and associated outcomes, in a small state (this one). In principle, the book sounded potentially interesting, and they were approaching a bunch of pretty serious and senior people to contribute. But it wasn’t clear there was much in it for me, and since the plan was for the introduction or foreword to have been written by the head of the Department of Prime Minister and Cabinet, it seemed likely that the thrust the organisers were looking for was a positive take on the New Zealand story. So as not to mess people about, I declined the invitation, only to have my arm twisted, with assurances that there was no such agenda. In the end I agreed to write something, and although the organisers/editors still seem keen on a more positive spin, by the time I discovered that I was committed.

The latest draft of my chapter, attempting to be positive where I can, is here.

An underperforming economy; the insufficiently recognised implications of distance (draft chapter)

I’ve had useful comments from various people on an earlier draft (none of them bear any responsibility for the current version though), but if any readers have comments you’d like to add to the mix, you can earlier leave them as comments to this post or email me directly (address in the “About Michael Reddell’s blog” tab).

The potential market for the book, as I understand it, is people like students of public policy, perhaps in parts of Asia. Many of these potential readers, I’m given to understand, see New Zealand as a sucesss story. Within the (severe) limitations of length, I’ve set out to provide a more balanced take on the economic story. In a way, I guess, New Zealand is a sort of success story. 200 years ago on these islands there was not much more than a subsistence economy, and only recently had overseas trade resumed after the inhabitants had been isolated for several hundred years. From that to one of the richest countries in the world in a hundred years was remarkable. And even now, after a century of relative decline, there is only a handful of countries in east Asia and the southwest Pacific with material living standards matching or exceeding our own (Australia, Japan, Singapore, Taiwan, with South Korea coming close). And from a macroeconomic policy perspective, we’ve now had low and stable inflation again for 25 years, have had low and stable public debt, and a considerable measure of financial stability. That isn’t nothing by any means.

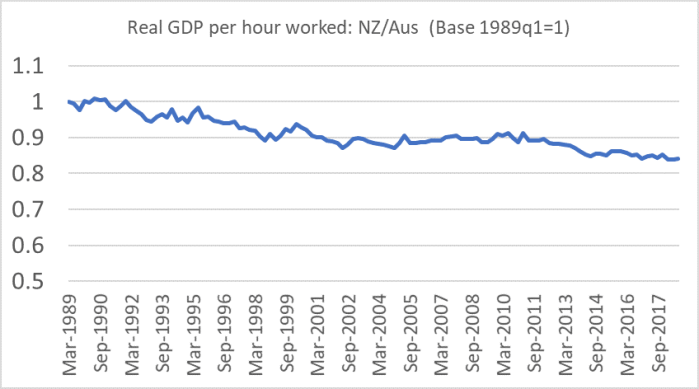

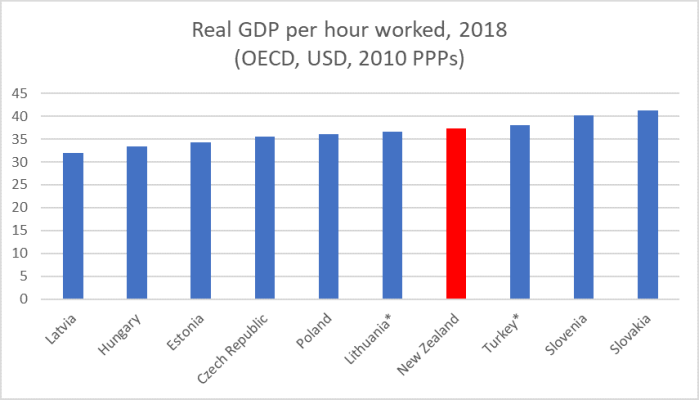

But it doesn’t exactly mark us out. What does mark us out is that century of relative decline: of course, we are much richer than we were 100 years or so ago, but then we were among the top three countries in the world (GDP per capita), and now we languish a long way down the advanced country rankings (especially on productivity measures). With productivity levels not quite 60 per cent of those in the leading bunch of advanced economies, we are getting closer to the point where New Zealand could really only be described as an upper middle income country.

My story, as a regular readers know, is that our physical remoteness – in an era where, internet notwithstanding, distance appears to be not much less of a constraint than ever in many respects – is the key issue in our underperformance. It isn’t that – as some models and sets of estimated equations suggest – distant countries are inevitably poorer, but that distant countries seem to thrive (to the extent they do) mostly on natural resources, and industries building directly on those resources. And with a limited stock of natural resources, there are limits to the number of people that such places can support top tier incomes for (a very different proposition than for economies – eg those of northwest Europe – where most of the most productive economies are found) where natural resources are simply no longer that important, and where the advantages of proximity can be realised more readily. The story is much the same for Australia as for New Zealand – and Australia has also been in (less severe) relative decline over the last 100 years – with the difference that Australia found itself able to utilise whole new sets of natural resources, either unknown or uneconomic previously. New Zealand has had nothing – that material – similar, and no big asymmetric technology shocks in our favour for a long time either. Against that backdrop, using policy to drive population growth (rapid by advanced country standards) simply did not make sense – putting more people in a fairly unpropitious location, albeit one with some reasonable economic institutions (rule of law etc). It didn’t make sense decades ago – before people fully appreciated the nature of New Zealand’s relative economic decline – and it doesn’t now. There was a valuable signal, that policymakers and their advisers simply chose to ignore, when New Zealanders – who know New Zealand best – starting leaving in numbers that (while cyclical variable) are really large by international or historical standards (absent a civil war or the like).

Perhaps the new bit to my story in this draft chapter – which was prompted by the way the initial specification was framed – was to think about why the stark economic underperformance has been allowed to go on, not just by our politicians and political parties, but with no compelling remedies offered by our major economic policy advisory institutions (The Treasury in particular) or by international agencies that offer advice (notably the OECD). I suggest a story in which it is simply difficult to identify that right comparator countries when thinking about economywide productivity and economic performance issues. For many areas of policy – monetary policy is an example, but it is probably true of health and education and welfare – pretty much any advanced market economies can offer useful benchmarking, but if remoteness really does matter (not just to, say, defence, but) to the viable options and business opportunities available here, then the experiences of – say – Belgium or Denmark just aren’t likely to be that useful, even if Denmark has a similar population and was once the major competitor for UK dairy markets.

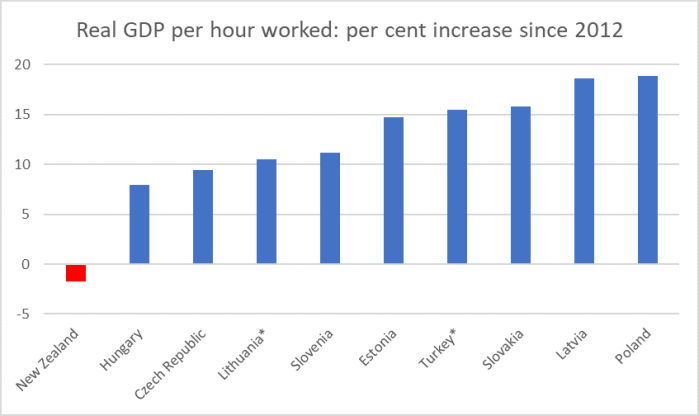

We may be able to learn something from reflecting on the differences, but it is typically much more compelling if one can point to another similar country (or 2 or 10 of them) and learn from them. And thus I note an important difference between New Zealand and many of the (now fast) emerging advanced economies of central and eastern Europe. Not only are they physically proximate to various highly productive economies (easy and cheap to meet fellow policymakers and analysts regularly, including in EU fora), but have a lot of similarities across each other (similar location, similar communist past, and so on). I don’t claim to know Hungary, Slovenia, the Czech Republic or Slovakia in great detail, but if I were a policymaker in any of them, I’d be (almost obsessively) benchmarking my economic policies against those of the others, and of nearby rich and productive countries (eg Austria and Switzerland). There are never exact parallels, but in New Zealand’s case it is hard to find good parallels at all. I suggest that Israel might be in some respects the best for New Zealand – but it is little studied here (and its productivity performance is about as bad as ours – partly, I’ve suggested, for similar reasons).

The lack of easy examples to benchmark ourselves against isn’t really an acceptable excuse, but I suspect it is part of the explanation. It is long been a problem for the OECD in their advice to New Zealand: they’ve repeatedly brought a northern European mindset to a remote corner of the world, after early on investing quite a lot in the idea that the New Zealand reforms were exemplary, and almost sure to reverse our underperformance. Places like the OECD work a lot on illustrating cross-country comparisons, but they simply never found the right ones for New Zealand (on these economywide issues) and have not shown much sign of trying. It is particularly problematic because the OECD are full-on committed to high immigration, regardless of the experience of an individual country (see my post about the then OECD Chief Economist extraordinary performance when she launched their 2017 New Zealand report – there is a new report due out in a few weeks, and I’m not holding my breath).

Of course, New Zealand politicians no longer seem to have any appetite for trying to reverse the staggering decline in New Zealand’s relative performance. But just possibly they might if their advisers were offering a compelling diagnosis and set of prescriptions. As it, The Treasury seems to have no more idea than the OECD, and seems to have abandoned much interest in the productivity issue, in favour of the feel-goodism and smorgasbord of random indicators that makes up the Living Standards Framework, supporting the “wellbeing Budget”. I was exchanging notes the other day with someone about the mystery as to who the next Secretary to the Treasury will be (there is a vacancy a month from now, and applications closed three months ago). It is hard to be optimistic that it will make much difference who gets the job – given the hoops they will have to have jumped through to get it – but sadly it is a story of a low-level equilibrium: no political demand for answers and options to reverse our decades of relative decline. and no bureaucratic supply of such answers or the supporting analysis either.

Anyway, for anyone interested here are the concluding paragraphs.

Conclusion

After the bold reforming period of the 1980s and early 1990s, official and political economic policymaking in New Zealand appears to have been at sea, without a tiller or compass, for at least a couple of decades. Much that was positive was done during the reform era, and various good institutional reforms were put in place. Much needed to be done, and in some respects it was to the credit of a small country that so much – initially attracting considerable international admiration – could have been put in place so quickly. Seared by the experience of the quasi-crisis of 1984, and rapid escalation of official debt in the previous decade, New Zealand has since enjoyed an enviable degree of macroeconomic stability: low and stable public debt, low and stable inflation, and domestic financial stability (even amid severe policy-induced upward pressures on house prices and household debt). Unemployment rates that are fairly low on average are another successful element. In those areas of policy, meaningful international benchmarks have provided a routine check of policy, and the external advice sometimes provided has typically been drawn from countries (small floating exchange rate countries), where the comparisons are apt and insightful.

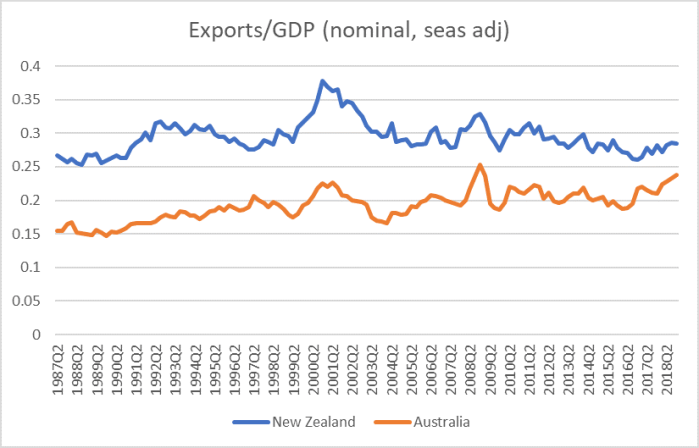

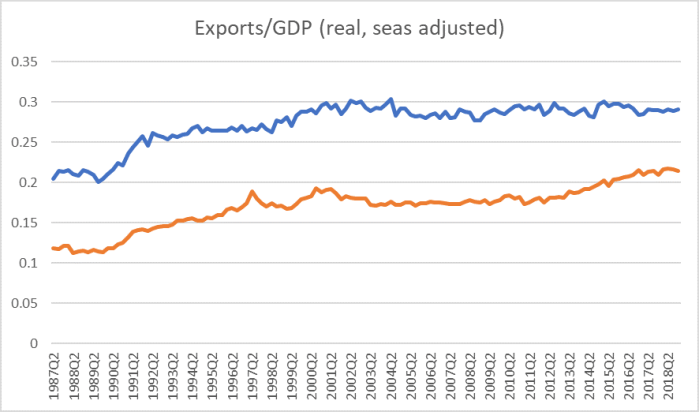

But if stability has been successfully regained and maintained, on the wider counts of economic performance only a “fail” mark could possibly be assigned. Among the failures, policymakers managed to preside over reforms that have created artificial scarcity of urban land and sky-high housing prices, in common with many of their Anglo peers. But the productivity failure is more stark, because it is more specific to New Zealand. Despite numerous (de)regulatory steps taken to open the economy to international competition – and a considerable increase in the real volume of exports and imports – foreign trade as a share of GDP has shrunk and with it the relative size of the tradables sector. The export sector itself remains heavily dominated by industries reliant on domestic natural resources (a fixed asset) – services exports have been shrinking as a share of GDP – and, despite rapid population growth, business investment has been modest at best.

To an outsider, perhaps the surprising feature of such an underperforming advanced economy is that population growth has nonetheless been quite rapid. Birth rates have been below long-term replacement rates for several decades now. But defying the revealed preferences of New Zealanders, who have left the country in huge (but cyclically variable) numbers over the last 50 years for 25 years now policy has been set to bring in one of the largest migrant flows (per capita) of any advanced country. Regularly presented as a skills-focused approach, it has remained difficult to attract many really talented people to a small remote country with lagging incomes and productivity[1] and there have been few (apparent or realised) outward-oriented economic opportunities in New Zealand for either natives or migrants.

Advocates and defenders of New Zealand immigration policy often attempt to invoke arguments and indicative evidence from other countries. Even then, the value of insights appears more limited than the champions believe: not one of the high immigration advanced economies (Canada, Australia, New Zealand, Israel – or the United States) has been at the forefront of productivity growth over the last 50 years, and only the US is now near the frontier in levels terms. But even if those arguments might have some validity in some other countries, there has been too little serious engagement with the specifics of the New Zealand situation: remoteness, lack of newly-exploitable natural resources, and the actual experience (lack of demonstrable gains for New Zealanders) following 25 years with a high level of (notionally) skills-based immigration. As by far the most remote of any advanced country, it is perhaps the last place one might naturally expect to see policy actively working (encouraged by local officials and international agencies) to support rapid population growth.

Looking ahead, if New Zealanders are once again to enjoy incomes and material living standards matching the best in the OECD, policy and academic analysts will have to focus afresh on the implications, and limitations, of New Zealand’s extreme remoteness and how best policy should be shaped in light the unchangeable nature of that constraint (at least on current technologies) Past experience – 1890s, 1930s, and 1980s – shows that policies can change quickly and markedly in New Zealand. But with no reason to expect any sort of dramatic crisis – macro-economic conditions are stable, unlike the situation in the early 1980s – it is difficult to see what might now break policy out of the 21st century torpor or, indeed, whether the economics institutions would have the capacity to respond effectively if there was to be renewed political appetite for change.

[1] OECD (2016) adult skills data suggest that although the gap between skills of natives and migrants is small, migrants to New Zealand are, on average, less skilled than natives.

There won’t be any posts for a few days as we are heading off this morning to attend the funeral for my wife’s (extremely aged) grandmother. Back blogging on Tuesday.