Just a quick post today, prompted by yesterday afternoon’s about the change in the formulation of the debt target foreshadowed by the Minister of Finance.

My proposition was that, with a target range 10 percentage points wide, governments will be expected to stay within that range (more or less) all the time. And that will means that in normal times – proxied by when the output gap (perhaps adjusted for the terms of trade) is around zero – the government will still have to hold pretty closely to the 20 per cent of GDP target midpoint. They might be able to safely fluctuate between 19 per cent and 21 per cent (or thereabouts) but anything much beyond that would run a material risk of moving outside the target range – prompting either procyclical fiscal adjustments or the abandonment of the target – the next time a reasonably significant recession hit. That risk is compounded by the fact that output gaps – and detrended terms of trade – are only really best guesses in the first place. When we think the output gap is zero, hindsight might reveal it to have been +2 per cent of GDP – increasing the probable revenue losses when the economy next takes a hit.

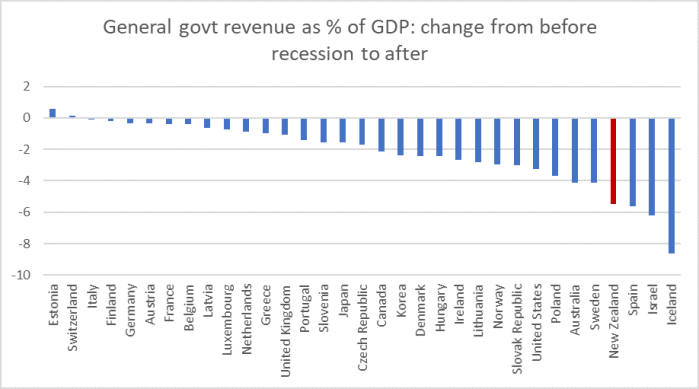

I noted in yesterday’s post that New Zealand government tax revenue had fallen by around 6 percentage points of GDP in the period from the peak in the years just prior to the recession to the trough in the years just after. Not all of that was cyclical – there were some tax cuts just prior to the recession, and again in late 2010 – but much of it probably was. And whether or not the revenue loss was the automatic stabilisers at work or discretionary policy changes, a debt target would have constrained choices (on the tax side) that governments of the day had thought appropriate. And my more general point was that a couple of years in which taxes/GDP were a couple of percentage points lower than normal – adding to the debt – shouldn’t be thought exceptional.

But I thought I should check that, and so I dug out the data on government current revenue (mostly taxes) as a per cent of GDP, to see what had happened in other countries in and around the 2008/09 recession. Here is the change by country (lowest year just after the recession less highest year just prior).

New Zealand – which did have a pretty severe recession – had the fourth biggest reduction in revenue as a share of GDP. I guess that was exaggerated by the effect of the discretionary changes.

But what really interested me was that I noticed a number for the euro-area as a whole. Revenue as a share of GDP had barely changed, in aggregate across the whole area. The whole area, of course, had monetary policy adjustment open to it, but individual countries that are in the euro-area did not.

But the median fall in the share of revenue to GDP for OECD countries not in the euro area was 2.9 percentage points. On the other hand, the reduction for the median euro-area country was only 0.7 percentage points. I guess that was a mix of crisis countries, indebted countries, the Maastricht fiscal rules, or whatever. But given the limitations of monetary policy, it hardly seems like an optimal adjustment: automatic stabilisers (in mostly quite high tax countries) should probably have generated more of a fall just on their own.

Anyway, it left me pretty comfortable that my ad hoc suggestion that the government needs to plan around its fiscal target on the basis that a serious recession could easily knock a couple of percentage points of GDP off revenue for a couple of years at least, which in turn would add to the debt. If they don’t do so, they could find themselves engaged in pro-cyclical fiscal adjustment, which will be even more problematic in the next recession, given how much closer to the limits of conventional monetary policy we (and other countries) are likely to be.