Yesterday afternoon I saw this in my Twitter feed

My first thought was along the lines of “well, I guess there is nothing about New Zealand economic policy”, (a) so poor has our long-term performance been, and (b) because surely outcomes matter?. But I’m a policy geek sort of person, ANZSOG is chaired by our very own State Services Commissioner, and ANU is the top-ranked university in Australasia, so I clicked the link to see what examples of successful policymaking in New Zealand they’d found. To my surprise I found this

New Zealand’s economic turnaround: How public policy innovation catalysed economic growth (PDF, 0.2MB) – Michael Mintrom and Madeline Thomas

(Downloads of all the individual chapters appear to be free, and there are pieces on ACC, early childhood education, Kiwisaver, nuclear-free New Zealand, and so on, some of which may interest some readers.)

But I was a bit flummoxed even by the title of this economic chapter. I recognised the “public policy innovation” – thirty years on I still support most of it – but the idea of an “economic turnaround” or “catalysed economic growth” seemed, to say the least, at odds with the data.

Mintrom is a public policy academic, now at Monash University in Melbourne. He worked for The Treasury for a few years in the late 1980s before heading off to do his PhD. But, from the look of his publications, he seems to know a lot about public policy processes, but not necessarily a great deal about economic growth or overall economic performance. Thomas is his research assistant, with a psychology degree and some experience working on social policy with local governments.

When I got into the chapter itself it turned out the authors were focusing on a handful of specific initiatives undertaken in the late 1980s and early 1990s:

- reduction of market interventions (controls, subsidies, import restrictions etc),

- creation of SOEs and subsequent privatisations,

- simplification of the tax system and introduction of GST, and

- passing responsibility for monetary policy to an independent Reserve Bank.

And they lay out early on how they define success. Their first criterion is endurance, and thus they argue that “these policy innovations have now remained in place for decades. Thus, judged by endurance, they have been highly successful.”

There, it would appear, speaks someone more interested in processes than outcomes. After all, the broad range of policies the 1980s and 90s reforms replaced – exchange controls, heavy import protection, monetary policy set by ministers – also lasted for decades, and were generally not accounted a success. The Soviet Union managed 70 years.

But the authors offer three other perspectives from which to view the success of the policy programme. There was something called the “programmatic perspective”, which seems to be encapsulated in these two sentences:

A highly coherent theory of change guided the development of these policy innovations. After a relatively short time, it was clear the changes were producing beneficial outcomes.

Then there is the “process perspective”, where they claim (and I mostly wouldn’t disagree) that “the policy innovations were well designed and generally well managed”.

And, thirdly, there is the political perspective, which they describe as “more complicated”. That, presumably, does duty not only for the deep divisions that opened up in the Labour Party, Jim Anderton’s breakaway, and the divisions that opened up in National, culminating in the founding of New Zealand First, to all of which one could add the public sense that politicians hadn’t been straight with them (many readers will be too young to recall that in 1987 Labour published its manifesto the week after the election) and the replacement of FPP by MMP (you may think that change good, but it simply wouldn’t have happened without the ructions of the previous few years).

Remarkably, in a chapter focused on economic policy and – at least according to the title – economic growth, the authors take as their “starting point” several very positive assessments of the reforms written from 1994 to 1996. Some of those articles are valuable, but each was written with the benefit of almost no distance or perspective, and were written a quarter of a century ago. I found it remarkable that in a chapter about New Zealand’s economic growth, there were no references at all to the literature over at least the last decade about New Zealand’s disappointing productivity performance (sometimes, but quite wrongly, characterised as the New Zealand “productivity paradox”). Those concerns, from extremely orthodox sources, have been around much longer than that: I happened to be dipping into the OECD’s 2000 report on New Zealand yesterday and found explicit concerns there about the failure of the New Zealand economy to converge, highlighting in particular the disappointing productivity growth.

The first part of the chapter is devoted to rehearsing some of the political and economic context for the reforms – with which I mostly have only relatively minor quibbles – before they move on to focus on the four areas of reform (listed above). Again, as pure description, it isn’t too bad – with the odd annoying mistake (eg the exchange rate was not pegged to the US dollar in 1984, the price freeze had been lifted before the 1984 election), but whenever there is any sort of evaluative tone it is almost always very upbeat. And perhaps only a young Treasury official from those days could describe, with a straight face, the Treasury’s approach to other departments as “Treasury analysts showed a great desire to….seek insight from colleagues in other departments”.

There is a variety of odd claims. Thus,

The move to a more independent Reserve Bank came after several years of a floating New Zealand dollar, which was also viewed as a key element of market liberalisation; it was therefore uncontroversial.

Where did they get that from? The Reserve Bank Act was intensely controversial at the time, with considerable opposition (wrongheadly in my view, but it was there nonetheless) from most prominent academic economists in New Zealand and some vocal business lobby groups. The authors talk up the legislation passing Parliament unanimously (perhaps so if Jim Anderton was away that day), but if they’d done even the slightest refreshing of memories, they’d have been aware that the legislation divided both major party caucuses. National – in Opposition – voted for the legislation, but Ruth Richardson’s former economic adviser recorded later that the vote in favour at caucus secured a majority of only one: Sir Robert Muldoon (opposed) was away seriously ill, and Winston Peters (opposed) for some reason skipped the meeting. And I’ve perhaps mentioned before that in every subsequent election – down to and including 2017 – one or other political party was campaigning on a platform of changing the Policy Targets Agreement or the Reserve Bank Act.

There are other odd claims. The authors are mildly circumspect about aspects of the privatisation programme (“some sales were poorly managed”), but then cite as evidence of the “policy success” of the Labour government’s privatisation programme, that the succeeding National government did more privatisations.

The authors begin their Analysis and Conclusions section suggesting that in the early 80s New Zealand was heading towards “economic collapse”, but that is simply overblown political rhetoric for a process of stagnation, fairly high and variable inflation, and rising debt. The broad direction of policy was still towards liberalisation, but it was a halting, half-hearted, and inconsistent process. A crisis it wasn’t – even if forced devaluations make good headlines. Thus, the authors note that “unemployment grew” and yet the historical backdating of the HLFS suggests that the unemployment rate in June 1984 was 4.4 per cent, almost identical to the current rate.

What else struck me? There was the claim – about the 80s period – that “through listening and working with others – even those who might have strong objections to a proposals – it is possible for advocates of change to improve policy design and build a strong colation to support change”. No doubt that is true generally, but it bears very resemblance to anyone else’s impressions of 1980s/90s reform period – it was. after all, Roger Douglas, who championed the approach of “crash through or crash”.

Our authors carry this lesson forward:

“subsequent New Zealand governments have achieved important reforms while moving more slowly and working to ensure implementation is well managed. For example, the National Party-led coalition of 2009-17 [wasn’t a coalition, and it was 2008-17, but I guess those are details] established a new program of privatisation of government assets. Important work was done that drew on lessons from hre past and met considerable success.”

You might – as I did – have supported those more recent partial privatisations, but lets remember how small they were. One of the companies involved was already market-listed (Air New Zealand) and all are still majority state-owned. And the list of “important reforms” undertaken by that more recent government was limited, to say the very least.

The very final (short) paragraph begins this way.

In sum,we judge New Zealand’s economic turnaround to have been a major public policy success. Innovative public policy changes catalysed economic growth.

And yet, remarkably, in the entire chapter there is not a single number or chart or even a discussion of the specifics of economic growth. Not one. And despite (rightly) lauding the removal of protection and subsidies, no mention of the fact that foreign trade as a share of GDP is no higher now than it was in 1984. Absent evidence of this “catalysed economic growth”, perhaps we are just supposed to imagine it, and somehow feel better for the thought? But I hope this isn’t how ANZSOG helps train our public servants.

My own take on the reform and stabilisation effort of the 1980s/90s is roughly as follows:

- stabilisation was a major success. We have low and stable inflation, low and fairly stable government debt. We also have a considerable measure of financial stability. For all that, we should be truly grateful. But we should also recognise that (a) low and stable became a pretty global phenomenon (especially in the advanced world) around that time, and (b) that various other well-managed countries (eg Australia, Canada, Sweden, Switzerland) have much the same sort of fiscal record we do. That leaves me sceptical of stories which put too much emphasis on specific New Zealand events, circumstances, law, individuals, or policy processes. Moreover – and I don’t think this appears in the chapter at all – we have greatly benefited from a big increase in the terms of trade (reversing the couple of decade decline that policymakers from the late 60s to mid 80s had to cope with),

- many of the specific reforms (including those Mintrom and Thomas deal with) served us well. Lower import protection, a well-designed GST, injecting much greater efficiency into state trading operations and a bunch of others benefited most New Zealanders.

- but that isn’t true of all the reforms. One might focus in on the RMA and associated provisions which have given us among the most unaffordable house and urban land prices in the developed world, or one might look at the tax treatment of savings. And then there are the immigration policy reforms.

- and, as honest observers have known for 20 years, there has simply not been the productivity turnaround that champions of the reforms hoped for at the time (and there is also no reason to suppose that problem is just that we didn’t engage in radical enough reform.)

Here is a table I was working on the other day, comparing average productivity in New Zealand with that of a leading bunch of OECD countries.

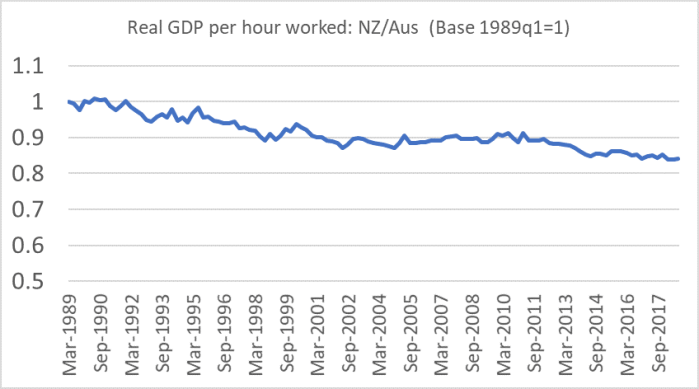

The book was an ANZSOG project. Here is labour productivity for New Zealand relative to Australia, indexed to when the New Zealand domestic data start in 1989.

I reckon there is a plausible argument that the whole reform programme taken together slowed the rate of decline in New Zealand’s relative fortunes (although even that isn’t clear-cut: the rate of decline slowed, but I’ve not seen any careful attempt to assess how much of that was policy and how much about, say, improvements in the terms of trade).

But that isn’t the case Mintrom and Thomas attempt to make. Judged by economic growth outcomes – the sort of criterion their title asks us to use – the programme just cannot be judged a great success. Perhaps the processes were good in some respects, and there was certainly a lot of intellectual rigour behind some of the reforms. It remains a fascinating case study in concentrated far-reaching reform. But the productivity results really suggest that the episode belongs in another book, about the disappointing results despite the very best of intentions. Those are salutary lessons policy advisers need to be trained in too.

How we – certainly anyone who supported, voted for, worked on the reforms – wish the outcomes had been different – much better. But they weren’t. That is a failure – uncomfortable as it is, there is no other word for it – politicians and policy advisers have to grapple with honestly.