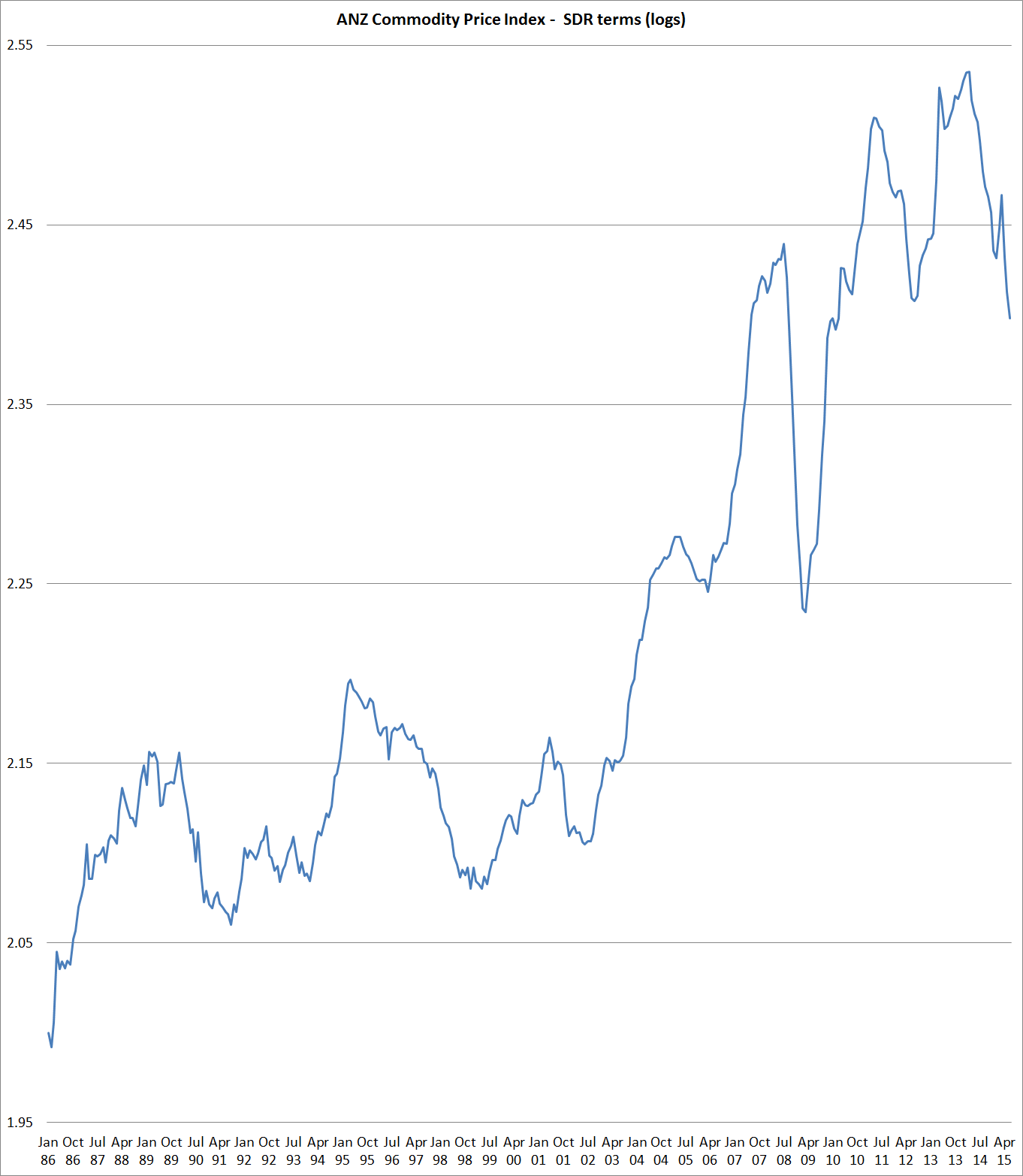

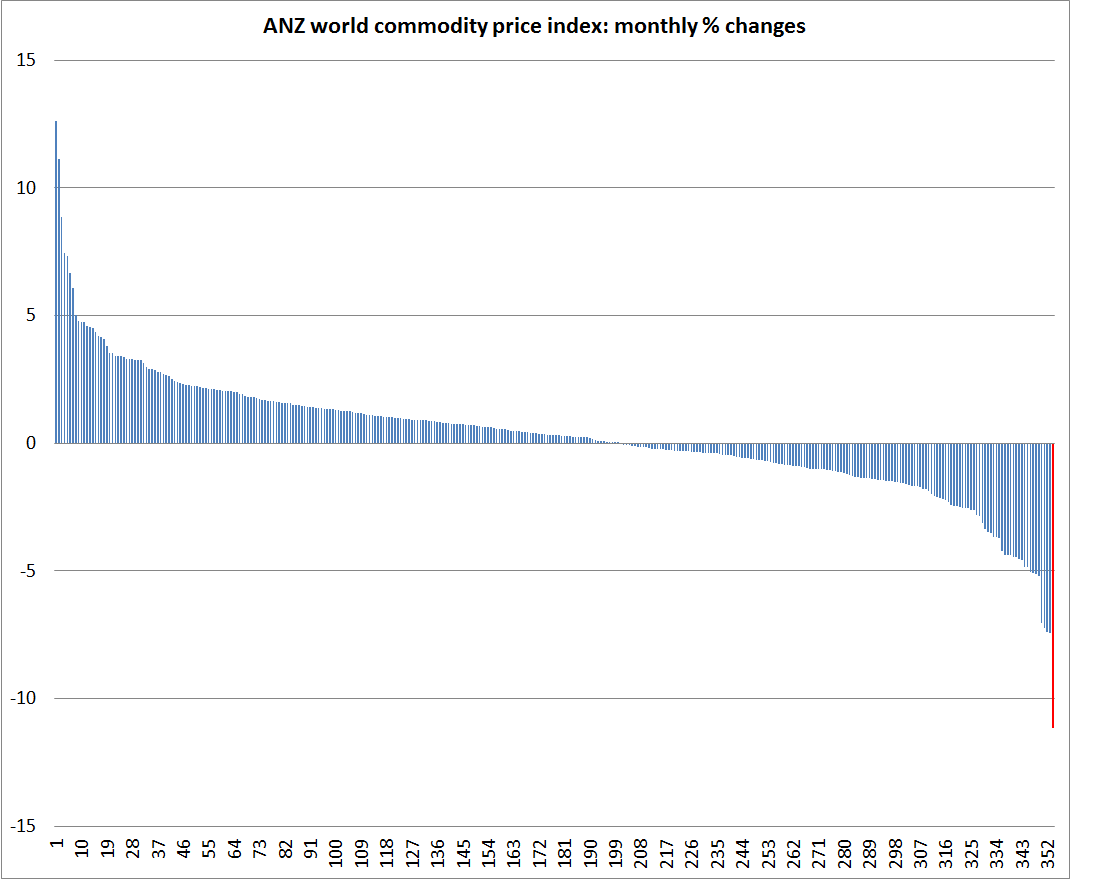

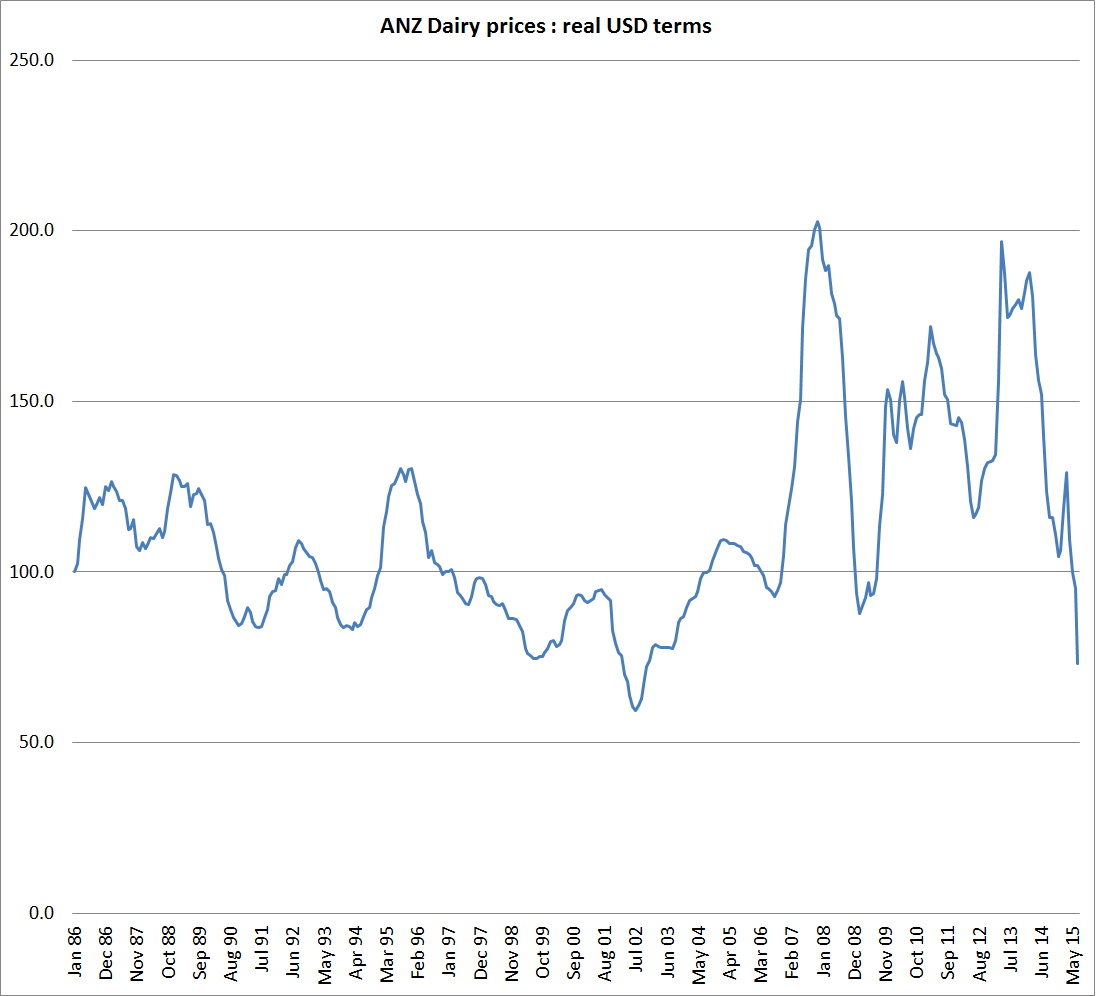

In the last 24 hours we’ve had two gloomy headline indicators out. The ANZ Commodity Price Index for July was out, with a record 11 per cent fall in the world prices of New Zealand export commodities. And the latest GDT auction saw another 10 per cent fall in whole milk powder prices, with portents of further falls to come.

Neither piece of news was that surprising on the day, but to say that is to risk underestimating the severity of what has been going on.

As the ANZ notes, the latest fall was the largest fall in the almost 30 year history of their series. What they didn’t mention is that it was the largest fall by a large margin. By an even larger margin it was the largest monthly fall in world dairy prices.

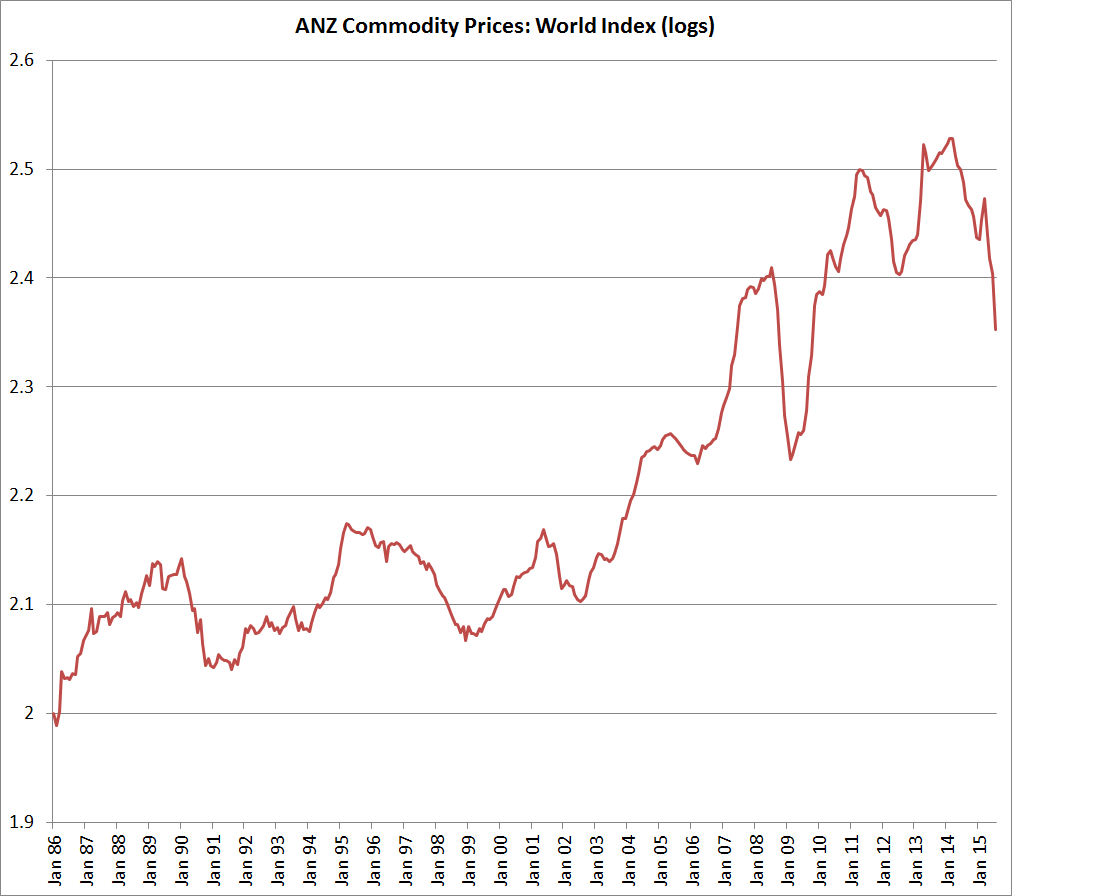

On the ANZ measure, the scale of the fall in commodity prices in the last year or so now matches what happened during the 2008/09 recession.

For dairy prices themselves, the fall in the GDT index now materially exceeds the scale of the fall in 2008/09. Real dairy prices now appear to be around the lowest levels for 30 years – although not necessarily at levels wildly inconsistent with trends up to 2006.

The fall in commodity prices didn’t cause New Zealand’s recession in 2008/09. A drought didn’t help. Neither did lingering inflationary pressures that for a while made the Reserve Bank reluctant to cut the OCR. And, of course, there was the recession that engulfed the rest of the world, which in turn helped exaggerate the fall in commodity prices. So I’m not suggesting that the falls in New Zealand commodity prices necessarily mean we are now heading for negative GDP quarters, but the loss of national income is now large and the risks of some pretty bad outcomes must be rising. There are no forces operating in the other direction, to boost growth rates. The real exchange rate is only around 10 per cent below the average for the previous couple of years – as I pointed out the other day, that is a pretty modest adjustment by historical standards.

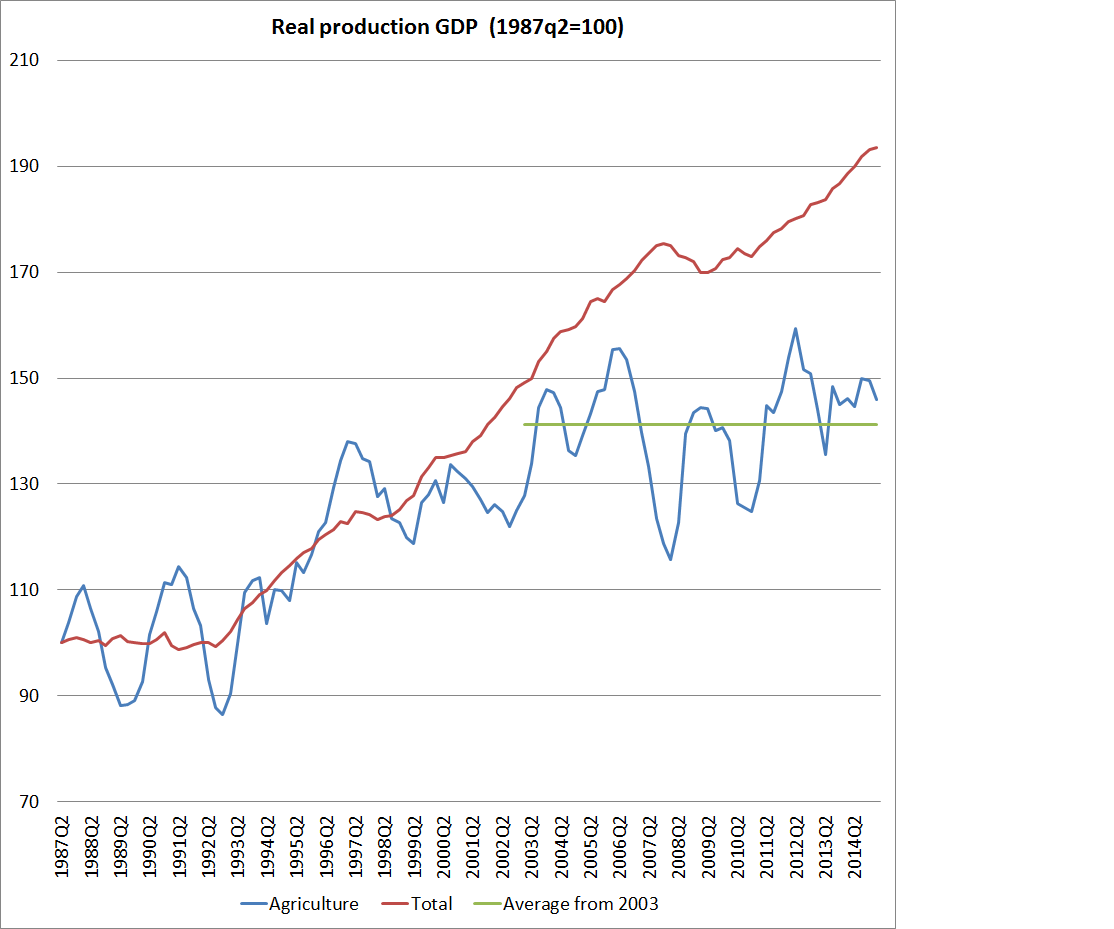

For a few years, I’ve been intrigued by how little growth there has been in real value-added in the agricultural sector. The terms of trade have been high, and in particular world dairy prices have been high, and yet over 10 years or so there has been almost no growth in what SNZ record as real value-added in the agricultural sector. Here is the most recent version of a chart I’ve run previously.

Total factor productivity growth in agriculture has also been quite remarkably weak.

I’ve noted previously that some of this may have reflected the incentives of rising prices. It is well-known that dairy production processes have become much more input-intensive over the last decade or more. Much of that is about supplementary feed, but it also includes irrigation and other more capital-intensive production models. In principle, in the face of high product prices these additional inputs could improve the profitability of the agricultural sector, even though the real (constant price) value-added is not increased. If more inputs are being used to produce more outputs, and those outputs can be sold profitably, then it is just one of the ways in which farmers (and their suppliers) capture the benefits of the rising terms of trade.

I was never sure quite how persuasive that reassuring story was. But a reader has got in touch to point me to some papers which suggest that things might be nowhere near as rosy as that story suggests. A basic proposition of economics is that one should produce to the point where the marginal revenue from the additional production equals the marginal cost of doing so. Beyond that point, one starts losing money on every additional unit of production.

I don’t suppose anyone imagines that this model exactly describes how any single business actually operates. But it is a tendency towards which economists typically, and implicitly, assume that firms in a competitive market will gravitate. Why, for example, would one produce more if you were going to lose money on each new unit of production. And in the rural sector, where land is huge component of inputs, a farmer generating the highest rates of profit should be able to bid a higher price for land. Resources should gravitate to those best able to use them.

But there is no guarantee of this happening, especially over relatively short periods of time.

In their paper “The intensification of the NZ Dairy Industry – Ferrari cows being run on two-stroke fuel on a road to nowhere?”, presented at an agricultural economics conference last year, Peter Fraser and two co-authors (Warren Anderson, an academic at Massey, and Barrie Ridler,a Principal at Grazing Systems Limited) argue that many New Zealand dairy farmers have been applying anything but the principle of producing until marginal revenue equals marginal cost. I spent quite a bit of time working with Peter during the 2008/09 dairy price crash – I knew about debt but he (at MAF) knew, and taught me, a lot about dairy. I have a lot of time for his (often-trenchantly-expressed) views.

Fraser et al argue that most of the farm models used by farmers and their advisors in New Zealand take an average cost approach rather than a marginal cost approach, which is inducing increases in production beyond the point of profit maximisation.

none of the mainstream dairy industry farming simulation models (e.g. the Whole Farm Model, Farmax, DairyMax, Udder) and performance measures (e.g. information derived from Dairy Base or Red Sky, benchmarks such as milksolids per hectare, average profit per hectare, gross farm returns, production at x percentile, etc.) are economic models or measures as none employ marginal analysis. As a result, none can profit maximise at a farm level and all are likely to lead to a production decision where marginal costs are greater than marginal revenue.

They argue that this misinformation has not been driven out by competitive processes partly because many dairy farmers are not necessarily setting out to be profit-maximisers.

The corollary is that if farmers are focused on accumulating assets then a ‘satisficing’ position of having sufficient cash flows to pay drawings and to service debt is likely to suffice. Critically, this can also explain why more resources are flowing into the dairy industry: farmers are willing to borrow (and banks willing to lend) in order to accumulate assets (and potentially realise [untaxed] capital gains, especially if converting a dry stock farm into a dairy farm, as this is akin to property development).

In short, a combination of systemic misinformation combined with farmer motives can go a fair way towards explaining why a $10 note may be left on the pavement after all.

One can debate whether this explanation for why is wholly persuasive (the more aggressive dairy developments in recent years, seem far removed from the traditional Waikato or Taranaki (satisficing?) family dairy farmer), but the fact that many farmers are not getting good marginal-based advice and analysis does seem reasonably clear.

Fraser et all go on to support their case with results from a Lincoln University model farm, suggesting that using more sophisticated models (using marginal analysis) profit maximisation would typically result from milking fewer cows (per hectare).

The argument appears to be that much of the growth in total milk production in New Zealand in recent years (perhaps 10-15 per cent of total production) is resulting from an average-cost led focus on boosting total production, rather than maximising profits. Even at the higher prices that were prevailing until recently, production volumes should probably have been lower (the authors also note the potential environmental benefits).

Quite how all this feeds into thinking about the current situation, and the likely response to falling payouts, I’m not sure. Marginal revenue is plummeting, and even an average-cost based approach would presumably lead to some reduction in production. On the other hand, there is an awfully large stock of debt to service, and maintaining production levels remains sensible if (but only if, and only to the extent that) current payouts are covering short-run marginal costs.

Relatedly, a reader notes:

I would contend that the family farming structure adapts more readily to the pressure of a price slump. The corporates’ general means of survival is by committing more capital to sustain an existing production plan. Family farms shift more quickly into survival mode and if the household has a trained nurse or teacher sends her back to work to support the family household! The dairy industry in its drive to maximise total production has blithely discarded the flexibilities inherent in the cooperative based systems developed over the previous 150 years. It seems there may be a price to be paid for that negligence.

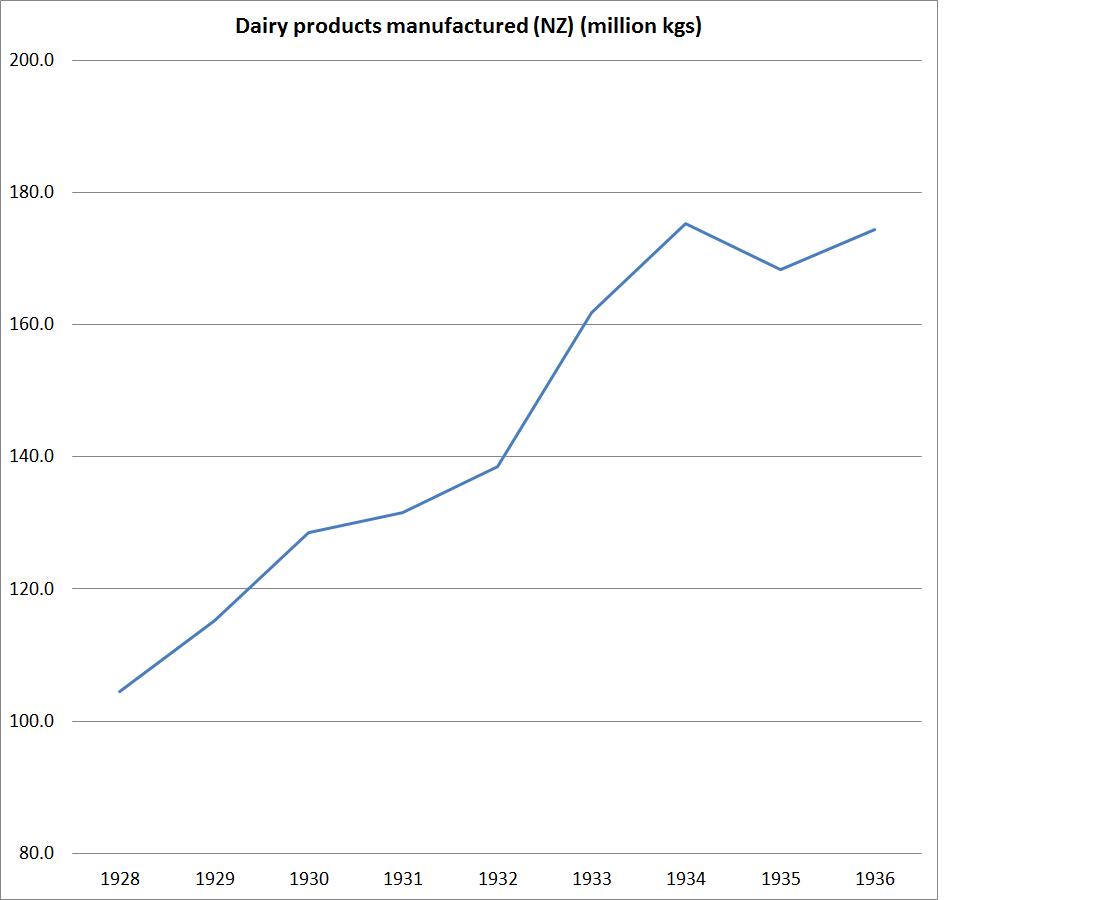

On which note, however, I have long been struck by the production response of the New Zealand dairy industry to the collapse of export prices in the Great Depression If one didn’t price the farmer’s family labour, short-run variable marginal costs were presumably extremely low, and there was a great deal of debt to service.

I don’t claim expertise in this area, but I found the analysis stimulating and one reconciliation for those otherwise puzzling GDP data I showed earlier. It does look as though participants in the industry will need to think harder about how best to maximise returns, not just production. I like driving obscure and remote roads when we travel the country on family holidays, and I’m often prompted to wonder about the economics of collecting milk from the remote suppliers that linger in such places, and just how long that can go on. On its own that is a small issue, but perhaps symptomatic of an industry not yet adequately focused on medium to long-term profit maximisation. Industry structure issues often crop up in the context of discussions like this. Co-operative structures or not should be a choice for farmers – and they are common internationally in the dairy sector – but direct government legislative interventions facilitated the existing, less than fully competitive, industry structure. So far, the gains to New Zealand from having done so are less than fully apparent.