The Governor’s OCR press release this morning held few surprises. Disappointments, yes, but not really any surprises. Given that in the June MPS the Governor had articulated only a fairly modest change of view, and had refused to acknowledge any sort of mistake in how monetary policy had been run last year, it was hardly surprising that, at a review between MPSs, at which he does not have the benefit of a full new set of forecasts, he wasn’t willing to cut by 50 basis points, as some had suggested was likely. From the tone of the news release, such a cut probably wasn’t even seriously considered.

But if two cuts in six weeks might have broadly kept pace with the deteriorating data over the last couple of months, it does not make any inroads into the overly tight policy put in place when the Governor (and his advisers) misread inflation pressures last year. And that is the bigger problem. The Bank still seems to think it has things broadly right.

Here was my list of some sobering inflation statistics from my post last week in the wake of the CPI

Reciting the history in numbers gets a little repetitive, but:

• December 2009 was the last time the sectoral factor model measure of core inflation was at or above the target midpoint (2 per cent)

• Annual non-tradables inflation has been lower than at present only briefly, in 2001, when the inflation target itself was 0.5 percentage points lower than it is now.

• Non-tradables inflation is only as high as it is because of the large contribution being made by tobacco tax increases (which aren’t “inflation” in any meaningful sense).

• Even with the rebound in petrol prices, CPI inflation ex tobacco was -0.1 over the last year – this at the peak of a building boom.

• CPI ex petrol inflation has never been lower (than the current 0.7 per cent) in the 15 years for which SNZ report the data.

• Both trimmed mean and weighted median measures of inflation have reached new lows, and appear to be as low as they’ve ever been.

This, by contrast, is the Bank’s take:

Headline inflation is currently below the Bank’s 1 to 3 percent target range, due largely to previous strength in the New Zealand dollar and a large decline in world oil prices.

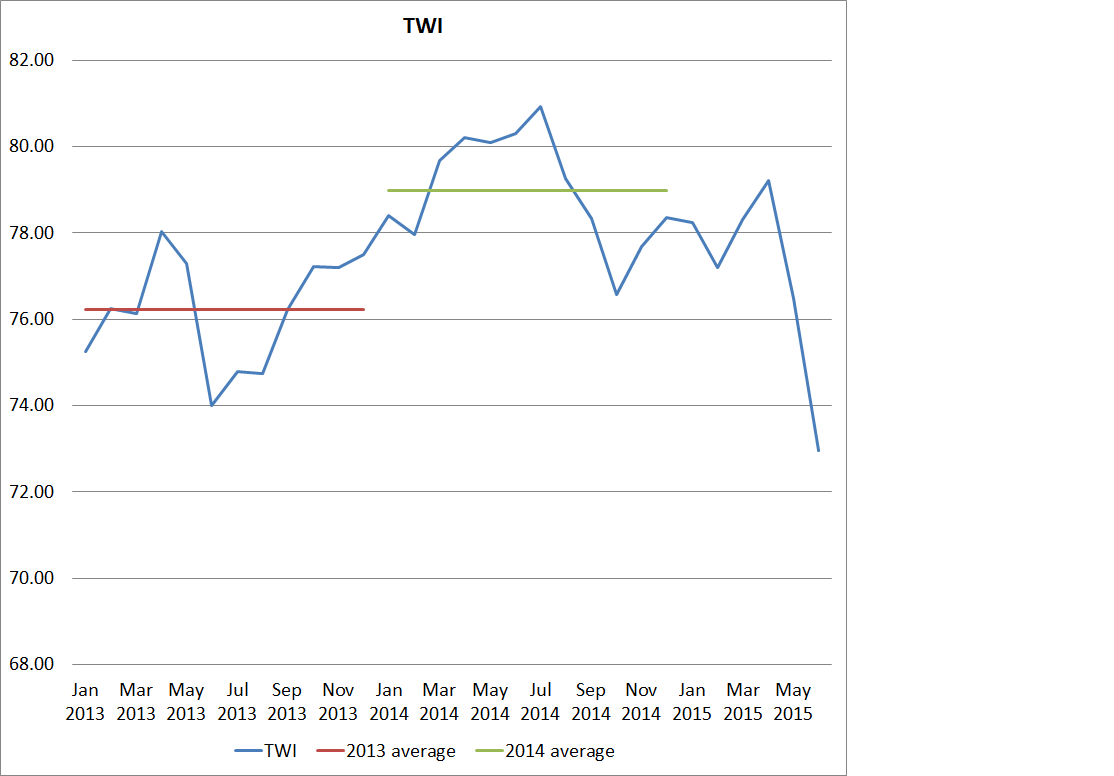

It just doesn’t wash. CPI inflation ex-petrol was 0.7 per cent in the year to June. CPI inflation ex tobacco (large excise increases) was…..actually not inflation, but slight deflation, a fall of 0.1 per cent in the last year. And what of the exchange rate? Direct exchange rate effects are not that large these days, but typically pass into consumer prices quite quickly (and one of the fastest routes is through petrol pricing). The TWI in 2014 was around 4 per cent higher than in 2013, but that increase probably only subtracted around 0.4 percentage points from the annual inflation rate. And as the TWI peaked in the middle of last year, the effect might have been even smaller by the year to June, the most recent CPI inflation we have.

Focusing on headline inflation, as the Bank does in the extract above, seems like an effort to distract attention from the surprisingly weak core domestic inflation, whichever indicator of it one prefers to concentrate on. And that weakness came at the very peak of a major building boom.

I was also a bit disappointed to see this sentence in the statement

While the currency depreciation will provide support to the export and import competing sectors, further depreciation is necessary given the weakness in export commodity prices.

Today would have been a good opportunity to have backed away from commenting on the exchange rate, except as it affects the inflation outlook, in these statements. What does “necessary” here mean? I assume it means something about stabilising the NIIP position (as a % of GDP) at a lower level, or improving the long-term growth prospects for New Zealand. But that has nothing to do with monetary policy. The nominal exchange rate is not an instrument in the Governor’s toolkit, and the real exchange rate is…well…a real phenomenon. I happen to agree with the Governor’s unease about the level of the real exchange rate, but it is an endogenous real phenomenon. Better for the Governor to focus on getting core inflation back to around the target midpoint – not just headline, relying on direct price effects of the lower exchange rate. As it happens, the OCR path consistent with that obligation of the Governor’s would probably lower the exchange rate somewhat further as well.

I’ve made the point previously, but will state it again. When the Reserve Bank – even more than other international central banks – has misjudged inflation pressures for so long, it would be better for them now to err on the side of running policy a little looser than they really think wise. Clearly there is something wrong in their mental model of inflation at present (and I’m not suggesting anyone else has a fully persuasive alternative), but after years of such low inflation, it might no bad thing if core inflation ended up a little above the target midpoint for a few quarters a year or two down the track. I’m not suggesting a price level target, just that the policy reaction function needs to take more, and more aggressive, account of the repeated over-forecasting of inflation, and inflation pressures. Among others, the 5.8 per cent of the labour force still unemployed might appreciate the chance to get back to work.

To play devil’s advocate, the CPI is actually much higher and probably above the 1-3% band. Wrongly, housing prices are now left out of the index and only rental prices included. We prefer to say we have low inflation and somewhere over there an asset bubble which we’ll ignore, but as a consumer you have to pay for it anyway.

Clearly we all have to have somewhere to live. Housing is not an optional asset class, it is something that has to be consumed either through outright purchase or rental. With about 32% of the population living in Auckland and Auckland house prices increasing in double digit figures, inclusion of housing purchase costs would have a material impact on the CPI figure.

LikeLike

A reasonable counter, except that the Governor and Minister actively chose to set the target for the CPI as currently defined (ie with construction costs in, but not existing house prices). If the govt wants to change the target, then the RB should deliver on that new target.

There is a counter argument in the other direction. The cost of accommodation is really the rental cost of housing. If we calculated the CPI that way (as say the consumption deflator in the national accounts does) inflation would be even lower than the current measure. Reasonable people can differ on the appropriate definition: personally, I have a historical hankering for the imputed rents measure (which the RB used to favour) and tend to think the current method is a reasonable middle ground compromise. It is also the method used in Australia.

LikeLike

Hi Michael,

Did you have any thoughts on Governor Wheeler’s speech this morning? As you noted in this post, he still seems to think they have policy settings broadly right, especially in his little dig – “Some local commentators have predicted large declines in interest rates over coming months that could only be consistent with the economy moving into recession”.

LikeLike

“Pretty bad” would be my succinct summary. Having been out for much of the day, I will blog about it tomorrow.

LikeLike

Excellent Michael, loved your contribution on Q & A. I believe our exchange rate is now too low & is well under valued. Check the economists Big Mac Burger prices which suggests our exchange rate should be 75c or slightly higher.My biggest grumble at the moment is the retail price of milk which should have dropped 50% to match the 50% drop at the farm gate. If this happened the CPI would quickly fall.

Does a currency trader (the PM) make a good judge of the NZ exchange rate?

Keith

LikeLike

Thanks Keith. We can agree to differ on the exchange rate. And no, I wouldn’t have thought being a trader (and then, mainly, a manager of traders) gave any great insight into exchange rate levels. Short-term exchange rate dynamics are another things – traders tend to trump economists there.

LikeLike