On Donal Curtin’s blog the other day I noticed a reference to a recent paper published in New Zealand Economic Papers (unusually it appears to be accessible to non-subscribers) that looked at, among other things, whether inflation targeting had reduced the variability of long-term interest rates in New Zealand and Australia. They conclude that it has. Donal uses the results to encourage politicians to stay clear of any changes to monetary policy.

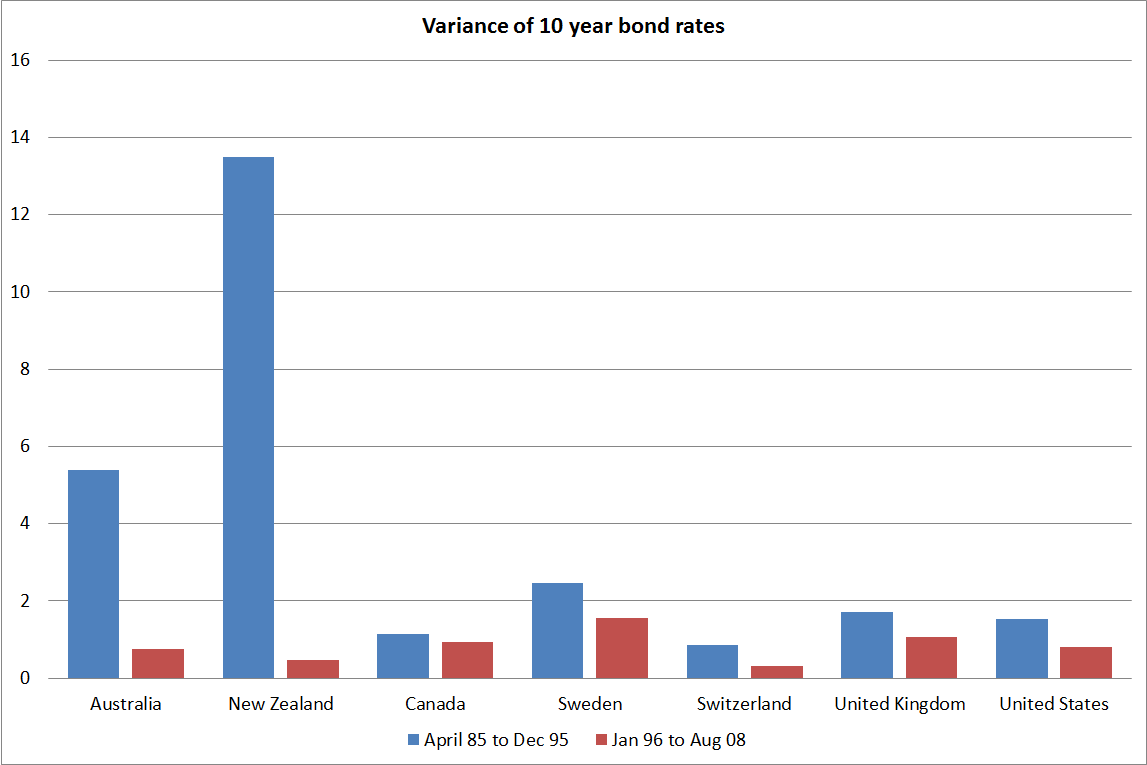

There is no doubt that long-term interest rates in New Zealand (and Australia) are much less variable than they were in the early days of liberalisation. There was an awful lot going on back then. The authors present the data for two sub-periods, April 1985 to December 1995 (which commences shortly after New Zealand interest rates were liberalised), and January 1996 to August 2008 (a period which ends just prior to the worst of the crisis, and the prevalence of near-zero short-term interest rates in many countries). For the countries they report, here are the data:

In the late 1980s, inflation in Australia and New Zealand was also much higher than in the other countries. Australia’s inflation rate averaged around 8 per cent, and New Zealand’s 10 per cent, while the US had an inflation rate of around 4 per cent. Sweden’s inflation rate was also still on the high side.

There is little doubt that getting inflation under control (lower and less variable) was part of what helped markedly reduce the variability in nominal interest rates. It did that in all these countries. But how much of that is down to “inflation targeting” per se? I’d suggest very little. After all, as early as 1990q3, just a few months after the first PTA was signed, New Zealand’s annual CPI inflation rate was already the second lowest among the countries these authors look at. In the UK case, the central bank didn’t even have operational independence until mid-1997, and in the United States anything closely resembling inflation targeting really only dates to the last few years.

I don’t want to get into a debate here as to whether inflation targeting is the best option for advanced economies these days, but to get a better sense of the contribution of inflation targeting we’d really need a country (preferably several) to change their regime. A decade with several countries running NGDP targets, or wage inflation targets, or even price levels targets, in parallel with others still running inflation targets might shed rather more light on the issue. For New Zealand, as I’ve argued elsewhere, inflation targeting was a specific form of articulating a commitment to more stable macro conditions than we’d had previously. It may have provided more discipline (on the Reserve Bank) than operating without an explicit target, but even there one could be reasonably sceptical. Most other advanced countries had already got inflation a long way down – as had we (see above) before they got very serious about anything like inflation targeting.

There is a variety of good reasons for encouraging Opposition parties not to tamper too much with the essence of the monetary policy targeting framework (and perhaps to focus their energies instead on reforming the Reserve Bank, including its governance framework). Whatever is wrong with New Zealand’s economic performance over the long-term has little or nothing to do with the details of the monetary policy arrangements. But I wouldn’t take much from this NZEP paper on that score. It won’t, for example, shed any light on whether the Labour Party’s proposed restatement of the goal would make things better or worse, or just make no difference.

Here is how Labour last year proposed to amend section 8 of the Reserve Bank Act. The new section would read.

“The primary function of the Bank with respect to monetary policy is to enhance New Zealand’s economic welfare through maintaining stability in the general level of prices in a manner which best assists in achieving a positive external balance over the economic cycle, thereby having the most favourable impact on the stability of economic growth and the level of employment.”

It was clever piece of drafting. I argued at the time, and still believe, that it would have made no material difference to the conduct of monetary policy. The inclusion of similar sorts of words in the Policy Targets Agreement in 1996 didn’t (but it allowed Winston Peters to tell the world that he had secured changes). I was never sure whether Labour recognised, or not, that the change would make little or no difference. I think their people were smart enough to know, but also to know that, in political positioning product differentiation and branding matter.

Of course, other possible changes might make more difference. Some might (conceivably) be for the better. There is certainly no reason to suppose that inflation targeting will prove to be the last word in how best to conduct monetary policy.

Inflation targeting sounds like a good idea; it would let market participants form better estimates of the prices at which they will be able to buy and sell goods and services in the future. Unfortunately monetary authorities have implemented inflation ceiling policies with little concern for negative deviations from target, creating a lot of unnecessary uncertainty. Of course rather than a price level (= average inflation target) it would probably be better to have a target for the level of NGDP. At least that way when some gold bug rants about the monetary authority “debasing the currency” the reply will be we are just stabilizing the growth of incomes, not “intentionally” targeting higher inflation.

LikeLike

[…] – Mean Squared Errors My longstanding hatred and loathing of logit – Chris Blattman How sacrosanct should inflation targeting be? – croaking cassandra Examining Federal Reserve reform proposals – Brookings Institution The Big Lesson of the […]

LikeLike