Longstanding readers will know that I was pretty critical of the previous government for the utter absence of any sign of a set of economic policies that might have begun to reverse the decades of relative economic decline. Worse, they and their acolytes too often seemed to make up stories about how well things were going when the data pretty clearly pointed in the opposite direction. I’m not sure I’d be quite as harsh as Kerry McDonald and Don Brash, who recently gave the Key-English government an overall score of 0/10, but I’d be close, especially around productivity (and also around housing).

What has become increasingly disconcerting is that the new government – now almost a third of the way through its term – also has no credible ideas about reversing the decline and little interest either. They seem increasingly reduced to making stuff up as well, and trotting out the same lines again and again without any sign of a really understanding the challenge, without any sign of a compelling analytical framework, and without any reason to think that the policies they talk of will make any material (helpful) difference.

I woke this morning to the news that the Minister of Finance had an op-ed in the Herald explaining how the government was going to restore our economic fortunes. With suitably low expectations, I tracked it down. Even with low expectations, I was struck by how weak it was, and left wondering why the Minister and his PR team thought the article was a good idea.

The Minister begins thus

The coalition Government is helping business modernise our economy to be fit for purpose for the 21st century.

Presumably he is aware that one sixth of the 21st century has already gone? And that his party was in government for half that time? But let that pass: as rhetoric it might be empty, but it is probably harmless.

This means being smarter in how we work, lifting the value of what we produce and export, supporting the environment, planning for future generations and giving everyone a fair shot at success. It means making sure that all hard-working Kiwis share in the rewards of economic growth.

All of which is hard to argue with, but isn’t exactly a) specific, or (b) new. I keep a copy of National’s 1975 election manifesto by my desk, and flicking through it – 43 years on now – I think I spotted all those points (actually, in light of Eugenie Sage’s announcement on Sunday, I also found a pledge to “discourage all forms of environmental pollution and encourage the recycling of materials. We will place a levy on difficult-to-dispose-of products’). Labour’s 1972 manifesto, or its 1984 one, or its 1999 one probably had them all too.

Most New Zealanders know we cannot go on relying on a volatile mix of population growth, an overheated housing market buoyed by speculation, and exporting raw commodities as our growth drivers.

Quite a bit of that was in the 1975 manifesto too. They are old lines, each trotted out by politicians of either main party for decades as the symptoms presented. Not always even very accurately – does anyone actually think an “overheated housing market buoyed by speculation” added to national prosperity? And not with much sense that the speaker had any sort of robust model of the New Zealand economy. Let alone serious policies in response: for example, if this paragraph is to be believed, the current government is apparently uneasy about rapid population growth, but continues to run the same immigration policy as both its predecessor governments for the last 20 years.

And despite all this, a few sentences later the Minister of Finance tries to assert that

the fundamentals fuelling the economy are strong

Quite which “fundamentals” he has in mind – presumably not those in the previous quote (above) – isn’t clear. In fact, all he offers in support of his view is

Last week, the Reserve Bank said growth will still average 3 per cent over the next three years. And Mainfreight managing director Don Braid said recently: “I think the business environment is good right now.”

A government agency whose forecasts seem to command increasing scepticism among other forecasters, and one prominent business person. Perhaps you are persuaded. I’m not.

But finally we get to some of the things the government is promising. First, what the Minister presents as a key component

Our plan to become more productive is built on getting our infrastructure sorted. This year, and for the next 10 years, we will invest more than $4 billion getting roads, rail and coastal shipping humming. We are sorting out Auckland’s congestion to save the $1b loss in productivity it causes each year.

Haven’t we heard these infrastructure stories (“we are taking steps to clear the backlog”) for 15 years now? But even if they are doing everything well in this area, look at the number in the final sentence. $1 billion – assuming the estimate is robust – is a great deal of money to you and me individually, but this is an economy with an annual GDP of $280 billion. On the Minister’s own numbers, fixing congestion would lift GDP by about 0.36 per cent. It would be very welcome, but it is tiny relative to the scale of the economic underperformance: with no productivity growth at all for the last three years, it might take 10 similar initiatives to just reverse the further slippage (relative to other countries) in the last few years. But this was the only hard number in the entire article.

So what else does the Minister have to offer in his economic strategy?

We are investing to improve the skills of our workforce so that workers can adapt to changing workplaces. New programmes like our Mana in Mahi/Strength in Work apprenticeship scheme will get young people off the dole and support employers with the costs of giving them an apprenticeship to help them grow their business.

As I’ve noted numerous times previously, on OECD data New Zealand workers are among the most highly-skilled in the OECD. And where the government is spending most heavily in the broad area of skills, it seems to be in providing fee-free tertiary education – a policy that will (a) mostly redistribute money to people (and their families) who would already undertake tertiary education, and (b) to the limited extent it encourages further participation, presumably do so mostly among those for whom tertiary education offers lower expected returns. It doesn’t have the feel of a productivity-enhancing policy, and the government has not (that I’ve seen) offered any numbers to the contrary. As for getting “young people off the dole”, it is (of course) a worthy objective but haven’t we seen many such initiatives in the last 50 years?

Other policies supporting small and medium enterprises to manage costs include greater access to training programmes, e-invoicing and cutting compliance costs.

There may well be some useful stuff in that list. But surely every government in modern times has talked of cutting compliance costs? And, in practice, haven’t most ended up increasing them overall? The previous government liked to boast of the 500 (?) items that comprised its Business Growth Agenda, but none of it (not even all of it) began to reverse decades of underperformance. It was symptom of the drive for action without analysis.

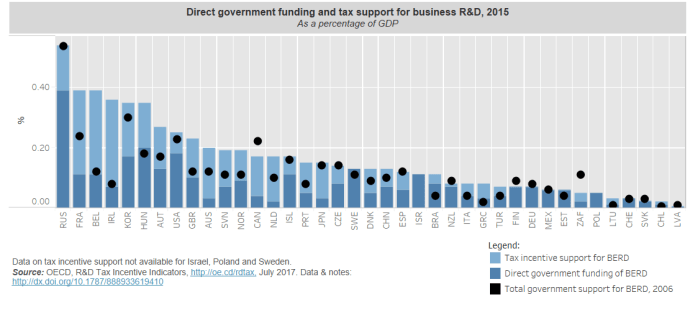

New Zealand was built on innovation. The best path for us to get richer as a country is to invest in new opportunities and find better ways of doing things. The coalition Government is supporting business to lift research and development investment, with $1b set aside in the Budget for R&D tax incentives.

Hard to disagree with the second sentence, but without some compelling analysis suggesting that the government and its advisers understand why firms haven’t regarded it as worth their while to spend more heavily on R&D, it is difficult to be optimistic that more subsidies are the answer. As I noted in an earlier post on the government’s proposals in this area

R&D tax credits aren’t the only form of government spending to subsidise business R&D – in fact, the government’s new scheme involves doing away with the current grants. And as it happens, OECD numbers suggests we already spend more (per cent of GDP) on such subsidies than Germany (DEU), and quite a lot more than Switzerland (CHE). [both of which have far far higher levels of actual business R&D]

All of which might suggest taking a few steps back and thinking harder about why firms themselves don’t see it as worth undertaking very much R&D spending here. But given a choice between hard-headed sceptical analysis and being seen to “do something”, all too often it is the latter that seems to win out.

But we are only stepping up to the big stuff

Our bold goal for New Zealand to have a net zero emissions economy by 2050 is essential as we face up to climate change. This goal creates economic opportunities. The business community is alongside us, with 60 of our biggest firms forming the Climate Leaders Coalition. The $100 million Green Investment Fund and the One Billion Trees initiative are key parts of this work.

Perhaps it is “essential”. Perhaps it even creates “economic opportunities” – big changes in regulation and relative prices always do, for some people. But the government’s own consultative document, and modelling commissioned for them from NZIER, suggests that once one looks at the entire economy, a serious net-zero emissions target by 2050 will result in losses of real GDP per capita of 10 to 22 per cent (relative to the baseline in which no such target is adopted by New Zealand). No democratic government is history has ever consulted on proposals that would lead to such a dramatic fall in expected future living standards and productivity. And, as a reminder, on the government’s own numbers, the costs would fall wildly disproportionately on the poorest New Zealanders. And, yes, there probably will be a lot more trees planted – many of them probably on good, easy to access and harvest, land – but just last week the government had to announce large subsidies to get even that programme underway. Subsidies have never been the path to improved economywide economic prosperity. Of course, few suppose the government proposes adopting a net-zero target for economic purposes, but they should at least stop misrepresenting the analysis on the economic effects from their own consultants.

We are also committed to ensuring no one is left behind in our economy. That’s why we have put in place the Families Package and lifted the minimum wage. It is why we have a $1b annual fund for regional infrastructure and economic development opportunities.

So the regions are so “stuffed” that only an annual subsidy scheme is going to help ensure they aren’t “left behind”? That seems to be the implication of what the Minister of Finance is saying there. And perhaps the Minister skipped over the likely tension between the laudable desire (see above) to get young people off the dole, and the really substantial increase in the minimum wage his government is putting in place (at a time when there is little or no economywide productivity growth)?

There are challenges in the world that are outside of New Zealand’s control. That is why we are running a surplus and being prudent with our debt levels. We are also diversifying our export markets to create new opportunities for our exporters.

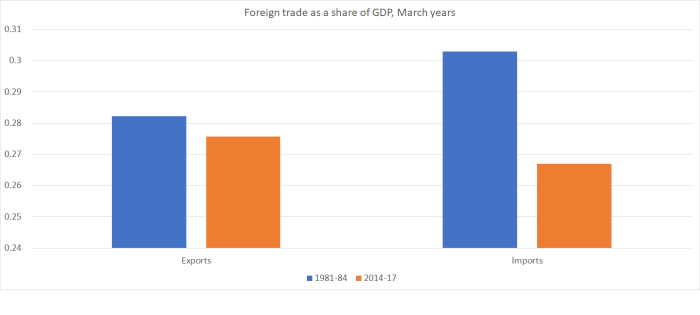

There is no hint of what, specifically, the Minister has in mind with his final sentence. But there is a certain sameness to it, going back decades and decades (nice quotes – including about the potential role of forestry – in that 1975 manifesto I mentioned earlier). And, actually, taken over the decades there has been a huge amount of diversification of export markets – no single country takes more than a quarter of New Zealand firms’ exports – but it hasn’t enabled New Zealand to lift the foreign trade share of its GDP much. In fact, over the last 35 years that share has shrunk.

As Don Brash noted in his article the other day, the previous government had fine words too

Key spoke about the need to increase the export orientation of the economy, and set a target for exports of goods and services of 40 per cent of GDP, up from 30 per cent when he came to office. Today, exports are just 27 per cent of GDP

Just no policies to make a difference.

The Minister of Finance attempts to end his article on an upbeat note

We are committed to working with business, workers and communities to build a stronger, more productive economy that delivers the quality of life that all New Zealanders deserve.

A worthy objective indeed, but there is nothing in what he told his readers that is likely to address – and begin to reverse – the decades and decades of underperformance. If we take seriously the government’s own numbers around the proposed emissions goal, the relative underperformance could be even worse under this government (were it to win nine years in office) than under its two predecessors.

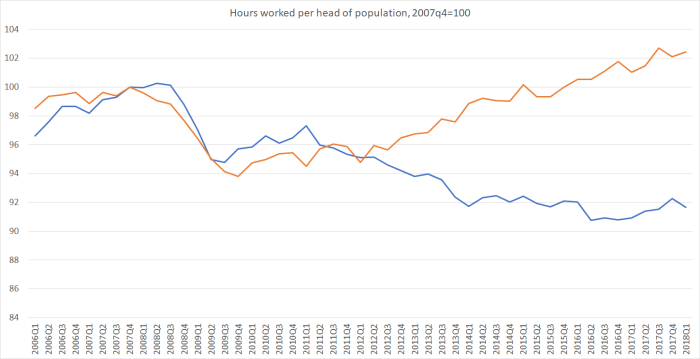

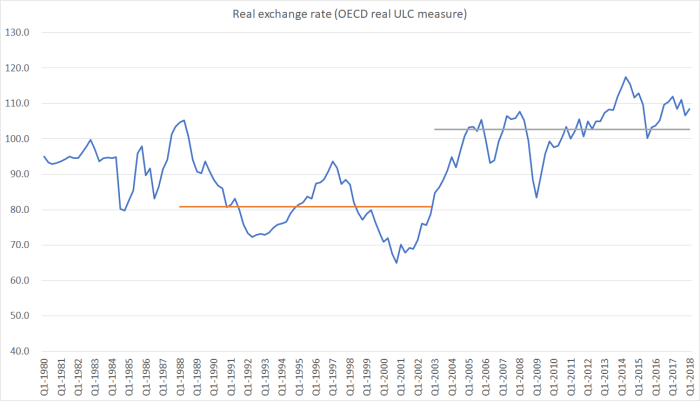

I presume (hope) the Minister believes what he says, but until he starts to confront the implications of charts like this he is unlikely to make any progress (except perhaps by chance)

With a real exchange rate now averaging 25 per cent higher than in the previous 15 years, in a country where productivity has dropped further behind, it shouldn’t be any surprise at all that foreign trade shares are falling, that the economy is increasingly skewed towards the non-tradables sector (where competition is often, and often of necessity) quite limited, or that firms don’t see the likely payoff to investing heavily in R&D. These are classic symptoms of a severely unbalanced economy. Most often they arise from misguided government choices. In our case, the biggest single misguided choice is the grim determination – or perhaps enthusiastic dream – to keep on rapidly driving up our population in such an isolated location where the opportunities to take on the world from here seem few – and all the fewer with such a severely out-of-line real exchange rate.

Really successful economies – ones with materially stronger productivity growth than their peers – tend to have strong, and rising, real exchange rates. But that strength is a consequence of success, an outcome of success, a way of spreading the gains. Driving up the real exchange rate has never been a part of successful strategy to lift the relative productivity performance of the economy. The reformers here in the 1980s recognised the importance of a sustained lower real exchange rate as part of a successful economic transition. It is tragic that today’s political and economic leaders seem to have almost completely lost sight of that.

We have – and will have – a 21st century economy. But the question is whether it will be a struggling upper middle economy, with hazy memories of glory days long gone, or one that once again matches many of the richer countries in the advanced world, something I’m pretty sure we could do, but for a small number of people. If the government really believes they have the answer for how they can do it with a population that they actively drive further up every year, they surely owe it to us to lay out their reasoning, their analysis, with much more specificity than the Minister of Finance has yet done. That might include explaining why their clever wheezes and proposed reforms will make the difference their predecessors also claim to have aspired to for decades now.

Then again, perhaps tangible achievement no longer matters. Under the government’s wellbeing approach perhaps warm feelings will substitute for world-leading incomes?