There are plenty of things I could comment on around the Reserve Bank Monetary Policy Statement released this morning:

- there was the questionable view that GDP growth is about to snap back (this very quarter) to above-potential rates,

- there was the welcome acknowledgement (departing from the Wheeler view) that changes in net migration tend to have larger (short-term) demand effects than supply effects,

- there was the Governor’s rather glib claim that they had looked back, reviewed their own past performance, and concluded that nothing should have been done differently. The Governor claimed they’d been at the lowest end of expectations etc, which while no doubt true about the major banks, certainly isn’t true if he’d checked out (say) the lower quartile responses to the bank’s own expectations survey. More starkly, the Bank – unlike anyone else – is paid to deliver core inflation near 2 per cent, and it has consistently failed for years now to do that. Some things should have been done differently. But I guess contrition is too much to hope for from public sector agencies.

But what disconcerted me most was the rather glib complacency that continues to flow from the mouths of senior Bank management about readiness for the next serious economic downturn, whenever it happens.

Brian Fallow asked them how well-placed they were to cope with such a downturn, given that the OCR is now at 1.75 per cent, whereas going into the previous recession it was at 8.25 per cent. The Governor claimed we were well-placed because we have a floating exchange rate, and suggested it had always been the key shock absorber in New Zealand. There is some truth in that observation, but it isn’t that relevant here: we’ve had a floating exchange rate for decades now, and in each downturn during that period cuts in short-term interest rates (the OCR since 1999) have been a significant part of responding to, and mitigating the severity of, any downturn. In fact, the exchange rate falls so sharply partly because of the size of the cuts in short-term interest rates. But in the next downturn it seems likely that the Reserve Bank won’t be able to cut the OCR by the 500 basis points or more that have been typical. On their own telling, they can only usefully cut it by about 250 basis points. That might enough in a mild downturn, but the focus of the question was (rightly) on the next serious downturn.

Then the Bank’s chief economist John McDermott chipped in. He reminded Fallow, and other listeners, of the Bulletin article the Bank had published a couple of months ago looking, in particular, at alternative monetary tools (eg QE) used in other countries. He went on to add that New Zealand also had “lots of fiscal headroom”.

I wrote about the Bulletin article in a post here. There was some good and useful material in the article, but as I noted then it was inadequate

they know how poorly the world economy coped with, and recovered from, the last downturn, even deploying all sorts of unconventional policies (fiscal and monetary) on top of the considerable conventional monetary policy leeway that existed going into that recession. Even here – where we never reached the limits of conventional policy – the output gap remained negative, and the unemployment rate above official estimates of the NAIRU for eight or nine years. Eight or nine years…….. That is just a huge amount of lost capacity, and of lives that are permanently blighted (prolonged involuntary spells of unemployment do that to people).

I’m at a loss to know how any serious people, who actually care about the consequences – for people’s lives among other things – can be so complacent. After all, as surely even the Bank senior management recognises (a) every OECD country (bar Japan) went into the last recession with more conventional monetary policy capacity than the Reserve Bank has now, and (b) the performance (even cyclical performance) of almost every OECD country in the last decade has been pretty deeply underwhelming, even with the combination of conventional monetary policy, unconventional monetary policy, and considerable fiscal stimulus in many cases.

Here, for example, are the OECD estimates of output and unemployment gaps for the OECD as a whole.

These are massive gaps, losses that will never be made up (in the sense that people only have one life – years unemployed aren’t usually made up for by more working years later in life). There is nice column in today’s Financial Times that reflects – with some anger – on this failing and the responsibility of central bankers, well-intentioned as they all, no doubt, were.

And yet Orr and McDermott seem unbothered about our situation if we were to be faced with a new serious recession.

Lets take the fiscal headroom strand of their argument. We certainly do have fairly low levels of government debt – not yet as they were in 2008, but towards the low end of OECD countries. Australia had low public debt in 2008 too, and is famed for its aggressive use of fiscal policy in the 2008/09 downturn. Between 2007 and 2009, the OECD’s estimate of the change in the structural primary fiscal balance (the bit, in principle, under discretionary government control) was equal about 5 percentage points of GDP (from a 1 per cent surplus to about a 4 per cent deficit).

But it isn’t as if Australia just used fiscal policy. The RBA cash rate was also cut by 425 basis points. Oh, and the exchange rate fell very sharply indeed – as one would have expected. Even with all that policy support – and some considerable Chinese fiscal/credit stimulus thrown in – Australia’s unemployment rate still rose by almost 2 per cent (and in the subsequent decade has never got close to the 2007 levels again).

I looked through the complete set of OECD countries for the period around the 2008/09 recession. Quite a number of them sought to use fiscal policy in a counter-cylical fashion in the last recession, but none did more (on this metric) than Australia. In fact, New Zealand – which didn’t do discretionary fiscal easing to counter the recession, but had had big fiscal loosenings in train anyway (which Treasury thought were quite sustainable), saw our structural primary balance widen almost as much as Australia’s did.

What I take from that experience is that it is very unlikely – no matter how much headroom New Zealand might appear to have – that a change in the structural fiscal position larger than Australia implemented in 2008/09 would prove politically tenable. Otherwise, surely, somewhere in the OECD – eg among those countries without a floating exchange rate, without Chinese stimulus – we’d have seen it happen. And even in Australia the peak fiscal stimulus didn’t last long, and debates about trying to get back to surplus consumed a fair degree of political oxygen over the following few years.

And, recall, we had that sort of fiscal stimulus in play ourselves over the 2008/09 period and even then, with big OCR cuts – more than any other country – and a falling exchange rate, we still ended up with a serious recession, and a very slow re-absorption of excess capacity. So the Reserve Bank’s complacency now is pretty alarming. We pay them to worry about contingencies and tail risks, not to blithely suggest everything is fine.

The other aspect of all this that the Reserve Bank has never openly engaged with is that, all else equal, the next downturn will be more troublesome for policymakers precisely because people increasingly recognise that conventional monetary policy is reaching its limits, and unconventional policy as others have applied it just isn’t that powerful. Going into the last recession, most people worked on the assumption that central banks would cut rates deeply and then the economy would rebound, and that there was no reason to think of medium-term inflation deviating far from target. Thus, while short-term interest rates fell sharply, implied longer-term nominal interest rates (eg implied 5 year rates five years forward). But when the next serious recession happens, there will inevitably be a great deal of questioning of just how much monetary policy can do. Inflation expectations – whether embedded in bond yields, or just in how firms and households behave – will be likely to fall away quite quickly. Central banks will need to cut nominal interest rates more aggressively just to avoid real interest rates rising. And most central banks don’t have much nominal interest rate space left. Rational fears of looming deflation are likely to be even more to the fore – and better-grounded – than they were in the years after 2008/09. It seems reckless not to be addressing these issues now.

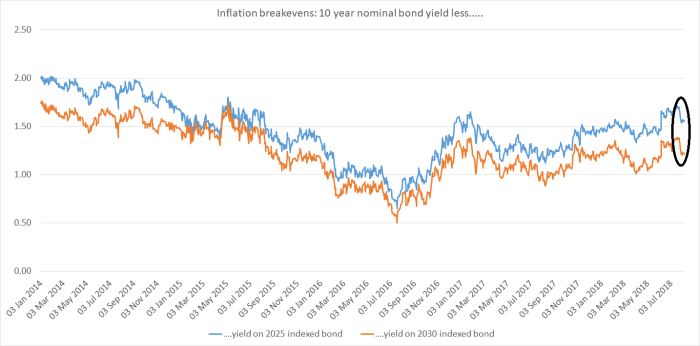

And for all that the Reserve Bank continues to repeat the line that current inflation expectations are just fine, the bond markets still don’t agree. If anything, inflation breakevens (a proxy for inflation expectations in reasonably settled times) have fallen back a bit in recent weeks.

The current average observation of the two series is about 1.4 per cent. It has now been 18 months since there was any sign of consistent progress in getting back to 2 per cent. But again, you never see the Reserve Bank engage with this indicator either. The narrative, after all, always seems to be that there is really nothing to worry about.

And it is ordinary working people, not senior central bankers, who will bear the brunt if things do go badly in the next recession, and central bank failure to act now contributes to those bad outcomes. Since politicians also tend to pay the price, one might hope the Minister of Finance would be taking the lead in requiring the Reserve Bank and Treasury to fully, and openly, address these issues. Ours, unfortunately, also seems too invested in a “nothing to worry about” narrative.

As I was typing this post, a reader sent me an email prompted by watching the Bank’s press conference

Larry Summers [former US Treasury Secretary, former President of Harvard etc] earlier this year gave a talk on ‘secular stagnation’ – how it is remarkable that so much monetary and fiscal support is now needed to keep economies afloat. What’s going on in NZ such that, at time when the terms of trade are so good, monetary policy you say is very stimulatory 1.75 ocr compared with 3.5 for neutral?) , and fiscal policy is stimulatory, and to become more stimulatory, yet the outlook for the economy and inflation, by any historical standard, is very subdued. What do you think the NZ economy would look like in a 2-3 year’s time if monetary and fiscal policy now were both returned to ‘neutral’? What’s going on?

It is a good question (although not sure I’d phrase the final main sentence that way). After all, for all that the Bank talks in the MPS of other countries starting to tighten monetary policy, outside the US – itself recipient of a big late-cycle fiscal stimulus – the changes are pretty patchy and small. And yet global inflation is pretty subdued, and (as the chart above shows) after all these years, output and unemployment gaps are only closing just now. I suspect part of the answer is that neutral nominal interest rates are lower than most people think, but that only pushes the question back one more step to ask why that would be. In part – but only a part – it will have reflected the failure to use monetary policy more aggressively soon enough. That’s clearly true here as well (and with less excuse here as those conventional limits – to cutting the OCR – simply weren’t reached here.

When you say above, “…that a change in the structural fiscal position larger than Australia implemented in 2008/09 would prove politically tenable.” Did you mean untenable?

LikeLike

Indeed. Thanks for spotting that.

Correction: sorry, I read your comment on the fly. Actually my wording was correct: “unlikely…….to be tenable” but with too many words in the middle.

LikeLike

It almost seems as if they are signalling in advance that they don’t intend to do their jobs properly.

Fiscal policy, with its murky politics and long lead times, should only be a last resort if the monetary authority has been incompetent. And the exchange rate, if it is to work well as an adjustment factor, depends a lot on the signalling and actions of the monetary authority.

LikeLike

I’ve read calls for stronger fiscal response via stronger automatic stabilizers from various orthodox economists in the last year…Blanchard I think was one. Also imf papers saying fiscal multipliers are much more positive than previously assumed…aka austerity and expansionary fiscal contraction is not correct response to a recession. Adair Turner talks about overt monetary finance aka Japan as a way forward. Governments will baulk at using fiscal stimulus if the narrative about austerity and responsibility is overegged and that’s why it’s important to not vilify government spending and deficits. We are all Keynesians in a foxhole ….As Lucas said I believe.

LikeLike

It is certainly true that fiscal multipliers will be larger when monetary policy has run out of capacity than in normal times (since in normal times, monetary policy would be adjusted to offset fiscal changes).

And automatic stabilisers should certainly be left to work, altho bear in mind that ours are weaker than those in many countries.

I have no particular problem with using countercyclical fiscal policy if the authorites (govt and RB) are so negligent as to get us into a recession without fixing the monetary policy tool. But they really should fix monetary policy, can enable interest rates to be cut (effectively) further below -0.75 per cent. That requires doing something about the convertibility (without limit) of RB banknotes.

LikeLike

[…] I recorded in a post the same day, the Governor and his offsiders responded with a degree of confidence that […]

LikeLike