At the end of yesterday’s post, I included a reader’s comment highlighting a recent lecture by prominent US economist (and former Treasury Secretary) Larry Summers in which, among other things, he posed the question of how it was that so much of the advanced world has had pretty underwhelming economic growth rates even with real interest rates so much lower than we had been used to (for several hundred years) and – at least in the US case – with such large fiscal deficits. Linked to this, he raised some of the sorts of concerns I’ve repeatedly raised here about the preparedness of authorities to cope with the next recession – as he notes, the recipe for dealing with recessions in the US has been 500 basis points of cuts in the Fed funds rate, and no one – including market prices – thinks that the US (or Japan or the ECB) is going to have that sort of capacity when the next recession comes.

At the time, I hadn’t gotten round to listening to that talk – to the New York Economic Club in May – or to another talk Summers had done about the same time to an ECB conference. But I did get round to doing so this morning. For those who, like me, prefer to read texts of addresses (a lot quicker), there aren’t transcripts unfortunately, but both talks are only about 20 minutes long (there is a long Q&A session in the first).

Both talks are worth listening to. I don’t find everything in them persuasive at all – he is, for example, a big fan of increased tax and government spending, and of much-increased government infrastructure spending (even as he recounts the extreme inefficiency of the way much US infrastructure spending is actually done). But he is a smart speaker, and the talks are not riddled with excessive amounts of jargon. And, even if our neutral interest rates are still higher than in most other places, we face some of the similar challenges. In particular, about coping with the next serious recession, whenever it comes.

And Summers reminded his listeners of stylised results that the probability of a recession in any one year (conditional on not already being in a recession or just emerged from it) seems to be about 20 per cent. Recessions are almost never recognised until far too late – again he reminded listeners of an Economist magazine exercise in looking at IMF forecasts: not once, in some 180 case of countries experiencing a year of negative GDP growth had the IMF forecast such an outcome 12-18 months in advance. Closer to home, in writing the other day about the Reserve Bank’s survey of expectations, I noticed that in the August 2008 survey, respondents (including many of the main forecasters) on average still didn’t see any sign of a recession.

Summers takes the view – hard for any serious person to contest – that the eventual recovery in the US after 2009 was very slow, unsatisfactorily so. On OECD estimates, only this year has the output gap closed, and last year the unemployment gap closed. Many other countries had at least as bad as experience: our own wasn’t much better. He argues more should have been done with fiscal policy, but perhaps the key point is that more needed to be done (on top of 500 basis points of interest rate cuts, several rounds of QE, other specific liquidity measures, and a significant fiscal stimulus). Next time round, there isn’t 500 basis points of conventional capacity.

We had 575 basis points of OCR cuts, a bigger swing in the structural fiscal position than in the US, bank guarantees, special liquidity provisions, and a big fall in the exchange rate. Despite that, we had years and years of excess capacity (whether on RB, Treasury, or OECD numbers) and core inflation still isn’t back to target. Next time, there isn’t 500 basis points of conventional capacity.

I’m less convinced that Summers has a solution to the problem. Structural reforms to lift potential growth would be good, but even if they happen they don’t deal with the natural cyclicality of the economy, take years to produce their full effect – and don’t seem remotely likely in today’s dysfunctional US political system.

On monetary policy, if I heard him correctly, he toys with the possibility of moving from an inflation target to something like a price level target or a nominal GDP target: both might have some merit, although both would be hard to make credible, especially for policymakers who have erred on the side of caution for the last decade. Perhaps his closest-to-specific advice was that if the inflation target is supposed to be symmetric (as both the US and NZ ones are), surely 9 years into a recovery, with unemployment at 4 per cent or just below (and pretty subdued productivity growth) if ever inflation should be a bit above 2 per cent it is probably now. The same could, almost certainly, be said for New Zealand (or, perhaps to a lesser extent, Australia). Such higher inflation outcomes would help hold up inflation expectations, and help induce a little more resilience (gains at the margin) in coping with the next serious recession.

Perhaps it isn’t his specific domain, but I was a bit surprised that Summers made no mention of actually addressing the fundamental administrative barrier that limits the ability of central banks to lower official short-term interest rates below about 0.75 per cent. If, as Summers does, you take seriously the view that low neutral rates will be with us for some time – he seems to see little in prospect (from savings behaviour or investment demand) to change that situation – then it should be untenable to keep in place the adminstrative restriction that allows people to move limitless amouts from interest-bearing accounts (potentially negative interest) at no substantial cost. One doesn’t have to call for the abolition of cash to believe this constraint can be very substantially alleviated (whether by capping the overall note issue, and auctioning new increments) or putting a conversion fee in place for significant transfers. If authorities – politicians and central banks – aren’t willing to address that issue, and soon, they really need to be thinking again about raising inflation (or price level or NGDP) targets, to allow more leeway in recessions. These issues have to be addressed now: to do so only in the middle of the next recession will undermine the effectiveness (including in stabilising expectations) of any change.

What staggers me is the apparent indifference of policymakers and politicians to these issues and risks. The experience of the last decade really should be fresh enough in everyone’s mind – and the awareness of the limitations of conventional policy at present – to create a sense of urgency about getting prepared. But there doesn’t seem to be such urgencty….in the euro-area, in the US, in the UK, in Japan, or in New Zealand. I touched yesterday on the rather glib complacent responses the Reserve Bank senior management gave at the press conference

I see that rather shortsighted attitude was carried over to the Bank’s FEC appearance (from Newsroom’s account).

Orr said that should this scenario [sustained weak growth] eventuate, the bank had a set of “unconventional tools” that it had been developing.

Assistant governor John McDermott spoke in May about five unconventional tools the bank had been working on that could be used during a financial crisis. One of these is quantitative easing, essentially the practice of printing money to buy bonds to stimulate the economy.

The bank would buy Government and commercial bonds as well as foreign government bonds, with the intention of weakening the Kiwi dollar.

Other approaches the bank could take include negative interest rates of as low as -0.75 percent, and guaranteeing bank liquidity by offering term lending facilities for banks.

But this scenario remains unlikely – it would effectively be a crisis occurring on top of an existing crisis.

Orr and McDermott know that even with all the quantitative easing and associated liquidity measures in other countries – that eventually reached the limits of conventional policy – the recoveries were very slow and painful almost everywhere. And if that final sentence is really to be read as them suggesting we can’t have a significant downturn now because somehow we are still in an “existing crisis”, they really aren’t fit to be doing their job. Nominal interest rates in New Zealand at present might be low at present by historical standards, but there is no credible sense in which the New Zealand economy has been in “crisis” in recent years.

In passing, one aspects of Summers’ talk I found unconvincing was his suggestion that despite the big apparent fall in neutral interest rates, the underlying fall is likely to have been much larger, masked – he claimed – by the effect of fiscal policy across much of the advanced world. He refers to both stock and flow measures. On stocks, government debt is certainly higher than it was in many/most advanced countries, but as this IMF chart highlights total debt in the advanced world as a whole total debt (public plus non-financial private) as a share of GDP is barely changed over 25 years, and is lower than it was going into the last recession.

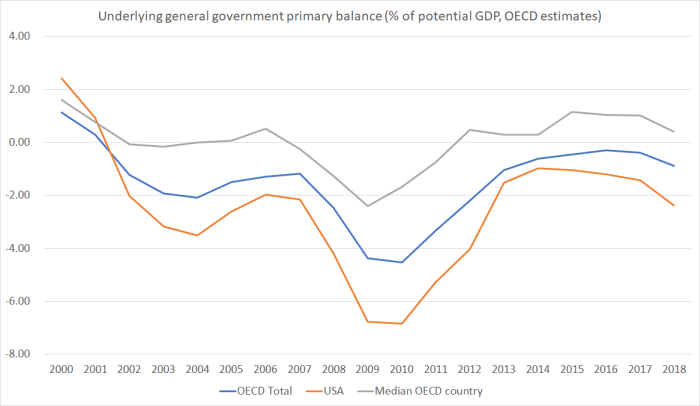

As for flow measures, here is a chart showing OECD estimates of the structural primary fiscal deficit (general government) for the OECD as a whole, median OECD country, and for the United States specifically (where deficits are widening again now).

Actually, the latest observations for all three series are no worse than they were in 2006 or 2007, just prior to the last recession. The median OECD country has been running a small primary surplus, and the average for the last five years is little different than for the five years prior to the recession. It is hard to see much compelling basis for the suggestion that fiscal policy is masking an ever deeper decline in the underlying neutral interest rates than what we (appear to) observe.

Anyway, for those interested in such issues, Summers is worth listening to and thinking about.

Interesting post. It made me wonder whether the very weak recovery from the last recession is in any way related to the (seemingly) huge gap opening up between the Joe Averages and the Have Lots, both in terms of people and businesses. If the average worker doesn’t have a lot of disposable income because of high rent/house prices or low wages they cannot contribute to economic growth through consumption. And if the highly-paid bank bosses (for example) are just squirreling their money away in tax havens and not creating new enterprises everybody loses.

LikeLiked by 1 person

Well put, Minsk — I share your thoughts. To me, this is a no-brainer!

LikeLike

It was an argument that was being run, esp in the US context. In principle, it might explain some of a fall in neutral interest rates, but even if so the central banks just need to cut nominal rates a bit further than otherwise.

Bear in mind that there hasn’t been a significant increase in inequality here for prob 25 years, at least if corrected for housing costs. Housing isn’t a small factor of course.

LikeLike

“Assistant governor John McDermott spoke in May about five unconventional tools the bank had been working on that could be used during a financial crisis. One of these is quantitative easing, essentially the practice of printing money to buy bonds to stimulate the economy.

The bank would buy Government and commercial bonds as well as foreign government bonds, with the intention of weakening the Kiwi dollar.”

Michael, please give us your opinion on the use of one other unconventional tool — “helicopter money” as espoused by Milton Friedman. Rather than — metaphorically speaking” — tossing money out of a helicopter, the unconventional tool would duplicate that used by the first Labour government in New Zealand in the 1930s, namely having the RBNZ create new money ex nihilo to lend at a low nominal rate (in effect zero because the government owns the RBNZ) for the government (either central or local) to spend on new infrastructure. This is what Canada did from the 1930s through ’til 1972 or thereabouts when it was persuaded by the BIS to desist.

LikeLike

Unsterilised govt purchases for govt goods and services is certainly a last-resort option. Bear in mind that with market interest rates near zero (or even below) the interest-free element wouldn’t be overly important.

Bear in mind that the Labour experiment didn’t end well – fx crisis at the end of 1938, and near-default on our external debt the following year. But that experiment was tried when the economy had already recovered, not at the depths of a recession/depression.

LikeLike

Well, that would deal with our persistently overvalued currency, would it not (without solving any of the underlying causes)?

LikeLike