I’ve run various posts over the last few years urging the authorities (Reserve Bank, Treasury, and the Minister of Finance) to get better prepared for the next serious recession (and lamenting the relative inaction on this front in other countries too, many of whom are worse-positioned than New Zealand is).

As a reminder, we went into the last recession with the OCR at 8.25 per cent, while the OCR now – years into a growth phase, with resources (on official assessments) fairly full-employed – is 1.75 per cent. In that last recession, the Reserve Bank cut interest rates a long way, the exchange rate fell a long way, there was really large fiscal stimulus cutting in as the recession deepened, and there were lots of other interventions (guarantee scheme, special liquidity provisions) and it was still as severe as any New Zealand recession for decades, and took years to fully recover from (on official output and unemployment gap estimates perhaps seven or eight years). Lives were blighted, in some cases permanently, in an event where there were no material constraints on the freedom of action of the New Zealand authorities. In fact, our Reserve Bank cut the OCR (over 2008/09) by more than any other advanced country central bank.

Next time, whenever it is, it seems very unlikely that the Reserve Bank will have that degree of freedom, particularly around monetary policy. On current policies and practices around bank notes, it seems unlikely that the OCR could be usefully cut below about -0.75 per cent. Beyond that point, most of the action would be in the form of people shifting from bank deposits etc to physical currency, rather than buffering the economic downturn.

Our Reserve Bank has long appeared disconcertingly complacent about this issue/risk. The latest example was comments by the new Governor and his longserving chief economist following the latest Monetary Policy Statement. They talk blithely about the unconventional policy options other countries have used, but never confront the fact that almost no advanced country could have been comfortable with the speed of the bounceback from the last recession. Output and unemployment gaps of eight or nine years (the OECD’s estimate for advanced countries as a whole) aren’t normal and shouldn’t be acceptable.

Quite why the Reserve Bank is so complacent is something one can debate. My hypothesis is that it is some mix of assuming we will never face the problem (recall that they have spent years hankering to get the OCR back up again) and of noting that other people/countries will most likely face the problem before New Zealand does. They also like to remind us that New Zealand has a floating exchange rate as if this somehow differentiates us (as a reminder so do Australia, Canada, Norway, Sweden, the US, the UK, Japan, Korea, Israel, and even the euro-area as a whole). Whatever the explanation, robust contingency planning, and building resilience into the system, is what we should be expecting from the Reserve Bank (and Treasury). There is no sign of it happening. Meanwhile, the Governor plays politics in areas (eg here and here) that really aren’t his responsibility.

In my post on Saturday, I touched again on the desirability of doing something – specific and early, consulted on and well-signalled – about removing the effective lower bound on nominal interest rates. That would tackle the issue at source. Monetary policy has been the primary stabilisation tool for decades for good reasons. Among other things, it is well-understood and there is a fair degree of (political and economic) consensus around the use of the tool. And confidence that the tool is at hand in turn proves (somewhat) self-stabilising, because people expect – and typically get – a strong monetary policy response.

Perhaps the other reason why authorities – perhaps especially in New Zealand – have been so complacent is the view that “never mind, if monetary policy is hamstrung there is always fiscal policy”. After all, by international standards, public debt here is low (on an internationally comparable measure from the OECD, general government net financial liabilities, about 1 per cent of GDP, which puts us in the lower quartile – less indebted – among OECD countries.)

The implicit view appears to be that, with such modest levels of debt, if and when there is another serious recession, New Zealand governments can simply spend (or cut taxes) “whatever it takes” to get economic activity back on course again. After all, the upper quartile of OECD countries have net general government liabilities in excess of 80 per cent of GDP.

I’m sceptical for a variety of reasons.

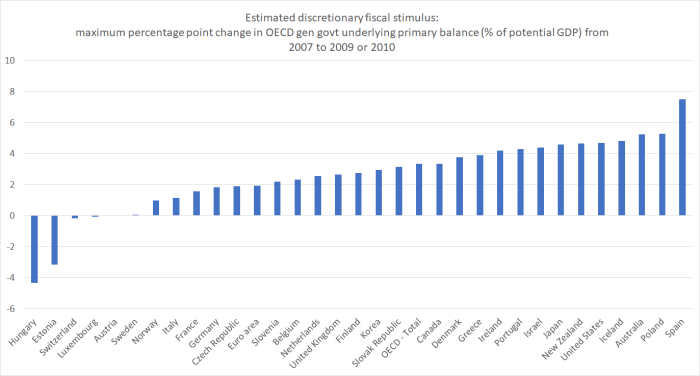

One of them is the experience of the last recession. For this, I had a look at the OECD data on the underlying general government primary balance as a per cent of potential GDP:

- general government = all levels of government

- underlying = cyclically-adjusted (ie removing the impact of the fluctuating business cycle on revenue (mostly), and adjusted for identified one-offs (eg recapitalisations of banking systems)

- primary balance = excluding financing costs, so that comparisons aren’t affected by changes in interest rates themselves

- as a per cent of potential GDP = so that a temporary collapse in actual GDP doesn’t muddy the comparison

The numbers aren’t perfect, and there are inevitable approximations, but they are the best cross-country data we have. Changes in this balance measure are a reasonable measure of discretionary fiscal policy.

Here is how those underlying primary balances changed from 2007 (just prior to the recession) over the following two or three years. I’ve taken the largest change I could find, and in every case that was over either two years to 2009, or over three years to 2010.

Some countries (Hungary, Estonia) were engaged in severe fiscal consolidation from the start. Several others experienced almost no change in their structural fiscal balances.

Quite a few countries saw 5 percentage point shifts in their underlying fiscal balances. Spain – a country with no control over its domestic interest rates – is recorded as having gone well beyond that. I don’t know much about the specifics of Spain, but for those who are upbeat about the potential scope of discretionary fiscal policy I’d take it with at least a pinch of salt – on the OECD numbers, the Spanish primary deficit dropped again quite sharply the next year (and Spanish unemployment didn’t peak until several years later).

Note that both Australia and New Zealand are towards the right-hand end of that chart. In Australia’s case, most of the movement resulted from deliberate counter-cyclical use of fiscal policy (the Kevin Rudd stimulus plans). In New Zealand, by contrast, the change in the underlying fiscal position was almost entirely the result of discretionary fiscal commitments made by Labour government at a time when Treasury official forecasts did not envisage a recession at all. From a narrow counter-cyclical perspective, those measure might have been fortuitous, but they were not deliberate discretionary counter-cyclical fiscal policy measures. In fact, at the time they were seen in some quarters as exacerbating pressure on the exchange rate, and limiting the scope of any interest rate reductions.

Perhaps it is worth stressing again that in not one of the OECD countries did the reduction in structural fiscal surpluses (expansion in deficits) last more than two years. In every single country, by 2011 structural fiscal policy (on this measure) had moved – sometimes modestly, sometimes quite sharply – into consolidation phase. In most countries, either conventional monetary policy limits had been reached or (as in individual euro area countries) there was no scope for conventional monetary policy. And it was to be years before output and unemployment gaps closed in most of these countries.

What is my point? Simply, that it looks as though the political limits of discretionary fiscal stimulus were reached quite quickly, even in countries where there was no market pressure (any of the established floating exchange rate countries other than Iceland), and even though the economic rebound in most was anaemic at best. That is why so many countries needed more conventional monetary capacity than in fact they had (and QE in various forms was not much of a substitute).

The OECD table on underlying primary balances only has data going back a few decades. No doubt experiences in wartime were rather different – in those circumstances huge shares of the nation’s resources can be marshalled and deployed in ways which (incidentially) stimuluate demand and activity. But looking across the OECD countries over several decades, I couldn’t any examples of discretionary fiscal policy being used as a counter-cyclical tool materially more aggressively than happened over 2008 to 2010. In Japan, for example, the structural fiscal balance worsened by about 6 percentage points over seven years after 1989.

So from revealed behaviour patterns, I’m sceptical as to just how much practical capacity there is for fiscal policy to do much, and for long, in the next serious recession, even in modestly-indebted New Zealand. The limits aren’t technical – they mostly weren’t last time – but political. Perhaps people will push back and run some argument along the lines of “oh, but we’ve learnt the lessons of unnecessary premature austerity last time round”. To which my response would be along the lines of “show me some evidence, or reason to believe that things would, or even should, be much different next time”. When – outside wartime – has it ever happened? And what about our political systems makes you comfortable that it is likely to happen next time? We could probably run large structural deficits for a year or two, but pretty quickly the pressure is likely to mount to begin reining things back in again (especially if, for example, the next recession is accompanied by heavy mark-to-market losses on government investments – eg NZSF).

And recall that here in New Zealand we had almost as much fiscal stimulus last time as any country, and even supported by huge cuts in interest rates (and without a home-grown financial crisis), we had a nasty recession (even a double-dip in 2010) from which it took ages to recover.

And all of this is without even examining how effective realistic fiscal policy is likely to be. The easiest fiscal stimulus is a tax cut (or even a lump sum cash handout). You can do clever ones, like the UK temporary cut in GST, which not only put more money in people’s pockets, but actively encouraged them to shift consumption forward – only to then create problems as the deadline for raising the value-added tax rate loomed. But putting money in people’s pocket – in a recession, and often explicitly temporarily – doesn’t guarantee they spend much of it. The most effective demand-stimulating fiscal policy (supply side measures are another issue – but lets just agree that deep cuts in company tax and related rates will not happen in the depths of a recession) is direct government purchases of goods and services. Most talked of is government capital expenditure, infrastructure and all that.

But, approve or otherwise, no government has a reserve list of projects, designed and consented, just waiting to get starting the moment it is apparent the next deep recession in upon us (that moment usually being several months after the recession has begun). It is almost certainly politically untenable for them to do so – if the project is so good, so the argument will run, why not do it when times are good? And so realistic government fiscal stimulus through the capital expenditure side will take months and years (more probably the latter) to even begin to get underway. Faced with the actual physical destruction in Christchurch, look how long it took for major reconstruction to get underway.

What of income tax cuts? Either the cuts are focused on those who pay the most taxes (in which case there is quickly one form of political pushback) or perhaps they take the form of a tax credit paid as a lump sum to everyone (in which case there is likely to be pushback of another political type – ideas around “everyone becoming a welfare beneficiary). I’m not attempting to defend either type of response, just to anticipate the risks.

By contrast, monetary policy – the OCR – can be adjusted almost immediately, and often begins to have an effect before the central bank even announces its formal decision (market expectations and all that). And if monetary policy changes don’t affect everyone equally, they affect the entire country – a borrower/saver/exporter in Invercargill just as their counterparts in Auckland. In the line from a US Fed governor, monetary policy gets in “all the cracks” (although he was contrasting it with regulatory interventions). Government capital expenditure is, by its nature, very specific in location. There probably isn’t a natural backlog of major (useful) capital projects in Invercargill or Dunedin.

I’m not saying fiscal policy has no useful place in the stabilisation toolkit – although my prior is that it is better-oriented towards the medium-term, with the automatic stabilisers allowed to work fully – but that we should be very cautious about expecting that it is any sort of adequate substitute for monetary policy in the real world of politics, distrust of governments and so on, in which we actually dwell. It is well past time for the Reserve Bank and the Treasury, led by the Minister of Finance, to be taking open steps towards ensuring that New Zealand has the conventional monetary policy capacity it would need in any new serious recession.